|

市场调查报告书

商品编码

1690765

南美航空燃料:市场占有率分析、产业趋势和成长预测(2025-2030 年)South America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

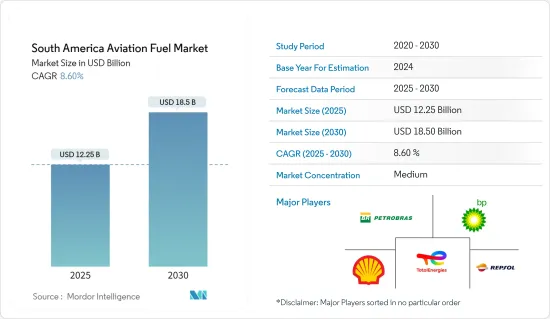

南美航空燃料市场规模预计在 2025 年为 122.5 亿美元,预计到 2030 年将达到 185 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.6%。

关键亮点

- 从中期来看,近期机票价格低廉导致的空中交通復苏、经济状况增强以及可支配收入增加是推动市场成长的一些主要因素。

- 另一方面,由于南美国家拥有大量基于石化燃料的航空燃料,导致环境恶化,未来几年市场可能面临障碍。

- 南美洲是生质燃料的主要地区之一。随着航空业继续向生质燃料转变,在不久的将来很可能会出现巨大的机会。

- 巴西是南美洲最大的航空燃料消费国,在该地区具有优势。由于市场的成长,预计巴西将在预测期内保持其主导地位。

南美洲航空燃料市场趋势

商业领域将经历显着成长

- 民航经营定期和非定期航空服务,并为客运和货运提供商业航空运输。在这一领域,私营部门是航空燃料的主要消费者之一,约占航空公司总营运支出的四分之一。

- 2022 年 12 月拉丁美洲和加勒比海地区 (LAC) 的总客运量为 3,230 万人次。同时,LATAM地区航空集团共运送乘客53,861人次。

- 巴西、巴拉圭和秘鲁等国家正在进行的机场私有化预计将有助于发展机场基础设施并增加容量,从而支持该地区的市场。

- 相反,该地区短程航班的比例明显增加,短程航班在空中交通中所占的比重也越来越大。廉价航空公司(LCC)和超低成本航空公司(ULCC)在拉丁美洲发展势头强劲。目前,该地区的廉价航空公司发展速度比以往任何时候都快,并显示出超越传统航空公司的迹象。

- 此外,2023 年 8 月,BP 航空在 LABACE 2023 上宣布,计划在巴西圣保罗州保利尼亚建立一个飞机燃料供应中心。该设施预计将于 2023 年开始运营,是该公司超过 1,000 万美元战略投资的一部分。该计划旨在提高物流灵活性并改善飞机运营商的燃料供应选择。

- 此外,Air bp 正在圣保罗孔戈尼亚斯机场开发一个新的燃料箱,目标是在 2024 年运作。这两个即将建成的设施代表着一项重大投资,并体现了 Air bp 致力于加强航空领域基础设施和服务的承诺。

- 因此,预计上述因素将在预测期内推动商业部门的成长。

巴西占市场主导地位

- 在南美洲,巴西是最大的航空燃料消费国。该国的航空指定产品包括航空煤油(QAV)、航空汽油和代用航空煤油(替代QAV)。

- 巴西民航市场规模庞大,根据巴西民航局报告,2022 年巴西民航航班数量达 831,000 架次,较与前一年同期比较增长 39%。根据西班牙航空运输协会2022年数据显示,其中国内航班73.1万架次,大幅增加33.7%;国际航班10万架次,大幅成长89%。

- 由于部分批次的化学检测结果不合格,巴西石油公司暂停进口航空燃料供应,影响了巴西的航空燃料销售。这一事态发展也导致 BR Distribuidora 和 Raizen 等主要燃料分销商暂停该产品的销售。不过,情况已有所好转,航空燃油销售已从影响中恢復。

- 此外,2023年10月,波音公司将在巴西正式开设工程技术中心,加入波音公司在全球的15个工程基地,透过尖端技术开发推动航太创新。波音公司也宣布与坎皮纳斯州立大学(Unicamp)合作提供资金支持,以扩大永续性的合作。此次扩展涉及 SAFMaps资料库第三阶段的开发,旨在了解巴西特定地区可持续航空燃料 (SAF) 生产最有前景的投入的可行性。

