|

市场调查报告书

商品编码

1690912

美国金属罐:市场占有率分析、行业趋势和成长预测(2025-2030 年)United States (US) Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

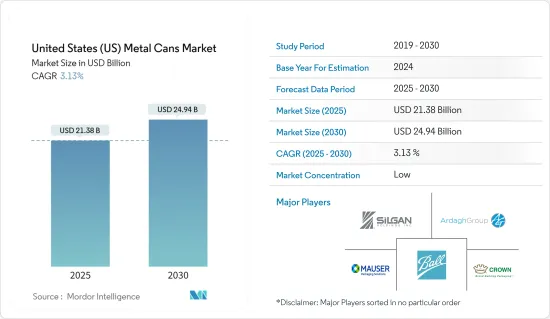

预计2025年美国金属罐市场规模为213.8亿美元,到2030年预计将达到249.4亿美元,预测期内(2025-2030年)的复合年增长率为3.13%。

关键亮点

- 金属罐越来越受欢迎是由于多种因素造成的,包括其永续性、耐用性和易用性,以及场外消费的增长和消费者对新形式(酒精和非酒精)、食品和气雾剂的偏好,而罐头是首选包装。

- 金属罐,尤其是铝罐,是全球回收最多的包装单元。铝罐在其生命週期结束时可以回收利用,且品质不会劣化,使其成为各行各业品牌的首选包装材料,优于塑胶和纸张等其他材料。在美国,每分钟有105,784个铝罐被回收,整体回收率约为50%,是所有饮料容器中回收率最高的。

- 预计到 2030 年,铝罐的需求将大幅增加,其中北美,尤其是美国,预计将对这一需求成长做出重大贡献。在美国,由于金属容器和包装的需求量庞大,纵向和横向的联盟不断形成。 2023 年 5 月,Manna Capital 与 Ball Corporation 合作,扩建其在美国的铝罐板製造和回收工厂。

- 金属罐用于宠物食品包装,在无塑胶宠物食品包装中发挥重要作用。美国对宠物食品的需求不断增加,推动了用于包装宠物食品的金属罐生产能力的提高。根据宠物永续发展联盟 (PSC) 于 2023 年 7 月发布的一项研究,光是在美国,宠物食品和零食产业每年就排放约 3 亿磅塑胶废弃物。这是一些加工商放弃塑胶包装、转而使用金属罐来生产宠物食品的关键因素。

- 金属罐包装面临其他包装解决方案的竞争。可用的替代包装解决方案包括塑胶、纸和玻璃。塑胶包装仍然是金属包装的主要竞争对手。食品和饮料行业是金属罐的主要用户,现在开始采用可回收塑胶包装解决方案。塑胶罐是透明的,这有助于品牌表明食品的品质。

- 此外,塑胶包装的逐渐增加也对市场构成了威胁。这主要是由于聚对苯二甲酸乙二醇酯(PET)等塑胶作为替代品的广泛使用。 PET 塑胶有可能取代食品和饮料领域的金属罐包装解决方案。

美国金属罐市场趋势

铝价确认成长

- 铝罐可以长时间保存食物,并提供几乎 100% 的防光、防氧、防湿气和其他污染物保护。这种材料具有防锈和防腐蚀的特性,是所有包装中保存期限最长的材料之一。铝罐在食品和饮料行业的使用日益增多,这是因为铝罐具有保护性、永续性优势和便利性。随着製造商和消费者都认识到铝包装的好处,预计这一趋势将会持续下去。

- 透过与罐体製造商合作开发新型铝製气雾罐合金,可以显着减轻罐体重量。这使得它更加永续性。全层运输包装也是如此,它在该领域应用越来越广泛,有利于物流和环境。

- 铝製气雾罐的市场占有率受到个人护理和汽车行业使用量的增加所推动。 100-250毫升的铝製气雾罐因其实用的包装选择而变得越来越广泛。其他细分市场(包括 251ml-500ml、100ml 以下和其他)在全球市场上获得了更好的收益。

