|

市场调查报告书

商品编码

1693383

印尼黏合剂:市场占有率分析、行业趋势和成长预测(2025-2030 年)Indonesia Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

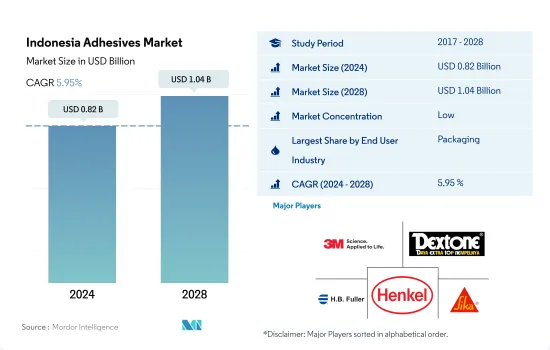

印尼黏合剂市场规模预计在 2024 年为 8.2 亿美元,预计到 2028 年将达到 10.4 亿美元,预测期内(2024-2028 年)的复合年增长率为 5.95%。

国内大量正在实施和计划实施的基础设施计划将对胶合剂需求的成长发挥关键作用。

- 受新冠疫情影响,2020年印尼胶黏剂消费量呈下降趋势。与 2019 年相比,当年的消费量下降了约 13%。该国的封锁是造成该国黏合剂短缺的主要原因。此外,由于生产设施停工和供应链中断,这些黏合剂的需求受到了严重影响。

- 印尼的包装产业在各行各业中发挥着至关重要的作用。因此,包装工业的发展与民族工业的发展密不可分。事实上,包装已成为该国工业产品的竞争因素之一。近年来,包装业与前一年同期比较增6%-7%,2021年营收达104,728亿印尼盾。实际上,即使新冠疫情开始蔓延,包装业务也没有受到太大影响。预计包装产业将以每年 6% 至 8% 的速度成长,与食品和饮料、製药和零售等主要支援产业的成长保持一致。

- 另一方面,工业界目前正在投资大型基础设施计划以加速国家的发展。例如,印尼计划投资超过400亿美元扩建雅加达地铁网络,预计此举将促进该国建筑业的发展。印尼还计划在未来几年内实施价值超过 4000 亿美元的雄心勃勃的建设计划,包括建造 25 个机场和新发电厂。所有这些变数都会影响对黏合剂的需求。

印尼胶黏剂市场趋势

政府推广纸和纸板包装的措施将推动产业

- 包装主要用于保护、容纳、资讯、实用和促销。这使得包装成为大多数行业的重要组成部分。预计不断成长的印尼市场将推动包装使用量,预测期内复合年增长率将达到 4.33%。 2017年,包装使用量达1.4346亿吨,包括纸、纸板和塑胶。受新冠疫情影响,供应链中断、包装材料短缺、货物进出口限制、工厂产能低等因素导致2020年市场出现-5.77%的负成长。

- 2021年,市场将达到4.28%的正成长,各类包装材料的使用量将达到1.5341亿吨。由于近年来电子商务行业的兴起,包装行业预计将在未来继续增长,这对包装行业来说是一个巨大的推动,因为运输货物需要专门的包装。

- 印尼是继中国之后第二大海洋塑胶废弃物排放,这也是印尼政府采取措施禁止使用塑胶的原因。印尼政府实施的生产者延伸责任(EPR)法规要求生产商和零售商重新设计产品包装,以包含更高比例的可回收材料。这将鼓励製造商使用纸和纸板作为包装基材,增加包装过程中使用的黏合剂的数量。

- 在当今竞争激烈的消费品市场中,企业采用有吸引力的包装来在竞争中脱颖而出并在市场上保持其品牌价值已成为必然。

汽车零件出口强劲成长带动产业成长

- 印尼的汽车产业仍然是一个有前景的产业,为该国的经济发展做出了重大贡献。印尼共和国产业部长阿古斯古米旺卡塔萨斯米塔表示,2021年印尼汽车产业呈现惊人成长,成长率达到17.82%的两位数。 2019年,印尼汽车产量约1,286,848辆,但受新冠疫情影响,2020年产量大幅下滑至690,176辆,降幅约46%。受此影响,2019年至2021年生产的汽车数量变化约为-13%,而2020年至2021年的变化约为63%。

