|

市场调查报告书

商品编码

1690744

美国託管服务业:市场占有率分析、行业趋势和成长预测(2025-2030 年)United States (US) Managed Services Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

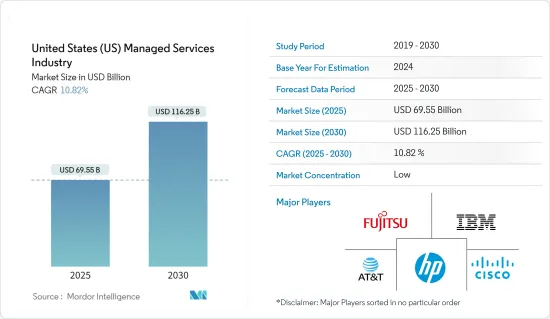

美国託管服务业预计将从 2025 年的 695.5 亿美元成长到 2030 年的 1,162.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.82%。

关键亮点

- 託管服务旨在透过将某些 IT 功能和流程外包给第三方供应商来提高业务效率并降低成本。这种方法提高了服务品质、业务效率和客户满意度,同时降低了成本。

- 根据市场研究,物联网 (IoT) 设备的激增正在推动对託管物联网服务的需求,并凸显了保护、监控和优化这些连接设备的需求。针对此, IT基础设施供应商正在共同合作开发物联网解决方案。

- 混合 IT 是内部部署基础架构和云端基础的解决方案的组合。物联网 (IoT) 的兴起迫使企业重新思考客户参与策略。託管服务供应商(MSP) 在加强安全性和确保物联网生态系统的强大保护方面发挥关键作用。

- 美国託管服务市场格局经常受到多种技术整合和行业法规遵守的挑战。企业必须遵循影响託管服务实施和营运的一系列标准和法律要求。

- 当新冠疫情和随后的停工首次爆发时,由于企业专注于生存并推迟了非必要的投资,需求暂时下降。这推迟了託管服务协议的推出。然而,远距工作的突然增加凸显了对安全性、云端迁移、协作工具和网路的需求,为託管服务供应商(MSP) 创造了产业成长机会。

美国託管服务业的趋势

云端运算将推动市场成长

- 云端基础的託管服务提供灵活性和可扩展性,并允许服务供应商远端存取、监控和解决其云端环境中的问题。此外,市场资料显示,人工智慧/机器学习、巨量资料分析、威胁情报和先进自动化平台等技术的采用正在推动向云端基础的服务的转变。市场参与企业正在根据行业趋势推出创新和协作服务。

- 例如,2023 年 11 月,全球网路安全供应商 SonicWall 收购了资安管理服务供应商 (MSP) Solutions Granted Inc. (SGI),后者为数百家託管服务供应商(MSP) 提供服务。此次收购加强了 SonicWall 对合作伙伴的承诺。扩展 SonicWall 的产品组合,包括美国的安全营运中心即服务 (SOCaaS)、託管检测和回应 (MDR) 以及其他针对 MSP 和 MSSP 的客製化託管服务。

- IT 和通讯部门在云端託管服务产业中占有重要份额。 2023财年,美国联邦政府已拨款约244亿美元用于主要联邦IT投资。云端託管服务在美国越来越受欢迎,因为它们能够简化 IT 营运、增强安全性并提供可扩展的解决方案,反映出稳定的市场成长率。

- 这些服务有助于云端基础设施的远端系统管理和维护,使企业能够专注于其核心目标,同时利用外部专业知识,从而促进行业成长。随着云端运算应用的激增,对託管服务的需求预计会增加,从而推动数位领域的创新和效率。

IT 和电讯是最大的终端用户产业

- 美国通讯业对资安管理服务的需求强劲,被公认为产业关键趋势之一。这主要是因为电信业者处理大量敏感资料,例如客户资讯和网路基础设施详细信息,使其成为网路攻击的理想目标。此外,通讯网路的复杂性和不断演变的网路威胁需要专业知识才能进行有效保护。

- 随着 5G 网路的出现,重点已转移到确保最终用户的安全性和高品质体验,通讯託管服务产业概览中强调了这一转变。根据VIAVISION统计,截至2023年4月,美国已有503个城市可以接入5G网络,比世界上任何其他国家都多,这要求美国必须从传统的以技术为中心的网络管理和优化方法发生重大转变。因此,对通讯管理服务的需求不断增加,以协助实现这一转变,从而促进市场的成长。

- 2023 年 7 月,领先的託管 IT、网路安全和云端解决方案供应商资料收购了总部位于德克萨斯州的安全託管服务供应商LevelSec。此次收购扩大了资料的全国影响力和行业专业知识,同时为 RevelSec 的客户提供了更广泛的资料服务。

- 根据市场报告,由于物联网、人工智慧和边缘运算等技术进步需要先进的网路基础设施,託管基础设施将占据相当大的市场占有率。託管服务在加速这些技术的采用方面发挥关键作用。

美国美国服务业概况

美国託管服务市场概况分为富士通、思科系统公司、IBM 公司、AT&T 公司和惠普公司等最大的公司,这些公司在市场上拥有强大的基本客群。这些公司总是提供越来越多的服务。随着公司采取强有力的竞争策略以在市场中生存并留住客户,市场竞争日益激烈。

