|

市场调查报告书

商品编码

1690088

汽车预测技术:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Automotive Predictive Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

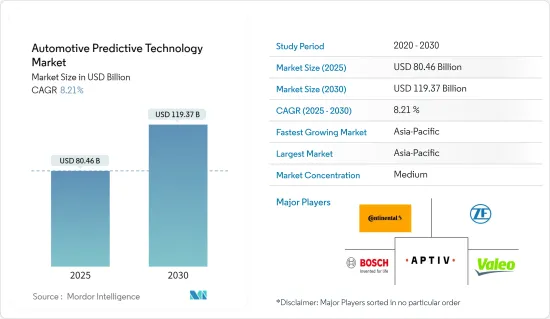

2025 年汽车预测技术市场规模预估为 804.6 亿美元,预计到 2030 年将达到 1,193.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.21%。

新冠疫情为汽车预测技术市场带来沉重打击。全球各地汽车和零件生产工厂的暂时关闭,导致供应链严重中断。然而,汽车行业正在显示出復苏的迹象,预计在预测期内将继续保持这一趋势。

市场对汽车先进技术特性的需求不断增长,从而推动了市场的发展。人工智慧和机器学习等技术创新正在增强安全措施,尤其是透过 ADAS(高级驾驶辅助系统)。此外,人们对预测性维护的兴趣日益浓厚,希望以经济高效的方式减少车辆停机时间并提高性能。

预测能力在自动驾驶汽车和自动驾驶技术中发挥关键作用,可以提醒驾驶员注意障碍物和其他驾驶提示。各大原始OEM都在大力投资自动驾驶汽车的开发,这为市场参与者带来了光明的机会。

受印度、中国和日本豪华汽车需求激增的推动,亚太地区预计将引领汽车预测技术市场。此外,该地区对 ADAS 的日益采用预计将在未来几年推动对预测技术的需求。

汽车预测技术市场趋势

预计 ADAS 领域将在预测期内占据市场主导地位

近年来,汽车产业不断加强研发,以增强ADAS(高级驾驶辅助系统)。这种强化不仅完善了 ADAS 技术,而且还推动了对夜间行人侦测、车道偏离警告以及包括摄影机和雷达在内的各种感测器等系统的需求增加。这些技术正在迅速融入车辆中,汽车製造商正在积极推广这些先进功能以推动市场需求。

奥迪、宝马、戴姆勒和沃尔沃等汽车製造商已开始在其产品中加入夜间行人侦测系统。这些系统有两个目的:如果它们侦测到行人在车辆的速度阈值内,它们可以警告驾驶或自动煞车。此类创新凸显了当今车辆中日益普遍的不断发展的安全标准。

为了抢占更大的市场份额,许多领先的服务供应商正在大力投资尖端 ADAS 技术的研发。这一领域并非完全由产业巨头主导。许多新兴企业从这些大公司获得资金,以带来创新的理念和技术。成熟企业和新兴新兴企业之间的协同效应正在催化 ADAS 技术的快速进步。

鑑于不断的进步和投资,ADAS 领域有望引领汽车领域的预测技术市场。由于高度重视提高安全性、改善驾驶舒适度和遵守严格的监管标准,ADAS 的采用正在蓬勃发展,并将在未来几年巩固其作为市场领导者的地位。

亚太地区预计将占据主要市场占有率

预计亚太地区将成为预测期内成长最快的市场。需求激增主要归因于汽车的混合动力化和电气化,以及电动车产量的增加。印度、中国和日本等国家正逐步将预测技术纳入乘用车之中。然而,配备该技术的车辆价格高、基础设施不足和监管障碍等挑战限制了其应用。

