|

市场调查报告书

商品编码

1836614

非公路用车辆引擎:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Off Highway Vehicle Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

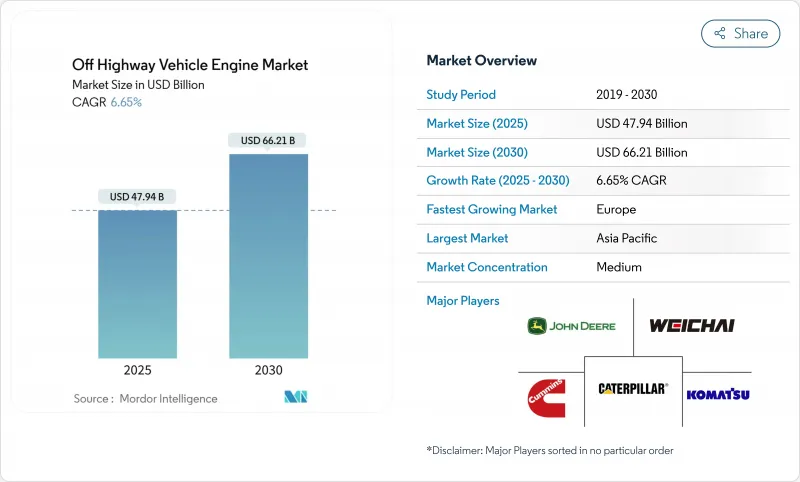

非公路用车辆引擎市场规模预计在 2025 年达到 479.4 亿美元,预计到 2030 年将达到 662.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.65%。

基础设施支出的增加、排放法规的日益严格以及农业、采矿和物料输送应用领域机械化程度的提高,正在重塑引擎需求。虽然成长仍然集中在柴油技术上,但得益于远端资讯处理、预测性维护以及与氢化植物油和可再生柴油的兼容性的快速发展,混合动力电动和燃料无关平台正在扩大其影响力。

全球非公路用车辆引擎市场趋势与洞察

庞大的全球基础设施管道(G7和BRI)

1.2兆美元的《基础设施投资与就业法案》推动美国中西部各州施工机械年销售额成长10%。中国「一带一路」倡议下的平行投资正在刺激非洲、东南亚和东欧地区对大型挖土机和推土机的需求。中国出口商预计,2023年施工机械的海外出货量将首次超过国内销售量,进而重新平衡全球供应链,并增强非公路用车引擎市场。多年的融资资源使製造商能够安心地扩大产能并改善混合动力相容设计。

亚太和非洲农业机械化进展

到2024年,拖拉机在南亚农场的普及率将达到74%,水泵和脱粒机的普及率将超过65%。印度和中国农村工资的上涨正推动农场转向资本密集模式,从而在30至120马力的范围内产生稳定的更换需求。撒哈拉以南非洲地区的机械化程度仍落后于南美洲,这意味着该地区拥有大量可在恶劣田间条件下可靠运作的小型、省油的引擎。服务型经营模式使小农户无需拥有机械即可使用,从而扩大了发动机供应商的市场覆盖范围,并进一步支持了非公路用车辆发动机市场。

加速小型机械电气化

到2024年,电动轮式装载机将占中国市场销量的10%,全球电动施工机械销售量将达到6,000至7,000台。多家中国原始设备製造商正在向100马力以下的传统引擎供应商施压,力求成本平价。欧洲都市区的柴油限购政策正在加速电池在室内拆除和废弃物作业中的应用。然而,由于柴油的能量密度高且需要快速加油,远距采矿、林业和24小时运作作业仍依赖柴油,这仍然非公路用车引擎市场的核心需求。

