|

市场调查报告书

商品编码

1693781

南美洲生物农药:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)South America Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

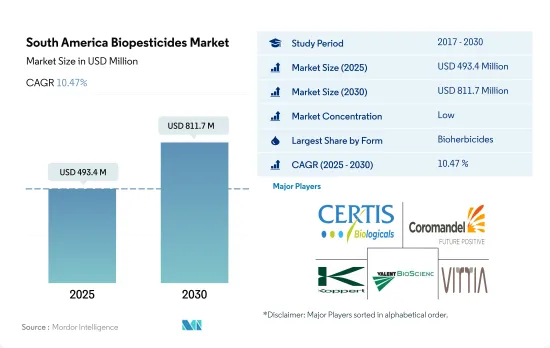

南美生物农药市场规模预计在 2025 年为 4.934 亿美元,预计到 2030 年将达到 8.117 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.47%。

- 生物农药是从动物、植物、昆虫或微生物(包括细菌和真菌)中提取的天然物质或药剂,用于控制农业害虫和感染疾病。

- 到2022年,生物农药市场价值将达到约3.03亿美元,其中沟施占比约80.5%。垄作法之所以占主导地位,主要是因为南美洲的耕作面积广阔。

- 2022 年,生物除草剂占南美洲生物农药市场的 35.0%。生物除草剂由病原体等微生物或源自微生物、昆虫或植物抽取物的植物毒素组成,是一种天然的除草手段。

- 2022 年,生物杀菌剂占南美洲生物农药市场的 24.2%。芽孢桿菌属在害虫防治上有广泛的应用。由于芽孢桿菌能形成芽孢、适应性强、抗逆性强、易于工业化生产和储存,其潜在应用越来越广泛。枯草桿菌可以有效防治植物病原菌镰刀菌和丝核菌。它还可以预防疾病并促进作物生长。

- 2022年,生物农药占南美洲生物农药市场的17.8%。同年,巴西占生物农药市场的57.7%。在巴西,有多种昆虫会危害大豆作物。鳞翅目昆虫和臭虫是最常见的昆虫,需要精心照顾。这些害虫对大豆和其他作物造成直接(产量损失)和间接(谷物品质损失)损害。

- 近年来,南美洲生物农药市场成长显着,其中巴西占据主导地位,2022 年占据 82.7% 的市场占有率。截至 2022 年 3 月,巴西已註册 433 种生物农药,过去九年成长了 404%。巴西消费量最大的生物农药是生物除草剂,2022年占市场占有率的38.2%,其次是生物杀菌剂、其他生物农药和生物杀虫剂。

- 生物除草剂的成功源自于其针对特异性目标的除草作用,且不会损害所施用的作物。 2022年,阿根廷占据南美洲生物农药市场的28.4%,其中连续作物占据市场主导地位,占有88.5%的份额。预计2022年连作作物的生物农药消费量将达20,800吨,2029年将达36,000吨。

- 2022年,南美洲其他地区将占13.5%的市场占有率,其中作物种植中消耗量最高的是生物除草剂,占31.8%,其次是生物杀菌剂,占23.2%,生物杀虫剂占18.6%。该地区已禁止使用多种化学农药,这为生物农药市场的成长创造了机会,因为秘鲁农业和灌溉部已禁止使用剧毒农药,并对超过 12 万人进行了有关农药正确使用、销售和生产的机会。

- 随着越来越多的农民采用永续和环保的害虫防治方法,南美生物农药市场预计将继续成长和扩大,尤其是在巴西。

南美洲生物农药市场趋势

由于国际上对大豆、玉米、向日葵和小麦的需求增加,有机种植面积增加。

- 根据有机农业实验室(FibL Statistics)的数据,2021年南美洲有机作物种植面积为672,800公顷。阿根廷和乌拉圭是该地区主要的有机生产国,大面积的土地用于种植有机作物。 2021年,阿根廷占该地区有机种植面积的11.5%。阿根廷生产的主要有机作物是甘蔗、原毛、水果、蔬菜和豆类。主要有机出口产品为大豆、玉米、向日葵和小麦。

- 2021年作物作物种植面积为38.43万公顷,其中经济作物占比最大,为53.9%。该地区是甘蔗、可可、咖啡和棉花等经济作物的主要产地。巴西是该地区最大的甘蔗生产国。

- 同时,乌拉圭是该地区有机蔬菜和水果的主要生产国。乌拉圭有机农民协会透过与各种有机零售商合作,在该国推广有机农业。世界银行资助的自然资源永续管理和气候变迁计划(DACC)在2022年帮助5,139名农民采用气候智慧型农业(CSA)实践,为该地区有机作物种植作物的扩大做出了贡献。

