|

市场调查报告书

商品编码

1690698

欧洲屋顶瓦:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe Roofing Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

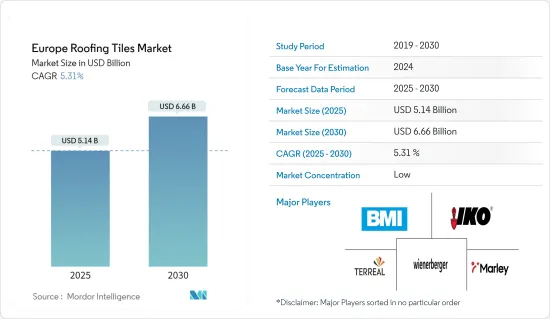

预计 2025 年欧洲屋顶瓦市场规模为 51.4 亿美元,预计到 2030 年将达到 66.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.31%。

2020 年 COVID-19 疫情爆发,导致全国封锁、製造活动和供应链中断以及全球生产停顿,对欧洲屋顶瓦市场产生了负面影响。不过,预计市场将在 2021 年至 2022 年间復苏,并在预测期内保持成长轨迹。

主要亮点

- 推动市场发展的关键因素包括建设产业的需求不断增长以及政府对绿建筑的政策。

- 屋顶瓦片往往比其他一些选择更贵,这可能会阻碍市场成长。此外,建设产业技术纯熟劳工的短缺也有望阻碍市场扩张。

- 然而,太阳能屋顶瓦的发展预计将为市场成长提供各种有利可图的机会。

- 在欧洲国家中,德国预计将凭藉其建筑业的成长主导区域市场。

欧洲屋顶瓦市场的趋势

住宅领域稳定成长

- 屋顶瓦片在住宅应用中越来越多地被使用,因为与沥青瓦屋顶相比,它们可以将传递到阁楼的热量减少近 70%。屋顶瓦片可用于各种住宅,包括独栋住宅、连栋住宅、公寓和公寓。由于住宅瓷砖的使用寿命较长,安装是最具成本效益的选择之一。

- 欧洲国家的强劲需求使得住宅建筑成为欧洲主要市场之一。英国政府表示,在拨出 100 亿英镑(127 亿美元)用于增加住宅供应的投资的帮助下,英国政府有望实现本届国会建造 100 万套住宅的宣言承诺。

- 2024年2月,政府支持的贷款基金获得30亿英镑(38亿美元)注资,用于在英国各地建造2万套新的经济适用住宅,帮助更多人获得住宅。

- 根据欧盟委员会声明,法国政府宣布了「住宅优先」计画(Le Logement D'abord)下的免税政策。该预算为80%的法国家庭提供住宅税的全面免除。对于剩余20%的富人,税率将从2021年起逐步降低,2023年住宅税将完全取消。

- 根据西班牙国家统计局 (INE) 的数据,2019 年至 2025 年期间,净住宅建设预计以平均每年约 135,000 套的速度增长。因此,预计住宅建设产业将在预测期的后半段显着成长。

- 上述趋势和事实表明,预测期内住宅领域对欧洲屋顶瓦片的需求强劲。

德国占据市场主导地位

- 德国经济是欧洲最大、世界五大经济体之一。德国也是欧洲住宅存量最大的国家,这显示德国在欧洲屋顶瓦需求方面占据主导地位。

- 根据联邦统计局(Destatis)的报告,2023年3月,德国批准建造24,500套住宅,与2022年3月相比减少了10,300份建筑许可(约29.6%)。

- 由于建筑价格大幅上涨,2022 年已完成建筑工程的价值与 2021 年相比下降了 4.8%。

- 根据德国之声报道,2023年至2025年间,德国新建住宅数量预计将下降32%。此外,预计2025年新建住宅将仅为20万套,而2022年将为29.5万套,可能导致住宅上涨。

- 德国住宅建设产业正在经历新订单大幅下滑、现有订单频繁取消的现象。例如,根据伊福经济研究所的调查,约有22%的德国企业回应称2023年10月的订单已被取消,约有48.7%的企业将在2023年10月遭遇新订单不足的困境,约有46.6%的企业将在2023年9月遭遇新订单不足的困境。

- 考虑到上述事实和数据,儘管德国住宅建筑业似乎正在萎缩,但预计德国在预测期内仍将保持其在欧洲屋顶瓦市场的主导地位。

欧洲屋瓦产业概况

欧洲屋顶瓦市场比较分散。受调查的市场中的主要企业(不分先后顺序)包括 Wienerberger AG、BMI Group、TERREAL、IKO Industries Ltd 和 Marley。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 政府对绿建筑的政策越来越有利

- 建设产业需求增加

- 限制因素

- 价格高于其他屋顶材料

- 建设产业技术纯熟劳工短缺

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 类型

- 黏土

- 混凝土的

- 其他类型

- 最终用户产业

- 住宅

- 商业的

- 基础设施

- 业/设施

- 地区

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 俄罗斯

- 北欧的

- 土耳其

- 其他欧洲国家

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)分析**/市占分析

- 主要企业策略

- 公司简介

- BMI Group

- Crown Roof Tiles

- Fornace Laterizi Vardanega Isidoro SRL

- IKO Industries Ltd

- INDUSTRIE COTTO POSSAGNO SpA

- Marley

- TERREAL

- Vortex Hydra SRL Italy

- Wienerberger AG

第七章 市场机会与未来趋势

- 太阳能屋顶瓦的开发

The Europe Roofing Tiles Market size is estimated at USD 5.14 billion in 2025, and is expected to reach USD 6.66 billion by 2030, at a CAGR of 5.31% during the forecast period (2025-2030).

