|

市场调查报告书

商品编码

1836482

北美汽车空气滤清器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)North America Automotive Airfilters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

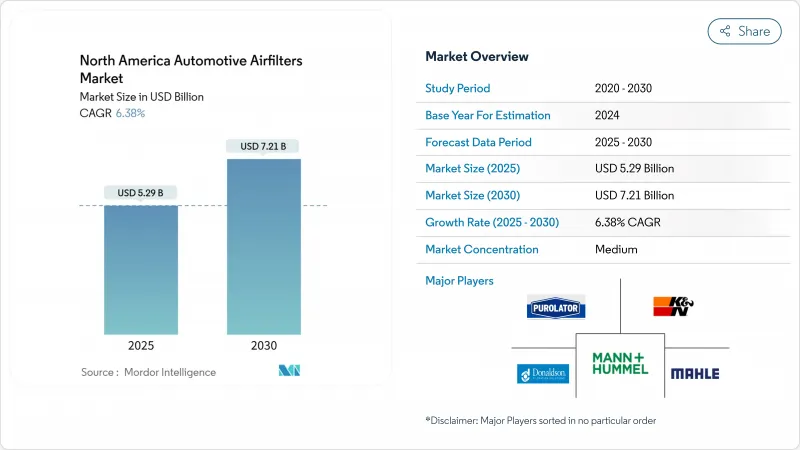

北美汽车空气滤清器市场预计在 2025 年达到 52.9 亿美元,到 2030 年将达到 72.1 亿美元,复合年增长率为 6.38%。

北美汽车空气滤清器市场的稳定扩张得益于老旧车辆强劲的更换需求、美国和加拿大日益严格的颗粒物和氮氧化物法规,以及市场转向高端座舱滤清器。由于野火烟雾、都市区雾霾和日常长途通勤,过滤已从一项日常维护工作转变为一项健康保护措施,座舱滤清器如今占据了汽车保有量的绝大部分。随着监管机构要求在不影响气流的情况下提高过滤效率,奈米纤维滤材的采用正在加速,而线上零售商则透过为消费者提供透明的定价和选择来重塑市场经济。同时,电池式电动车份额的上升和长期引擎进气滤清器数量的下降,迫使供应商将北美汽车空气滤清器市场的重点转向HEPA座舱、温度控制和智慧感测器产品。

北美汽车空气滤清器市场趋势与洞察

美国和加拿大加强PM和NOx排放法规,加速过滤器升级週期

加州于2024年12月核准的《先进清洁汽车II》豁免法案进一步收紧了区域标准,并将迟早影响北美汽车空气滤清器市场。奈米纤维复合材料能够以较低的压降实现所需的捕集效率,从而保持燃油经济性。随着PM2.5法规收紧至9µg/m³,能够证明过滤性能的供应商将享有定价权,而传统的纤维素产品线将面临利润压缩。重型车辆标准将于2027年生效,这将提高耐用性和保固门槛,鼓励轻型买家认识到长寿命过滤器的根本价值,并巩固北美汽车空气滤清器市场的高端地位。

野火过后快速了解客舱空气质量

2024 年,创纪录的森林大火产生的烟雾笼罩了加州、奥勒冈州和不列颠哥伦比亚省数週,导致颗粒物读数超过健康警戒基准值,并引发了消费者对 HEPA 级车厢过滤器的需求。同样的想法也蔓延到了道路上。通勤者将他们的汽车视为移动庇护所,并要求过滤器能够过滤掉病毒、过敏原和烟雾。大众市场原始设备製造商对此做出了回应,他们提供曾经仅用于高端装饰的多层车厢滤芯,售后市场公司正在为旧款车型提供改装套件。促销宣传活动强调世界卫生组织的 PM2.5 指导和儿童呼吸系统健康,以证明高端提升销售的合理性。导航应用程式会迭加烟雾地图,促使驾驶员启动再循环并提醒他们更换过滤器,从而加强回馈迴路。 Cabin Media 是北美汽车空气滤清器市场的核心参与者。

长寿命可清洗棉纱布过滤器可更换竞食

高性能品牌销售的可重复使用棉纱布过滤器的使用寿命从 12 个月延长至近五年。爱好者欣赏改进的气流和永续性讯息,特别是在沙漠环境中,因为在沙漠环境中灰尘较大,需要经常更换。零售商强调 50,000 英里的保固期和终身成本节约,从传统的纸质生产线中获取价值。主流采用仍然受到高昂的前期成本和繁琐的加油过程的限制,这些过程可能会污染空气流量感知器。即使是适度的转换率也会蚕食北美汽车空气滤清器市场售后市场的销售量。製造商正在透过推出带有抗菌衬里的可清洗、插入式座舱过滤器来应对,在恢復收益的同时与循环经济目标保持一致。

报告中分析的其他驱动因素和限制因素

- 配备专用 HEPA 车厢过滤器的 EV/HV 平台

- 支援物联网的智慧过滤器和更换预测应用程式集成

- 到 2035 年,纯电动车的普及将消除对引擎进气过滤器的需求

細項分析

随着监管机构将重点放在 PM2.5 捕获上,预计到 2024 年奈米纤维复合材料的复合年增长率将达到 8.30%,是所有材料中成长最快的。纸张/纤维素仍占北美汽车空气滤清器市场的 43.25%,但纸张和纤维素难以在不增加褶皱厚度(这会阻碍气流)的情况下达到新的效率目标。静电纺丝奈米纤维可去除 99.9998% 的 300-500nm 颗粒,且压降较低。供应商正在将奈米纤维涂层与纤维素芯混合,以降低成本并利用现有生产线。随着原始设备製造商 (OEM) 追求碳中和供应链,植物来源聚合物和再生纤维素正在吸引研发资金。氧化石墨烯增强纤维素奈米纤维在实验室测试中实现了 99.98% 的捕获率,同时可在土壤中生物降解,为未来的主流应用指明了方向。

聚丙烯和纸浆价格的波动将阻碍对冲策略较弱的小型企业,迫使它们转向契约製造或专业领域。拥有纸浆和树脂工厂的垂直整合跨国公司拥有成本优势,可以尝试融合熔喷、纺粘和电纺层的混合堆迭技术。从2025年到2030年,奈米纤维的应用将逐渐从涡轮增压汽油SUV转向轻型商用货车,到2030年,北美汽车空气滤清器市场规模将从个位数扩大到15%左右。

车厢滤清器已占销售额的 55.10%。这是北美汽车空气滤清器市场舒适性超过动力传动系统零件的罕见例子。受野火烟雾、疫情和 HEPA 过滤器定位的推动,车厢单元的复合年增长率为 7.50%。引擎滤清器对于所有销售的内燃机汽车仍然必不可少,但随着纯电动车规模的扩大,检查间隔将会增加,销量将逐渐下降。美国能源局研究确定了空气清净机的能量係数,间接促使汽车工程师朝着更高的 CADR(洁净空气输送率)目标迈进。汽车车厢滤清器正在抄袭家用空气清净机的行销语言,包括多层颗粒碳抗菌堆迭、智慧型手机控制的再循环和 LED 寿命指示器。供应商透过向活性碳中註入铜或银离子来区分,承诺在几分钟内惰性病毒。这种技术转变巩固了车厢滤清器作为北美汽车空气滤清器市场经济成长引擎的地位。

儘管HEPA(高效空气滤清器)备受追捧,但大众市场车辆仍在继续配备符合成本限制的颗粒物专用座舱滤清器。售后市场将填补这一空白,2025年在线销售的替换座舱滤清器中,30%将升级为活性碳或HEPA。因此,即使纯电动车(BEV)取消了引擎滤清器,经销商仍将看到平均售价上涨、销量结构变化和利润贡献提升。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 美国和加拿大的PM和NOx排放法规更加严格(EPA Tier-3、CARB LEV III)

- 山火过后车内空气净化的快速认知

- 车龄超过 12.5 年的轻型车辆的老化正在推高售后市场的车辆数量。

- 配备专用 HEPA 车厢过滤器的 EV/HV 平台

- 支援物联网的智慧过滤器和更换预测应用程式集成

- 原始设备製造商转向涡轮增压汽油SUV的低摩擦奈米纤维引擎介质

- 市场限制

- 长寿命、可清洗的棉纱布过滤器导致更换竞食

- 随着纯电动车的普及,到2035年,引擎进气过滤器的需求将消失

- 聚丙烯和纤维素纸浆价格波动对净利率带来压力

- 由于假冒电商过滤器的广泛存在,品牌份额下降

- 价值/供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依材料类型

- 纸张/纤维素

- 合成纱布/棉

- 形式

- 奈米纤维复合材料

- 其他活性物(活性碳、金属网)

- 按过滤器类型

- 进气(引擎)空气滤清器

- 车厢空气滤清器

- 按车辆类型

- 搭乘用车

- 轻型商用车(LCV)

- 中型和重型商用车(MHCV)

- 按销售管道

- OEM

- 售后市场

- 独立售后市场

- 授权服务中心

- 网路零售

- 按国家

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mann+Hummel

- Donaldson Company

- Purolator Filters LLC

- K&N Engineering

- AIRAID(Truck Hero)

- S&B Filters Inc.

- Mahle GmbH

- Bosch Automotive Aftermarket

- Denso Corporation

- Cummins Filtration

- Fram Group

- Clarcor(Part of Parker-Hannifin)

- ACDelco(GM)

- AFE Power

- Wix Filters

- Sogefi Group

- H&V(Engineered Media)

- Roki Co., Ltd.

- Champion Laboratories

- Luber-finer

第七章 市场机会与未来展望

The North America Automotive Air Filters market generated USD 5.29 billion in 2025 and is forecast to climb to USD 7.21 billion by 2030, advancing at a 6.38% CAGR.

Robust replacement demand from an ageing vehicle parc, tightening U.S.-Canada particulate and NOx limits, and migration toward premium cabin filtration underpin this steady expansion of the North America automotive air filters market. Cabin filters now dominate unit volumes because wildfire smoke episodes, urban smog, and prolonged daily commutes convert filtration from a maintenance chore into a health safeguard. Nanofiber media adoption accelerates as regulators press for higher filtration efficiency without airflow penalties, while online retail reshapes route-to-market economics by giving consumers transparent pricing and choice. At the same time, the rising share of battery electric vehicles erodes long-term engine-intake filter volumes, forcing suppliers to pivot toward HEPA cabin, thermal-management, and smart-sensor products within the North American automotive air filters market.

North America Automotive Airfilters Market Trends and Insights

Stricter U.S.-Canada PM & NOx Emission Norms Drive Filter Upgrade Cycles

U.S. EPA light- and medium-duty standards for model years 2027-2032 push fleet average CO2 targets to 85 g/mile, compelling automakers to specify higher-efficiency engines and cabin media that capture finer particulates without throttling airflow.California's Advanced Clean Cars II waiver, approved in December 2024, further tightens regional benchmarks that sooner or later cascade across the North American automotive air filters market. Nanofiber composites benefit by delivering the required capture efficiency with lower pressure drop, preserving fuel economy. Suppliers capable of documenting filtration performance under the tougher PM2.5 limit of 9 µg/m3 secure pricing power, whereas legacy cellulose lines suffer margin compression. Heavy-duty standards effective from 2027 raise durability and warranty thresholds, nudging light-duty buyers to perceive long-life filters as baseline value, reinforcing premium tiers within the North America automotive air filters market.

Rapid Cabin-Air Quality Awareness Post-Wildfire Seasons

Record wildfire smoke in 2024 blanketed California, Oregon, and British Columbia for weeks, pushing particulate readings above health-alert thresholds and igniting consumer demand for HEPA-grade cabin filters. State policy reviews now mandate high-efficiency filtration for buildings exposed to smoke plumes.That same mindset spills onto driveways: commuters treat vehicles as rolling shelters and seek filters with viral, allergen, and smoke removal claims. Mass-market OEMs respond by offering multi-layer cabin cartridges once limited to luxury trims, while aftermarket players package retrofit kits for older models. Promotional campaigns highlight World Health Organization PM2.5 guidance and children's respiratory health to justify a premium upsell. The feedback loop tightens as navigation apps overlay smoke maps, nudging drivers to activate recirculation and reminding them to change filters. This human-health narrative cements Cabin Media as the North American automotive air filter market's heartbeat.

Long-Life Washable Cotton Gauze Filters Cannibalizing Replacements

Reusable cotton-gauze filters marketed by performance brands extend service life from 12 months to nearly 5 years. Enthusiasts appreciate airflow gains and sustainability messaging, especially in desert states where dust traditionally forces frequent swaps. Retailers emphasize 50,000-mile warranties and lifetime cost savings, pulling value away from conventional paper lines. Mainstream uptake remains capped by a higher upfront price and the messy oil-recharge process that can foul mass-airflow sensors. Nevertheless, even modest conversion rates shave volumes in the aftermarket segment of the North America automotive air filters market. Manufacturers counter by launching drop-in washable cabin filters with antimicrobial linings, recapturing revenue while aligning with circular-economy goals.

Other drivers and restraints analyzed in the detailed report include:

- EV/HV Platforms Adopting Dedicated HEPA Cabin Filters

- Integration of IoT-Enabled Smart Filters With Predictive Replacement Apps

- BEV Adoption: Eliminating Engine-Intake Filter Demand By 2035

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nanofiber composites held a modest slice in 2024 yet are on course for 8.30% CAGR, the fastest of any material, as regulators focus on PM2.5 capture. While Paper/Cellulose still accounts for 43.25% of the North American automotive air filters market, paper and cellulose struggle to meet new efficiency targets without thickening pleats that choke airflow. Electrospun nanofibers remove 99.9998% of 300-500 nm particles at low pressure drop, a metric validated in Macromolecular Materials and Engineering studies. Suppliers blend nanofiber coatings with cellulose cores to keep costs palatable and to use existing production lines. Sustainability pressures add complexity: plant-based polymers and recycled cellulose draw R&D funding as OEMs pursue carbon-neutral supply chains. Graphene-oxide-reinforced cellulose nanofibers delivered 99.98% capture in laboratory tests while biodegrading in soil, signaling pathways for future mainstream deployment.

Price volatility in polypropylene and pulp hampers smaller firms with weak hedging strategies, pushing them toward contract manufacturing or specialty niches. Vertically integrated multinationals with pulp plantations and resin plants enjoy cost leverage and can experiment with hybrid stacks mixing melt-blown, spunbond and electrospun layers. Over 2025-2030, nanofiber adoption trickles down from turbo-gasoline SUVs into light commercial vans, raising the North America automotive air filters market size captured by the material from single digits to mid-teens by decade's end.

Cabin filters already control 55.10% of revenue. They are fighting engine-intake filters for every incremental dollar, a rare instance where a comfort feature outranks a drivetrain component in the North America automotive air filters market. Cabin units grow 7.50% CAGR, boosted by wildfire smoke, pandemics, and HEPA positioning. Engine filters remain essential for sold internal-combustion vehicles but confront longer service intervals and gradual volume attrition as BEVs scale. Research from the U.S. Department of Energy sets energy factors for air cleaners, indirectly nudging automotive engineers toward higher CADR (clean air delivery rate) targets. Automotive cabins copy home-air-purifier marketing language: multi-layer particulate-carbon-antimicrobial stacks, smartphone-controlled recirculation, and LED life indicators. Suppliers differentiate by impregnating activated carbon with copper or silver ions, promising viral inactivation within minutes, a claim validated by ISO 18184 tests. This technology shift cements cabin filters as the North America automotive air filter market's economic growth engine.

Despite the glamour around HEPA, mass-market vehicles continue to ship with particulate-only cabin filters that comply with cost ceilings. The aftermarket fills the gap: 30% of replacement cabin filters sold online in 2025 carry carbon or HEPA upgrades. As a result, distributors watch average selling price climb while the volume mix changes, improving margin contribution even as BEVs delete engine filters.

The North America Automotive Air Filters Market is Segmented by Material Type (Paper / Cellulose, Synthetic Gauze / Cotton, and More), Filter Type (Intake Filters and Cabin Filters), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEMs and Aftermarket) and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Mann+Hummel

- Donaldson Company

- Purolator Filters LLC

- K&N Engineering

- AIRAID (Truck Hero)

- S&B Filters Inc.

- Mahle GmbH

- Bosch Automotive Aftermarket

- Denso Corporation

- Cummins Filtration

- Fram Group

- Clarcor (Part of Parker-Hannifin)

- ACDelco (GM)

- AFE Power

- Wix Filters

- Sogefi Group

- H&V (Engineered Media)

- Roki Co., Ltd.

- Champion Laboratories

- Luber-finer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter U.S.-Canada PM & NOx emission norms (EPA Tier-3, CARB LEV III)

- 4.2.2 Rapid cabin-air quality awareness post-wildfire seasons

- 4.2.3 Ageing light-vehicle parc greater than 12.5 yrs fueling aftermarket volumes

- 4.2.4 EV/HV platforms adopting dedicated HEPA cabin filters

- 4.2.5 Integration of IoT-enabled smart filters with predictive replacement apps

- 4.2.6 OEM shift toward low-restriction nanofiber engine media for turbo-gasoline SUVs

- 4.3 Market Restraints

- 4.3.1 Long-life washable cotton gauze filters cannibalising replacements

- 4.3.2 BEV adoption eliminating engine-intake filter demand by ~2035

- 4.3.3 Polypropylene & cellulose pulp price volatility squeezing margins

- 4.3.4 Proliferation of counterfeit e-commerce filters undermining branded share

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Material Type

- 5.1.1 Paper/Cellulose

- 5.1.2 Synthetic Gauze/Cotton

- 5.1.3 Foam

- 5.1.4 Nanofiber Composite

- 5.1.5 Others (Activated Carbon, Metal Mesh)

- 5.2 By Filter Type

- 5.2.1 Intake (Engine) Air Filters

- 5.2.2 Cabin Air Filters

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCV)

- 5.3.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.4.2.1 Independent Aftermarket

- 5.4.2.2 Authorized Service Centers

- 5.4.2.3 Online Retail

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mann+Hummel

- 6.4.2 Donaldson Company

- 6.4.3 Purolator Filters LLC

- 6.4.4 K&N Engineering

- 6.4.5 AIRAID (Truck Hero)

- 6.4.6 S&B Filters Inc.

- 6.4.7 Mahle GmbH

- 6.4.8 Bosch Automotive Aftermarket

- 6.4.9 Denso Corporation

- 6.4.10 Cummins Filtration

- 6.4.11 Fram Group

- 6.4.12 Clarcor (Part of Parker-Hannifin)

- 6.4.13 ACDelco (GM)

- 6.4.14 AFE Power

- 6.4.15 Wix Filters

- 6.4.16 Sogefi Group

- 6.4.17 H&V (Engineered Media)

- 6.4.18 Roki Co., Ltd.

- 6.4.19 Champion Laboratories

- 6.4.20 Luber-finer

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

高效能空气微粒过滤器(HEPA)市场:按滤材类型、过滤器类型、过滤等级、应用、最终用户和分销管道划分,全球预测(2026-2032年)

高效能空气微粒过滤器(HEPA)市场:按滤材类型、过滤器类型、过滤等级、应用、最终用户和分销管道划分,全球预测(2026-2032年) 汽车空气滤清器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车空气滤清器:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球汽车空气滤清器市场规模、份额、趋势和成长分析报告

2026-2034年全球汽车空气滤清器市场规模、份额、趋势和成长分析报告 汽车空气滤清器市场规模、份额、趋势及预测(按类型、动力方式、车辆类型、销售管道及地区划分),2026-2034年颗粒过滤器测试市场(按过滤器类型、过滤器材料、粒径范围、流速、终端用户产业和应用划分)-全球预测,2026-2032年

汽车空气滤清器市场规模、份额、趋势及预测(按类型、动力方式、车辆类型、销售管道及地区划分),2026-2034年颗粒过滤器测试市场(按过滤器类型、过滤器材料、粒径范围、流速、终端用户产业和应用划分)-全球预测,2026-2032年 引擎空气滤清器市场-全球产业规模、份额、趋势、机会和预测,按产品类型(进气滤清器和空调滤清器)、最终用途(乘用车和商用车)、地区和竞争格局划分,2020-2030年预测

引擎空气滤清器市场-全球产业规模、份额、趋势、机会和预测,按产品类型(进气滤清器和空调滤清器)、最终用途(乘用车和商用车)、地区和竞争格局划分,2020-2030年预测 活性碳空气过滤器:全球市占率排名、总销售额和需求预测(2025-2031年)商用车空气滤清器市场按产品、滤芯类型、滤芯形状、车辆类型和最终用途划分-全球预测,2025-2032年汽车空气滤清器市场(按滤清器材料、车辆类型、滤清器类型、技术和最终用户划分)—2025-2032 年全球预测

活性碳空气过滤器:全球市占率排名、总销售额和需求预测(2025-2031年)商用车空气滤清器市场按产品、滤芯类型、滤芯形状、车辆类型和最终用途划分-全球预测,2025-2032年汽车空气滤清器市场(按滤清器材料、车辆类型、滤清器类型、技术和最终用户划分)—2025-2032 年全球预测 2032年汽车引擎空气滤清器市场预测:按类型、车辆类型、燃料类型、销售管道、应用和地区进行全球分析

2032年汽车引擎空气滤清器市场预测:按类型、车辆类型、燃料类型、销售管道、应用和地区进行全球分析