- 总体而言,由于政府措施可能进一步提振市场,巴西航空燃料市场预计在预测期内将实现良好成长。

南美洲航空燃料产业概况

南美航空燃料市场较为分散。主要企业(排名不分先后)包括 Petroleo Brasileiro SA、BP PLC、Shell PLC、TotalEnergies SE 和 Repsol SA。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概述

- 介绍

- 至2029年的市场规模及需求预测(单位:美元)

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 主角

- 近期机票价格低廉,导致航空旅客数量回升

- 人口可支配所得增加

- 限制因素

- 南美国家石化燃料航空燃料占比高

- 主角

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 燃料类型

- 空气涡轮燃料(ATF)

- 航空生质燃料

- 阿布古斯

- 应用

- 商用

- 防御

- 通用航空

- 地区

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Petroleo Brasileiro SA

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy SL

- Exxon Mobil Corporation

- Allied Aviation Services Inc.

- 市场排名/份额(%)分析

第七章 市场机会与未来趋势

- 航空生质燃料的日益普及

简介目录

Product Code: 71500

The South America Aviation Fuel Market size is estimated at USD 12.25 billion in 2025, and is expected to reach USD 18.50 billion by 2030, at a CAGR of 8.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the recovering number of air passengers, on account of cheaper airfare in recent times, more robust economic conditions, and increasing disposable income are among the major driving factors for the market.

- On the other hand, the market can face hurdles in the coming years due to the high share of fossil-fuel-based aviation fuels in South American countries, which are responsible for the degradation of the environment.

- Nevertheless, South America is one of the leading regions in biofuels. With an increasing shift towards aviation biofuels, significant opportunities are likely to be created in the near future.

- Brazil is the largest consumer of aviation fuels in South America, resulting in its dominance in the region. With the growing market, the nation is expected to continue its dominance during the forecast period.

South America Aviation Fuel Market Trends

The Commercial Sector to Witness a Significant Growth

- Commercial aviation involves the operation of both scheduled and non-scheduled aircraft, facilitating the commercial air transportation of passengers or cargo. Within this sector, the commercial segment stands out as one of the leading consumers of aviation fuel, constituting approximately a quarter of the total operating expenditure for airline operators.

- The total number of passengers transported in Latin America and the Caribbean (LAC) was 32.3 million in December 2022, which is the highest number of passengers. Meanwhile, the LATAM region had a total number of 53,861 passengers boarded by the airline group.

- The ongoing privatization of airports in countries like Brazil, Paraguay, and Peru is anticipated to contribute to the development of airport infrastructure and an increase in capacity, thereby providing support to the studied market in the region.

- Conversely, there has been a notable rise in the share of short-haul flights within the region, leading to an increased proportion of air traffic. In Latin America, the low-cost (LCC) and ultra-low-cost (ULCC) movements are experiencing significant momentum. Currently, more than ever, low-cost carriers in the region are witnessing accelerated growth, outpacing legacy airlines in their ascent.

- Moreover, in August 2023, Air bp has revealed plans to establish an aircraft fuel supply hub in Paulinia, located in Brazil's Sao Paulo state, as announced during LABACE 2023. The facility, anticipated to commence operations in 2023, is part of the company's strategic investment exceeding USD 10 million. This initiative aims to enhance logistical flexibility and provide improved fuel supply options for aircraft operators.

- Additionally, Air bp is in the process of developing a new fuel tank farm at Sao Paulo Congonhas Airport, set to become operational in 2024. These two upcoming facilities signify a significant investment, demonstrating Air bp's commitment to bolstering infrastructure and services in the aviation sector.

- Thus, the factors mentioned above are expected to drive growth in the commercial segment during the forecast period.

Brazil to Dominate the Market

- In South America, Brazil holds the distinction of being the largest consumer of aviation fuels. The designated products for aircraft use in the country encompass aviation kerosene (QAV), aviation gasoline, and alternative aviation kerosene (alternative QAV).

- The commercial aviation market in Brazil is substantial, with 831,000 flights recorded in 2022, marking a notable 39% increase compared to the previous year, as reported by ANAC. Within this total, 731,000 flights were domestic, reflecting a significant uptick of 33.7%, while international flights accounted for 100,000, showcasing a remarkable 89% increase, according to the Anuario do Transporte Aereo 2022.

- The sales of aviation fuel in Brazil faced an impact from Petrobras' suspension of the supply of imported aviation fuel due to chemical test results from a specific batch, which raised potential concerns. This development also prompted major fuel distributors, including BR Distribuidora and Raizen, to temporarily halt the sale of the product. However, the situation has improved and sales of aviation fuel has recovered from that impact.

- Moreover, In October 2023, Boeing officially inaugurated its Engineering and Technology Center in Brazil, joining the roster of 15 Boeing engineering sites worldwide dedicated to advancing aerospace innovation through cutting-edge technology development. In collaboration with the State University of Campinas (Unicamp), Boeing has also disclosed financial support to expand their sustainability collaboration. This extension involves the development of the third phase of the SAFMaps database, aimed at comprehending the viability of the most promising inputs for Sustainable Aviation Fuel (SAF) production in specific regions of Brazil.

- Overall, the aviation fuel market for Brazil is expected to register decent growth during the forecast period, owing to the supporting government initiatives, which are likely to aid the market's growth further.

South America Aviation Fuel Industry Overview

The South American aviation fuel market is semi-fragmented. Some of the major companies (in no particular order) are Petroleo Brasileiro SA, BP PLC, Shell PLC, TotalEnergies SE, and Repsol SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Recovering Number of Air Passengers, on Account of the Cheaper Airfare in Recent Times

- 4.5.1.2 Increasing Disposable Income of Population

- 4.5.2 Restraints

- 4.5.2.1 High Share of Fossil-Fuel-Based Aviation Fuels in South American Countries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 AVGAS

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Defense

- 5.2.3 General Aviation

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Petroleo Brasileiro SA

- 6.3.2 Repsol SA

- 6.3.3 BP PLC

- 6.3.4 Shell PLC

- 6.3.5 TotalEnergies SE

- 6.3.6 Pan American Energy SL

- 6.3.7 Exxon Mobil Corporation

- 6.3.8 Allied Aviation Services Inc.

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Shift Towards Aviation Biofuels

02-2729-4219

+886-2-2729-4219

运输燃料市场:依燃料类型、来源、混合比例、最终用户和分销管道划分-2026-2032年全球市场预测航空燃料市场:2026-2032年全球市场预测(按燃料类型、混合比例、飞机类型、原料、添加剂、最终用户和分销管道划分)

运输燃料市场:依燃料类型、来源、混合比例、最终用户和分销管道划分-2026-2032年全球市场预测航空燃料市场:2026-2032年全球市场预测(按燃料类型、混合比例、飞机类型、原料、添加剂、最终用户和分销管道划分) 航空燃料市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球航空燃油终端市场规模、份额、趋势及成长分析报告(2026-2034)

航空燃料市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年全球航空燃油终端市场规模、份额、趋势及成长分析报告(2026-2034) 航空燃料市场报告:按燃料类型、飞机类型、最终用途和地区划分,2026-2034年

航空燃料市场报告:按燃料类型、飞机类型、最终用途和地区划分,2026-2034年 2026年全球航空燃料市场报告航空汽油(Avgas)市场规模、占有率、成长及全球产业分析:依终端用户和地区划分的洞察与预测(2026-2034)

2026年全球航空燃料市场报告航空汽油(Avgas)市场规模、占有率、成长及全球产业分析:依终端用户和地区划分的洞察与预测(2026-2034) 航空燃料市场-全球产业规模、份额、趋势、机会、预测:按燃料类型、应用、类型、地区和竞争格局划分,2021-2031年运输燃料市场-全球产业规模、份额、趋势、机会和预测:按燃料类型、最终用户、地区和竞争对手划分,2021-2031年

航空燃料市场-全球产业规模、份额、趋势、机会、预测:按燃料类型、应用、类型、地区和竞争格局划分,2021-2031年运输燃料市场-全球产业规模、份额、趋势、机会和预测:按燃料类型、最终用户、地区和竞争对手划分,2021-2031年 2026-2030年全球国防飞机航空燃料市场

2026-2030年全球国防飞机航空燃料市场

▼