报告中分析的其他驱动因素和限制因素

- 更严格的 Stage V/Tier 5 标准引发预购与改装週期

- 原始设备製造商转向混合动力模组化引擎平台

- 后处理成本上升与价格敏感的买家

細項分析

2024年,施工机械将占非公路用车引擎市场收入的58.36%,这得益于政府针对道路、桥樑和运输系统的奖励策略。亚太地区的计划和美国资金的激增,正在支撑对依赖121-400马力缸体的挖土机、推土机和装载机的需求。随着铜、锂和镍计划的扩张以适应电池供应链,采矿设备正在復苏。林业和物料输送细分市场青睐约翰迪尔PowerTech™ PSS 9.0 L等发动机,该发动机在陡峭的地形中可提供高达330马力的动力。电动小型装载机的复合年增长率将达到6.27%,这表明在工作週期可预测且充电设施齐全的地区,早期电气化取得了成功。然而,大马力柴油机对于24小时不间断的运作铲车和地下运输仍然至关重要,这维持了非公路用车辆引擎市场的稳定。

欧洲轻型工程车辆正在采用远端资讯处理技术来减少怠速时间,从而降低12%的消费量并延长大修间隔。亚洲租赁业者青睐模组化发动机,以便于维护,在繁忙的都市区上减少停机时间。非洲的「一带一路」计划正在推动对90-200千瓦中阶引擎的需求,这些引擎兼具燃油效率和耐用性。拉丁美洲矿业巨头要求采用符合欧盟第五阶段标准的动力传动系统,以因应当地法规的收紧。这些动态共同推动施工机械保持其领先地位,并推动采矿设备逐步获得非公路用车辆引擎的市场份额。

2024年,31-70马力的引擎将占据非公路用车辆引擎市场份额的64.51%,到2030年的复合年增长率将达到7.02%。城市人口密集化需要高机动性的机器,这些机器能够适应狭窄的道路,并减少对已完工路面的附带损害。原始设备製造商正在整合启停功能和先进的燃油图,并声称其油耗降低了两位数,这对车队经理来说很有吸引力。远端资讯处理平台可以查看怠速时间,并允许无线参数微调,以满足当地的噪音和排放法规,而无需前往经销商。

采矿卡车和大型挖土机(卡特彼勒的 3512B-EUI(1,450 匹马力)仍然是该领域的标竿)使用 400 匹马力以上的高功率引擎。儘管产量低,但这些引擎价格昂贵,售后零件市场收入也很高。相反,30 马力以下的平台受电气化影响最大,因为现在电池组可以在草坪护理、高尔夫球场和小型市政运营中提供全班性能。因此,研发支出正转向支援非公路用车辆引擎市场的中阶产品,而高马力的 Prestige 系列则得以保留。

区域分析

受大型基础建设项目和农业机械化加速推动,2024年亚太地区销售额将维持38.17%的成长率。 2023年,中国施工机械出口量超过国内销量,缓解了国内市场的疲软,并为长沙和徐州生产的发动机创造了全球销售管道。在印度,政府补贴将提高拖拉机的可负担性,儘管季风波动较大,但2025年的零售量仍将增加。需求将偏向31-120马力的发动机,适用于拥挤的都市区工地和小块农田。区域原始设备製造商青睐获得Tier 3和Stage V认证的模组化发动机,使其无需重新设计即可出口到非洲和欧洲,从而增强了非公路用车发动机市场的扩充性。

欧洲的复合年增长率高达 7.19%,受益于第五阶段排放标准合规投资以及《绿色协议》对铁路、可再生能源和循环经济设施的关注。客户优先考虑具有被动再生功能的颗粒过滤器和整合碳计量板的远端资讯处理系统。日本小松公司的第五阶段产品组合已证明具有更长的免维护期,这对于面临严格运转率目标的租赁公司来说是一个极具吸引力的提案。欧洲各市政当局也试用氢燃料内燃机垃圾车,供应商也支持替代燃料的研发。

北美正在利用《基础设施投资与就业法案》来支持州际公路维修、桥樑更换和港口疏浚等项目对引擎的持续需求。加州即将推出的Tier 5排放法规将设定全球最严格的标准,促使原始设备製造商在实施数年后测试下一代SCR和氨感测器。南美、中东和非洲是高成长但成本敏感的地区。货币逆风和资金筹措缺口将限制短期内发动机的采用,但随着大宗商品週期改善以及多边金融机构对依赖从亚洲进口的可靠中马力发动机和在巴西翻新的发动机的道路、发电厂和灌溉项目的支持,发动机仍有上涨空间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 庞大的全球基础设施管道(G7和「一带一路」倡议)