在亚太地区,汽车製造商不仅采用预测技术,并将其推广到新产品中。例如

- 2024年1月,玉柴集团宣布成立广西低碳智慧动力传动系统研究院。该实验室将专注于预测控制技术与巨量资料的集成,以改善动力传动系统系统。重点关注智慧动力传动系统、新能源系统和高效内燃机。此外,我们正在探索利用甲醇、氢和氨等低碳和零碳燃料的动力传动系统。该实验室的预测控制技术旨在推动永续和智慧汽车解决方案的发展,提高性能并减少排放气体。

- 2023年5月,位于班加罗尔的大陆印度技术中心在开发适合印度道路的ADAS解决方案方面取得了显着进展。其创新的模组化ADAS可轻鬆适应不同的汽车平臺,确保广泛的兼容性。

这些发展标誌着亚太地区预测技术的快速成长,预计未来几年需求将会成长。

汽车预测技术产业概况

汽车预测技术市场由成熟企业和新兴企业主导,它们争夺市场占有率。该领域的主要波动包括大陆集团、采埃孚股份公司、罗伯特·博世、安波福集团和法雷奥集团。

最近的趋势证实了将先进的预测和人工智慧技术融入汽车的显着转变。此举不仅旨在提高安全性和效率,也凸显了该产业对创新和丰富用户体验的坚定承诺。透过伙伴关係并利用彼此的技术力,这些公司在汽车创新领域中占据重要地位。例如

- 2024 年 1 月,在 CES 2024 上,HERE Technologies 与博世和戴姆勒卡车股份公司合作发布了用于商用车的 ADAS(高级驾驶辅助系统)。该系统将 HERE 的 ADAS 地图与博世的 Electronic Horizon 软体结合,与戴姆勒卡车的预测动力传动系统控制 (PPC) 无缝整合。即时考虑道路复杂性、交通标誌和速度规定可提高驾驶员的舒适度并优化燃料和电池效率。

- 2024年1月,同样在CES 2024上,英飞凌和Aurora Labs推出了一款尖端的人工智慧驱动的汽车维护解决方案。该解决方案基于英飞凌的 TriCore AURIX TC4x 微控制器和 Aurora Labs 的代码行智慧 (LOCI) AI,旨在提高转向和煞车等关键汽车零件的可靠性和安全性,从而提高车辆的整体性能和安全性。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 联网汽车需求不断成长

- 资料分析和机器学习的进步

- 市场限制

- 安装和维护成本高

- 波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 车型

- 搭乘用车

- 商用车

- 最终用户

- 车队车主

- 保险公司

- 其他最终用户

- 按组件

- 软体

- 硬体

- ADAS

- 机载诊断

- 其他硬体

- 按应用

- 安全与保障

- 车辆维护

- 预测性智慧停车

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 巴西

- 墨西哥

- 阿拉伯聯合大公国

- 其他国家

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- Continental AG

- Aptiv PLC

- Garrett Motion Inc.

- Harman International Industries Incorporated

- Visteon Corporation

- ZF Friedrichshafen AG

- Valeo SA

- Robert Bosch GmbH

- Verizon

- Infineon Technologies AG

第七章 市场机会与未来趋势

- 与 ADAS(高级驾驶辅助系统)集成

The Automotive Predictive Technology Market size is estimated at USD 80.46 billion in 2025, and is expected to reach USD 119.37 billion by 2030, at a CAGR of 8.21% during the forecast period (2025-2030).

COVID-19's outbreak dealt a blow to the automotive predictive technology market. Temporary shutdowns of vehicle and component manufacturing facilities worldwide led to significant supply chain disruptions. Yet, the automotive industry has shown signs of recovery and is poised to continue this trend during the forecast period.

The market is being propelled by a rising demand for advanced technological features in vehicles. Innovations like artificial intelligence and machine learning are enhancing safety measures, notably through advanced driver-assistance systems (ADAS). Additionally, there's a focus on predictive maintenance, aiming to reduce vehicle downtime and boost performance in a cost-effective manner.