- 与竞争包装类型相比,铝罐的回收率和再生利用率更高。据铝业协会称,铝罐是市场上回收最多的材料之一。 2022 年 4 月,鲍尔公司与 Recycle Aerosol LLC 合作,以提高美国铝製气雾罐的回收率。此次合作将促进气雾罐的回收利用,并建立一个将旧罐回收製成新气雾罐的封闭式环形回路系统。

- 根据铝业协会统计,铝业每年回收超过400亿个罐头。在美国,回收目前掩埋垃圾掩埋场的铝每年可节省 8 亿美元。

- 如今,铝製饮料罐已成为国内最可回收的饮料容器。美国罐头製造商协会 (CMI) 的饮料行业成员正致力于将美国铝回收率提高到新的水平。 CMI 发布了一份详细的入门指南和蓝图,说明如何实现 CMI 雄心勃勃的 2020-2021 年回收率目标。 CMI成员宣布的新的铝饮料回收率目标是,到2030年,美国的回收率达到70%,到2040年达到80%,到2050年达到90%。

非酒精饮料预计将成长

- 饮料业包括碳酸饮料、果汁、咖啡、茶等多种饮料。该公司的目标客户是那些偏好不断变化的、追求清爽、高偏好饮料的消费者。对健康和保健的关注正在推动消费者对更健康饮料的需求。这推动了对强化水、运动饮料、维生素和矿物质强化饮料以及益生菌等机能饮料的需求。消费者越来越关注糖的摄取量及其对健康和福祉的影响。因此,对无糖、天然和有机饮料的需求日益增长。饮料产业格局的不断发展是推动非酒精饮料罐市场成长的主要因素。

- 非酒精饮料领域的新产品推出对成长做出了重大贡献。例如,2023 年 1 月,百事可乐推出了碳酸柠檬莱姆软性饮料 Starry。它在美国零售店有两种口味:普通口味和零糖口味。碳酸饮料传统上都是罐装,百事公司推出的Starly为市场增添了另一种使用罐装包装的产品。这可能会导致对通常用于碳酸饮料的标准和超薄饮料罐的需求增加。

- 根据饮料业杂誌报道,红牛是2022年美国最大的机能饮料品牌,销售额约68.5亿美元。能量饮料(包括红牛)通常采用罐装,因为罐装方便、易于携带,并且能够保持产品的新鲜度和碳酸化。红牛销量的成长直接带动了作为该产品类型主要包装的饮料罐的需求成长。

- 据有机贸易协会称,美国有机饮料消费量预计将在 2022 年达到 25 亿美元,2025 年达到 28 亿美元。有机饮料通常包括有机果汁、茶和其他健康食品,并且通常采用符合有机和永续性原则的环保容器包装。

- 铝罐是有机饮料的理想选择,因为它们可回收并符合有机运动的永续性概念。随着消费的增长,作为有机饮料包装选择的罐头的需求也可能会增加。

美国金属罐市场概况

美国金属罐市场是一个竞争激烈的市场。由于消费者倾向于选择更具特色的品牌,品牌身份验证在市场上发挥重要作用。市场渗透率不断提高,大型企业在现有市场中占有一席之地,策略联盟进一步加剧了竞争。该市场也是该行业中占有较大份额的主要公司的所在地。由于金属罐製造商需要剥离大量高度专业的资产,退出市场的门槛很高,竞争对手之间的竞争可能会加剧。在该地区营运的主要企业包括 Crown Holdings Inc.、Ball Corporation、Silgan Holdings Inc.、Mauser Packaging Solutions(BwayHolding Corporation)和 Ardagh Metal Packaging SA(Ardagh Group SA)。

- 2023年9月,永续铝解决方案供应商Novelis宣布与北美Ball Corporation签署了一份主力客户协议。根据协议条款,Novelis 将向北美的球罐製造厂提供铝板。

- 2023 年 5 月,铝製饮料罐製造商 Ardagh Metal Packaging 和 Crown Holdings 宣布计划投资一项新的津贴计划,作为其持续支持在专门从事单流回收分类的资源回收设施内安装更多铝罐捕获设备的努力的一部分。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场动态

