|

市场调查报告书

商品编码

1693961

美国工业感测器:市场占有率分析、行业趋势和成长预测(2025-2030 年)United States (US) Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

预计 2025 年美国工业感测器市场规模为 176.6 亿美元,到 2030 年将达到 246.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.93%。

工业感测器是工厂自动化和工业 4.0 的重要组成部分。运动、环境和振动感测器等感测器用于监测设备的健康状况,包括线性和角度定位、倾斜检测、水平、衝击和跌落检测。美国工业有望在经济和人口方面加强其运营,从而为国内利润和出口潜力做出贡献。

关键亮点

- 工业感测器系统通常由 24V DC 供电,这与由 3V 或 5V 供电的消费系统中的感测器有很大不同。因此,工业感测器系统需要额外的电源管理来有效驱动感测器。这些系统使用 IO-Link 等数位输出直接连接到微控制器或无线电收发器。

- 美国物联网的日益普及可以归因于快速数位化、技术进步、政府措施、政策和旨在促进数位转型和工业 4.0 的投资等因素。随着工业 4.0 和物联网的普及,製造业的重大转变要求企业采用更敏捷、更聪明、更具创新性的方式来推动生产,利用自动化和技术补充和增强人力,以减少因製程故障而导致的工业事故。连网型设备和感测器的高度渗透以及 M2M通讯的实现正在製造业中产生越来越资料点。

- 过去两年,全球汽车产业受到低迷的打击,美国也出现了同样的趋势。该部门的感测器和感测器组件数量有所增加。过去几年,MEMS 压力感测器在智慧汽车领域得到了广泛应用。为此,Asystom 推出了一系列自主性不断增强的多感测器 IIoT 装置。

- 多感测器功能将新型机载、连网、节能电子设备与动态分析功能结合,满足了各种工业设备的预测性维护需求。除了性能提升之外,这些创新产品还环保且可 100% 升级。

- 儘管感测器整合提高了工业自动化水平,但它需要额外的成本,限制了其在成本敏感的应用中的使用。此外,新产品研发活动的高开发成本对于缺乏资金的中小型感测器製造商来说是一个重大挑战。近年来,成本差距不断缩小,但仍然昂贵。然而,由于生产力在某些工业环境中至关重要,这些感测器正被全部区域的多个组织广泛采用。然而,高昂的初始投资仍是市场成长的主要障碍。

美国工业感测器市场趋势

物联网的日益普及导致对感测元件的需求正在推动市场

- 物联网 (IoT) 是工业 4.0 的关键组成部分。它广泛用于製造业和服务业的生产系统监控。透过提高性能,这项技术为製造业开闢了新的创新可能性。物联网的采用和使用已经改变了各行各业运作、通讯和利用数据的方式,而且其成长没有放缓的迹象。

- 工业物联网使各行各业能够重新思考经营模式,并从工业物联网设备中获得可操作的资讯和知识。数据共用生态系统已经开始形成新的收益来源和伙伴关係。

- 同时,从感测器收集的即时数据使工业物联网能够为「决策」设备提供动力,从而开发出能够利用这些内建功能采取特定行动的机器人。这是在仓库中发生的,是机器人物联网 (IoRT) 的一部分。物联网技术作为数位转型的重要方面,在製造业中的重要性日益凸显。

- 感测器稳定可靠的性能连接重工业业务资产,每天驱动重要指标。製造商不断监控其生产线上资产的运作。 IIoT 透过 IIoT 平台和工业连接整合这些复杂产业中常见的传统机械,以满足各种使用案例、角色和应用。

- IIoT 使用智慧感测器来监控和改进工业流程和设备。这些感测器即时捕获和分析有关机器、组件和技术的数据,然后储存该数据以供进一步分析或发送以通知技术人员或操作员出现问题。根据全球行动通讯系统协会的数据,到 2025 年,北美消费者和工业物联网 (IoT) 连接总数预计将成长到 54 亿。

