|

市场调查报告书

商品编码

1836637

汽车气动致动器:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Automotive Pneumatic Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

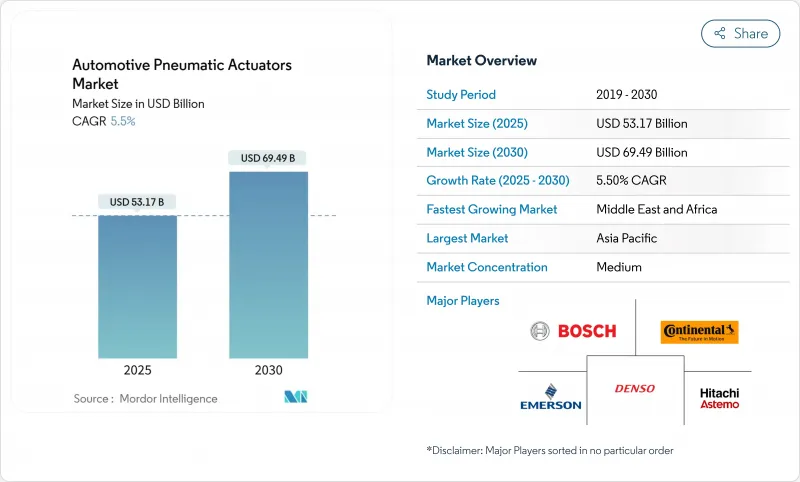

预计 2025 年汽车气动致动器市场规模为 531.7 亿美元,到 2030 年将达到 694.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.50%。

儘管面临节能电动致动器的竞争,汽车製造商仍依赖气动元件来实现安全、动力传动系统和底盘功能。更严格的排放法规和日益普及的ADAS(高级驾驶辅助系统)正在推动气动元件的需求,亚太地区凭藉其强大的供应链引领市场。同时,由于本地组装专案的扩张,中东、非洲和南美洲也正在经历快速成长。

全球汽车气动致动器市场趋势与洞察

更严格的排放法规鼓励精确的空燃比控制

美国环保署 (EPA) 第三阶段重型车辆法规将于 2024 年生效,该法规将收紧氮氧化物基准值,迫使柴油机製造商改进依赖高解析度气动阀门的废气再循环 (EGR) 和计量策略。在欧洲,类似的欧 7 草案将引发需求高峰。实验室测试将被现场检验测试取代,致动器必须在实际振动和温度变化下保持精确度。拥有可闭合数位回馈迴路的电动气动套件的供应商将在竞标中享有明显优势。监管时间表将加快中标决策,并确保整个预测期内的收益可见度。

全球汽车产量增加

随着轻型和重型车辆产量的增加,每个组装单元都将配备多个致动器点,从而推高所有气压应用的基准需求。日本汽车工业协会 (JAMA) 已确认,2025 年原始设备製造商 (OEM) 的时间表包括在煞车、油门和 EGR 迴路中整合气动解决方案,以确保燃油效率和合规性。平台共用将进一步扩大产量,因为现在可以在同级车型中安装单一致动器系列,从而提高供应商的规模经济效益。西方製造商正在将组装转移到东南亚,促使致动器製造商将模组化生产线设在同一地点。因此,即使竞争对手的电动致动器提高了成本提案,产量的復苏也确保了汽车气动致动器市场的短期成长。

转向节能电动致动器

机电系统将电池电能转换为运动,效率高达 80%。这种差异在电动车中更为明显,每节省一瓦电,就意味着续航里程的增加。生产线製造商也将焊接机器人和物料输送臂迁移到电动缸,以提高路径精度。然而,在压缩空气已整合到汽车平臺的重载节点(例如重型卡车的气压煞车)中,气动技术仍然占据主导地位。因此,供应商正在致力于开发混合技术致动器,该执行器结合了低能耗位置控制,同时保留了基于压力的力道。

