|

市场调查报告书

商品编码

1690949

北美收缩和拉伸膜:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)North America Shrink And Stretch Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

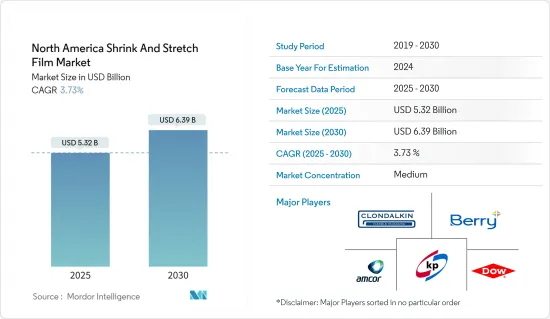

北美收缩和拉伸薄膜市场规模预计在 2025 年为 53.2 亿美元,预计到 2030 年将达到 63.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.73%。

主要亮点

- 收缩拉伸膜是采用先进製程生产的聚苯乙烯薄膜。这些薄膜用于包装应用,具有独特的化学性质,使其在柔韧性和拉伸性方面有所区别。拉伸膜是一种柔韧、可拉伸的薄聚乙烯薄膜,用于包裹托盘货物,而收缩膜是一种包裹单一产品或物品的薄膜,需要加热进行包装。这些薄膜可以防止因空气和湿气造成的腐败,从而提高包装商品的品质。

- 收缩套筒标籤是 360 度列印的标籤,通常会加热以符合要贴标产品的形状。收缩套筒标籤印刷在塑胶或聚酯薄膜材料的两面上。收缩套标的耐用性使其成为暴露在潮湿和磨损中的产品的理想选择。

- 随着品牌越来越关注 2025 年永续性目标,探索更多永续性选择对于实现这些承诺变得越来越重要。许多宝特瓶饮料製造商选择可回收的聚乙烯 (PE) 收缩膜而不是硬纸板或纸板。

- Amcor 表示,PE 收缩膜是美国回收率最高的塑胶薄膜之一,透过北美 18,000 个商店回收点进行收集。透过利用消费后回收 (PCR) 内容扩大您的循环经济努力,您可以获得额外的永续性效益,同时提供与标准 PE 收缩膜相同的多功能性和性能。

- 除了功能优势外,拉伸和收缩膜还具有物流优势。使用这些薄膜可以更容易处理和存放散装产品,大大提高仓库效率。同时,收缩包装的捆包紧凑且易于堆放,从而优化了储存设施和车辆的空间利用率。因此,公司可以节省成本并提高其供应链的整体业务效率。

北美收缩和拉伸膜市场趋势

食品饮料产业市场显着成长

- 拉伸膜主要由线型低密度聚乙烯(LLDPE) 製成,是北美食品和饮料行业的主要产品。它是堆迭的理想选择,可确保产品在运输过程中的安全,并防止因错位造成的潜在损坏。该薄膜以其良好的拉伸性和韧性而闻名,能够完美地适应各种形状和尺寸的产品,提供稳定性并隔绝灰尘和湿气等外部因素。

- 另一方面,收缩膜通常由聚烯或聚氯乙烯(PVC) 製成,具有不同但同样重要的用途。当施加热量时,收缩包装会收缩并紧密包裹产品,形成紧密的密封。这项特性使它们非常适合捆绑瓶子、罐子和盒子等物品,以便于处理和运输。此外,其防篡改密封对于维护产品完整性和增强消费者对食品和饮料行业的信心至关重要。

- 拉伸膜和收缩膜对于延长食品和饮料产品的保质期都至关重要。这些薄膜可作为抵御灰尘、湿气和微生物等污染物的保护屏障,有助于维持产品的新鲜度和品质。这些因素对于生鲜食品尤其重要,因为它们在储存和运输过程中需要严格的卫生和温度控制。透过延长保质期,这些薄膜不仅可以减少食物浪费,还可以确保消费者收到最佳状态的产品。

- 拉伸膜和收缩膜的另一个优点是它们可以增加产品的可见度,使其在货架上展示时更具吸引力。透明、有光泽的收缩膜可使包装的产品看起来更美观,这使得它在零售环境中特别受欢迎,因为视觉吸引力是消费者选择的主要驱动力。此外,製造商可以将品牌名称和产品详细资讯直接列印在薄膜上,从而减少了对额外标籤和包装材料的需求,并简化了包装流程。

- 根据美国人口普查局2023年12月的资料,美国食品和饮料机构的每月零售额达到约903亿美元,较上月增加7.4%。零售额的成长凸显了包装薄膜的需求不断增长,尤其是蔬菜、水果、鱼和肉的包装薄膜。