- 此外,各製造商正在为物联网设备配备感测器以提高其效能。例如,2023 年 5 月,美国物联网 (IoT) 解决方案供应商 iMatrix Systems 推出了一系列专为食品和农业储存、运输监控、製药和农业应用而设计的温度和湿度感测器。 NEO系列感测器能够快速且准确地测量温度和湿度的变化,非常适合用于冷藏和冷藏运输等动态冷藏环境。

压力感测器占很大市场占有率

- 压力感测器用于许多製程应用和液压和气压设备中,以监测相对系统压力。这些感测器由于在航太、汽车、医疗和消费品等各行业的应用不断扩大,多年来经历了显着的成长。从实验室应用到工厂和机械工程,由于测量技术的发展,压力和液位测量设备与其应用领域一样多样化。

- 在过去的几年里,越野车和越野车都配备了创新的轮胎压力控制系统。例如,在梅赛德斯 G63 AMG 6X6 中,驾驶可以分别检查和改变前轴和后轴的轮胎压力。据悉,该系统可在不到20秒的时间内将轮胎压力从0.5巴提升至1.8巴。此类应用,加上对轮胎压力监测系统 (TMPS) 日益增长的需求,预计将在预测期内占据轮胎压力应用中对压力感测器需求的主导地位。

- 压阻式和电容式感测器在压力感测器市场占据主导地位,因为它们在汽车、医疗、石化和石油天然气行业的应用日益广泛。由于光学感测器和谐振固态感测器在危险环境中的应用,预计在预测期内将出现增长。

- 例如,2023年9月,能源科技公司贝克休斯宣布推出最新产品-氢能药物氢额定压力感测器。氢气压力感测器旨在提供长期稳定性并承受恶劣环境,可用于各种应用,包括燃气涡轮机、氢气生产电解和氢气加气站。

- 由于人口老化加剧、医疗支出增加以及人口慢性病增多,医疗保健产业也迎来了巨大的成长机会。美国的人均医疗保健支出比世界上任何其他国家都多。美国有明确的医疗保健系统资金来源,大部分费用由私人保险承担。 2023财年,私人保险将承担约三分之一的医疗保健费用。

美国工业感测器市场概况

美国工业感测器市场高度细分,主要参与者包括 TE Connectivity Ltd.、Omega Engineering Inc.、Honeywell International Inc.、Rockwell Automation Inc. 和 Siemens AG。市场参与企业正在采取联盟和收购等策略来加强其产品供应并获得可持续的竞争优势。

- 2023 年 6 月-义法半导体面向工业市场推出首款 MEMS 防水/防液体绝对压力感测器,并宣称具有 10 年长寿命计画。最新的防水压力感测器提供数位转型所需的环境稳健性以及保护客户 MEMS 设计所需的长期可用性。

- 2023 年 1 月 - Quadric 和 ams Osram 建立合作伙伴关係,开发整合感测模组,将最先进的 Mira 系列可见光和红外线CMOS 感测器与 Quadric 先进的 Chimera GPNPU 处理器结合。整合的超低功耗模组实现了穿戴式科技中新型的智慧感应。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 物联网的日益普及推动了对感测组件的需求

- 更重视预测性维护和远端监控

- 市场挑战/限制

- 高成本和营运问题

第六章市场区隔

- 连结性别

- 有线解决方案

- 无线解决方案

- 按类型

- 流量感测器

- 市场概览

- 最终用户产业

- 温度感测器

- 市场概览

- 最终用户产业

- 液位感测器

- 市场概览

- 最终用户产业

- 压力感测器

- 市场概览

- 最终用户产业

- 气体感测器

- 市场概览

- 最终用户产业

- 其他感测器

- 流量感测器

第七章竞争格局

- 公司简介

- Texas Instruments Incorporated

- TE Connectivity Ltd

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- Stmicroelectronics Inc.

- Ams-osram AG

- NXP Semiconductors NV

- Bosch Sensortec GMBH(Bosch Internationals)

- Sick AG

- ABB Ltd

- Omron Corporation

- Emerson Electric Co.