- 市场驱动因素

- 金属包装回收率高

- 罐装食品方便且成本低廉

- 市场限制

- 替代包装解决方案的可用性

第六章市场区隔

- 依材料类型

- 铝

- 钢

- 按罐型

- 食物

- 蔬菜

- 水果

- 宠物食品

- 汤

- 咖啡

- 其他的

- 气雾剂

- 化妆品和个人护理

- 家居用品

- 药品和动物用药品

- 油漆和清漆

- 汽车/工业

- 其他气溶胶

- 饮料

- 酒精饮料

- 非酒精饮料

- 食物

第七章竞争格局

- 公司简介

- Crown Holdings Inc.

- Ball Corporation

- Silgan Holdings Inc.

- Mauser Packaging Solutions(Bway Holding Corporation)

- Ardagh Metal Packaging SA(Ardagh Group SA)

- DS Containers

- CCL Container(CCL Industries Inc.)

- Independent Can Company

- Tecnocap Group

- CAN-PACK Group(Giorgi Global Holdings Inc.)

- Allstate Can Corporation

- Envases Group(ABA Packaging Corporation)

第八章投资分析

第九章:市场的未来

The United States Metal Cans Market size is estimated at USD 21.38 billion in 2025, and is expected to reach USD 24.94 billion by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Key Highlights

- The increasing popularity of metal cans can be attributed to various factors, including their sustainability, durability, and ease of use, as well as the increase in non-premise consumption and consumer preference for new formats (alcoholic and nonalcoholic), food and aerosol in which cans are the preferred packaging.

- Metal cans, especially aluminum, are the most recycled packaging units worldwide. They can be recycled at the end of their lifecycle without quality degradation, making them the preferred packaging material for brands across industries, ahead of other materials, such as plastic and paper. In the United States, 105,784 aluminum cans are recycled each minute, leading to an overall recycling rate of nearly 50%, the highest recycling rate for any beverage container.

- The demand for aluminum cans is expected to increase significantly by 2030, and North America, specifically the United States, is anticipated to contribute hugely to that demand growth. Several vertical and horizontal alignments are constantly taking place in the country owing to the immense demand for metal packaging. In May 2023, Manna Capital collaborated with Ball Corporation to expand the aluminum can sheet manufacturing and recycling facility in the United States.

- Metal cans are used for pet food packaging and have played a significant role in plastic-free pet food packaging. The increased demand for pet food in the United States is driving the increase in the production capacity of metal cans for pet food packaging. According to a Pet Sustainability Coalition (PSC) study published in July 2023, the pet food and treats industry generates an estimated 300 million pounds of plastic waste annually from the United States alone. This is a significant factor due to which some processors are moving away from plastic packaging and gravitating more toward metal cans for pet food.

- Metal cans packaging faces much competition from other packaging solutions. Alternatives such as plastic, paper, or glass packaging solutions are available. Plastic packaging continues to be the main competitor of metal packaging. The food and beverage industry, the primary user of metal cans, has started adopting recyclable plastic packaging solutions. Plastic cans are transparent, which helps brands to show their food's quality.

- Moreover, incremental enhancements in plastic packaging are posing a threat to the market. This can primarily be attributed to the popularity of plastics, such as polyethylene terephthalate (PET), as substitutes. PET plastics threaten to displace metal can packaging solutions in the food and beverage sector.

United States (US) Metal Cans Market Trends

Aluminum to Witness the Growth

- Aluminum cans offer long-term food quality preservation benefits and nearly 100% protection against light, oxygen, moisture, and other contaminants. The material is rust and corrosion-resistant, providing one of the most extended shelf lives considering any packaging. The rising application of aluminum cans in the food and beverage industry can be attributed to their protective properties, sustainability advantages, and convenience. This trend is expected to continue as both manufacturers and consumers recognize the benefits associated with aluminum packaging.

- Significant weight reductions are made possible by creating new alloys for aluminum aerosol cans, which are advanced in collaboration with slug manufacturers. This promotes even greater sustainability. The same applies to complete-layer transport packaging, which is utilized more frequently in the sector and benefits logistics and the environment.