预计美国将主导市场

- 美国对收缩膜和拉伸膜的需求不断增长,主要是由于对仓储和配送过程中货物有效包装、捆绑和保护的需求不断增长。此外,该地区每年都会举办一项活动,强调消费产业对这些薄膜的强劲需求。

- 美国加工食品的消费量正在大幅增加,从而推动了对拉伸和收缩薄膜的需求。随着消费者越来越多地转向方便食品,高效的包装解决方案变得越来越重要。收缩膜的需求量特别大,因为它有助于黏合和保护冷冻食品、零食包装、已烹调产品等。

- 收缩膜以其密封和防篡改的特性而闻名,在加工食品领域尤其受到青睐,因为它可以确保食品的新鲜度和安全性。此外,其清晰、光滑的表面不仅提高了产品的可见度,还增加了货架吸引力,这在竞争激烈的零售业中是一个至关重要的优势。这种视觉吸引力,加上收缩膜的保护性能,使食品公司能够吸引消费者并确保产品的完整性。

- 饮料瓶的高消费量也推动了收缩膜和拉伸膜的需求。收缩膜特别适用于多瓶装饮料,例如六瓶或十二瓶装。它能够与瓶子的形状紧密贴合,确保包装美观、稳定,并方便消费者使用。此外,收缩膜提供的防篡改密封进一步增加了消费者对产品安全性的信心。随着美国瓶装饮料消费量的增加,对拉伸和收缩膜等包装解决方案的需求也持续成长。

- 该地区的市场参与者正在积极创新和推出新产品,以巩固其市场地位并扩大客户群。

- 根据饮料业出版物,截至 2023 年 5 月 21 日的 52 週内,美国自有品牌饮用水销售额超过 53 亿美元。由于消费者对健康补水的兴趣日益浓厚,瓶装水销量激增,预计将对收缩膜和拉伸膜的消费产生重大影响,进一步推动对这些材料的需求。

北美收缩和拉伸膜行业概况

随着许多公司进入包装产业,北美收缩和拉伸薄膜市场比较分散。此外,技术创新和参与者的发展也加剧了市场竞争。

- 2023 年 8 月包装解决方案提供商 Group O 被选为北美独家经销商,提供重新定义包装永续性的新产品。该公司提供的产品是首款采用 30% 消费后回收 (PCR) 材料製成的机器製造的拉伸膜。该产品标誌着包装领域的重大飞跃,尖端性能与永续性性相结合,塑造负责任商业的未来。

- 2023 年 4 月 Holden Industries Inc. 的子公司 Nosco Inc. 宣布推出其专有的 EcoClear 薄膜,用于 StretchPak 和其他卡片包装应用。这款不含 PVC 的薄膜是经过精心设计的,旨在满足主要零售商的永续性需求。它提供了高度透明的显示,以增强您的产品的外观。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 以循环经济为重点的工业生态系分析

- 法律规范

- 收缩膜和拉伸膜价格分析

第五章 市场动态

- 市场驱动因素

- 工业部门需求增加

- 物料输送中防篡改的必要性

- 市场挑战

- 回收挑战

第六章 市场细分

- 产品类型

- 食物

- 裹

- 套筒标籤

- 材料

- 低密度聚乙烯 (LDPE) 和线型低密度聚乙烯(LLDPE)

- 聚氯乙烯(PVC)

- 聚对苯二甲酸乙二醇酯(PET)

- 其他材料

- 最终用途产业

- 饮食

- 消费品

- 药品

- 工业的

- 其他最终用途产业

- 地区

- 美国

- 加拿大

第七章 竞争格局

- 公司简介

- Berry Global Inc.

- Klockner Pentaplast Group

- Amcor Group GmbH

- Clondalkin Group Holdings BV

- Dow Inc.

- Taghleef Industries LLC

- Sealed Air Corporation

- Intertape Polymer Group Inc.

- Emsur Macdonell SA

- Transcontinental Inc.

- Heat Map Analysis

- Competitor Analysis-Emerging Vs. Established Players

第八章投资分析

第九章:市场的未来

简介目录

Product Code: 72593

The North America Shrink And Stretch Film Market size is estimated at USD 5.32 billion in 2025, and is expected to reach USD 6.39 billion by 2030, at a CAGR of 3.73% during the forecast period (2025-2030).

Key Highlights

- Stretch and shrink films are polythene films made with advanced engineering. These films are used for packing items and have unique chemical properties that differentiate them in terms of flexibility and stretchability. Stretch films are thin polythene films that are flexible and elastic and are used to wrap around pallet loads, whereas shrink films are thin films wrapped around a single product or commodity and require heat to pack. These films help keep items from spoiling due to air and moisture, improving the quality of packed goods.

