|

市场调查报告书

商品编码

1690693

欧洲 PCB:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe PCB - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

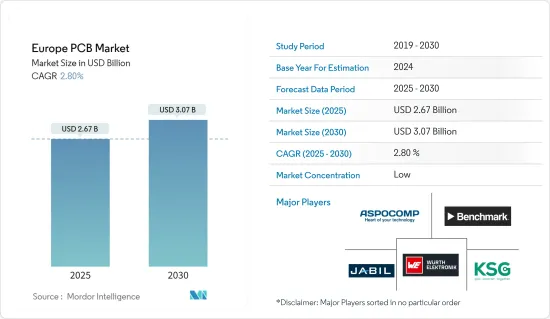

预计2025年欧洲 PCB 市场规模为 26.7 亿美元,到 2030 年将达到 30.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 2.8%。

主要亮点

- 联网汽车中 PCB 的采用正在加速市场的发展。这些车辆配备了有线和无线技术,方便与智慧型手机等运算设备的连接。这种技术可以让驾驶者解锁汽车、远端启动气候控制系统、检查电动车的电池状态,甚至使用智慧型手机追踪汽车。

- 电子元件的小型化使得可以製造随身携带的小型可携式和手持式计算设备成为可能。因此,市场上出现了更小、更轻且处理能力更强大的设备。电子元件变得越来越适合穿戴,因为它们可以轻鬆嵌入(例如在衣服或包包中)并且可以长时间携带。

- 近年来,欧洲PCB製造业在技术进步和产能扩张方面的投资不断增加。例如,2022 年 9 月,总部位于格尔德恩的 Unimicron Germany 公司投资 1,200 万欧元(1,289 万美元)用于新工厂和先进的高科技 PCB 製造流程。新建筑毗邻内层製造工厂,该工厂于 2018 年竣工,是欧洲最现代化的工厂之一。该公司表示,此项投资将有助于加强其在印刷基板技术和永续性的技术领先地位。

- 电子设备的小型化意味着将更多的电晶体节点封装到更小的积体电路中。然后将 IC 与所需的系统或设备连接,组装后,系统就能够执行其所需的功能。尺寸、重量和功率 (SWaP) 优化是电子製造领域的最新技术。无论是在航太、医疗、国防、 IT 和通讯或消费市场,当务之急是在不影响运算能力和效率的情况下实现产品小型化。

- 新冠肺炎疫情对该地区的经济产生了重大影响。包括电子製造业在内的许多终端用户产业都感到担忧。然而,在疫情过后,由于许多地区政府正在推动半导体产业的发展,市场将见证成长。

欧洲 PCB 市场趋势

柔性和刚挠性 PCB 的日益普及推动了市场

- 柔性和刚挠性 PCB(用于穿戴式电子产品、软性显示器和医疗应用)的日益普及预计将推动欧洲 PCB 市场的发展。

- 在欧洲,由于对穿戴式装置的需求不断增加以及健身活动的活性化,已经推出了多种产品。法国政府也为每个公民推出了国家数位平台,例如电子病人环境(ENS),以便医疗保健使用者和提供者能够安全、轻鬆地存取数位服务和资讯。

- 新《护理法》使得 ENS 的发展成为可能,它使公民能够存取所有护理资讯和服务(安全通讯、远端咨询、预约系统、连网穿戴设备等)。预计这将成为市场成长的驱动力。

- 整个欧洲对多层柔性 PCB 的需求正在增加。这些电路基板通常由单面和双面电路混合製成。本产品具有组装密度高、灵活性强、连接线束需求减少、尺寸紧凑、易于结合电阻控制功能等优点。此外,多层柔性PCB有望在包括航太工业在内的各个工业领域中广泛应用。许多公司正在积极采用新技术,以获得相对于竞争对手的竞争优势。

- 医疗应用不断寻找改善功能的方法。多层电路基板可以处理这种情况所需的所有控制功能。但此类应用程式需要更高的灵活性和便携性。设备变得越来越小,但越来越复杂。血糖值监测仪、心臟监测仪和静脉治疗输液帮浦等设备的各种包装标准会限制设备内可用于容纳必要电路的空间。