- 2024 年 2 月 - Ubiquity 与富士通合作,增强最后一哩数位基础设施的弹性。 Ubiquity 将利用富士通的网路营运中心来支援其在美国四大主要市场的最后一哩光纤宽频基础设施。富士通在 Ubiquity 上列出了其位于德克萨斯州的运营商级 NOC 的全天候託管网路服务。

- 2024 年 1 月-思科宣布与日立子公司 Hitachi Vantara 合作推出新一代混合云端託管服务,Hitachi Vantara 专门从事资料储存、基础架构和混合云端管理。这些服务专门针对解决现代企业面临的持续资料管理挑战。该联合解决方案名为“日立 EverFlex 与思科混合云”,将自动化解决方案与预测分析结合。日立 EverFlex 与思科支援的混合云是自动化和预测分析的结合,旨在为企业提供面向未来的套件,以简化基础设施管理、最佳化成本并提高营运效率。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- COVID-19 工业影响评估

第五章市场动态

- 市场驱动因素

- 转向混合IT的转变日益加剧

- 提高成本和业务效率

- 市场问题

- 整合和监管问题、可靠性问题

第六章市场区隔

- 按部署

- 本地

- 云

- 按类型

- 託管资料中心

- 託管安全

- 託管通讯

- 主机网路

- 託管基础设施

- 託管行动性

- 按公司规模

- 中小型企业

- 大型企业

- 按行业

- BFSI

- 资讯科技/通讯

- 医疗保健

- 娱乐媒体

- 零售

- 製造业

- 政府

- 其他最终用户产业

第七章竞争格局

- 公司简介

- Fujitsu Limited

- Cisco Systems Inc.

- IBM Corporation

- AT& T Inc.

- HP Inc.

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Technologies Inc.

- Rackspace Technology Inc.

- Tata Consultancy Services Limited

- Citrix Systems Inc.

- Wipro Limited

第八章投资分析

第九章:市场的未来

The United States Managed Services Industry is expected to grow from USD 69.55 billion in 2025 to USD 116.25 billion by 2030, at a CAGR of 10.82% during the forecast period (2025-2030).

Key Highlights

- Managed services comprise outsourcing specific IT functions or processes to third-party providers, aiming to streamline operations and reduce costs. This approach enhances service quality, operational efficiency, and customer satisfaction while lowering expenses.

- Market research indicates that the soaring number of Internet of Things (IoT) devices has heightened the demand for managed IoT services, emphasizing the need to secure, monitor, and optimize these connected devices. In response, IT infrastructure providers are collaborating on IoT solutions.

- Hybrid IT combines on-premise infrastructure with cloud-based solutions. The rise of the Internet of Things (IoT) has prompted organizations to rethink their customer engagement strategies. Managed service providers (MSPs) play a crucial role in bolstering security within the IoT ecosystem, ensuring robust protection.

- Relatively speaking, managed services are known to be cost-effective and efficient, as compared to in-house services in the US, as they enable organizations to focus on their core competencies while outsourcing the non-core areas.In the US managed services market outlook, the integration of diverse technologies and adherence to industry regulations often pose challenges. Companies must navigate a web of standards and legal requirements, impacting the implementation and operation of managed services.

- The initial days of the COVID-19 pandemic and subsequent lockdowns caused a temporary dip in demand as businesses focused on survival and delayed non-essential investments. This led to a delay in implementing managed services contracts. However, the surge in remote work highlighted the need for security, cloud migration, collaboration tools, and networking, creating opportunities for industry growth among Managed Service Providers (MSPs).

United States (US) Managed Services Industry Trends

Cloud to Witness Significant Market Growth

- Cloud-based managed services offer flexibility and scalability, empowering service providers to remotely access, monitor, and resolve issues within the cloud environment. Furthermore, market data shows that the adoption of technologies like AI/ML, big data analytics, threat intelligence, and advanced automation platforms is propelling this transition to cloud-based services. Market players are launching innovative and collaborative services in response to industry trends.

- For example, in November 2023, SonicWall, a global cybersecurity provider, acquired Solutions Granted Inc. (SGI), a Managed Security Service Provider (MSSP) catering to hundreds of Managed Service Providers (MSPs). This acquisition bolsters SonicWall's commitment to its partners. It expands its portfolio to include US-based Security Operations Center services (SOCaaS), Managed Detection and Response (MDR), and other tailored managed services for MSPs and MSSPs.

- The IT and Telecom sector holds a significant market share in the cloud-managed services industry. For the 2023 fiscal year, the US federal government allocated around USD 24.4 billion for major federal IT investments, where cloud-managed services are gaining traction in the United States due to their ability to streamline IT operations, bolster security, and offer scalable solutions, thereby reflecting a steady market growth rate.

- These services facilitate remote management and maintenance of cloud infrastructure, which enables businesses to focus on their core objectives while leveraging external expertise, thereby fostering industry growth. The demand for managed services is set to rise as cloud adoption continues to surge, fostering innovation and efficiency in the digital realm.