- The aluminum aerosol can market share is driven by the increased usage of these cans in the personal care and automotive industries. Due to their practical packaging options, 100 to 250-ml aluminum aerosol cans are becoming more widely used. Other segments, including 251 ml to 500 ml, less than 100 ml, and others, are capturing better revenue in the global market.

- Aluminum cans have a higher recycling rate and more recycled content than competing package types. According to the Aluminum Association, it is one of the most recycled materials on the market. In April 2022, Ball Corporation partnered with Recycle Aerosol LLC to boost the recycling rates of aluminum aerosol cans in the United States. The collaboration would increase aerosol can recycling and establish a closed-loop system in which used cans are recycled into new aerosol cans.

- According to the Aluminum Association, the aluminum industry recycles more than 40 billion cans annually. The United States saves up to USD 800 million per year by recycling the amount of aluminum that goes into landfills presently.

- Recently, aluminum beverage cans have become the most recyclable beverage containers in the country. The beverage industry members of the Can Manufacturers Institute (CMI) are on a mission to raise US aluminum recycling rates to new levels. CMI published an in-depth primer and roadmap to explain how the CMI's ambitious 2020-2021 recycling rate targets were met. The new aluminum beverage recycling rate targets, announced by CMI members, aim to achieve 70% by 2030, 80% by 2040, and 90% recycling rates by 2050 in the United States.

Non-alcoholic Beverages to Witness Growth

- The beverage industry includes a variety of beverages, from carbonated soft drinks and juices to coffee and tea. It targets consumers with ever-changing tastes for refreshing and indulgent drinks. Health and wellness concerns are driving consumers to seek healthier beverages. This has increased the demand for functional drinks such as fortified water, sports drinks, vitamin and mineral-fortified beverages, and probiotics. Consumers are becoming increasingly aware of their sugar intake and its impact on their health and well-being. As a result, there is a growing need for sugar-free, natural, and organic drinks. The evolving landscape of the beverage industry has been a key driver for the growth of the non-alcoholic beverage cans market.

- New product launches in the non-alcoholic beverage sector have significantly contributed to the growth. For instance, in January 2023, PepsiCo launched Starry, a lemon and lime carbonated soft drink with a crisp and refreshing taste. The drink is available in Regular and Zero Sugar versions at United States retailers. Carbonated soft drinks are traditionally packaged in cans, and PepsiCo's introduction of Starry adds another product to the market that relies on cans for packaging. This can increase demand for standard and slimline beverage cans commonly used for carbonated beverages.

- According to the Beverage Industry Magazine, Red Bull was the United States' largest energy beverage brand in 2022, based on sales of about USD 6.85 billion. Energy drinks, including Red Bull, are typically packaged in cans due to their convenience, portability, and ability to preserve the product's freshness and carbonation. As Red Bull's sales grow, it directly contributes to an increased demand for beverage cans as the primary packaging choice for this product category.

- According to the Organic Trade Association, in 2022, the US consumption of organic beverages amounted to USD 2.5 billion and is forecasted to reach USD 2.8 billion by 2025. Organic drinks, which often include organic juices, teas, and other health-conscious options, are typically packaged in eco-friendly containers that align with organic and sustainable principles.

- Aluminum cans are a suitable choice for organic beverages because they are recyclable and align with the sustainability ethos of the organic movement. As consumption grows, the demand for cans as a packaging option for organic beverages may also increase.

United States (US) Metal Cans Market Overview

The US metal cans market is competitive in nature. Brand identity plays a significant role in the market due to the consumers' inclination toward a more well-identified brand. Market penetration is growing, with a strong presence of major players in established markets, and strategic partnerships are further intensifying the competition. The market also has significant players operating in the industry with higher shares. The barriers to exiting the market are high since metal can manufacturers require a significant divestment of quite specialized assets, which tends to intensify the competitive rivalry. Some of the key players operating in the region include Crown Holdings Inc., Ball Corporation, Silgan Holdings Inc., Mauser Packaging Solutions (BwayHolding Corporation), and Ardagh Metal Packaging SA (Ardagh Group SA).