- 亚太和非洲农业机械化进展

- 更严格的 Stage V/Tier 5 标准活性化预购和改装週期

- 原始设备製造商转向模组化混合动力引擎平台

- 远端资讯主导驱动的预测性维护缩短了更换週期

- HVO/可再生柴油相容性扩大了内燃机的相关性

- 市场限制

- 加速小型设备电气化

- 后处理成本上升以及来自价格敏感型买家的竞争

- 大宗商品价格波动对引擎净利率带来压力

- 租赁车队的检修间隔延长

- 价值/供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争的激烈程度

第五章市场规模与成长预测:价值(美元)

- 按车辆类型

- 农业机械

- 施工机械

- 矿山机械

- 林业和物料输送设备

- 按输出功率(HP)

- 30 HP 或更少

- 31-70 HP

- 71-120 HP

- 121-400 HP

- 超过400马力

- 按燃料类型

- 柴油引擎

- 汽油

- 天然气/沼气

- 混合动力/电动/燃料电池

- 按引擎排气量(L)

- 2L以下

- 2.1~3.5 L

- 3.6~7 L

- 7公升或更多

- 依推进技术

- 传统内燃机

- 杂交种

- 电池电动

- 燃料电池电力

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 土耳其

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 市占率分析

- 公司简介

- AGCO Corporation

- Caterpillar Inc.

- Cummins Inc.

- Deere & Company

- Deutz AG

- Komatsu Ltd

- Mahindra Powertrain

- Scania AB

- Volvo Penta

- Yanmar Co.

- Weichai Power

- Kubota Corporation

- Perkins Engines

- MAN Engines

- Rolls-Royce Power Systems(MTU)

- Doosan Infracore

- FPT Industrial

- Kohler Engines

- Hatz Diesel

第七章 市场机会与未来展望

The Off Highway Vehicle Engine Market size is estimated at USD 47.94 billion in 2025, and is expected to reach USD 66.21 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030).

Increasing infrastructure spending, tighter emission rules, and rising mechanization across agriculture, mining, and material-handling applications are reshaping engine demand. Growth remains anchored in diesel technology but hybrid-electric and fuel-agnostic platforms are widening their footprint, helped by rapid progress in telematics, predictive maintenance, and compatibility with hydrotreated vegetable oil and renewable diesel fuels.

Global Off Highway Vehicle Engine Market Trends and Insights

Massive Global Infrastructure Pipeline (G7 & BRI)

The USD 1.2 trillion Infrastructure Investment and Jobs Act is driving annual construction equipment sales growth of 10% across the US Midwest states. Parallel investments under China's Belt and Road Initiative stimulate demand for heavy excavators and bulldozers across Africa, Southeast Asia, and Eastern Europe. Chinese exporters shipped more construction machines abroad than they sold domestically for the first time in 2023, rebalancing global supply chains and reinforcing volume in the off-highway vehicle engine market. Multi-year funding windows enable manufacturers to scale capacity and refine hybrid-ready designs with confidence.

Growing Mechanization of Agriculture in Asia-Pacific and Africa

Tractor penetration reached 74% of South Asian farms in 2024, while water pumps and threshers exceeded 65% adoption. Rising rural wages across India and China push farms toward capital-intensive practices, creating steady replacement demand in the 30-120 HP range. Sub-Saharan Africa still trails South America in mechanization, signaling a sizeable addressable pool for compact, fuel-efficient engines that perform reliably in harsh field conditions. Service-oriented business models allow smallholders to access machinery without ownership, broadening market reach for engine suppliers and further supporting the off-highway vehicle engine market.