In line with the COVID-19 outbreak in 2020, nationwide lockdowns around the globe, disruptions in manufacturing activities and supply chains, and production halts negatively impacted the European roof tiles market. However, the market recovered from 2021 to 2022 and is expected to continue its growth trajectory during the forecast period.

Key Highlights

- Besides, major factors driving the market studied include increasing demand from the construction industry and favorable government policies for green buildings.

- Roof tiles tend to be more expensive than a few other options, which is likely to hamper the market's growth. The lack of skilled workers in the construction industry is also anticipated to impede market expansion.

- Nevertheless, the development of solar roof tiles is expected to offer various lucrative opportunities for the market's growth.

- Among the European countries, Germany is expected to dominate the regional market due to the growth in its construction industry.

Europe Roofing Tiles Market Trends

Consistent Growth of the Residential Segment

- The usage of roofing tiles for residential applications is increasing because they can reduce the overall heat transfer into the attic by almost 70%, compared to an asphalt shingle roof. Roofing tiles are available for various residences, including single-family homes, townhomes, condominiums, and apartment buildings. The installation of roofing tiles in residential applications is one of the most cost-effective choices due to their long lifespan.

- Strong demand from various European countries makes residential construction one of the significant markets in Europe. According to the UK government, it is on track to meet its manifesto commitment to build 1 million homes in the current parliament with the support of the GBP 10 billion (USD 12.7 billion) investment allocated to boost housing supply.

- In February 2024, an increase of GBP 3 billion (USD 3.8 billion) was made in a government-backed loan fund to build 20,000 new affordable homes across the United Kingdom to help more people own a house.

- As per the European Commission, under its Housing First Plan (Le Logement D'abord), the French government announced tax waivers. Under the budget, the housing tax was entirely removed for 80% of French households. With regard to the remaining 20%, the country's wealthiest households, there was a gradual decrease in this tax rate from 2021, followed by a complete cessation of housing tax by 2023.

- According to Spain's National Statistics Institute (INE), the net household construction is anticipated to increase at an average pace of around 135,000 units every year from 2019 to 2025. Thus, the residential construction industry is expected to grow significantly over the latter period of the forecast period.

- The above-mentioned trends and facts indicate a strong demand for European roof tiles in the residential segment during the forecast period.

Germany to Dominate the Market

- The German economy is the largest in Europe and among the top five largest in the world. It also has the largest housing stock among European countries, which indicates its dominance over the demand for European roof tiles.

- According to the Federal Statistical Office (Destatis) report, in March 2023, the construction of 24,500 dwellings was permitted in Germany, a decrease of 10,300 (approx. 29.6%) in building permits compared with March 2022.

- The turnover in building completion work fell by 4.8% in 2022 compared to 2021 because of the substantial increase in construction prices.

- According to Deutsche Welle, Germany is expected to see a 32% drop in new housing construction between 2023 and 2025. Furthermore, it is estimated that only 200,000 homes will be completed in 2025 compared to 295,000 in 2022, which could lead to an increase in housing prices.

- Germany's residential construction industry has also witnessed new orders being considerably slower and existing orders being canceled much more frequently. For instance, according to the IFO Institute, around 22% of German companies witnessed orders getting canceled in October 2023, about 48.7% of companies also mentioned a lack of new orders in October 2023, and 46.6% mentioned the same in September 2023.

- Considering the above-mentioned facts and figures, even though the German housing construction industry seems to shrink, the country's dominance over the European roof tiles market is expected to be maintained during the forecast period.

Europe Roofing Tiles Industry Overview

The European roof tiles market is fragmented in nature. The major companies in the market studied (in no particular order) include Wienerberger AG, BMI Group, TERREAL, IKO Industries Ltd, and Marley.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increased Favorable Government Policies for Green Buildings

- 4.1.2 Increasing Demand from Construction Industry

- 4.2 Restraints

- 4.2.1 Higher Price Among Other Roofing Options

- 4.2.2 Lack of Skilled Workers in the Construction Sector

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Clay

- 5.1.2 Concrete

- 5.1.3 Other Types

- 5.2 End-user Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 Italy

- 5.3.4 France

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC

- 5.3.8 Turkey

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis **/ Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BMI Group

- 6.4.2 Crown Roof Tiles

- 6.4.3 Fornace Laterizi Vardanega Isidoro SRL

- 6.4.4 IKO Industries Ltd

- 6.4.5 INDUSTRIE COTTO POSSAGNO SpA

- 6.4.6 Marley

- 6.4.7 TERREAL

- 6.4.8 Vortex Hydra SRL Italy

- 6.4.9 Wienerberger AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Solar Roof Tiles