- 软硬复合PCB 是具有刚性和柔性部分的印刷电路基板,适用于各种应用。软硬复合板 (PCB) 因其高应力吸收能力和节省空间而已在汽车行业中得到应用。这些 PCB 比标准刚性 PCB 的使用寿命更长,并且在恶劣环境下更可靠。 PCB 常见于控制模组、液晶萤幕、娱乐和控制系统以及其他应用。

德国占据主要市场占有率

- 德国是汽车工业最突出的地区之一。半导体公司和汽车製造商正在积极投资新兴自动驾驶汽车的创新。政府的有利倡议是投资进一步推动市场的主要动力。

- 区域参与者也是国际参与者的主要供应商,从而增强了该地区的市场。例如,在疫情爆发之前,总部位于德国的欧洲科技公司Aixtron SE就收到了日本住友电工设备创新公司(SEDI)的订单,要求其订单8x6吋晶圆配置的AIX G5+工具,以扩大GaN-on-SiC(氮化镓-碳化硅)射频(RF)装置的生产能力。这些应用是无线的,包括雷达、卫星通讯和快速扩展的5G行动网路的基地台。

- 据KBA称,近年来,德国新电动车註册数量急剧增加。 2022年1月至11月,新註册电动车366,234辆。 2022年3月,电动车公司特斯拉在德国柏林附近的格兰海德开设了第一家欧洲工厂。该工厂的总产能为每年 50 万台,初始生产率为第 6 週每週 1,000 台,计划到 2022年终增加到每週 5,000 台。此类发展预计将进一步提振对 PCB 的需求,而 PCB 是电动车不可或缺的零件。

- 由于许多大型电力计划被搁置,国家电网需要帮助来适应可再生能源和分散式能源的崛起。同时,各国政府正努力使电网适应新的需求。四家国家电网营运商为提高输电能力所采取的措施总额达 500 亿欧元(536.9 亿美元)。因此,利用PLC累积资料并采取适当措施的用途可能会扩大,从而振兴PLC市场。

- 市场上有许多供应商提供专为 PCB 製造商设计的干膜图形化和阻焊成像灵活平台。例如,为 PCB 製造及相关市场提供直接成像 (DI) 系统的 Limata 推出了 X1000,这是一个灵活、经济高效的系统平台,用于干膜图形化和阻焊成像,专为具有短期生产配置的 PCB 製造商而设计。

欧洲 PCB 产业概况

欧洲印刷基板市场高度分散,主要参与者包括 Jabil Inc.、Aspocomp Group PLC、KSG GmbH、Benchmark Electronics Inc. 和 Wurth Elektronik Group(伍尔特集团)。该市场的竞争对手正在采取联盟、合併、投资和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2022 年 8 月 - Wurth Elektronik ICS 透过成立 Wurth Elektronik ICS Italia Srl 扩大在义大利的业务。但由于义大利的需求不断增长以及众多移动机械和商用车製造商的存在,该公司决定进一步扩大在欧洲的业务。

- 2022 年 6 月 - KSG 设计了一种创新的真空蚀刻模组,可最大限度地减少蚀刻过程中水坑的影响,从而尽可能提高效率。运输辊的最佳化放置也改善了製程化学品的流动特性。此外,采用单独喷嘴控制的间歇蚀刻可改善铜蚀刻,使基板顶部和底部的蚀刻图案更加均匀。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 典型的 PCB 製造工作流程

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 技术小型化需求不断成长,PCB 种类和密度不断增加

- 欧洲加大对 PCB 製造的研发与投资

- 柔性和刚柔结合 PCB 的采用日益增多(穿戴式电子产品、软性显示器、医疗应用)

- 市场限制

- 组件小型化导致复杂性增加

- 严格的监理合规要求

第六章 市场细分

- 按类别

- 标准多层 PCB

- 刚性 1-2 面 PCB

- HDI/微孔/积层

- 柔性 PCB

- 软硬复合板

- 其他类别

- 按行业

- 工业电子

- 航太和国防

- 消费性电子产品

- 通讯

- 车

- 医疗

- 其他行业

- 按国家

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲国家

第七章 竞争格局

- 公司简介

- Jabil Inc.