- 数百万南美农民继续在没有外部投入的情况下耕种,儘管国内产量很低,但他们仍有巨大潜力成为该地区经济的未来。随着人们健康意识的增强,南美洲对环保和永续农业系统的市场正在不断增长。

在阿根廷、巴西和哥伦比亚,约有 49.0% 的消费者有兴趣购买有机食品。

- 南美洲是世界上最重要的有机食品生产地和出口地之一。南美洲的人均有机食品支出相对世界其他地区较低。 2022年人均支出为4.3美元。然而,这些出口导向国家目前正在产生的国内需求却常常被忽略。

- 在阿根廷、巴西和哥伦比亚等南美国家,对有机食品等自然生长产品的需求日益增长。 2021 年威斯康辛州经济发展调查证实,消费者愿意为有机食品支付更高的价格。调查显示,43-49%的消费者註重健康。巴西在有机包装食品和食品饮料的人均支出排名世界第43名。

- 根据全球有机贸易组织2021年发布的数据,2021年阿根廷有机产品市场规模为1,590万美元,占全球市场规模的0.03%,人均消费量为0.35美元。

- 目前,该地区的有机食品市场高度细分,潜在客户仅来自高所得家庭,产品供应仅限于少数超级市场和专卖店。该地区的许多超级市场、专卖店和当地农贸市场,尤其是哥斯达黎加、墨西哥和南美洲的都市区,现在都出售有机食品,以满足日益增长的被压抑的需求。预计不断增强的消费者意识和购买模式将使该地区更了解有机食品的永续性属性。

南美洲生物农药产业概况

南美洲生物农药市场细分化,前五大公司占14.10%的市占率。市场的主要企业包括 Certis USA LLC、Coromandel International Ltd、Koppert Biological Systems Inc.、Valent Biosciences LLC、Vittia Group 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 有机种植区

- 有机产品人均支出

- 法律规范

- 阿根廷

- 巴西

- 价值炼和通路分析

第五章市场区隔

- 形式

- 生物真菌剂

- 生物除草剂

- 生物杀虫剂

- 其他生物防治剂

- 作物类型

- 经济作物

- 园艺作物

- 耕地作物

- 国家

- 阿根廷

- 巴西

- 南美洲其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Atlantica Agricola

- Biolchim SPA

- Certis USA LLC

- Coromandel International Ltd

- Corteva Agriscience

- IPL Biologicals Limited

- Koppert Biological Systems Inc.

- T. Stanes and Company Limited

- Valent Biosciences LLC

- Vittia Group

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

The South America Biopesticides Market size is estimated at 493.4 million USD in 2025, and is expected to reach 811.7 million USD by 2030, growing at a CAGR of 10.47% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, used to manage agricultural pests and infections.

- The biopesticides market was dominated by row, which accounted for about 80.5% and was valued at about USD 303.0 million in 2022. The dominance of row was mainly due to their large cultivation area in South America.

- Bioherbicides accounted for 35.0% of South America's biopesticides market in 2022. Bioherbicides consist of microorganisms such as pathogens and other microbes or phytotoxins derived from microbes, insects, or plant extracts that act as a natural means of weed control.

- Biofungicides accounted for 24.2% of the South American biopesticides market in 2022. Bacillus species have wide applications in pest control. The formation of spores makes them adaptable and resistant to stress, making it easy to industrialize production and storage, thus increasing the potential for the application of Bacillus species. Bacillus subtilis can effectively control the plant pathogenic bacteria Fusarium and Rhizoctonia. It can also prevent diseases and promote crop growth.

- Bioinsecticides accounted for 17.8% of South America's biopesticides market in 2022. Brazil dominated the bioinsecticides market with a share of 57.7% in the same year. In Brazil, there is a complex of insects that attack soybean crops. Lepidopterans and stink bugs are the most common insects that require extensive care. These insects cause direct damage (yield reduction) and indirect damage (reduced grain quality) to soybean and other crops.

- The South American biopesticides market has seen significant growth and dominance in recent years, particularly in Brazil, which accounted for 82.7% of the market share in 2022. This growth is due to the registration of 433 biopesticides in Brazil as of March 2022, representing a 404% increase over the past nine years. Bioherbicides are the most consumed biopesticides in Brazil, which accounted for 38.2% of the market share in 2022, followed by biofungicides, other biopesticides, and bioinsecticides.

- The success of bioherbicides can be attributed to their target-specific weedicide action, which does not harm the crops they are applied to. Argentina accounted for 28.4% of the South American biopesticides market in 2022, with row crops dominating the market with a share of 88.5%. The consumption volume of biopesticides by row crops was 20.8 thousand metric tons in 2022, and it is expected to reach 36.0 thousand metric tons by 2029.