- In September 2023, Novelis, a sustainable aluminum solutions provider, declared that it entered into an anchor customer agreement with Ball Corporation in North America. The agreement stipulates that Novelis will provide aluminum sheets to the Ball can manufacturing facilities in North America under the terms of the contract.

- In May 2023, Ardagh Metal Packaging and Crown Holdings, producers of aluminum beverage cans, announced their plans to invest in a new grant initiative as part of their ongoing support for initiatives to encourage the installation of further aluminum can capture equipment within material recovery facilities, which specialize in sorting single-stream recyclables.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price offered by Canned Food

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By Can Type

- 6.2.1 Food

- 6.2.1.1 Vegetables

- 6.2.1.2 Fruits

- 6.2.1.3 Pet Food

- 6.2.1.4 Soups

- 6.2.1.5 Coffee

- 6.2.1.6 Other Foods

- 6.2.2 Aerosols

- 6.2.2.1 Cosmetics and Personal Care

- 6.2.2.2 Household

- 6.2.2.3 Pharmaceutical/Veterinary

- 6.2.2.4 Paints and Varnishes

- 6.2.2.5 Automotive/Industrial

- 6.2.2.6 Other Aerosols

- 6.2.3 Beverages

- 6.2.3.1 Alcoholic Beverages

- 6.2.3.2 Non-alcoholic Beverages

- 6.2.1 Food

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 Ball Corporation

- 7.1.3 Silgan Holdings Inc.

- 7.1.4 Mauser Packaging Solutions (Bway Holding Corporation)

- 7.1.5 Ardagh Metal Packaging S.A. (Ardagh Group SA)

- 7.1.6 DS Containers

- 7.1.7 CCL Container (CCL Industries Inc.)

- 7.1.8 Independent Can Company

- 7.1.9 Tecnocap Group

- 7.1.10 CAN-PACK Group (Giorgi Global Holdings Inc.)

- 7.1.11 Allstate Can Corporation

- 7.1.12 Envases Group (ABA Packaging Corporation)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

金属罐市场-2025-2030年预测

金属罐市场-2025-2030年预测 金属罐、桶、鼓和罐市场按材质、产品类型、终端用户产业、产能和销售管道划分-2025-2032年全球预测金属罐和玻璃瓶市场(按包装类型、材料、封盖类型、产量、最终用户和分销管道)—2025-2032 年全球预测食品和饮料金属罐市场(按材料、类型、尺寸、罐体设计、材料特性、最终用途和分销管道)—2025-2032 年全球预测

金属罐、桶、鼓和罐市场按材质、产品类型、终端用户产业、产能和销售管道划分-2025-2032年全球预测金属罐和玻璃瓶市场(按包装类型、材料、封盖类型、产量、最终用户和分销管道)—2025-2032 年全球预测食品和饮料金属罐市场(按材料、类型、尺寸、罐体设计、材料特性、最终用途和分销管道)—2025-2032 年全球预测 全球金属桶市场一套三个金属罐的全球市场

全球金属桶市场一套三个金属罐的全球市场 全球金属罐市场:市场规模、份额、趋势分析(按产品、应用、封盖类型、材料和地区)、展望和预测(2025-2032 年)全球特种马口铁罐市场:2025-2030 年预测

全球金属罐市场:市场规模、份额、趋势分析(按产品、应用、封盖类型、材料和地区)、展望和预测(2025-2032 年)全球特种马口铁罐市场:2025-2030 年预测 2025年全球食品饮料金属罐市场报告

2025年全球食品饮料金属罐市场报告 食品饮料金属罐市场-全球产业规模、份额、趋势、机会和预测,按材料(铝罐、钢罐)、应用(食品、饮料)、地区和竞争细分,2020-2030 年预测

食品饮料金属罐市场-全球产业规模、份额、趋势、机会和预测,按材料(铝罐、钢罐)、应用(食品、饮料)、地区和竞争细分,2020-2030 年预测