- Aspocomp Group PLC

- KSG GmbH

- Benchmark Electronics Inc.

- Wurth Elektronik Group(Wurth Group)

- LeitOn GmbH

- MicroCirtec Micro Circuit Technology GmbH

- Becker & Muller Schaltungsdruck GmbH

- AT&S Austria Technologies & Systemtechnik AG

- MEKTEC Europe GmbH(Nippon Mektron Ltd)

- Unimicron Technology Corporation

- Sumitomo Electric Industries Ltd(Sumitomo Corporation)

- ICAPE Group

- Elvia PCB Group

- Fujikura Ltd

- Multek Corporation

- NCAB Group

- Exception PCB Limited

- Lab Circuits

- Eurocircuits

- TTM Technologies Inc.

第八章 市场展望

The Europe PCB Market size is estimated at USD 2.67 billion in 2025, and is expected to reach USD 3.07 billion by 2030, at a CAGR of 2.8% during the forecast period (2025-2030).

Key Highlights

- PCBs adoption in connected vehicles accelerated the market. These vehicles have been fully equipped with both wired and wireless technologies, making it easy for them to connect to computing devices like smartphones. With such technology, drivers can unlock their vehicles, start climate control systems remotely, check their electric car's battery status, and track their vehicles using smartphones.

- Electronic components miniaturization made it possible to build small portable and handheld computing devices that can be carried anywhere. As a result, smaller and lighter devices having high processing capacity are available on the market. They are becoming more wearable since components can be easily embedded (for example: in clothing and bags) and carried for long periods.

- In recent years, the European PCB manufacturing sector is witnessing robust investments in technological advancements and capacity expansions. For instance, in September 2022, Unimicron Germany, headquartered in Geldern, committed EUR 12 million (USD 12.89 million) to a new facility and advanced high-tech PCB production processes. The new structure is adjacent to the inner layer manufacturing, which was completed in 2018 and is one of the most modern in Europe. According to the company, the investment will help it enhance its technological leadership in printed circuit board technology and sustainability.

- Miniaturization in electronic devices comprises fitting more transistor nodes on a smaller integrated circuit. The IC is then interfaced within its intended system or device so that, once assembled, the system can perform the desired function. Optimizing size, weight, and power (SWaP) is the latest technology in electronics manufacturing. Be it aerospace, medical, defense, telecommunications, or the consumer market, the need of the hour is a miniaturized product without compromising computing capability and efficiency.

- The COVID-19 pandemic had a significant impact on the region's economy. Many end-user industries were concerned, including those in electronics manufacturing. However, in the post-pandemic scenario, the market is witnessing growth due to many regional governments pushing the semiconductor industry.

Europe PCB Market Trends

Increasing Adoption of Flexible and Flex-Rigid PCBs to Drive the Market

- Increasing adoption of flexible and flex-rigid PCBs (wearable electronics, flexible displays, and medical applications) is expected to drive the European PCB market.

- Europe is undergoing multiple product launches due to the augmented demand for wearables and growing fitness activities. In addition, the Government of France is implementing national digital platforms, such as Electronic Patient Environment (ENS), for every citizen to facilitate safe and easy access to digital services and information for healthcare users and providers.

- ENS development was made possible with the new Care Act, where citizens can access all their care information and services (secure messaging, teleconsulting, the appointment system, and connected wearables, among others). It is expected to drive market growth.

- The need for multilayer flexible PCBs is increasing throughout Europe. These circuit boards are usually created by mixing single and double-sided circuits. The product includes several advantages: higher assembly density, increased flexibility, less requirement for the connecting wiring harness, smaller size, and more straightforward incorporation of impedance-controlled features. Further, as a result, multilayer flexible PCBs are expected to gain widespread adoption in various industrial sectors, including the aerospace industry. Multiple companies have been working tirelessly to introduce new technologies, giving competitors a competitive advantage.