Predictive features play a crucial role in autonomous vehicles and self-driving technologies, alerting drivers to obstacles and other driving cues. Major OEMs are pouring investments into the development of autonomous vehicles, signaling promising opportunities for market players.

Asia-Pacific is set to lead the automotive predictive technology market, driven by a surging demand for luxury vehicles in India, China, and Japan. Furthermore, the rising adoption of ADAS in the region is anticipated to amplify the demand for predictive technologies in the coming years.

Automotive Predictive Technology Market Trends

ADAS Segment Likley to Dominate the Market During the Forecast Period

In recent years, the automobile industry has ramped up its R&D efforts to bolster Advanced Driver-Assistance Systems (ADAS). This intensified focus has not only refined ADAS technologies but also ignited a heightened demand for systems like night-time pedestrian detection, lane departure warnings, and an array of sensors including cameras and RADAR. These technologies are swiftly being embedded into vehicles, with automotive players actively pushing these advanced features to stimulate market demand.

Leading the charge, OEMs like Audi, BMW, Daimler, and Volvo have begun integrating night-time pedestrian detection systems into their offerings. These systems serve a dual purpose: they either alert the driver or autonomously engage the brakes when a pedestrian is detected within the vehicle's speed threshold. Such innovations underscore the evolving safety standards becoming commonplace in today's vehicles.

In a bid to capture a larger slice of the market, numerous major service providers are pouring substantial investments into R&D for cutting-edge ADAS technologies. This landscape isn't solely dominated by industry giants; a plethora of startups, often buoyed by funding from these major entities, are injecting fresh ideas and technologies. This synergy between established players and emerging startups is catalyzing swift progress in ADAS technology.

Given the relentless advancements and investments, the ADAS segment is poised to spearhead the predictive technology market within the automotive realm. With a concerted emphasis on bolstering safety, amplifying driving comfort, and adhering to rigorous regulatory standards, the adoption of ADAS is surging, solidifying its position as a market leader in the coming years.

Asia-Pacific Expected to Hold Significant Market Share

During the forecast period, the Asia-Pacific region is poised to emerge as the fastest-growing market. The surge in demand can be attributed primarily to the hybridization and electrification of vehicles, coupled with a rising production of electric vehicles. Nations such as India, China, and Japan are gradually embracing predictive technology in passenger cars. However, the adoption has been tempered by the higher price segment of these tech-equipped vehicles and challenges like inadequate infrastructure and regulatory hurdles.

In the Asia-Pacific, automobile manufacturers are not just adopting predictive technology but are also rolling out new products featuring it. For instance,

- In January 2024, Yuchai Group unveiled the Guangxi Low-carbon and Intelligent Powertrain Laboratory. The lab, spotlighting predictive control technology and the integration of big data, aims to refine powertrain systems. Its focus spans intelligent powertrains, new energy systems, and high-efficiency internal combustion engines. Moreover, it explores powertrains harnessing low- and zero-carbon fuels like methanol, hydrogen, and ammonia. The lab's predictive control technology is designed to enhance performance and curtail emissions, championing the cause of sustainable and intelligent automotive solutions.

- In May 2023, Bengaluru's Continental Technology Centre India made notable advancements in crafting ADAS solutions tailored for Indian roads. Their innovative modular ADAS can be effortlessly adapted across diverse vehicle platforms, ensuring broad compatibility.

These developments signal a burgeoning opportunity for predictive technology in the Asia-Pacific, with demand set to escalate in the coming years.

Automotive Predictive Technology Industry Overview

The automotive predictive technology market is witnessing a blend of established giants and emerging players, all competing for a slice of the market share. Key players making waves in this arena include Continental AG, ZF Friedrichshafen AG, Robert Bosch, Aptiv PLC, and Valeo SA.