报告中分析的其他驱动因素和限制因素

- ADAS 的普及需要精确的驱动

- 减轻重量以提高燃油效率的趋势

- 气动复杂性与高维修成本

細項分析

2024年,煞车气室和驻车煞车卡钳单元将占汽车气动致动器市场的31.50%。所有乘用车和商用车都必须配备这些零件,这巩固了基准基线。儘管电子机械驻车煞车正在豪华轿车领域取得进展,但重型卡车的鼓式煞车仍然依赖气室来实现高扣夹力和低单位成本。涡轮增压器排气泄压阀致动器将是成长最快的领域,复合年增长率为6.70%。油门、暖通空调混合门和废气再循环蝶阀将保持中等个位数成长,这主要受监管或舒适性需求的驱动。

气动燃油喷射轨道调节器在巴西流行的灵活燃料布局中依然存在,门锁柱塞在成本敏感的掀背车中仍然很常见。供应商正在尝试将智慧压力感测器嵌入致动器主体,以便将健康数据输入车辆控製网路。即使在直接电动马达驱动缩小竞争差距的情况下,此增强功能仍能延长气动设备的使用寿命。总体而言,由于多种应用,汽车气动致动器市场仍维持着数十亿美元的收入。

2024年,乘用车将占汽车销售量的56.70%,反映了全球工厂的高产量。然而,重型商用车预计将以5.90%的复合年增长率推动汽车气动致动器市场规模的扩张。车队营运商重视空气煞车和空气悬吊迴路在高强度工作循环下的耐用性,而更严格的二氧化碳排放法规要求优化压缩机管理,而非全面更换技术。轻型商用厢型车将实现强劲的复合年增长率,这主要得益于电商小包裹需求和城市物流的成长。施工机械和采矿设备主要需要耐高温排气阀控制设备和坚固的转向稳定器。

虽然摩托车仍然是一个集中在部分亚洲经济体的微型细分市场,但Scooter原始设备製造商正在试验低压气动伺服系统,用于自动离合器执行。郊区乘用车因其NVH优势而倾向于紧凑型电动驱动,而重型车辆则因其力密度和久经考验的耐用性而保留气压驱动。这种脱节将影响一级供应商未来的平台策略,迫使他们建立模组化系列,从微型到重型,而无需重新编写其认证通讯协定。

区域分析

受中国多品牌乘用车生产和日本高精度阀门产能的推动,亚太地区将在2024年占据全球销售量的45.50%。该地区的复合年增长率预计将达到7.10%,因为越南、泰国和印度的供应基地正在提升价值曲线,使区域内采购对全球製造商更具吸引力。韩国的电动气动研发中心利用该国先进的半导体生态系统,将压力MEMS感测器整合到致动器PCB上,增强了其竞争地位。儘管电动车正在兴起,但成本优化的微型车市场仍采用气动暖通空调和涡轮增压排气泄压阀阀装置,为供应商提供了产量。

中东和非洲是成长最快的丛集,复合年增长率为7.80%。沙乌地阿拉伯的「2030愿景」产业政策正在吸引CKD组装,企业也需要商用卡车致动器组件的在地化,以支持其建筑业的繁荣发展。阿拉伯联合大公国(UAE)正在利用自由区物流,将零件套件转口到非洲市场。土耳其加入欧洲关税同盟的便利性正在促进零件出口,迫使气动设备供应商扩大其在伊兹密尔和布尔萨的工厂。这些动态正在将采购从跨洲运输转向更靠近市场的生产,从而缩短了前置作业时间并减少了货运排放。

在南美,该地区独特的灵活燃料引擎架构正在刺激对废气再循环 (EGR) 和燃油轨致动器的需求,因为燃烧化学计量会根据乙醇混合物的变化而每日变化。跨国供应商正在推动在地采购法规,以便在米纳斯吉拉斯安装弹性体硫化机,而不是进口密封件。阿根廷的重型卡车组装厂在货币稳定措施后正在復苏,这增加了对大容量煞车室的需求。外汇波动和政治风险抑制了前景,但装置量的惯性使整个西半球的汽车气动致动器市场保持韧性。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 更严格的排放法规鼓励精确的空燃比控制