- 2019年至2021年,印尼汽车业贸易连续多年保持顺差。 2020年,全球疫情导致进出口双双下滑,限制和扰乱了经济活动,扰乱了全球供应链,打击了整体生产。然而,2021年生产强劲,导致出口和进口均大幅成长,贸易差额达19.3亿美元。虽然 2021 年的商业活动水准是近十年来最高的,但贸易顺差与 2019 年和 2020 年相比却是最低的,当时的顺差分别为 20 亿美元和 19.5 亿美元。

- 在全球范围内,电动车的发展标誌着印尼交通运输部门方式的根本转变。鑑于该国的镍蕴藏量,印尼完全有能力成为全球电动车供应链的主要企业。为了成为该地区电动车未来的一部分,印尼需要投资技术、人才、可再生能源和基础设施。

印尼胶黏剂产业概况

印尼胶合剂市场较为分散,前五大企业市占率合计为15.91%。市场的主要企业有:3M、DEXTONE INDONESIA、HB Fuller Company、Henkel AG & Co. KGaA 和 Sika AG。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑与施工

- 鞋类皮革

- 包装

- 木製品和配件

- 法律规范

- 印尼

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 航太

- 车

- 建筑与施工

- 鞋类和皮革

- 医疗保健

- 包装

- 木製品和配件

- 其他的

- 科技

- 热熔胶

- 反应性

- 溶剂型

- 紫外线固化胶合剂

- 水性

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他的

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- 3M

- ALTECO co., ltd.

- DEXTONE INDONESIA

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI SpA

- Pidilite Industries Ltd.

- PT. Pamolite Adhesive Industry

- Sika AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、限制因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 92438

The Indonesia Adhesives Market size is estimated at 0.82 billion USD in 2024, and is expected to reach 1.04 billion USD by 2028, growing at a CAGR of 5.95% during the forecast period (2024-2028).

The numerous ongoing and planned infrastructure projects in the country to have a key role in the growth of adhesive demand

- The consumption of adhesives in Indonesia has shown a downward trend in 2020 due to the impact of COVID-19. The consumption was reduced by about 13% in terms of volume in the same year compared to 2019. The lockdown in the country has largely become the major reason for the shortage of adhesives in the country. Moreover, due to the shutdown of production facilities and supply chain disruption, the demand for these adhesives is largely being impacted.

- The Indonesian packaging industry plays an important role in all industries and businesses. Therefore, the development of the packaging industry cannot be separated from the development of the national industry. In fact, packaging has become one of the determining factors for the competitiveness of national industrial products. In recent years, the packaging sector has grown by 6%-7% year-on-year, with a realized value of IDR 104,728 billion in 2021. In reality, as the COVID-19 epidemic began to spread, the packing business did not suffer considerably. The packaging industry is expected to increase at a 6%-8% annual rate, in conjunction with the growth of the major supporting sectors, such as food and beverage (Mamin), pharmaceutical, and retail.

- On the other side, the industry is now investing in massive infrastructure projects to accelerate the country's growth. For example, Indonesia is planning to invest over USD 40 billion to expand Jakarta's metro network, which is expected to strengthen the country's construction industry. Indonesia is also planning ambitious construction projects worth more than USD 400 billion in the future years, including the construction of 25 airports and new power plants. All of these variables influence the demand for adhesives.

Indonesia Adhesives Market Trends

The government initiatives to promote paper and paperboard packaging will escalate the industry size

- The packaging is mainly used for protection, containment, information, utility of use, and promotion. This makes packaging an integral part of most industries. The growing Indonesian market is expected to boost packaging usage and register a CAGR of 4.33% during the forecast period. In 2017, packaging usage accounted for 143.46 million tons of packaging, including paper and paperboard and plastic. Due to COVID-19, in 2020, the market registered a negative growth of -5.77%, and this was due to disruption in the supply chain, shortage of packaging material, restrictions on the import and export of goods, and factories operating at low capacity.

- In 2021, the market registered a positive growth of 4.28%, with 153.41 million tons of packaging material used for various purposes. It is expected that the packaging industry will keep growing as there has been a rise in the e-commerce sector which has given a significant boost to the packaging industry in the past few years as special packaging is required for shipping goods.