- Medical applications are continuously looking for ways to improve their functionality. A multilayer circuit board can handle all of the necessary control functions in these cases. However, these applications require greater flexibility and portability. Devices are becoming smaller while becoming more complicated. The various packaging criteria for blood glucose monitors, heart monitors, and intravenous treatment infusion pumps can limit the space amount within the device for the essential circuitry.

- Rigid-flex PCBs have printed circuit boards with rigid and flexible parts, making them suitable for various applications. Because of their high stress-absorbing capability and space-saving properties, Rigid-Flex PCBs have been used by the automotive industry. These PCBs have a longer life than standard rigid PCBs and are more reliable even under harsh environments. PCBs are often found in control modules, LCD screens, entertainment and control systems, and other applications.

Germany Holds Major Market Share

- Germany is one of the prominent regions in the automotive industry. The semiconductor companies are actively investing in innovations for emerging autonomous vehicles in the country along with the automotive manufacturers. The favorable government initiatives majorly trigger the investments which further drive the market.

- The regional players are also key suppliers to foreign players, strengthening the region's market. For instance, before the pandemic, Aixtron SE, a German-based European technology company, received an order from the Japanese group Sumitomo Electric Device Innovations, Inc. (SEDI) for an AIX G5+ tool with an 8x6-inch wafer configuration to expand the production capacity of GaN-on-SiC (gallium nitride-on-silicon carbide) radio frequency (RF) devices. It is for wireless applications such as radars, satellite communication, and base stations for the rapidly expanding 5G mobile networks.

- According to KBA, the number of new electric vehicles registered in Germany increased dramatically in recent years. From January to November of 2022, 366,234 new electric cars were registered. In March 2022, the electric vehicle company Tesla opened its first European factory in Grunheide, near Berlin, Germany. At total capacity, the plant is expected to produce 500,000 cars annually, with initial plans to build 1,000 vehicles per week at the six-week mark, increasing to 5,000 per week by the end of 2022. Such developments will further propel the demand for PCBs as they form an essential component of Electric Vehicles.

- The electricity grid in the country needs help to cope with the extent of renewable and distributed energy in the country, and many major power projects are on hold. At the same time, the government endeavors to adapt the grid to the new demands placed upon it. The measures by the four national grid operators to boost power transmission capacity sufficiently add up to a cost of EUR 50 billion (USD 53.69 billion). It is likely to escalate the usage of PLC to accumulate data and further take successive measures, thereby fueling the PLC market.

- Many vendors in the market have flexible platforms for dry-film patterning and solder mask imaging designed for PCB manufacturers. For instance, Limata, a provider of Direct Imaging (DI) systems for PCB manufacturing and adjacent markets, introduced the X1000, a flexible, cost-efficient system platform for dry-film patterning and solder mask imaging designed for PCB manufacturers with quick turnaround production configurations.

Europe PCB Industry Overview

Europe's Printed Circuit Board Market is highly fragmented, with significant players like Jabil Inc., Aspocomp Group PLC, KSG GmbH, Benchmark Electronics Inc., and Wurth Elektronik Group (Wurth Group), among others. Players in the market are adopting strategies such as partnerships, mergers, investments, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- August 2022 - Wurth Elektronik ICS expanded its operations in Italy by establishing Wurth Elektronik ICS Italia Srl. However, the company decided to expand its presence further in Europe due to rising demand and many mobile machinery and commercial vehicle manufacturers in Italy.