- Shrink sleeve labels refer to 360-degree printed labels that typically use heat in the application process to conform to the product's shape to which the label is applied. Shrink sleeve labels are printed on either side of the plastic or polyester film materials. The durability of the shrink sleeves makes them ideal for products that encounter moisture or friction.

- With various brands increasing their focus on sustainability goals for 2025, exploring more sustainability options is becoming increasingly central to meeting their pledges. Many bottled beverage producers are choosing recycle-ready polyethylene (PE) shrink film over corrugate and paperboard because it uses less energy and lowers greenhouse emissions in the distribution channel without compromising run speeds and machinability.

- Amcor stated that PE shrink is one of the most recycled types of plastic films in the United States, collected through the 18,000 in-store drop-off locations in North America. Expanding efforts to close the loop on a circular economy with post-consumer recycled (PCR) content can achieve additional sustainability benefits while providing the same versatility and performance as standard PE shrink films.

- In addition to their functional benefits, stretch and shrink films offer logistical advantages. The use of these films can significantly improve warehouse efficiency by enabling easier handling and storage of bulk products. Shrink-wrapped bundles, on the other hand, are compact and easier to stack, optimizing space utilization in storage facilities and vehicles. As a result, companies can achieve cost savings and improve overall operational efficiency in their supply chains.

North America Shrink and Stretch Film Market Trends

The Food and Beverage Industry is Witnessing Significant Market Growth

- Stretch film, primarily crafted from linear low-density polyethylene (LLDPE), is a cornerstone in the North American food and beverage industry. It is the go-to choice for palletizing, ensuring products remain secure during transit, thus averting potential damages from shifting. Renowned for its elasticity and robustness, this film adeptly conforms to products of varied shapes and sizes, providing stability and shielding against external elements like dust and moisture.

- On the other hand, shrink film, often fashioned from polyolefin or polyvinyl chloride (PVC), serves a distinct yet equally vital role. When subjected to heat, it contracts, snugly enveloping the goods and creating a secure seal. This feature makes it perfect for bundling items like bottles, cans, and boxes, simplifying handling and transportation. Furthermore, its tamper-evident seal is pivotal in upholding product integrity and bolstering consumer trust in the food and beverage domain.

- Both stretch and shrink films are pivotal in prolonging the shelf life of food and beverage items. Acting as a protective shield against contaminants such as dust, moisture, and microbes, these films are instrumental in preserving product freshness and quality. These factors are especially crucial for perishables, demanding stringent hygiene and temperature controls during storage and transit. By extending shelf life, these films not only combat food wastage but also ensure consumers receive products in prime condition.

- Enhancing product visibility and shelf appeal is another forte of stretch and shrink films. Shrink film, with its clear, glossy finish, elegantly showcases packaged products, a feature particularly prized in retail settings where visual allure can sway consumer choices significantly. Furthermore, manufacturers can directly print branding and product details on the film, reducing the need for additional labels and packaging materials, thereby streamlining the packaging process.

- According to data from the US Census Bureau for December 2023, monthly retail sales from US food and beverage stores hit around USD 90.3 billion, marking a notable 7.4% surge from the preceding month. This uptick in retail sales underscores the heightened demand for films, especially for packaging items like vegetables, fruits, fish, and meat.

The United States is Expected to Hold the Majority Share in the Market

- The rising demand for shrink and stretch films in the United States is primarily fueled by the growing need for effective packaging, bundling, and safeguarding of goods during warehousing and distribution. Additionally, the region hosts annual programs highlighting the robust demand for these films from consumer industries.

- With a notable surge in processed food consumption, the United States has witnessed a corresponding uptick in the need for stretch and shrink films. As consumers increasingly favor convenience foods, the importance of efficient packaging solutions has escalated. Shrink films, in particular, are in high demand, given their role in bundling and safeguarding items like frozen meals, snack packs, and ready-to-eat products.

- Shrink films, known for their ability to create a tight, tamper-evident seal, are especially prized in the realm of processed foods, ensuring both freshness and security. Furthermore, their clear, glossy finish not only enhances product visibility but also boosts shelf appeal, a crucial advantage in the fiercely competitive retail landscape. This visual allure, coupled with the protective attributes of shrink films, aids food companies in attracting consumers and ensuring product integrity.

- The significant consumption of beverage bottles is yet another driver for the demand for stretch and shrink films. Shrink films, in particular, are favored for crafting multi-packs of beverage bottles, such as six or twelve-packs. Their ability to snugly conform to bottle shapes ensures an appealing and stable package and makes them easier for consumers to handle. Moreover, the tamper-evident seal provided by shrink films further bolsters consumer confidence in product safety. Given the escalating consumption of bottled beverages in the United States, the demand for packaging solutions like stretch and shrink films is poised for a corresponding rise.

