|

市场调查报告书

商品编码

1693617

美国商用车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)United States Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

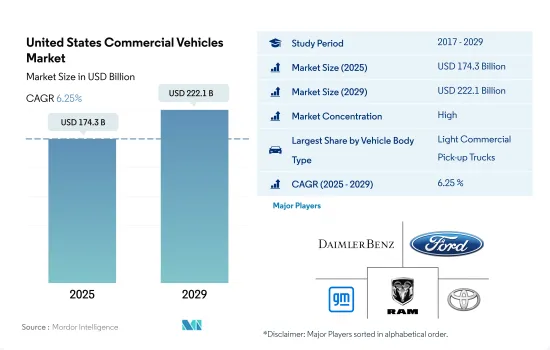

预计 2025 年美国商用车市场规模为 1,743 亿美元,到 2029 年将达到 2,221 亿美元,预测期内(2025-2029 年)的复合年增长率为 6.25%。

强劲的经济推动了美国商用车的多样性,需求从都市区送货车到远距卡车。

- 由于货运量增加、区域价值链全球化、驱动技术进步和对安全的日益重视等因素,商用车市场正在不断发展。自2005年以来,燃料价格一直在稳步上涨,影响了柴油卡车的成长。此外,美国燃料生产商的产能已接近最大限度,扩大生产的空间已不大。

- 疫情的爆发给商用车产业供应链造成了前所未有的破坏。全球范围内实施的封锁和其他限制措施导致了前所未有的旅行和行动限制。基础设施和物流等严重依赖运输的行业陷入停滞,为製造业和货运业带来了新的瓶颈。

- 随着电动和混合动力汽车需求的飙升,一些国家已将电动车充电基础设施的发展列为优先事项。因此,各国推出了多项政策和奖励来鼓励基础建设发展。美国政府率先立法推动电动车普及,目标是到2040年逐步淘汰汽油车和柴油车的生产,实现大多数汽车使用电池驱动。各国政府和地方政府也正在推出奖励和法规,鼓励转型为永续交通。美国政府计划在2030年为所有车型和技术安装50万个公共充电器。

美国商用车市场趋势

政府措施和不断增长的需求推动美国电动车销售繁荣

- 近年来,美国电动车(EV)的普及率一直呈现蓬勃发展之势。这种增长是由人们对电动车的认识不断提高、对环境问题的日益关注以及政府法规的实施所推动的。特别是2016年,加州推出了零排放汽车(ZEV)计划,旨在减少二氧化碳排放,改善空气品质。这项措施不仅推动了加州电动车的普及,也影响了其他州采取类似的零排放汽车法规。因此,2017 年至 2022 年间,电池式电动车(BEV) 的需求激增 634%。

- 美国对电动商用车的需求也在上升。电子商务行业的蓬勃发展、物流活动的增加以及政府对清洁交通的倡议等因素正在推动这一增长。纽约州州长于2021年9月签署了一项重要措施—先进清洁卡车(ACT)法规。该法规设定的目标是到2035年使所有新型轻型汽车实现零排放,到2045年使所有中型和重型汽车实现零排放。受此影响,2022年美国电动商用车需求与前一年同期比较激增21%。

- 政府的回扣、补贴和战略规划等措施正在进一步支持全国范围内的汽车电气化。 2022年5月,拜登总统宣布了一项30亿美元的计划,旨在促进国内电池製造业的发展,以实现从燃气驱动汽车向电动车的过渡。预计这项措施将显着推动该国的电动车发展,尤其是在 2024 年至 2030 年期间,从而增加对电池组的需求。

美国商用车产业概况

美国商用车市场相当集中,前五大公司占了80.10%的市场。市场的主要企业是:戴姆勒股份公司(梅赛德斯-奔驰股份公司)、福特汽车公司、通用汽车公司、Ram Trucking, Inc. 和丰田汽车公司(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 人口

- 人均GDP

- 消费者汽车支出(cvp)

- 通货膨胀率

- 汽车贷款利率

- 电气化的影响

- 电动车充电站

- 电池组价格

- 新款 Xev 车型发布

- 物流绩效指数

- 燃油价格

- OEM生产统计

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 车辆类型

- 商用车

- 公车

- 大型商用卡车

- 轻型商用皮卡车

- 轻型商用厢型车

- 中型商用卡车

- 商用车

- 推进类型

- 混合动力和电动车

- 按燃料类别

- BEV

- FCEV

- HEV

- PHEV

- ICE

- 按燃料类别

- 天然气

- 柴油引擎

- 汽油

- LPG

- 混合动力和电动车

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Daimler AG(Mercedes-Benz AG)

- Daimler Truck Holding AG

- Ford Motor Company

- General Motors Company

- Hino Motors Ltd.

- Isuzu Motors Limited

- PACCAR Inc.

- Ram Trucking, Inc.

- Toyota Motor Corporation

- Volvo Group

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 93001

The United States Commercial Vehicles Market size is estimated at 174.3 billion USD in 2025, and is expected to reach 222.1 billion USD by 2029, growing at a CAGR of 6.25% during the forecast period (2025-2029).

The diversity of commercial vehicles in the United States is driven by a robust economy, with demands ranging from urban delivery vans to long-haul trucks

- The commercial vehicle market is undergoing constant evolution due to factors like increased traffic in goods, globalization of regional value chains, advancements in drive technology, and a heightened focus on safety. Since 2005, fuel prices have been on a steady rise, impacting the growth of diesel trucks. Additionally, fuel producers in the United States are operating at near-maximum capacity, leaving little room for production expansion.

- The onset of the pandemic led to unprecedented disruptions in the commercial vehicle industry's supply chains. Lockdowns and other restrictions imposed globally resulted in mobility and travel limitations of an unprecedented scale. Industries heavily reliant on transportation, such as infrastructure and logistics, came to a standstill, presenting new hurdles for the manufacturing and freight sectors.

- With the surging demand for electric and hybrid vehicles, several countries have prioritized upgrading their electric vehicle charging infrastructure. Consequently, numerous policies and incentives have been introduced to foster infrastructure growth. The US government has taken the lead in enacting legislation to promote electric vehicle adoption, aiming to phase out gasoline and diesel vehicle production by 2040, with a majority of vehicles running on batteries. Governments and municipalities have also implemented incentives and regulations to expedite the shift toward sustainable mobility. By 2030, the US government plans to establish 500,000 public chargers, catering to all vehicle types and technologies.

United States Commercial Vehicles Market Trends

Rapid growth in electric vehicle sales driven by government initiatives and increasing demand in the US

- The United States has witnessed a significant surge in the adoption of electric vehicles (EVs) in recent years. This uptick can be attributed to a heightened awareness of EVs, growing environmental concerns, and the implementation of government regulations. Notably, in 2016, California introduced the Zero-Emission Vehicle (ZEV) program aimed at curbing carbon emissions and improving air quality. This initiative has not only spurred the growth of electric cars within California but has also influenced other states to adopt similar ZEV regulations. Consequently, the nation saw a remarkable 634% surge in demand for battery electric vehicles (BEVs) from 2017 to 2022.

- The demand for electric commercial vehicles in the United States is also on the rise. Factors such as the booming e-commerce industry, increased logistics activities, and governmental initiatives for cleaner transportation have fueled this growth. In a significant move, the governor of New York signed the Advanced Clean Truck (ACT) Rule in September 2021. This rule sets a target for all new light-duty vehicles to be zero-emission by 2035 and the same for medium- and heavy-duty vehicles by 2045. As a result, the United States witnessed a 21% surge in demand for electric commercial vehicles in 2022 compared to the previous year.

- Governmental efforts, including rebates, subsidies, and strategic plans, are further bolstering the electrification of vehicles nationwide. In May 2022, President Biden unveiled a USD 3 billion plan to expedite domestic battery manufacturing, with the aim of transitioning gas-powered vehicles to electric ones. This push is expected to significantly boost electric mobility in the country, particularly during 2024-2030, thereby amplifying the demand for battery packs.

United States Commercial Vehicles Industry Overview

The United States Commercial Vehicles Market is fairly consolidated, with the top five companies occupying 80.10%. The major players in this market are Daimler AG (Mercedes-Benz AG), Ford Motor Company, General Motors Company, Ram Trucking, Inc. and Toyota Motor Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Daimler AG (Mercedes-Benz AG)

- 6.4.2 Daimler Truck Holding AG

- 6.4.3 Ford Motor Company

- 6.4.4 General Motors Company

- 6.4.5 Hino Motors Ltd.

- 6.4.6 Isuzu Motors Limited

- 6.4.7 PACCAR Inc.

- 6.4.8 Ram Trucking, Inc.

- 6.4.9 Toyota Motor Corporation

- 6.4.10 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

人工智慧及其在商用车市场的应用,全球(2024-2029)

人工智慧及其在商用车市场的应用,全球(2024-2029) 商用车市场:按车辆类型、燃料类型、变速箱类型、负载容量、动力传动系统、应用和分销管道划分-2025年至2032年全球预测

商用车市场:按车辆类型、燃料类型、变速箱类型、负载容量、动力传动系统、应用和分销管道划分-2025年至2032年全球预测 2025年全球商用车市场报告

2025年全球商用车市场报告 东协商用车:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

东协商用车:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年) 2025-2029年全球商用车市场

2025-2029年全球商用车市场 2025 年至 2033 年商用车市场规模、份额、趋势及预测(按车型、推进类型、最终用途和地区划分)2025 年至 2033 年日本商用车市场报告,按车辆类型(客车、重型商用卡车、轻型商用皮卡、轻型商用厢式货车、中型商用卡车)、发动机类型(混合动力和电动车、内燃机)和地区划分

2025 年至 2033 年商用车市场规模、份额、趋势及预测(按车型、推进类型、最终用途和地区划分)2025 年至 2033 年日本商用车市场报告,按车辆类型(客车、重型商用卡车、轻型商用皮卡、轻型商用厢式货车、中型商用卡车)、发动机类型(混合动力和电动车、内燃机)和地区划分 商用车市场:依产品、最终用途及地区划分亚太商用车:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度商用车市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

商用车市场:依产品、最终用途及地区划分亚太商用车:市场占有率分析、产业趋势与成长预测(2025-2030 年)印度商用车市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

▼