- Endress+Hauser AG

- The Krohne Group

- Yokogawa Electric Corporation

- Meggitt Sensing Systems

- Vega Grieshaber KG

- Analog Devices, Inc.

- Sensata Technologies Inc.

- Infineon Technologies AG

第八章 市场展望

- 当前地缘政治情势如何影响市场

- 经济放缓/衰退的预期影响

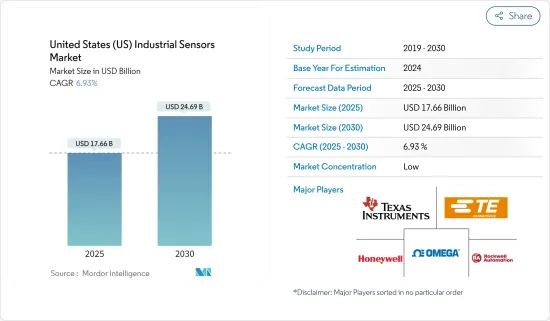

The United States Industrial Sensors Market size is estimated at USD 17.66 billion in 2025, and is expected to reach USD 24.69 billion by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

Industrial sensors are a crucial part of factory automation and Industry 4.0. Sensors such as motion, environmental, and vibration sensors are used to monitor equipment health, from linear or angular positioning, tilt sensing, leveling, shock, or fall detection. United States industries are positioned to augment their operations economically and demographically, serving both domestic interests and export possibilities, which will rise soon.

Key Highlights

- An industrial sensor system is often powered by a 24V DC source, which is very different from a sensor in a consumer system that is powered by a 3V or 5V source. As a result, industrial sensor systems require additional power management to drive the sensors effectively. These use digital outputs such as IO-Link directly to a microcontroller or the wireless transceiver.

- The increasing adoption of IoT in the United States can be attributed to factors like rapid digitalization, technological advancements, government initiatives, policies, and investments aimed at promoting digital transformation and Industry 4.0. Due to Industry 4.0 and the acceptance of IoT, massive shifts in manufacturing require enterprises to adopt agile, smarter, and innovative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. With the high adoption rate of connected devices and sensors and the enabling of M2M communication, there has been an increase in the data points generated in the manufacturing industry.

- Although the global automotive sector witnessed a recession in the past two years, the trend was also reflected in the United States. The number of sensors and sensor components increased in the sector. MEMS pressure sensors have witnessed significant adoption in the smart automotive sector in the last few years. For the same, Asystom launched a range of multi-sensor IIoT devices featuring increased autonomy.

- The multi-sensor capability has addressed the predictive maintenance needs of a wide array of industrial equipment, integrating new on-board, connected, energy-saving electronics performing in situ analysis. Apart from increased performance, these innovative products are eco-responsible and 100% upgradeable.

- Although the integration of sensors increases the industrial automation level, it incurs an additional cost, which limits the use in cost-sensitive applications. Additionally, high development costs involved in the research and development activities to manufacture new products act as a critical challenge, mainly for the cash-deficient small and medium-sized sensor manufacturers. While the cost disparity has been declining in the past few years, they still cost more. However, as productivity is crucial in several industrial settings, these sensors have been widely adopted by multiple organizations across the region. However, higher initial investment still poses a significant challenge to the market's growth.

United States (US) Industrial Sensors Market Trends

Growing Adoption of IoT Leading to Demand for Sensing Components Drives the Market

- The Internet of Things (IoT) is a critical component of Industry 4.0. It has extensive applications in the monitoring of production systems in manufacturing and services. This technology opens up new and innovative possibilities in manufacturing by facilitating higher performance. The implementation and use of the Internet of Things transformed how industries operate, communicate, and utilize data, and it is only continuing to grow.

- The Industrial Internet of Things enabled industries to rethink business models, generating actionable information and knowledge from IIoT devices. A data-sharing ecosystem started to build new revenue streams and partnerships.

- On the other hand, aggregated and real-time data from sensors led to the development of robots that can take specific actions because of these built-in capabilities, whereby IIoT becomes a driver of 'decision-making' devices. This happened in warehouses as the Internet of Robotic Things (IoRT). As an essential aspect of digital transformation, IoT technology is becoming increasingly important in the manufacturing industry.