- June 2022 - KSG designed an innovative vacuum etching module that minimizes the puddling effect during the etching process to make it as efficient as possible. The transport rollers' optimal placement also ensures improved run-off characteristics for the process chemistry. Furthermore, intermittent etching with individual nozzle control improves copper etching, resulting in a more uniform etching pattern on the top and bottom sides of the printed circuit board.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.3.1 Typical PCB Manufacturing Workflow

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising demand for miniaturization of technology and growth in diversity and density of PCBs

- 5.1.2 Increasing R&D and investments in PCB manufacturing in Europe

- 5.1.3 Increasing adoption of flexible and flex-rigid PCBs (Wearable electronics, Flexible displays and Medical applications)

- 5.2 Market Restraints

- 5.2.1 Increasing complexity due to miniaturization of components

- 5.2.2 Strict requirements to comply with legislations

6 MARKET SEGMENTATION

- 6.1 By Category

- 6.1.1 Standard Multilayer PCBs

- 6.1.2 Rigid 1-2-sided PCBs

- 6.1.3 HDI/Micro-via/Build-up

- 6.1.4 Flexible PCBs

- 6.1.5 Rigid Flex PCBs

- 6.1.6 Other Categories

- 6.2 By End-user Vertical

- 6.2.1 Industrial Electronics

- 6.2.2 Aerospace and Defense

- 6.2.3 Consumer Electronics

- 6.2.4 Communications

- 6.2.5 Automotive

- 6.2.6 Medical

- 6.2.7 Other End-user Verticals

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jabil Inc.

- 7.1.2 Aspocomp Group PLC

- 7.1.3 KSG GmbH

- 7.1.4 Benchmark Electronics Inc.

- 7.1.5 Wurth Elektronik Group (Wurth Group)

- 7.1.6 LeitOn GmbH

- 7.1.7 MicroCirtec Micro Circuit Technology GmbH

- 7.1.8 Becker & Muller Schaltungsdruck GmbH

- 7.1.9 AT&S Austria Technologies & Systemtechnik AG

- 7.1.10 MEKTEC Europe GmbH (Nippon Mektron Ltd)

- 7.1.11 Unimicron Technology Corporation

- 7.1.12 Sumitomo Electric Industries Ltd (Sumitomo Corporation)

- 7.1.13 ICAPE Group

- 7.1.14 Elvia PCB Group

- 7.1.15 Fujikura Ltd

- 7.1.16 Multek Corporation

- 7.1.17 NCAB Group

- 7.1.18 Exception PCB Limited

- 7.1.19 Lab Circuits

- 7.1.20 Eurocircuits

- 7.1.21 TTM Technologies Inc.

8 MARKET OUTLOOK

印刷电路板市场:产业趋势及全球预测(至 2035 年)-依 PCB 类型、材料类型、应用和地区划分

印刷电路板市场:产业趋势及全球预测(至 2035 年)-依 PCB 类型、材料类型、应用和地区划分 高频高速基板:2025-2031年全球市占率及排名、总营收及需求预测

高频高速基板:2025-2031年全球市占率及排名、总营收及需求预测 高密度互连PCB市场-全球产业规模、份额、趋势、机会和预测,以互连层数(单层HDI、双层或多层HDI和全层HDI)、应用、区域和竞争格局划分,2020-2030年预测

高密度互连PCB市场-全球产业规模、份额、趋势、机会和预测,以互连层数(单层HDI、双层或多层HDI和全层HDI)、应用、区域和竞争格局划分,2020-2030年预测 高密度互连 (HDI) 印刷基板市场按技术节点、应用和地区划分

高密度互连 (HDI) 印刷基板市场按技术节点、应用和地区划分 印刷基板(PCB)软体:全球市场份额和排名、总收入和需求预测(2025-2031年)

印刷基板(PCB)软体:全球市场份额和排名、总收入和需求预测(2025-2031年) 印刷基板市场:按类型、基板结构、材料、元件安装、层数、製造流程、应用、最终用途产业和销售管道- 全球预测 2025-2032

印刷基板市场:按类型、基板结构、材料、元件安装、层数、製造流程、应用、最终用途产业和销售管道- 全球预测 2025-2032 全球印刷基板市场:2034 年的机会与策略

全球印刷基板市场:2034 年的机会与策略 高频和 HDI PCB 全球市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终用户和功能HDI PCB市场(按技术节点、应用和地区)

高频和 HDI PCB 全球市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、流程、最终用户和功能HDI PCB市场(按技术节点、应用和地区) PCB标准多层薄膜的全球市场

PCB标准多层薄膜的全球市场