- 全球汽车产量增加

- 需要精确操作的ADAS的普及

- 减轻重量以提高燃油效率

- 采用氢内燃机的气门正时

- 透过支援 OTA 的致动器软体收益

- 市场限制

- 转向节能电动致动器

- 气动致动器的复杂性和高维护成本

- 密封用高级弹性体短缺

- Tier-1脱碳,抑制气动设备研发

- 价值/供应链分析

- 监管状况

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模与成长预测:价值(美元)与数量(单位)

- 按应用程式类型

- 节气门致动器

- 燃油喷射致动器

- 致动器

- 废气再循环致动器

- 涡轮增压器废气旁通致动器

- HVAC致动器

- 门锁致动器

- 其他的

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中大型商用车

- 非公路用车

- 摩托车

- 按致动器机构

- 单膜片气压

- 真空增压气压

- 电动气动(EP)

- 伺服气压

- 齿条和小齿轮

- 转叶

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Emerson(ASCO Valve)

- Hitachi Astemo Ltd

- CTS Corporation

- Schrader Duncan Ltd

- Rotex Automation

- Nucon Industries Pvt Ltd

- Magneti Marelli SpA

- Mitsubishi Electric Corp

- Del-Tron Precision Inc

- Procon Engineering

- Valeo SA

- Aisin Corporation

- Mahle GmbH

- BorgWarner Inc

第七章 市场机会与未来展望

The Automotive Pneumatic Actuators Market size is estimated at USD 53.17 billion in 2025, and is expected to reach USD 69.49 billion by 2030, at a CAGR of 5.50% during the forecast period (2025-2030).

Despite competition from energy-efficient electric actuators, vehicle makers continue to rely on pneumatic devices for safety, powertrain, and chassis functions. Stricter emission regulations and the growing adoption of ADAS drive demand, with Asia-Pacific leading due to strong supply chains. At the same time, the Middle East and Africa, as well as South America, see rapid growth from expanding local assembly programs.

Global Automotive Pneumatic Actuators Market Trends and Insights

Stricter emission norms driving precise air-fuel control

The US EPA's Phase 3 heavy-duty standards enacted in 2024 tighten NOx thresholds, compelling diesel makers to refine EGR and dosing strategies that rely on high-resolution pneumatic valves. Similar Euro 7 drafts trigger demand peaks in Europe. Field-valid testing replaces laboratory cycles, forcing actuators to sustain precision under real-world vibration and temperature excursions. Suppliers with electro-pneumatic packages that close the digital feedback loop enjoy distinct bidding advantages. The regulatory timetable accelerates award decisions, locking in revenue visibility for the forecast period.

Increasing global vehicle production

Rising light-duty and heavy-duty volumes lift baseline demand across all pneumatic applications because every unit assembled carries multiple actuator points. The Japan Automobile Manufacturers Association confirmed that OEM schedules for 2025 still embed pneumatic solutions in brake, throttle, and EGR circuits to assure fuel efficiency and compliance. Platform sharing further magnifies volumes because a single actuator family can now be fitted across sibling models, raising economies of scale for suppliers. Western manufacturers are repositioning final-assembly footprints toward Southeast Asia, which encourages actuator makers to co-locate module lines. The production rebound therefore secures near-term growth in the automotive pneumatic actuators market even as electric rivals sharpen their cost proposition.

Shift toward energy-efficient electric actuators

Electromechanical systems convert battery power into motion with up to 80% efficiency, dwarfing the 20% ceiling of air-driven counterparts. The delta becomes more pronounced in electric cars, where every watt saved extends range. Line-builders are also migrating their welding robots and material-handling arms to electric cylinders for tighter path accuracy. Yet pneumatics still dominates the highest-force nodes, such as heavy truck drum brakes, where compressed air is already integral to the vehicle platform. Consequently suppliers are channeling R&D toward mixed-technology actuators that preserve pressure-based force while embedding low-energy position control.