- The consistent and reliable performance of sensors has led the assets in heavy industrial operations to drive critical daily metrics. Manufacturers are constantly monitoring the uptime of assets along their production lines. IIoT integrates legacy machinery commonplace within these complex industries via industrial connectivity with IIoT platforms for different use cases, roles, and applications.

- IIoT uses smart sensors to monitor and improve industrial processes and equipment. These sensors capture and analyze data about machines, components, and techniques in real time and then transmit that data for storage, further analysis, or to notify a technician or operator that something is going wrong. According to the Global System for Mobile Communications Association, by 2025, North America's total number of consumer and industrial Internet of Things (IoT) connections is forecast to grow to 5.4 billion.

- Moreover, various manufacturers are deploying sensors in IoT devices to boost their performance. For instance, in May 2023, iMatrix Systems, a US-based provider of Internet of Things (IoT) solutions, launched a range of temperature and humidity sensors designed for use in food and produce storage, transport monitoring, pharmaceutical, and agriculture applications. The NEO series sensors can quickly and accurately measure changes in temperature and humidity, making them ideal for use in dynamic refrigeration environments like cold storage and refrigerated transportation.

Pressure Sensors to Hold Significant Market Share

- Pressure sensors are utilized to monitor relative system pressure in many process applications, as well as hydraulics and pneumatics. These sensors have witnessed significant growth over the years owing to the increasing applications across various industries, such as aerospace, automotive, healthcare, consumer goods, etc. Ranging from laboratory applications to plant and mechanical engineering, pressure and level measuring devices have become as diverse as their areas of application, thanks to the evolution of measurement technologies.

- In the past few years, exclusive cross-country and off-road cars have been installed with an innovative tire pressure control system. For instance, the G63 AMG 6X6 from the Mercedes enables the driver to check and vary the tire pressure of both the front and rear axles separately. Reportedly, the system takes less than 20 seconds to raise the tire pressure from 0.5 bar to 1.8 bar. Such applications, coupled with increasing demand for Tire Pressure Monitoring Systems (TMPS), are expected to govern the need for pressure sensors in tire pressure applications over the forecast period.

- Piezoresistive and capacitive sensors dominate the pressure sensors market as they are increasingly used in the automotive, medical, petrochemical, oil, and gas industries. Optical and resonant solid-state sensors are anticipated to exhibit increased growth over the forecast period due to their applications in hazardous environments.

- For instance, in September 2023, Baker Hughes, an energy technology company, announced the launch of its latest product for hydrogen-druck hydrogen-rated pressure sensors. Designed to offer longer-term stability and withstand harsh environments, the hydrogen pressure sensors can be used in various applications, including gas turbines, hydrogen production electrolysis, and hydrogen filling stations.

- The medical industry is also observing significant growth opportunities owing to rising geriatric populations, increasing healthcare expenditures, and growing chronic diseases among the considerable population. The USA spends more money on healthcare per person than any other country in the world. Nevertheless, the United States has a distinct method of funding their healthcare system, with most of the costs being covered by private insurance. In the fiscal year 2023, private insurance covers approximately one third of total health spending.

United States (US) Industrial Sensors Market Overview

The United States Industrial Sensors Market is highly fragmented, with the presence of major players like TE Connectivity Ltd, Omega Engineering Inc., Honeywell International Inc., Rockwell Automation Inc., and Siemens AG. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- June 2023 - STMicroelectronics introduced the first MEMS water/liquid-proof absolute pressure sensor with a declared 10-year longevity program for the industrial market. The latest waterproof pressure sensors provide the environmental robustness needed to power digital transformation with the long-term availability necessary to protect customers' MEMS designs.

- January 2023 - Quadric and ams OSRAM established a collaborative partnership to create integrated sensing modules that combine the cutting-edge Mira Family of CMOS sensors for visible and infrared light with Quadric's advanced Chimera GPNPU processors. The integrated ultra-low power modules will allow wearable technology to use new types of smart sensing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of IoT Leading to Demand for Sensing Components

- 5.1.2 Growing Emphasis on the Use of Predictive Maintenance and Remote Monitoring

- 5.2 Market Challenges/Restraints

- 5.2.1 High Cost and Operational Concern

6 MARKET SEGMENTATION

- 6.1 By Connectivity

- 6.1.1 Wired Solutions

- 6.1.2 Wireless Solutions

- 6.2 By Type

- 6.2.1 Flow Sensors

- 6.2.1.1 Market Overview

- 6.2.1.2 End-user Industry

- 6.2.2 Temperature Sensors

- 6.2.2.1 Market Overview

- 6.2.2.2 End-user Industry

- 6.2.3 Level Sensors

- 6.2.3.1 Market Overview

- 6.2.3.2 End-user Industry

- 6.2.4 Pressure Sensors

- 6.2.4.1 Market Overview

- 6.2.4.2 End-user Industry

- 6.2.5 Gas Sensors

- 6.2.5.1 Market Overview

- 6.2.5.2 End-user Industry

- 6.2.6 Other Sensors

- 6.2.1 Flow Sensors

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 TE Connectivity Ltd

- 7.1.3 Omega Engineering Inc.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Siemens AG

- 7.1.7 Stmicroelectronics Inc.

- 7.1.8 Ams-osram AG

- 7.1.9 NXP Semiconductors N.V.

- 7.1.10 Bosch Sensortec GMBH (Bosch Internationals)

- 7.1.11 Sick AG

- 7.1.12 ABB Ltd

- 7.1.13 Omron Corporation

- 7.1.14 Emerson Electric Co.

- 7.1.15 Endress + Hauser AG

- 7.1.16 The Krohne Group

- 7.1.17 Yokogawa Electric Corporation

- 7.1.18 Meggitt Sensing Systems

- 7.1.19 Vega Grieshaber KG

- 7.1.20 Analog Devices, Inc.

- 7.1.21 Sensata Technologies Inc.

- 7.1.22 Infineon Technologies AG

8 MARKET OUTLOOK

- 8.1 Impact of Current Geopolitical Scenarios on the Market

- 8.2 Impact of Anticipated Economic Slowdown/Recession

工业感测器市场机会、成长要素、产业趋势分析及2026年至2035年预测

工业感测器市场机会、成长要素、产业趋势分析及2026年至2035年预测 工业感测器市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、最终用户、功能、安装类型、设备及解决方案划分

工业感测器市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、最终用户、功能、安装类型、设备及解决方案划分 中国工业感测器市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

中国工业感测器市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本工业自动化感测器市场规模、份额、趋势及预测(按感测器类型、类型、自动化模式、最终用户和地区划分,2026-2034年)

日本工业自动化感测器市场规模、份额、趋势及预测(按感测器类型、类型、自动化模式、最终用户和地区划分,2026-2034年) 2026年全球工业感测器市场报告

2026年全球工业感测器市场报告 半导体气体感测器市场-2026-2031年预测

半导体气体感测器市场-2026-2031年预测 单单点感测器市场按技术、性别、功率、安装方式、应用和最终用户产业划分-2026-2032年全球预测按感测器类型、技术、应用、最终用户和分销管道分類的中风感测器市场—2026-2032年全球预测非冷冻金属封装检测器市场:按技术、检测器类型、波长、应用和分销管道划分,全球预测(2026-2032年)日本工业感测器市场报告(按感测器类型、最终用途产业和地区划分,2026-2034年)

单单点感测器市场按技术、性别、功率、安装方式、应用和最终用户产业划分-2026-2032年全球预测按感测器类型、技术、应用、最终用户和分销管道分類的中风感测器市场—2026-2032年全球预测非冷冻金属封装检测器市场:按技术、检测器类型、波长、应用和分销管道划分,全球预测(2026-2032年)日本工业感测器市场报告(按感测器类型、最终用途产业和地区划分,2026-2034年)