|

市场调查报告书

商品编码

1836602

太阳能控制窗膜:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Solar Control Window Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

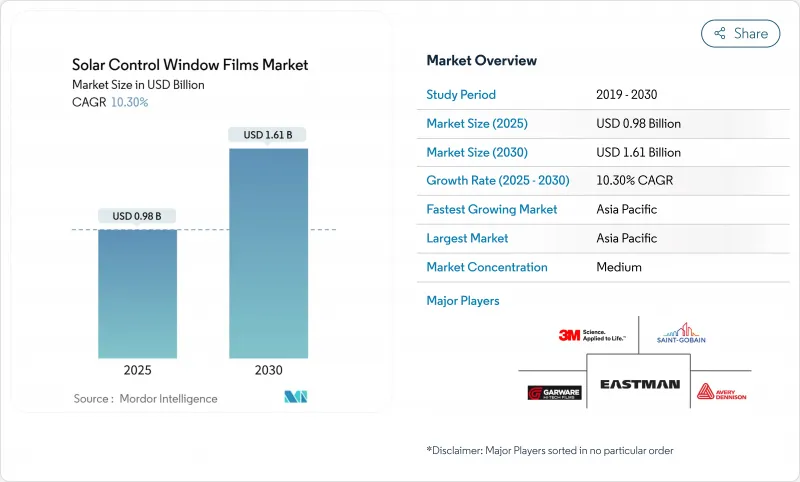

预计 2025 年太阳能控制窗膜市场规模为 9.8 亿美元,到 2030 年将达到 16.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.30%。

真空镀膜反射产品在目前的规格中占据主导地位,兼具高红外线阻隔性和中性美感,而陶瓷-金属混合材料则在极端温度波动的气候条件下提升了性能阈值。亚太地区的建筑热潮、欧盟的净零排放法规以及美国的财政激励措施,都在共同推动销售成长,即便原料成本波动。这些因素正在强化太阳能控制窗膜市场,使其成为提升更广泛能源效率价值的关键槓桿。

全球太阳能控制窗膜市场趋势与洞察

越来越重视减少碳足迹

企业气候承诺正在推动太阳能控制窗膜市场的发展,因为这些薄膜可降低5-15%的冷却负荷,并合格基于科学的排放目标。尖峰需求的降低与炎热气候下的电网弹性目标一致。房地产投资信託基金也将嵌装玻璃升级视为资产增值手段,而非延期维护。随着可再生能源的普及,像膜这样的需求侧解决方案因稳定负载曲线而声名鹊起。即使在资本支出放缓的时期,这种定位也能稳固采购预算。

欧洲净零建筑标准推动Low-E薄膜的采用

主要亮点

- 欧盟修订的《建筑能源效率指令》要求成员国每年维修3%的公共部门占地面积,以在2050年前达到零排放标准。改造窗膜是一项关键目标,它可以在不更换昂贵窗框的情况下提高隔热性能。跨国公司目前正在亚洲和北美复製相同的外墙标准,将欧洲基准输出到世界各地。生命週期碳排放条款也更倾向于薄膜维修,而非高含量碳嵌装玻璃替代品。因此,供应商预计将在公共竞标中获得更长的订单。

高端商业大厦动态智慧嵌装玻璃的替代风险

主要亮点

- 电致变色和感温变色装置可动态调节玻璃色调,达到静态薄膜无法比拟的眩光抑制效果。随着製造成本的下降,建筑幕墙顾问越来越多地在高端计划中将这些系统指定用于双层幕墙和单元式幕墙。虽然价格溢价通常仅为薄膜安装的3-5倍,但长期能源模拟结果通常更倾向于动态控制。薄膜製造商正加大对中阶市场的行销力度,并拓展智慧玻璃的维修管道,在这些领域,智慧玻璃的投资回收期可能超过12年。

报告中分析的其他驱动因素和限制因素

- 亚太地区建设产业快速成长

- 紫外线防护与健康问题

- 在炎热潮湿的气候条件下发生分层的保固相关责任。

細項分析

真空镀膜反射产品将占2024年市场收入的43%,复合年增长率达10.62%,将推动该细分市场的太阳能控制窗膜市场规模远超过有色和透明窗膜。建筑师青睐能够选择性反射近红外光并透射可见光的超薄金属迭层。