- Market players in the region have been actively innovating their products and launching new offerings to bolster their market standing and expand their customer base.

- According to the Beverage Industry Magazine, sales of private-label bottled still water in the United States surpassed USD 5.3 billion for 52 weeks ending May 21, 2023. This surge in bottled still water sales, driven by heightened consumer interest in healthy hydration, is poised to significantly impact the consumption of shrink and stretch films, further propelling demand for these materials.

North America Shrink and Stretch Film Industry Overview

The North American shrink and stretch film market is fragmented due to many players entering the packaging industry. Moreover, innovations and developments by players are making the market competitive.

- August 2023: Packaging solutions provider Group O was selected as one of the only distributors in North America to offer a new product that redefines sustainability in packaging. The product offered by the company is a first-ever machine-grade stretch film with 30% post-consumer recycled (PCR) content. This product marks a significant leap in the realm of packaging, where cutting-edge performance meets sustainability, shaping the future of responsible commerce.

- April 2023: Nosco Inc., a subsidiary of Holden Industries Inc., announced the launch of its exclusive EcoClear Film for StretchPak and other carded packaging applications. This PVC-free film was strategically developed to meet the sustainability demands of major retailers. It offers a crystal-clear display for enhanced product appearance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis with an Emphasis on Circular Economy

- 4.4 Regulatory Framework

- 4.5 Shrink and Stretch Film Pricing Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand From Industrial Sector

- 5.1.2 The Need for Tamper-evident Protection in Material Handling

- 5.2 Market Challenges

- 5.2.1 Recycling Challenges

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Hoods

- 6.1.2 Wraps

- 6.1.3 Sleeve Labels

- 6.2 Material

- 6.2.1 Low-density Polyethylene (LDPE) and Linear Low-density Polyethylene (LLDPE)

- 6.2.2 Polyvinyl chloride (PVC)

- 6.2.3 Polyethylene terephthalate (PET)

- 6.2.4 Other Materials

- 6.3 End-use Industry

- 6.3.1 Food and Beverage

- 6.3.2 Consumer Goods

- 6.3.3 Pharmaceutical

- 6.3.4 Industrial

- 6.3.5 Other End-use Industries

- 6.4 Geography

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Berry Global Inc.

- 7.1.2 Klockner Pentaplast Group

- 7.1.3 Amcor Group GmbH

- 7.1.4 Clondalkin Group Holdings BV

- 7.1.5 Dow Inc.

- 7.1.6 Taghleef Industries LLC

- 7.1.7 Sealed Air Corporation

- 7.1.8 Intertape Polymer Group Inc.

- 7.1.9 Emsur Macdonell SA

- 7.1.10 Transcontinental Inc.

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging Vs. Established Players

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

全球拉伸膜和收缩膜市场:市场规模、份额和趋势分析(按材料、产品、应用和地区划分),细分市场预测(2026-2033 年)

全球拉伸膜和收缩膜市场:市场规模、份额和趋势分析(按材料、产品、应用和地区划分),细分市场预测(2026-2033 年) 拉伸膜包装市场-2026-2031年预测

拉伸膜包装市场-2026-2031年预测 拉伸膜及收缩膜市场机会、成长要素、产业趋势分析及预测(2026年至2035年)流延拉伸膜市场-2026-2031年预测

拉伸膜及收缩膜市场机会、成长要素、产业趋势分析及预测(2026年至2035年)流延拉伸膜市场-2026-2031年预测 拉伸膜包装市场:全球预测(2026-2032 年),按薄膜类型、材料、厚度、应用和最终用途产业划分

拉伸膜包装市场:全球预测(2026-2032 年),按薄膜类型、材料、厚度、应用和最终用途产业划分 全球流延拉伸膜市场吹塑拉伸包装膜市场机会、成长动力、产业趋势分析及2025-2034年预测

全球流延拉伸膜市场吹塑拉伸包装膜市场机会、成长动力、产业趋势分析及2025-2034年预测 2032 年拉伸膜市场预测:按产品类型、品种、材料、厚度、应用和地区进行的全球分析拉伸和收缩套标市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球透气拉伸膜市场规模依材料类型、最终用途产业、厚度、地区、范围和预测划分

2032 年拉伸膜市场预测:按产品类型、品种、材料、厚度、应用和地区进行的全球分析拉伸和收缩套标市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球透气拉伸膜市场规模依材料类型、最终用途产业、厚度、地区、范围和预测划分

▼