Recent trends underscore a pronounced shift towards embedding advanced predictive and AI technologies in vehicles. This move not only aims to bolster safety and efficiency but also underscores the industry's unwavering commitment to innovation and an enriched user experience. By forging partnerships and tapping into each other's technological prowess, these companies are carving out a leading position in the automotive innovation landscape. For Instance,

- In January 2024, at CES 2024, HERE Technologies, in collaboration with Bosch and Daimler Truck AG, unveiled an advanced driver-assistance system (ADAS) tailored for commercial vehicles. This system marries HERE's ADAS Map with Bosch's Electronic Horizon software, seamlessly integrating into Daimler Truck's Predictive Powertrain Control (PPC). The results in enhanced driver comfort and optimized fuel and battery efficiency, all thanks to real-time considerations of road intricacies, traffic signs, and speed regulations.

- In January 2024, also at CES 2024, Infineon and Aurora Labs rolled out cutting-edge AI-driven automotive maintenance solutions. Harnessing Aurora Labs' Line-of-Code Intelligence (LOCI) AI on Infineon's TriCore AURIX TC4x microcontrollers, these solutions aim to bolster the reliability and safety of pivotal automotive components like steering and braking, thereby elevating overall vehicle performance and safety.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand For Connected Cars

- 4.1.2 Advancements In Data Analytics And Machine Learning

- 4.2 Market Restraints

- 4.2.1 High Implementation And Maintenance Costs

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.2 End-User

- 5.2.1 Fleet Owners

- 5.2.2 Insurers

- 5.2.3 Other End-Users

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Hardware

- 5.3.2.1 ADAS

- 5.3.2.2 On-board Diagnosis

- 5.3.2.3 Other Hardware Types

- 5.4 By Application

- 5.4.1 Safety & Security

- 5.4.2 Vehicle Maintenance

- 5.4.3 Predictive Smart Parking

- 5.4.4 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Continental AG

- 6.2.2 Aptiv PLC

- 6.2.3 Garrett Motion Inc.

- 6.2.4 Harman International Industries Incorporated

- 6.2.5 Visteon Corporation

- 6.2.6 ZF Friedrichshafen AG

- 6.2.7 Valeo SA

- 6.2.8 Robert Bosch GmbH

- 6.2.9 Verizon

- 6.2.10 Infineon Technologies AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration With Advanced Driver Assistance Systems (ADAS)

2025年全球汽车预测分析市场报告

2025年全球汽车预测分析市场报告 汽车预测性维护感测器市场机会、成长驱动因素、产业趋势分析及2025-2034年预测

汽车预测性维护感测器市场机会、成长驱动因素、产业趋势分析及2025-2034年预测 全球汽车预测分析市场规模、份额、行业分析报告(按组件、车辆类型、最终用户、应用和地区划分)、展望和预测(2025-2032 年)

全球汽车预测分析市场规模、份额、行业分析报告(按组件、车辆类型、最终用户、应用和地区划分)、展望和预测(2025-2032 年) 2032 年汽车技术市场预测:按组件、部署、车辆类型、技术、应用、最终用户和地区进行的全球分析

2032 年汽车技术市场预测:按组件、部署、车辆类型、技术、应用、最终用户和地区进行的全球分析 汽车预测性维护市场:2025-2032年全球预测(按组件、技术、车辆类型、部署类型、预测性维护软体交付类型、服务类型和最终用户划分)汽车预测分析市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

汽车预测性维护市场:2025-2032年全球预测(按组件、技术、车辆类型、部署类型、预测性维护软体交付类型、服务类型和最终用户划分)汽车预测分析市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球汽车诊断市场全球汽车预测技术市场全球汽车预测市场报告(2025年)

全球汽车诊断市场全球汽车预测技术市场全球汽车预测市场报告(2025年) 汽车预测分析市场规模、份额和趋势分析报告:按零件、应用、车辆类型、最终用途、地区和细分市场预测,2025 年至 2033 年

汽车预测分析市场规模、份额和趋势分析报告:按零件、应用、车辆类型、最终用途、地区和细分市场预测,2025 年至 2033 年