薄膜製造商目前正在部署采用银、铟和镍合金的溅镀腔体,以实现0.20或更低的发射率。对于多用户住宅维修,染色聚酯薄膜因其初期价格实惠而仍然具有吸引力,但日益严格的能源法规正在逐步推动反射结构的应用。

陶瓷吸收器占2024年销售额的46%,这反映了其颜色稳定性、高熔点和可忽略的高频干扰。汽车原始设备製造商青睐奈米陶瓷层,以避免远端资讯处理天线的讯号衰减。然而,随着精製金属奈米颗粒分散体降低製造成本并恢復除雾器网格的导电优势,阳光控制窗膜的市场份额优势可能会下降。

纯金属薄膜的复合年增长率达10.56%,这得益于溅镀堆迭技术的改进,该技术可有效减少虹彩效应。如今,混合架构将氧化铝或二氧化硅沉积在银种子层上,形成一种兼具低反射率和高红外线阻隔率的复合光学堆迭。这些进步正在模糊历史界限,推动该类别朝着特定功能配方、眩光抑制、防涂鸦和光伏覆盖层的方向发展。

区域分析

亚太地区仍将是太阳能控制窗膜市场的重心,到2024年将占全球太阳能控制窗膜市场收益的45%,复合年增长率为10.78%。中国绿色建筑评估标准GB/T 50378和印度的Eco-Niwas标准都已规定了太阳能得热係数,这将加速高选择性膜材的普及。

北美已经建立了完善的维修奖励,加州的第 24 条修正案提高了薄膜在不改变建筑幕墙外观的情况下可以满足的外部遮阳係数阈值。

欧洲保持着成熟的渗透率,但也正在享受与 2030 年「适合 55 岁」气候方案相关的第二波需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查结果

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 人们对减少碳足迹的兴趣日益浓厚

- 欧洲净零建筑标准推动Low-E薄膜的广泛应用

- 亚太地区建设产业的成长

- 紫外线防护与健康问题

- 亚太地区电子商务仓库建设激增,需要采光控制

- 市场限制

- 高端商业大厦动态智慧嵌装玻璃的替代风险

- 炎热潮湿气候下分层的保固相关责任

- 聚酯和奈米陶瓷原料价格不稳定

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争的激烈程度

- 定价分析

第五章 市场规模及成长预测(金额)

- 按影片类型

- 透明(不反光)

- 染色(不反光)

- 真空镀膜(反射型)

- 高性能薄膜

- 其他电影类型

- 按吸收剂类型

- 有机的

- 无机/陶瓷

- 金属

- 按安装阶段

- 新建筑

- 改装

- 按最终用户产业

- 建造

- 车

- 海洋

- 设计

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 西班牙

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- 3M

- Avery Dennison Corporation

- Decorative Films, LLC

- Eastman Chemical Company

- Garware Hi-Tech Films

- Johnson Window Films, Inc.

- LINTEC Corporation

- Madico

- Polytronix, Inc.

- Purlfrost

- Saint-Gobain

- Sharpline Converting, Inc.

- SOLAR CONTROL FILMS INC

- Thermolite, LLC

- TintFit Window Films Ltd.

- TORAY INDUSTRIES, INC.

- Ziebart International

第七章 市场机会与未来展望

The Solar Control Window Films Market size is estimated at USD 0.98 billion in 2025, and is expected to reach USD 1.61 billion by 2030, at a CAGR of 10.30% during the forecast period (2025-2030).International decarbonization rules, rising utility costs, and proven payback periods below three years keep demand resilient.

Vacuum-coated reflective products dominate current specifications because they combine high infrared rejection with neutral aesthetics, while ceramic-metallic hybrids push performance thresholds in climates with extreme temperature swings. Asia Pacific construction booms, EU net-zero mandates, and US fiscal incentives all converge to keep volumes expanding even when raw-material costs fluctuate. These forces collectively reinforce the solar control window films market as a pivotal lever in the wider energy-efficiency value.