IT and Telecom to be the Largest End-user Vertical

- The telecom industry in the United States has a strong demand for managed security services and is identified as one of the major significant industry trends. This is primarily due to the telecom companies' handling of vast volumes of sensitive data, including customer information and network infrastructure details, making them prime targets for cyberattacks. Additionally, the complexity of telecom networks and the evolving nature of cyber threats necessitate specialized expertise for effective protection.

- With the advent of 5G networks, the focus has shifted to ensuring end users' security and quality experiences, a shift highlighted in the industry overview of telecom-managed services. According to VIAVISION, as of April 2023, 5G network access was available in 503 United States cities, the most of any country globally, and this requires a significant shift in managing and optimizing networks, moving away from the traditional technology-centric approach. As a result, there is a rising demand for telecom-managed services to aid in this transition, contributing to market growth.

- In July 2023, Dataprise, a leading provider of managed IT, cybersecurity, and cloud solutions, acquired RevelSec, a Texas-based security managed service provider. This acquisition expands Dataprise's national presence and enhances its vertical expertise while providing RevelSec clients access to a broader range of services from Dataprise.

- According to the market report, managed infrastructure holds a significant market share, driven by innovations like IoT, AI, and edge computing, which necessitate advanced network infrastructure. Managed services play an important role in facilitating the adoption of these technologies.

United States (US) Managed Services Industry Overview

The United States managed services market overview is fragmented and is dominated by largest companies, such as Fujitsu Limited, Cisco Systems Inc., IBM Corporation, AT&T Inc., and HP Inc., among other companies that have a strong client base in the market. These players are constantly providing increased and enhanced offerings. Companies are employing powerful competitive strategies in order to survive in the market and retain their clients, thereby intensifying competitive rivalry in the market.

- February 2024 - Ubiquity partnered with Fujitsu to augment Last-Mile Digital Infrastructure Resilience. Ubiquity would utilize the Fujitsu Network Operations Center to support last-mile fiber broadband infrastructure in four major US markets. Fujitsu delivers Ubiquity with 24x7 managed network services from their carrier-class NOC in Texas.

- January 2024 - Cisco, in collaboration with Hitachi Vantara, the subsidiary of Hitachi Ltd specializing in data storage, infrastructure, and hybrid cloud management, unveiled Next-Gen hybrid cloud managed services. These services are specifically tailored to tackle the persistent data management hurdles faced by contemporary businesses. The joint solution, known as Hitachi EverFlex with Cisco Powered Hybrid Cloud, combines automation solutions and predictive analytics. It aims to equip organizations with a forward-looking toolkit for streamlined infrastructure management, cost optimization, and enhanced operational efficiency.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Shift to Hybrid IT

- 5.1.2 Improved Cost and Operational Efficiency

- 5.2 Market Challenges

- 5.2.1 Integration and Regulatory Issues and Reliability Concerns

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Managed Data Center

- 6.2.2 Managed Security

- 6.2.3 Managed Communications

- 6.2.4 Managed Network

- 6.2.5 Managed Infrastructure

- 6.2.6 Managed Mobility

- 6.3 By Enterprise Size

- 6.3.1 Small and Medium Enterprises

- 6.3.2 Large Enterprises

- 6.4 By End-user Vertical

- 6.4.1 BFSI

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare

- 6.4.4 Entertainment and Media

- 6.4.5 Retail

- 6.4.6 Manufacturing

- 6.4.7 Government

- 6.4.8 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Limited

- 7.1.2 Cisco Systems Inc.

- 7.1.3 IBM Corporation

- 7.1.4 AT&T Inc.

- 7.1.5 HP Inc.

- 7.1.6 Microsoft Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Dell Technologies Inc.

- 7.1.9 Rackspace Technology Inc.

- 7.1.10 Tata Consultancy Services Limited

- 7.1.11 Citrix Systems Inc.

- 7.1.12 Wipro Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测

管理服务的全球市场(~2035年):各服务形式,各部署类型,各类型企业,各产业类型,各地区,产业趋势,预测 2025年全球託管服务市场报告全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告

2025年全球託管服务市场报告全球託管通讯服务市场:2032 年预测 - 按服务类型、部署方式、组织规模、最终用户和地区进行分析2025年电信託管服务全球市场报告 託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型)

託管服务市场:2025-2030 年全球预测(按服务类型、合约类型、组织规模、最终用户和部署类型) 全球管理资讯服务市场全球託管基础设施服务市场

全球管理资讯服务市场全球託管基础设施服务市场 託管IT基础设施服务市场规模、份额、成长分析(按类型、最终用户、企业规模、服务类别和地区)- 产业预测,2025 年至 2032 年

託管IT基础设施服务市场规模、份额、成长分析(按类型、最终用户、企业规模、服务类别和地区)- 产业预测,2025 年至 2032 年 2025-2029年全球託管IT基础设施服务市场2032 年託管服务市场预测:按服务类型、组织规模、部署模式、最终用户和地区进行的全球分析

2025-2029年全球託管IT基础设施服务市场2032 年託管服务市场预测:按服务类型、组织规模、部署模式、最终用户和地区进行的全球分析