Accelerating Electrification of Compact Equipment

Electric wheel loaders captured 10% of Chinese sales in 2024, with 6,000-7,000 electric construction machines sold worldwide. Cost parity achieved by several Chinese OEMs pressures legacy engine providers in the sub-100 HP class. European urban zones restrict diesel, accelerating battery adoption for indoor demolition and waste-handling tasks. However, long-haul mining, forestry, and 24-hour quarry operations still rely on diesel due to energy density and quick refueling needs, preserving core demand inside the off highway vehicle engine market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Stage V / Tier 5 Norms Triggering Pre-buy & Retrofit Cycles

- OEM Shift to Modular Hybrid-Ready Engine Platforms

- Escalating After-treatment Cost vs. Price-Sensitive Buyers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Construction equipment generated 58.36% of 2024 off-highway vehicle engine market revenue, a position fortified by government stimulus in roads, bridges, and transit systems. Asia Pacific megaprojects, together with the US funding surge, sustain demand for excavators, dozers, and loaders that rely on 121-400 HP blocks. Mining equipment shows renewed momentum because copper, lithium, and nickel projects expand to meet battery supply chains. Forestry and materials-handling niches favor engines like the John Deere PowerTech(TM) PSS 9.0 L delivering up to 330 hp in steep terrain. Electric compact loaders post a 6.27% CAGR, illustrating early electrification success where duty cycles and charging access are predictable. Nevertheless, high-horsepower diesel remains essential for round-the-clock mining shovels and underground haulage, upholding volume in the off highway vehicle engine market.

Compact construction fleets in Europe adopt telematics to trim idle hours, cutting fuel burn by 12% and extending overhaul intervals. Asian rental operators prefer modular engines with easy service access, keeping downtime low on busy urban sites. Belt and Road projects in Africa pull demand for mid-range 90-200 kW engines that balance fuel efficiency and toughness. Mining majors in Latin America request EU Stage V compliant powertrains to future-proof assets against tightening local rules. Together, these dynamics keep construction equipment in pole position while mining gradually widens its share of the off highway vehicle engine market.

The 31-70 HP category held 64.51% of off-highway vehicle engine market share in 2024 and records a 7.02% CAGR to 2030, fueled by compact excavators, skid-steers, and mid-size tractors used in rice paddies and horticulture. Urban densification calls for maneuverable machinery that fits narrow streets and reduces collateral damage on finished surfaces. OEMs integrate start-stop functions and advanced fuel maps, claiming double-digit consumption cuts that appeal to fleet managers. Telematics platforms visualize idle time and enable over-the-air parameter tweaks to meet local noise or emission constraints without dealership visits.

Higher brackets above 400 HP serve mining trucks and large hydraulic shovels, segments where Caterpillar's 3512B-EUI at 1,450 hp remains a benchmark. Despite lower unit volumes, these engines command premium pricing and aftermarket parts revenue. Conversely, sub-30 HP platforms suffer most from electrification encroachment because battery packs now deliver full-shift performance for lawn care, golf course, and small municipal tasks. The resulting polarization directs R&D spending toward mid-range products that anchor the off highway vehicle engine market while preserving high-horsepower prestige lines.

The Off Highway Vehicle Engine Market Report is Segmented by Vehicle Type (Agricultural Machinery and More), Power Output (Less Than or Equal To 30 HP, 31-70 HP, and More), Fuel Type (Diesel, Gasoline, and More), Engine Displacement (Less Than or Equal 2 L, 2. 1 To 3. 5 L, and More), Propulsion Technology (Conventional ICE and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained 38.17% revenue in 2024 due to large-scale infrastructure programs and accelerating farm mechanization. China exported more construction equipment than it sold at home during 2023, cushioning domestic softness and creating a global channel for engines produced in Changsha and Xuzhou. India's government subsidies improve tractor affordability, lifting 2025 retail volumes despite monsoon variability. Demand skews toward 31-120 HP units maneuvering in congested urban job sites or small farm plots. Regional OEMs favor modular engines certified for both Tier 3 and Stage V so they can ship to Africa or Europe without re-engineering, reinforcing the scalability of the off-highway vehicle engine market.