Global Solar Control Window Films Market Trends and Insights

Growing Emphasis on Reducing Carbon Footprints

Corporate climate pledges elevate the solar control window films market because films shave 5-15% cooling loads and qualify for science-based emission targets. Peak-demand trimming aligns neatly with grid-resilience objectives in hot regions. Real-estate investment trusts also treat glazing upgrades as accretive to asset value rather than as deferred maintenance. As renewable penetration accelerates, demand-side solutions such as films gain prestige for stabilizing load profiles. This positioning solidifies procurement budgets even during capex slowdowns.

Net-Zero Building Codes in Europe Driving Low-E Film Adoption

Key Highlights

- The EU's recast Energy Performance of Buildings Directive compels member states to renovate 3% of public-sector floor area annually and to meet zero-emission standards by 2050. Retro-orientated targets elevate window films by boosting thermal performance without costly frame replacement. Multinationals now replicate the same envelope standards in Asia and North America, exporting European benchmarks worldwide. Lifecycle-carbon clauses also favor thin-film retrofits over high-embodied-carbon glazing swaps. Consequently, suppliers see longer order visibility in public tenders.

Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers

Key Highlights

- Electrochromic and thermochromic units dynamically tint glass, providing glare mitigation that static films cannot match. As manufacturing costs fall, facade consultants increasingly specify these systems for double-skin or unitized curtain walls in prestige projects. Although price premiums remain 3-5 times film installations, long-term energy simulations often favor dynamic controls. Film suppliers respond by sharpening mid-market pitches and expanding retrofit channels where smart glass paybacks extend beyond 12 years.

Other drivers and restraints analyzed in the detailed report include:

- Upsurge in the Asia-Pacific Construction Industry

- Awareness of UV Protection and Health Concerns

- Warranty-Linked Liability for Delamination in Hot-Humid Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vacuum-coated reflective products captured 43% of 2024 revenue, and their 10.62% CAGR keeps the solar control window films market size for this segment well ahead of dyed and clear alternatives. Architects value the micro-thin metallic stack that selectively reflects near-infrared while admitting visible light.

Film manufacturers now deploy sputter chambers using silver, indium, and nickel alloys that achieve emissivity below 0.20. In mass-housing retrofits, dyed polyester films still appeal for initial affordability, yet energy-code tightening steadily redirects volume to reflective constructions.

Ceramic absorbers held 46% of 2024 revenue, reflecting their color stability, high melting point, and negligible radio-frequency interference. Automotive OEMs favor nano-ceramic layers because they avoid signal attenuation for telematics antennas. The solar control window films market share advantage may narrow, however, as refined metallic nanoparticle dispersions cut manufacturing costs and restore conductivity benefits for defogger grids.

Metallic-only films are marching at 10.56% CAGR, aided by sputter stack refinements that curb iridescence. Hybrid architectures now deposit alumina or silica atop silver seed layers, creating composite optical stacks that combine low reflectance with steep infrared rejection. Such progress blurs historic boundaries and pushes the category toward function-specific formulations, glare suppression, anti-graffiti, or photovoltaic overlay.

The Solar Control Window Films Market Report Segments the Industry by Film Type (Clear, Dyed, Vacuum Coated, and More), Absorber Type (Organic, Inorganic/Ceramic, and Metallic), Installation (New-Build and Retrofit), End-User Industry (Construction, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

Asia Pacific commanded 45% of 2024 revenues and is expanding at a 10.78% CAGR, ensuring it remains the gravitational center of the solar control window films market. China's Green Building Evaluation Standard GB/T 50378 and India's Eco-Niwas mandate solar-heat-gain coefficients that accelerate high-selectivity film uptake.

Retrofit incentives anchor North America. The Inflation Reduction Act's enhanced tax deduction accelerates envelope upgrades across federal and private portfolios, and California's Title 24 revisions elevate exterior-shade coefficient thresholds that thin films meet without altering facade appearance.

Europe maintains mature penetration yet enjoys a second wave of demand tied to the 2030 "Fit-for-55" climate package.

- 3M

- Avery Dennison Corporation

- Decorative Films, LLC

- Eastman Chemical Company

- Garware Hi-Tech Films

- Johnson Window Films, Inc.

- LINTEC Corporation

- Madico

- Polytronix, Inc.

