|

市场调查报告书

商品编码

1690840

货柜运输-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Container Shipping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

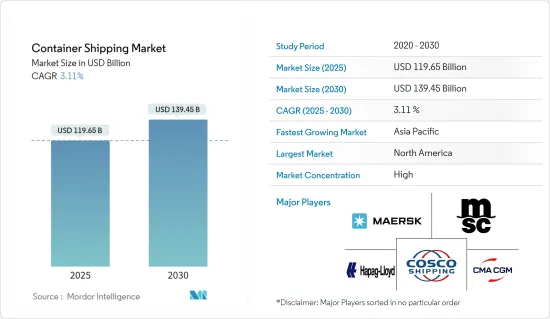

预计 2025 年货柜航运市场规模为 1,196.5 亿美元,到 2030 年将达到 1,394.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.11%。

关键亮点

- 全球货柜航运业可能正在应对红海的动盪局势。儘管如此,今年对大多数专家来说肯定是充满惊喜的一年。供应链专业人员正在策略性地重新规划贸易路线,并利用技术来增强韧性和创新能力。航运公司对产业成长持乐观态度,但仍保持谨慎,意识到地缘政治紧张等潜在干扰。

- 投资科技和规划位居投资趋势榜首,30%的受访者表示正在为此投入资金。即时可视性和追踪(24%)、协作和连接(27%)以及流程自动化(18%)也排名靠前。

- 交通量的成长得益于各种封锁措施的放鬆导致全球经济活动復苏、辅助包装推动部分地区商品消费势头强劲、库存重建导致电子商务强劲增长以及商业活动正常的季节性波动。

- 随着企业永续性目标的日益关注以及欧盟新出台的当地法规,永续性已成为许多托运人和运输业者在新的一年优先考虑的议题。

- 例如,根据欧盟的《碳边境调整机制》(CBAM)法律,所有欧盟进口商都必须报告与生产某些产品相关的碳排放。此外,自1月1日起,往返欧洲经济区(EEA)的航运公司必须遵守欧盟新的排放交易体系(ETS)法规,该法规已扩展到航运业。

- 许多航运业者已开始采取措施,实现更永续的航运,例如采用慢速航行以满足2023年国际海事组织温室气体战略等排放标准,或引入氨、甲醇和再生食用油等生质燃料。然而,欧盟的新要求可能会导致航运公司调整航班时刻表、征收额外费用并做出其他改变以实现永续性目标,这将不可避免地对托运人产生影响。

货柜船市场趋势

高柜货柜市场的兴起

- *高柜货柜有多种长度,包括 20 英尺和 40 英尺。高柜箱的主要特点是高度增加。高立方体货柜高 9 英尺 6 英寸,而标准货柜高 8 英尺 6 英寸。

- *任何需要垂直空间的地方都可使用高立方体容器。当运输因尺寸原因而不适合标准高度的货物时,或者当您想要有效地最大化货物数量时,这很有用。

- 高柜货柜整体普通货物(干货)。高柜整体用于运输普通货物(干货),但特别适合运输轻型、大量货物(高度可达 2.70 公尺)以及超重货物。

- 高箱货柜的主要优点是由于其高度(9 英尺 6 英寸),其立方体体积比标准货柜更大。这使得运输更大或更高的货物成为可能,为处理各种货物提供了灵活性。

- 货柜产量统计数据显示,几年前,干货货柜产量超过660万个,但未来几年,这一数字将下降到345万个标准箱。生产趋势仍在波动,预计产量将增加,主要原因是更换需求。新的高柜货柜的平均价格在 3,000 美元到 7,000 美元之间,而二手货柜的价格则在 1.50 美元到 5,000 美元之间,具体取决于尺寸。

亚太地区占市场主导地位

- 中国是全球商品供应国,几乎与所有国家都有贸易。一个国家的 GDP 很大程度上受到与其他国家贸易的影响。全球对中国商品(成品或原料)的需求很高。 2023年第一季,儘管面临国际市场阻力,但中国出口仍呈现明显復苏动能。

- 根据May Asia报道,中国3月出口年增14.8%,扭转了一段时间的下滑趋势。

- 根据最新发布的新华波罗的海国际航运中心发展指数,2023年全球航运中心城市前十名排名中,中国航运中心城市地位显着提升,舟山、香港、宁波、上海等城市均榜上有名,凸显了中国在全球航运领域日益增强的重要性。

- 日本是继中国和希腊之后亚洲第三大船舶持有国。包括日本在内的亚洲国家在货物处理性能方面处于领先地位,并拥有一些在效率和连接性方面排名世界前列的港口。

- 2023年4月至10月,印度所有主要港口的货物吞吐量为4.6398亿吨。去年4月至10月,印度主要港口的货物吞吐量为4.465亿吨。印度去年的商品出口额为 4,178 亿美元,比上年成长 40%。 23财年出口总额达4,474.6亿美元。政府推行了部分机械化,深化征兵,实施快速撤离措施,以提高业务效率。

- 在所有商品中,货柜是印度 2023-24 年 4 月至 5 月期间处理的最大货物,达 3,022 万吨,占总量的 22.6%。其次是POL原油(20.6%)、动力煤(15.1%)、其他大宗商品(8.2%)、铁矿石/球团(7.1%)、POL产品(6.7%)、其他煤炭(5.7%)、冶金煤(4.6%)、LPG/ LNG(1.8%)、钢铁(1.2%)、化学肥料(1.2%)、FRM干粉(1.1%)、食用油(1.1%)、其他矿石(1.0%)、FRM液体(0.9%)、水泥(0.4%)和糖(0.3%)。

货柜航运业概况

货柜航运市场本质上是细分的,有许多国际参与者。该领域的主要企业包括马士基、地中海航运、达飞、中远和赫伯罗特。由于全球海上贸易和工业化的成长,全球货柜运输市场预计将稳步成长。

海运货柜市场的成长受到船舶运输货物需求的增加和贸易相关协议的增加的推动。此外,运输和仓储成本的波动也会影响货柜市场的成长。预测期内市场的成长前景预计将受到航运自动化转型和海上安全标准提高等因素的推动。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

- 分析方法

- 研究阶段

第三章执行摘要

第四章 市场动态与洞察

- 当前市场状况

- 市场动态

- 驱动程式

- 国际贸易量增加

- 国家间贸易协定日益增多

- 限制因素

- 燃料价格上涨影响市场

- 贸易紧张局势加剧

- 机会

- 市场技术进步

- 不断扩大的世界贸易

- 驱动程式

- 价值链/供应链分析

- 行业法规政策

- 物流领域的技术发展

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响

- 市场最终用户洞察

第五章市场区隔

- 尺寸

- 小容器

- 大型容器

- 高柜

- 按类型

- 普通货柜运输

- 冷藏货柜运输

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 澳洲

- 印度

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 其他亚太地区

- 中东和非洲

- 埃及

- 卡达

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 哥伦比亚

- 南美洲其他地区

- 北美洲

第六章竞争格局

- 市场集中度概览

- 公司简介

- AP Moller-Maersk AS

- MSC Mediterranean Shipping Company SA

- CMA CGM

- China COSCO Holdings Company Limited

- Hapag-Lloyd

- ONE(Ocean Network Express)

- Evergreen Line

- Wan Hai Lines

- Zim

- SITC

- Zhonggu Logistics Corp.

- Antong Holdings(QASC)*

- 其他公司

第七章:市场的未来

第 8 章 附录

The Container Shipping Market size is estimated at USD 119.65 billion in 2025, and is expected to reach USD 139.45 billion by 2030, at a CAGR of 3.11% during the forecast period (2025-2030).

Key Highlights

- The global container shipping industry may be dealing with a volatile situation in the Red Sea. Still, this year should provide plenty of moments for most professionals in space. Supply chain professionals are strategically rethinking trade routes and embracing technology to foster resilience and innovation. While shipping companies are optimistic about the industry's growth, they remain vigilant, recognizing potential disruptions, such as geopolitical tensions.

- Investments in technology and planning are the top investment trend, with 30% of respondents saying that is where they spend money. Real-time visibility and tracking (24%), collaboration and connectivity (27%), and process automation (18%) also appeared on the list.

- The increase in volumes transported was due to the pick-up in global economic activity following the easing of various lockdown measures, the strong momentum in terms of the consumption of goods encouraged in some locations by support packages, strong e-commerce growth with inventory rebuilding, and the usual seasonal variation in business activity.

- A heightened focus on corporate sustainability goals and new regional regulations from the European Union (EU) puts sustainability at the top of mind for many shippers and carriers heading into this year.

- For example, under the EU's Carbon Border Adjustment Mechanism (CBAM) law, all EU importers need to report carbon emissions related to the production of certain products. Additionally, starting January 1, carriers shipping to, from, or within the European Economic Area (EEA) are subject to the EU's new Emission Trading System (ETS) regulations, which were expanded to include maritime shipping.

- Many ocean carriers have already made progress toward more sustainable shipping, including using slow steaming to meet emissions standards like the 2023 IMO GHG Strategy and introducing biofuels such as ammonia, methanol, and recycled cooking oil. However, the new requirements from the European Union may lead carriers to adjust schedules, implement surcharges, or make other changes to meet their sustainability goals, which would inevitably impact shippers.

Container Shipping Market Trends

Increasing high cube containers segment

- * High cube containers are available in various lengths, including 20-foot and 40-foot options. The key feature of high cube containers is the increased height. While a standard container is 8 feet 6 inches high, high cube containers are 9 feet 6 inches tall.

- * High cube containers are used when extra vertical space is needed. They are beneficial for transporting goods that may not fit within the standard height due to their dimensions or for maximizing cargo volume efficiently.

- High-cube containers are used for all types of general cargo (dry cargo). However, they are particularly suitable for transporting light, voluminous cargoes and overheight cargoes up to a maximum of 2.70 m tall.

- The primary advantage of high cube containers is their extra height (9 feet 6 inches), providing more cubic capacity than standard containers. This allows for transporting more significant or taller cargo, offering flexibility in handling various goods.

- Statistics on the production of containers show that a few years ago, more than 6.6 million dry freight containers were produced, which will drop to 3.45 million TEU in the next few years. The trend in production is still fluctuating, with expectations of an increase mainly driven by replacement needs. The average cost of a new high cube container can range from USD 3,000 to USD 7,000, while a used unit may be around USD 1,50 to USD 5,000, depending on the size.

Asia-Pacific dominating the market

- China is a global supplier of goods, trading with almost every nation. The GDP of the nation is significantly influenced by foreign commerce. Global demand for Chinese commodities (completed items or raw materials) is high. In the first quarter of 2023, China's exports showed a stunning recovery despite experiencing obstacles in international markets.

- According to May Asia, China's exports increased by an impressive 14.8% in March compared to the same month last year, marking a positive turn of events after a period of decline.

- In the top 10 global rankings for 2023, Chinese shipping center cities are notably represented, according to the most recent edition of the Xinhua-Baltic International Shipping Centre Development Index. Cities like Zhoushan, Hong Kong, Ningbo, and Shanghai were well-represented on this list, highlighting China's increasing importance in the global shipping sector.

- Japan is the third-largest ship-owning country in Asia after China and Greece. Asian countries, including Japan, lead in cargo handling performance and have several ports ranked among the top globally for efficiency and connectivity.

- All of India's major ports handled 463.98 million tons (MT) of cargo traffic between April and October of 2023. India's major ports handled 446.50 million tons (MT) of cargo traffic between April and October of the previous year. India exported USD 417.8 billion of goods a few years ago, a 40% increase from the prior year. Exports of goods totaled USD 447.46 billion in FY23. The government has implemented several mechanizations, deepened the draft, and implemented quick evacuation policies to increase operational efficiency.

- In April-May 2023-24, among all commodities, containers handled the highest cargo of 30.22 million tonnes in India, accounting for 22.6% of the total. Next in line were POL-crude (20.6%), thermal coal (15.1%), other commodities (8.2%), iron ore/pellets (7.1%), POL products (6.7%), other coal (5.7%), coking coal (4.6%), LPG/LNG (1.8%), iron & steel (1.2%), fertilizer (1.2%), FRM dry (1.1%), edible oil (1.1%), other ores (1.0%), FRM liquid (0.9%), cement (0.4%), and sugar (0.3%).

Container Shipping Industry Overview

The container shipping market is fragmented in nature, with the presence of many international companies. The top players in the segment include Maersk, MSC, CMA, COSCO, and Hapag Lloyd. Due to the increased seaborne trade and industrialization worldwide, the global shipping container market is expected to grow steadily.

The growth of the shipping container market is supported by increased demand for cargo transport via ships and a rise in trade-tied agreements. In addition, the growth of the shipping container market is affected by fluctuations in transportation and storage costs. Nevertheless, growth prospects for the market in the forecast period will be driven by factors such as a planned shift towards automation of shipping and increased safety standards at sea.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing volume of international trade

- 4.2.1.2 The rise of trade agreements between nations

- 4.2.2 Restraints

- 4.2.2.1 Surge in fuel costs affecting the market

- 4.2.2.2 Increasing trade tension

- 4.2.3 Opportunities

- 4.2.3.1 Technological advancements in the market

- 4.2.3.2 Expanding global trade

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Industry Policies and Regulations

- 4.5 Technological Developments in the Logistics Sector

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

- 4.8 Insights into End Users in the Market

5 MARKET SEGMENTATION

- 5.1 By Size

- 5.1.1 Small Containers

- 5.1.2 Large Containers

- 5.1.3 High Cube Containers

- 5.2 By Type

- 5.2.1 General Container Shipping

- 5.2.2 Reefer Container Shipping

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 Australia

- 5.3.3.4 India

- 5.3.3.5 Singapore

- 5.3.3.6 Malaysia

- 5.3.3.7 Indonesia

- 5.3.3.8 Thailand

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 Egypt

- 5.3.4.2 Qatar

- 5.3.4.3 Saudi Arabia

- 5.3.4.4 United Arab Emirates

- 5.3.4.5 South Africa

- 5.3.4.6 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Colombia

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 AP Moller-Maersk AS

- 6.2.2 MSC Mediterranean Shipping Company SA

- 6.2.3 CMA CGM

- 6.2.4 China COSCO Holdings Company Limited

- 6.2.5 Hapag-Lloyd

- 6.2.6 ONE (Ocean Network Express)

- 6.2.7 Evergreen Line

- 6.2.8 Wan Hai Lines

- 6.2.9 Zim

- 6.2.10 SITC

- 6.2.11 Zhonggu Logistics Corp.

- 6.2.12 Antong Holdings (QASC)*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

冷藏货柜:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

冷藏货柜:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 2025 年至 2033 年货柜运输市场报告(按产品、货柜尺寸(小型货柜、大型货柜、高箱货柜等)、应用和地区划分)

2025 年至 2033 年货柜运输市场报告(按产品、货柜尺寸(小型货柜、大型货柜、高箱货柜等)、应用和地区划分) 按货柜类型、材料类型、货柜尺寸、货柜所有者、应用和最终用户行业分類的货柜运输市场 - 2025-2032 年全球预测

按货柜类型、材料类型、货柜尺寸、货柜所有者、应用和最终用户行业分類的货柜运输市场 - 2025-2032 年全球预测 全球冷藏货柜运输市场

全球冷藏货柜运输市场 2025年全球货柜运输市场报告

2025年全球货柜运输市场报告 2032 年全球货柜航运市场预测:按类型、船舶大小、推进力、技术、应用、最终用户和地区划分

2032 年全球货柜航运市场预测:按类型、船舶大小、推进力、技术、应用、最终用户和地区划分 全球智慧航运货柜市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测2034 年货柜改装市场分析及预测:类型、产品、服务、技术、组件、应用、材料类型、流程、最终用户、安装类型全球40英尺货柜底盘市场

全球智慧航运货柜市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测2034 年货柜改装市场分析及预测:类型、产品、服务、技术、组件、应用、材料类型、流程、最终用户、安装类型全球40英尺货柜底盘市场 货柜运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

货柜运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)