- The government of Indonesia has taken steps toward the use of plastic, as Indonesia is the second-largest contributor of plastic waste in the ocean after China. The extended producer responsibility (EPR) regulation imposed by the Indonesian government will oblige producers and retailers to redesign their product packaging to have a higher proportion of recyclable material. This will encourage manufacturers to use paper and paperboard as the base material for the packaging, which will increase the volume of adhesives used in the packaging process.

- In today's competitive market of consumer products, it has become inevitable for companies to use attractive packaging to stand out from their competitors and maintain their brand value in the market.

Considerable growth of export values for automotive parts & components will proliferate the industry growth

- The automotive industry in Indonesia remains a promising sector that contributes significantly to the country's economic progress. According to Agus Gumiwang Kartasasmita, Minister of Sector Republic of Indonesia, the automobile industry in Indonesia witnessed tremendous growth in 2021, with a double-digit growth rate of 17.82%. In 2019, the country produced about 12,86,848 units of vehicles which drastically reduced to 6,90,176 units in 2020, accounting for a decline of about 46% owing to the COVID-19 pandemic. Due to this reason, the variation in automotive production between 2019 and 2021 resulted in about -13%, whereas between 2020 and 2021, the variation was about 63%.

- The trade in the automotive sector in Indonesia showed a surplus in all years from 2019 to 2021. Both exports and imports fell in 2020 as a result of the global pandemic, which generated limitations and disruptions in economic activities, so impeding the global supply chain and hurting total production. However, in line with the robust output in 2021, both export and import values increased significantly, with a trade balance of USD 1.93 billion. Although 2021 had the highest level of commercial activity in the prior ten years, the trade balance surplus was the lowest in comparison to 2019 and 2020, which had balance values of USD 2 billion and USD 1.95 billion, respectively.

- Globally, the development of EVs signaled a fundamental shift in the Indonesian transportation sector's policies. Given the country's nickel reserves, Indonesia is well-placed to become a major player in the global EV supply chain. To be a part of the region's EV future, Indonesia needs to invest in technology, talent resources, renewable energy, and infrastructure.

Indonesia Adhesives Industry Overview

The Indonesia Adhesives Market is fragmented, with the top five companies occupying 15.91%. The major players in this market are 3M, DEXTONE INDONESIA, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Indonesia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 ALTECO co., ltd.

- 6.4.3 DEXTONE INDONESIA

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Huntsman International LLC

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Pidilite Industries Ltd.

- 6.4.9 PT. Pamolite Adhesive Industry

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

导热箔黏合剂市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

导热箔黏合剂市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球永续黏合剂市场(按类型、原料、最终用途产业和地区划分)—预测至 2030 年

全球永续黏合剂市场(按类型、原料、最终用途产业和地区划分)—预测至 2030 年 纺织服饰黏合剂市场(按黏合剂类型、树脂类型、形态、织物类型、服饰类型和分销管道)—2025-2030 年全球预测弹性胶合剂市场-全球产业规模、份额、趋势、机会及预测,依树脂类型(聚氨酯、硅胶、硅烷改质聚合物等)、最终用户、地区及竞争情形细分,2020-2030 年预测

纺织服饰黏合剂市场(按黏合剂类型、树脂类型、形态、织物类型、服饰类型和分销管道)—2025-2030 年全球预测弹性胶合剂市场-全球产业规模、份额、趋势、机会及预测,依树脂类型(聚氨酯、硅胶、硅烷改质聚合物等)、最终用户、地区及竞争情形细分,2020-2030 年预测 全球导热箔黏合剂市场

全球导热箔黏合剂市场 全球黏合剂市场预测(2025-2030)全球机器人接头密封市场低创伤亲肤黏合剂市场-全球产业规模、份额、趋势、机会和预测(按应用、最终用户、地区和竞争细分,2020-2030 年)

全球黏合剂市场预测(2025-2030)全球机器人接头密封市场低创伤亲肤黏合剂市场-全球产业规模、份额、趋势、机会和预测(按应用、最终用户、地区和竞争细分,2020-2030 年) 2025年全球磁砖胶黏剂市场报告全球地毯背衬材料市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

2025年全球磁砖胶黏剂市场报告全球地毯背衬材料市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

▼