- Purlfrost

- Saint-Gobain

- Sharpline Converting, Inc.

- SOLAR CONTROL FILMS INC

- Thermolite, LLC

- TintFit Window Films Ltd.

- TORAY INDUSTRIES, INC.

- Ziebart International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Study Deliverables

- 1.3 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Emphasis on Reducing Carbon Footprints

- 4.2.2 Net-Zero Building Codes in Europe Driving Low-E Film Adoption

- 4.2.3 Upsurge in the Asia-Pacific Construction Industry

- 4.2.4 Awareness of UV Protection and Health Concerns

- 4.2.5 Rapid E-Commerce Warehouse Construction Requiring Day-Lighting Control in APAC

- 4.3 Market Restraints

- 4.3.1 Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers

- 4.3.2 Warranty-Linked Liability for Delamination in Hot-Humid Climates

- 4.3.3 Volatile Polyester and Nano-Ceramic Raw Material Prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

- 4.6 Pricing Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Film Type

- 5.1.1 Clear (Non-reflective)

- 5.1.2 Dyed (Non-reflective)

- 5.1.3 Vacuum-Coated (Reflective)

- 5.1.4 High Performance Films

- 5.1.5 Other Film Types

- 5.2 By Absorber Type

- 5.2.1 Organic

- 5.2.2 Inorganic / Ceramic

- 5.2.3 Metallic

- 5.3 By Installation Stage

- 5.3.1 New-Build

- 5.3.2 Retrofit

- 5.4 By End-user Industry

- 5.4.1 Construction

- 5.4.2 Automotive

- 5.4.3 Marine

- 5.4.4 Design

- 5.4.5 Other End-user Industry

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 Spain

- 5.5.3.5 France

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Decorative Films, LLC

- 6.4.4 Eastman Chemical Company

- 6.4.5 Garware Hi-Tech Films

- 6.4.6 Johnson Window Films, Inc.

- 6.4.7 LINTEC Corporation

- 6.4.8 Madico

- 6.4.9 Polytronix, Inc.

- 6.4.10 Purlfrost

- 6.4.11 Saint-Gobain

- 6.4.12 Sharpline Converting, Inc.

- 6.4.13 SOLAR CONTROL FILMS INC

- 6.4.14 Thermolite, LLC

- 6.4.15 TintFit Window Films Ltd.

- 6.4.16 TORAY INDUSTRIES, INC.

- 6.4.17 Ziebart International

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Growing Concerns Regarding UV Protection

2026年全球太阳能隔热窗膜市场报告

2026年全球太阳能隔热窗膜市场报告 太阳能控制窗膜市场-全球产业规模、份额、趋势、机会和预测,按DWT、应用、类型、燃料、地区和竞争格局划分,2021-2031年预测

太阳能控制窗膜市场-全球产业规模、份额、趋势、机会和预测,按DWT、应用、类型、燃料、地区和竞争格局划分,2021-2031年预测 太阳能控制窗膜市场按产品类型、应用和分销管道划分-2025-2032年全球预测

太阳能控制窗膜市场按产品类型、应用和分销管道划分-2025-2032年全球预测 北美太阳能控制窗膜:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

北美太阳能控制窗膜:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 太阳能控制窗膜市场报告,按类型(有机、金属、陶瓷)、薄膜类型(透明、染色、真空镀膜等)、应用(建筑、汽车等)和地区划分,2025 年至 2033 年

太阳能控制窗膜市场报告,按类型(有机、金属、陶瓷)、薄膜类型(透明、染色、真空镀膜等)、应用(建筑、汽车等)和地区划分,2025 年至 2033 年 太阳能控制窗膜市场规模、份额、按产品类型、薄膜类型、吸收器类型、应用、地区分類的成长分析 - 2025 年至 2032 年产业预测

太阳能控制窗膜市场规模、份额、按产品类型、薄膜类型、吸收器类型、应用、地区分類的成长分析 - 2025 年至 2032 年产业预测 太阳能控制窗膜市场机会、成长动力、产业趋势分析与预测 2025 - 2034

太阳能控制窗膜市场机会、成长动力、产业趋势分析与预测 2025 - 2034