- The Rest of South America accounted for 13.5% of the market share in 2022, with bioherbicides being the most consumed type in crop cultivation at 31.8%, followed by biofungicides and bioinsecticides at 23.2% and 18.6%, respectively. The ban on several chemical pesticides in the region presents an opportunity for the growth of the biopesticides market, as seen with the Ministry of Agriculture and Irrigation in Peru banning highly toxic pesticides and training over 120,000 people on proper pesticide use, marketing, and production.

- The South American biopesticides market is poised for continued growth and expansion, particularly in Brazil, as more farmers adopt sustainable and eco-friendly pest control methods.

South America Biopesticides Market Trends

Growing organic acreage owning to the rising international demand for soy, corn, sunflower, and wheat.

- The area under organic cultivation of crops in South America was recorded at 672.8 thousand hectares in the year 2021, according to the data provided by the Research Institute of Organic Agriculture (FibL statistics). Argentina and Uruguay are the major organic-producing countries in the region, with a large area under organic crops. Argentina occupied a share of 11.5% of the organic area in the region in 2021. The primary organic crops produced in Argentina include sugarcane, raw wool, fruits, vegetables, and beans. The primary organic exports are soy, corn, sunflower, and wheat.

- Cash crops accounted for the maximum share of 53.9% under organic crop cultivation in 2021, with 384.3 thousand hectares of land. The region is a major grower of cash crops like sugarcane, cocoa, coffee, and cotton. Brazil is the largest sugarcane-growing country in the region.

- On the other hand, Uruguay is a large grower of organic fruits and vegetables in the region. The Organic Farmers' Association of Uruguay promotes organic cultivation in the country by partnering with various organic retail outlets. The World Bank-financed Sustainable Management of Natural Resources and Climate Change project (DACC) assisted 5,139 farmers in 2022 to adopt climate-smart agriculture (CSA), which helped increase the area under cultivation of organic crops in the region.

- Millions of farmers in South America continue to practice no-external input agriculture, which may very well represent the future of the region's economy despite the noticeably low domestic production. The population is becoming more health conscious, which creates a larger market for South America's increasingly environmentally friendly and sustainable farming system.

Approximately 49.0% consumers in Argentina, Brazil and Colombia are interested in purchasing organic food.

- South America is one of the important producers and exporters of organic food products globally. The per capita spending on organic food products in South America is comparatively lesser than in other parts of the world. The average per capita spending was recorded at USD 4.3 in 2022. However, these export-oriented countries are now generating an often-overlooked domestic demand.

- The demand for naturally grown products like organic food in South American countries like Argentina, Brazil, and Colombia has increased. A survey conducted by Wisconsin Economic Development in 2021 observed that consumers are willing to pay higher prices for organically grown food. The study revealed that 43-49% of consumers are conscious about their health. Brazil ranks 43rd globally for per capita spending on organic packaged food and beverages.

- The organic products market in Argentina was valued at USD 15.9 million in 2021, representing 0.03% of the global market value, with a per capita consumption of USD 0.35, as per the data given by Global Organic Trade in 2021.

- Currently, the market for organic foods in the region is highly fragmented, with the availability of products limited to a few supermarkets and specialty stores, as only people from higher-income families are potential customers. Many supermarkets, specialized stores, and local farmers' markets in the region are now selling organic food to satisfy the growing latent demand for such products, mainly in Costa Rica, Mexico, and the urban areas of South America. Growing awareness among consumers and their buying patterns are expected to lead to a better understanding of the sustainability attributes of organic food in the region.

South America Biopesticides Industry Overview

The South America Biopesticides Market is fragmented, with the top five companies occupying 14.10%. The major players in this market are Certis USA LLC, Coromandel International Ltd, Koppert Biological Systems Inc., Valent Biosciences LLC and Vittia Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Atlantica Agricola

- 6.4.2 Biolchim SPA

- 6.4.3 Certis USA LLC

- 6.4.4 Coromandel International Ltd

- 6.4.5 Corteva Agriscience

- 6.4.6 IPL Biologicals Limited

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 Valent Biosciences LLC

- 6.4.10 Vittia Group

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

生物农药市场:按类型、作物、配方、应用和销售管道划分-2026-2032年全球市场预测

生物农药市场:按类型、作物、配方、应用和销售管道划分-2026-2032年全球市场预测 全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年)

全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球生物农药市场报告

2026年全球生物农药市场报告 生物农药市场规模、份额和趋势分析报告:按产品、作物类型、来源、应用、地区和细分市场划分 - 预测,2026-2033年

生物农药市场规模、份额和趋势分析报告:按产品、作物类型、来源、应用、地区和细分市场划分 - 预测,2026-2033年 生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测

生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测 生物农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

生物农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034)

日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034) 全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析

全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析