Europe, growing at 7.19% CAGR, benefits from Stage V compliance investments and the Green Deal's focus on rail, renewable energy, and circular economy facilities. Customers prioritize particulate filters with passive regeneration and telematics, integrating carbon accounting dashboards. Komatsu's Stage V portfolio demonstrates maintenance-free operation for a longer duration, a compelling proposition for rental firms facing tight utilization targets. European municipalities also pilot hydrogen ICE refuse trucks, supporting supplier R&D in alternative fuels.

North America capitalizes on the Infrastructure Investment and Jobs Act, which underwrites sustained engine demand for interstate highway revamps, bridge replacements, and port dredging. California's forthcoming Tier 5 rules set the strictest global bar, pushing OEMs to test next-generation SCR and ammonia sensors several years ahead of enforcement. South America, the Middle East, and Africa represent high-growth but cost-sensitive regions. Currency headwinds and financing gaps limit immediate penetration yet offer upside as commodity cycles improve and multilateral lenders sponsor roads, power plants, and irrigation schemes that rely on reliable medium-horsepower engines imported from Asia or remanufactured in Brazil.

- AGCO Corporation

- Caterpillar Inc.

- Cummins Inc.

- Deere & Company

- Deutz AG

- Komatsu Ltd

- Mahindra Powertrain

- Scania AB

- Volvo Penta

- Yanmar Co.

- Weichai Power

- Kubota Corporation

- Perkins Engines

- MAN Engines

- Rolls-Royce Power Systems (MTU)

- Doosan Infracore

- FPT Industrial

- Kohler Engines

- Hatz Diesel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Massive global infrastructure pipeline (G7 & BRI)

- 4.2.2 Growing mechanization of agriculture in Asia-Pacific and Africa

- 4.2.3 Stricter Stage V / Tier 5 norms triggering pre-buy & retrofit cycles

- 4.2.4 OEM shift to modular hybrid-ready engine platforms

- 4.2.5 Telematics-driven predictive maintenance shortening replacement cycles

- 4.2.6 HVO/renewable-diesel compatibility extending ICE relevance

- 4.3 Market Restraints

- 4.3.1 Accelerating electrification of compact equipment

- 4.3.2 Escalating after-treatment cost vs. price-sensitive buyers

- 4.3.3 Commodity-price volatility squeezing engine margins

- 4.3.4 Rental fleets extending overhaul intervals

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Agricultural Machinery

- 5.1.2 Construction Equipment

- 5.1.3 Mining Equipment

- 5.1.4 Forestry & Material-Handling Equipment

- 5.2 By Power Output (HP)

- 5.2.1 Less than or equal to 30 HP

- 5.2.2 31-70 HP

- 5.2.3 71-120 HP

- 5.2.4 121-400 HP

- 5.2.5 More than 400 HP

- 5.3 By Fuel Type

- 5.3.1 Diesel

- 5.3.2 Gasoline

- 5.3.3 Natural-/Bio-Gas

- 5.3.4 Hybrid-Electric & Fuel-Cell

- 5.4 By Engine Displacement (L)

- 5.4.1 Less than or equal 2 L

- 5.4.2 2.1 to 3.5 L

- 5.4.3 3.6 to 7 L

- 5.4.4 More than 7 L

- 5.5 By Propulsion Technology

- 5.5.1 Conventional ICE

- 5.5.2 Hybrid

- 5.5.3 Battery-Electric

- 5.5.4 Fuel-Cell Electric

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.3.1 AGCO Corporation

- 6.3.2 Caterpillar Inc.

- 6.3.3 Cummins Inc.

- 6.3.4 Deere & Company

- 6.3.5 Deutz AG

- 6.3.6 Komatsu Ltd

- 6.3.7 Mahindra Powertrain

- 6.3.8 Scania AB

- 6.3.9 Volvo Penta

- 6.3.10 Yanmar Co.

- 6.3.11 Weichai Power

- 6.3.12 Kubota Corporation

- 6.3.13 Perkins Engines

- 6.3.14 MAN Engines

- 6.3.15 Rolls-Royce Power Systems (MTU)

- 6.3.16 Doosan Infracore

- 6.3.17 FPT Industrial

- 6.3.18 Kohler Engines

- 6.3.19 Hatz Diesel

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment