|

市场调查报告书

商品编码

1693723

印度钢铁 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)India Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

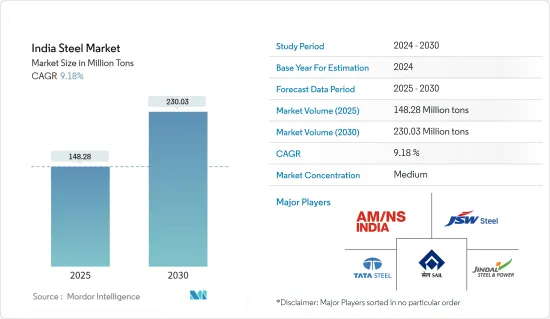

预计 2025 年印度钢铁市场规模为 1.4828 亿吨,2030 年将达到 2.3003 亿吨,预测期内(2025-2030 年)的复合年增长率为 9.18%。

关键亮点

- 在印度,由于新冠疫情爆发,汽车和运输、建筑和施工等所有行业的钢铁消费都受到限制。不过,由于终端用户产业平稳运转,遏制了病毒的传播,印度钢铁市场出现强劲復苏。目前,钢铁市场正从疫情中復苏,并经历强劲成长。

- 短期内,印度政府的强有力政策支持、钢铁业的强劲投资流入、都市化的加快以及建筑基础设施计划支出的增加预计将在预测期内推动市场发展。

- 然而,人均钢铁消费量低、生产成本高,大幅降低了印度钢铁製造商的利润率。价格波动给进口商造成了巨大损失,阻碍了印度钢铁市场的成长。

- 由于钢铁生产中使用氢代替碳,并且预计未来贸易和投资机会将增加,所研究的市场在预测期内可能会出现良好的成长。

印度钢铁市场趋势

高炉-碱性氧气转炉(BF-BOF)技术占市场主导地位

- BF-BOF 製程路线分为两步骤。炼钢:炼铁:将铁矿石、焦炭、石灰石装入高炉。铁矿石经过冶炼可生成熔融生铁。接下来是炼钢。将熔融生铁装入碱性氧气转炉(BOF)。煤炭是炼钢的主要含碳原料。它产生提炼铁矿石并将其转化为液态铁所需的高温。液态铁进入转炉,氧气吹过熔融的铁水以去除碳和其他杂质。

- 将钢铸造成钢锭或钢坯,再经过几道轧延工序加工成钢筋、线材、扁钢等长条类产品。如有必要,对钢材进行回火和涂层处理,以增强其性能和功能。

- 该高炉每天可生产高达10,000吨铁水。 ,一座高炉一次加热可生产高达300吨钢。

- 碱性氧气转炉(BOF)一直是印度生产粗钢最受欢迎的製程路线。其钢铁产量占全国的90%以上。截至2022年底,BOF技术将占产量的46%。

- 在印度,68%的钢铁是透过高炉炼钢生产的,焦煤是主要的还原剂。同时,也可采用粉煤(PCI)或天然气作为辅助还原剂。在 BF-BOF 路线上,绿色氢气正在被开发为 PCI 的替代品。

- 根据印度钢铁部的数据,截至 2022 年底,BOF 是印度粗钢生产最受欢迎的製程路线,产量约 5,743 万吨(占粗钢总量的 46%),比 2021 年成长 8.35%。

- 在预测期内,大多数 BOF 工厂将安装在印度。例如,塔塔钢铁 BSL 有限公司计划在 2024 财年在其位于奥里萨邦的 Meramandali 工厂增加 607 万吨的 BOF 产能,在其位于 Kalinganagar 工厂增加 300 万吨的 BOF 产能。此外,印度还有另外5,000万吨的潜在总生产量。

- 因此,考虑到印度高炉-碱性氧气转炉 (BF-BOF) 技术的成长趋势,BF-BOF 技术很可能会占据市场主导地位。因此,预计预测期内钢铁需求将会成长。

建筑和建筑业占据市场主导地位

- 钢是一种人造合金,属于铁基金属。它含有铁(地球上天然存在的金属元素)、碳和其他成分。建筑业是钢材广泛应用的领域,因为钢材具有很高的耐用性和强度,因此建筑结构都是用钢材製造的。钢骨可以抵御自然灾害,并可根据特定计划的需要进行客製化。

- 屋顶、檩条、内墙、天花板、覆层和外部隔热板等产品均由钢製成。钢材也用于建筑的许多非结构应用,例如暖气和冷气系统以及室内管道。

- 从住宅到停车场、高层建筑,各种建筑都依赖钢材来确保强度。钢材也用于屋顶和外墙覆层。扶手、架子和楼梯等内部固定装置也由钢製成。钢骨为建筑物提供了坚固、刚性的框架。

- 根据国家投资促进与便利局预测,2022-23年建筑业将占GDP的9%左右。该行业就业人数接近5,100万人。受住宅和非住宅领域成长的推动,预计到 2025 年该数字还将达到 1.4 兆美元。

- 据印度工业联合会 (CII) 称,预计 2022 年印度的住宅需求将强劲,其中前七大城市为:德里国家首都辖区、班加罗尔、海得拉巴、孟买、普纳、清奈和加尔各答。新增住宅约 402,000 套,比 2021 年成长 44%。 2023 年第一季(Q1)排名前七位的城市的住宅销售量为 114,000 套,比 2022 年增加了 99,500 多套。

- 政府社会部门计划,例如旨在促进全民住宅的Pradhan Mantri Awas Yojna、萨达尔·帕特尔城市住宅计划、100 个智慧城市任务以及中小城市的基础设施建设,正在促进印度钢铁行业的发展。

- 印度政府正致力于基础建设以促进经济成长。 2022-23 年,政府已拨款约 6,4573 亿印度卢比(77.7356 亿美元)用于新道路和桥樑的基础设施建设。该部已拨款 260 亿印度卢比(3.13 亿美元)用于中央维斯塔计划下非住宅办公大楼的建设。此外,国家基础设施管道(NIP)拥有价值 108 兆印度卢比(1.3 兆美元)的基础设施计划,处于不同的实施阶段。

- 因此,考虑到印度建筑业的成长趋势,建筑业很可能占据市场主导地位。因此,预计预测期内钢铁需求将会上升。

印度钢铁业概况

印度钢铁市场部分分散。主要企业(不分先后顺序)包括 JSW STEEL LIMITED、TATA STEEL、印度钢铁管理局有限公司 (SAIL)、AM/NS INDIA 和 JINDAL STEEL & POWER LIMITED。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 印度政府强而有力的政策支持

- 钢铁业大力投资

- 都市化加快,基础计划支出增加

- 限制因素

- 人均钢铁消费量低

- 生产成本高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 基本形式

- 粗钢

- 最终形态

- 成品钢

- 製造技术

- 高炉-氧气顶吹转炉(BF-BOF)

- 电弧炉(EAF)

- 其他的

- 最终用户产业

- 汽车和运输

- 建筑与施工

- 工具和机械

- 活力

- 消费品

- 其他终端用户产业(石油和天然气开采设备、家具、管道、桶、鼓、包装、半导体)

第六章竞争格局

- 合併、收购、合资、合作和协议

- 市场占有率分析

- 主要企业策略

- 公司简介

- AM/NS India

- Jindal Stainless LIMITED

- JINDAL STEEL & POWER LIMITED

- JSW STEEL LIMITED

- NMDC Steel Limited

- RASHTRIYA ISPAT NIGAM LIMITED

- Steel Authority of India Limited(SAIL)

- TATA STEEL

- Vedanta Limited

第七章 市场机会与未来趋势

- 循环经济的成长趋势

简介目录

Product Code: 93661

The India Steel Market size is estimated at 148.28 million tons in 2025, and is expected to reach 230.03 million tons by 2030, at a CAGR of 9.18% during the forecast period (2025-2030).

Key Highlights

- Steel consumption across industries in India, including automotive and transportation, building and construction, and others, was restricted owing to the COVID-19 pandemic. However, the Indian steel market witnessed a strong recovery with the smooth functioning of the end-user industries in curbing the spread of the virus. Currently, the steel market recovered from the pandemic and is expanding significantly.

- Over the short term, strong policy support by the Indian Government, the strong influx of investments in the steel sector, increasing urbanization, and increased spending on construction and infrastructure projects are projected to drive the market during the forecast period.

- However, due to low per capita steel consumption and high production costs, the profit margin significantly decreased for steel manufacturers in India. The price fluctuation caused huge losses to importers, which hampered the growth of the Indian steel market.

- Nevertheless, using hydrogen instead of carbon in steel manufacturing and increasing trade and investment opportunities in the future for the market studied are likely to create lucrative growth over the forecast period.

India Steel Market Trends

Blast Furnace-Basic Oxygen Furnace (BF-BOF) Technology to Dominate the Market

- The BF-BOF route is a two-stage process: Ironmaking: Iron ore, coke, and limestone are charged into a blast furnace. The iron ore is smelted to produce molten pig iron. Second, it is Steelmaking: Molten pig iron is charged into a basic oxygen furnace (BOF). Coal is used as the primary carbon-bearing material for steelmaking. It generates high temperatures necessary to smelt the iron ore and convert it into liquid iron. This liquid iron enters the converter, where oxygen is blown through the molten iron to remove carbon and other impurities.

- The resulting steel is cast into ingots or slabs and processed into long products like bars, wire, or flat steel strips in several rolling operations. To enhance the characteristics and functions of steel, tempering or coating applications are also done when required.

- Blast furnaces can produce up to 10,000 tons of molten pig iron daily. Then, BOFs can produce up to 300 tons of steel per heat.

- A basic oxygen furnace (BOF) was the most preferred process route for the production of crude steel in India. It accounts for over 90% of the country's steel output. At the end of 2022, BOF technology accounted for 46% of the production.

- In India, 68% of steel is made through the Blast Furnace route in which coking coal is the primary reductant. At the same time, Pulverised Coal Injection (PCI) or Natural Gas can be used as an auxiliary reductant. Green Hydrogen to replace PCI in the BF-BOF route is under development.

- According to the Ministry of Steel of India, BOF was the most preferred process route to produce crude steel in India at the end of 2022, with around 57.43 million tons (46% of total crude steel) produced, which was 8.35% higher than in 2021.

- Most BOF plant installations will occur in India in the forecast period. For instance, Tata Steel BSL Ltd. plans to add 6.07 MMT of BOF capacity at the Meramandali works and 3.0 MMT of BOF capacity at the Kalinganagar works in Odisha state by FY 2024. Moreover, India holds an additional 50.0 MMT potential gross capacity.

- Therefore, considering the growth trends of blast furnace-basic oxygen furnace (BF-BOF) technology in India, the BF-BOF technology is likely to dominate the market. It, in turn, is expected to enhance the demand for steel during the forecast period.

Building and Construction Industry to Dominate the Market

- Steel is a man-made alloy that falls within the ferrous metal classification. It contains iron (a naturally occurring metal element on earth), carbon, and other components. Construction is a sector where steel is widely used since structures are created using it due to its high durability and strength. Steel structures can also withstand natural calamities and be tailored to the needs of a specific project.

- Products, such as roofing, purlins, internal walls, ceilings, cladding, and insulating panels for exterior walls, are made of steel. Steel is also found in many non-structural applications in buildings, such as heating and cooling equipment and interior ducting.

- Buildings from houses to car parks, schools, and skyscrapers all rely on steel for strength. Steel is also used on roofs and as cladding for exterior walls. Internal fixtures and fittings, such as rails, shelving, and stairs, are also made of steel. It provides a robust and stiff frame to the building.

- According to the National Investment Promotion and Facilitation Agency, the building and construction industry accounted for nearly 9% of the GDP in FY 2022-23. Nearly 51 million people are employed in the industry. Moreover, The industry is expected to reach USD 1.4 trillion by 2025 owing to rising residential and non-residential sectors in the country.

- According to the Confederation of Indian Industry (CII), housing construction in the country witnessed strong demand in 2022, with the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata). It added around 402 thousand units of new home construction, which was 44% higher than in 2021. In the first quarter (Q1) of 2023, housing sales in the top seven cities stood at 1.14 lakh units, an increase of over 99,500 units compared to 2022.

- Government social sector programs such as the Pradhan Mantri Awas Yojna, which promotes housing for all, the Sardar Patel Urban Housing Project, the 100 Smart Cities Mission, and the construction of infrastructure in medium and small towns are promoting the growth of the Indian steel industry.

- The Government of India strongly focuses on infrastructure development to boost economic growth. In 2022-23, the government allocated around INR 64,573 crore (USD 7,773.56 Million) for developing new roads and bridge infrastructure. The ministry issued INR 2,600 crore (USD 313 Million) to construct non-residential office buildings under the Central Vista Project. Moreover, under the National Infrastructure Pipeline (NIP), infrastructure projects worth INR 108 trillion (USD 1.3 trillion) are at different stages of implementation.

- Therefore, considering the growth trends of building and construction in India, the building and construction industry is likely to dominate the market. It, in turn, is expected to enhance the demand for steel during the forecast period.

India Steel Industry Overview

The Indian steel market is partially fragmented in nature. The major players (not in any particular order) include JSW STEEL LIMITED, TATA STEEL, Steel Authority of India Limited (SAIL), AM/NS INDIA, and JINDAL STEEL & POWER LIMITED, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Policy Support by the Indian Government

- 4.1.2 Strong Influx of Investments in the Steel Sector

- 4.1.3 Increasing Urbanization and Increased Spending on Construction and Infrastructure Projects

- 4.2 Restraints

- 4.2.1 Low Percapita Steel Consumption

- 4.2.2 High Production Costs

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Basic Form

- 5.1.1 Crude Steel

- 5.2 Final Form

- 5.2.1 Finished Steel

- 5.3 Technology

- 5.3.1 Blast Furnace-basic Oxygen Furnace (BF-BOF)

- 5.3.2 Electric Arc Furnace (EAF)

- 5.3.3 Other Technologies

- 5.4 End User Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Tools and Machinery

- 5.4.4 Energy

- 5.4.5 Consumer Goods

- 5.4.6 Other End-user Industries (Oil and Gas Extraction Equipment, Furniture, Pipes, Barrels, Drums, Packaging, Semiconductors)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AM/NS India

- 6.4.2 Jindal Stainless LIMITED

- 6.4.3 JINDAL STEEL & POWER LIMITED

- 6.4.4 JSW STEEL LIMITED

- 6.4.5 NMDC Steel Limited

- 6.4.6 RASHTRIYA ISPAT NIGAM LIMITED

- 6.4.7 Steel Authority of India Limited (SAIL)

- 6.4.8 TATA STEEL

- 6.4.9 Vedanta Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Trend of Circular Economy

02-2729-4219

+886-2-2729-4219

全球马氏体时效钢市场:市场份额和排名、总销量和需求预测(2025-2031)

全球马氏体时效钢市场:市场份额和排名、总销量和需求预测(2025-2031) 粗钢市场按产品类型、钢种、製造流程、应用、形状和涂层划分-2025-2032年全球预测

粗钢市场按产品类型、钢种、製造流程、应用、形状和涂层划分-2025-2032年全球预测 2021-2031年粗钢市场规模及预测、全球及区域份额、趋势及成长机会分析报告涵盖范围:依产品类型、製造流程及最终用途产业划分

2021-2031年粗钢市场规模及预测、全球及区域份额、趋势及成长机会分析报告涵盖范围:依产品类型、製造流程及最终用途产业划分 2025年全球液压金属加工机械市场报告按产品类型、製程、形式、原料、应用和分销管道分類的钢铁市场—2025-2030 年全球预测2025年全球合金钢市场报告2025年全球轧延和拉伸钢板市场报告2025年全球钢铁市场报告

2025年全球液压金属加工机械市场报告按产品类型、製程、形式、原料、应用和分销管道分類的钢铁市场—2025-2030 年全球预测2025年全球合金钢市场报告2025年全球轧延和拉伸钢板市场报告2025年全球钢铁市场报告 全球钢铁市场(按类型、生产技术、最终用途产业和地区划分)—2030 年预测

全球钢铁市场(按类型、生产技术、最终用途产业和地区划分)—2030 年预测 钢铁的全球市场,规模,占有率,趋势,产业分析报告:各产品,各最终用途,各地区 - 市场预测,2025年~2034年

钢铁的全球市场,规模,占有率,趋势,产业分析报告:各产品,各最终用途,各地区 - 市场预测,2025年~2034年

▼