Other drivers and restraints analyzed in the detailed report include:

- ADAS proliferation demanding accurate actuation

- Lightweighting trend for fuel economy

- Complexity & high maintenance cost of pneumatics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake chambers and parking brake caliper units commanded 31.50% share of the automotive pneumatic actuators market in 2024. Their presence is mandated across every passenger and commercial vehicle variant, cementing baseline volume. Electromechanical parking brakes are penetrating luxury sedans, but heavy truck drum brakes still rely on air chambers that deliver high clamping force at low unit cost. Turbocharger wastegate actuators follow as the fastest riser, posting a 6.70% CAGR because downsized gasoline engines depend on accurate boost management to meet power and emission targets. Throttle valves, HVAC blend doors, and EGR butterflies retain mid-single-digit growth, each backed by regulatory or comfort imperatives.

Pneumatic fuel-injection rail regulators survive in certain flex-fuel layouts popular in Brazil, while door-lock plungers remain common in cost-sensitive hatchbacks. Across the board, suppliers experiment with smart pressure sensors embedded in actuator bodies to supply health data back to the vehicle control network. The enhancements prolong relevance of pneumatically powered devices even as direct electric motor drives tighten competitive gaps. Overall, the application mix underscores why the automotive pneumatic actuators market maintains double-digit billion-dollar revenues: it spans mandatory safety, emissions, and comfort functions that every vehicle must carry.

Passenger cars generated 56.70% of 2024 revenue, reflecting sheer production volume across global plants. Yet heavy commercial vehicles are projected to pace the automotive pneumatic actuators market size expansion with a 5.90% CAGR. Fleet operators prize the durability of air-brake and air-suspension circuits under intense duty cycles, while stricter CO2 quotas push for optimized compressor management rather than wholesale technology swaps. Light commercial vans track e-commerce parcel demand and achieve a robust CAGR on the back of city-logistics growth. Construction and mining equipment are, chiefly for high-temperature exhaust-flap controllers and robust steering stabilizers.

Two-wheelers remain a micro-segment concentrated in select Asian economies, yet scooter OEMs are trialing low-pressure air servos for automatic clutch actuation. The diversity highlights a bifurcation: suburban passenger cars gravitate toward compact electric drives for NVH advantages, whereas high-payload vehicles sustain pneumatics for force density and proven maintainability. That divergence shapes future platform strategies of tier-1 suppliers, compelling them to produce modular families that scale from micro to heavy-duty ratings without rewriting qualification protocols.

The Automotive Pneumatic Actuator Market is Segmented by Application Type (Throttle Actuators, Fuel Injection Actuators, Brake Actuators, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Actuator Mechanism (Single-Diaphragm Pneumatic and More), Sales Channel (OEM and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific generated 45.50% of global revenue in 2024, underpinned by China's multi-brand passenger car output and Japan's high-precision valve competence. The region is forecast to post a 7.10% CAGR as supply bases in Vietnam, Thailand, and India climb the value curve, making in-region sourcing attractive for global nameplates. Electro-pneumatic R&D centers in South Korea exploit the country's advanced semiconductor ecosystem to integrate pressure MEMS sensors onto actuator PCBs, heightening competitive edge. Notwithstanding electric-vehicle penetration, cost-optimized sub-compact segments still install pneumatically driven HVAC and turbo wastegate units, securing volume for suppliers.

Middle East & Africa stands out as the fastest-growing cluster at a robust CAGR of 7.80%. Saudi Vision 2030 industrial policy lures CKD assembly lines, each demanding localized actuator content for commercial trucks that service construction booms. The UAE leverages free-zone logistics to re-export spare parts kits deeper into African markets. Turkey's customs-union access to Europe boosts its component exports, compelling pneumatic suppliers to expand Izmir and Bursa facilities. These dynamics re-orient procurement away from trans-continental shipping toward near-market production, shortening lead times and cutting freight emissions.

In South America, flex-fuel engine architectures unique to the region stimulate EGR and fuel-rail actuator demand because ethanol blends alter combustion stoichiometry daily. Local content rules push multinational suppliers to site elastomer curing presses in Minas Gerais rather than import seal stacks. Argentine heavy-truck assembly rebounds after currency stabilization measures, adding lift for high-capacity brake chambers. Currency volatility and political risk temper the outlook, yet installed base inertia keeps the automotive pneumatic actuators market resilient in the hemisphere.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Emerson (ASCO Valve)

- Hitachi Astemo Ltd

- CTS Corporation

- Schrader Duncan Ltd

- Rotex Automation

- Nucon Industries Pvt Ltd

- Magneti Marelli SpA

- Mitsubishi Electric Corp

- Del-Tron Precision Inc

- Procon Engineering

- Valeo SA

- Aisin Corporation

- Mahle GmbH

- BorgWarner Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter emission norms driving precise air-fuel control

- 4.2.2 Increasing global vehicle production

- 4.2.3 ADAS proliferation demanding accurate actuation

- 4.2.4 Lightweighting trend for fuel economy

- 4.2.5 Hydrogen ICE valve-timing adoption

- 4.2.6 OTA-enabled actuator software monetisation

- 4.3 Market Restraints

- 4.3.1 Shift toward energy-efficient electric actuators

- 4.3.2 Complexity & high maintenance cost of pneumatics

- 4.3.3 Shortage of high-grade elastomers for seals

- 4.3.4 Tier-1 decarbonisation curbing pneumatic R&D

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Application Type

- 5.1.1 Throttle Actuators

- 5.1.2 Fuel Injection Actuators

- 5.1.3 Brake Actuators

- 5.1.4 Exhaust Gas Recirculation Actuators

- 5.1.5 Turbocharger Wastegate Actuators

- 5.1.6 HVAC Actuators

- 5.1.7 Door Lock Actuators

- 5.1.8 Others

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Off-Highway Vehicles

- 5.2.5 Two-Wheelers

- 5.3 By Actuator Mechanism

- 5.3.1 Single-Diaphragm Pneumatic

- 5.3.2 Vacuum-Boost Pneumatic

- 5.3.3 Electro-pneumatic (EP)

- 5.3.4 Servo-pneumatic

- 5.3.5 Rack-and-Pinion

- 5.3.6 Rotary-Vane

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 Emerson (ASCO Valve)

- 6.4.5 Hitachi Astemo Ltd

- 6.4.6 CTS Corporation

- 6.4.7 Schrader Duncan Ltd

- 6.4.8 Rotex Automation

- 6.4.9 Nucon Industries Pvt Ltd

- 6.4.10 Magneti Marelli SpA

- 6.4.11 Mitsubishi Electric Corp

- 6.4.12 Del-Tron Precision Inc

- 6.4.13 Procon Engineering

- 6.4.14 Valeo SA

- 6.4.15 Aisin Corporation

- 6.4.16 Mahle GmbH

- 6.4.17 BorgWarner Inc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车电液致动器市场按类型、车辆类型、动力系统、应用和分销管道划分,全球预测,2026-2032年

汽车电液致动器市场按类型、车辆类型、动力系统、应用和分销管道划分,全球预测,2026-2032年 2026-2034年全球汽车致动器市场规模、份额、趋势和成长分析报告

2026-2034年全球汽车致动器市场规模、份额、趋势和成长分析报告 汽车致动器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、应用、地区和竞争格局划分,2021-2031年)新能源汽车致动器市场(按推进类型、车辆类型、应用和销售管道)——2026-2032年全球预测电子停车控制器市场,依产品类型、车辆类型、销售管道和应用划分,全球预测,2026-2032年

汽车致动器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、应用、地区和竞争格局划分,2021-2031年)新能源汽车致动器市场(按推进类型、车辆类型、应用和销售管道)——2026-2032年全球预测电子停车控制器市场,依产品类型、车辆类型、销售管道和应用划分,全球预测,2026-2032年 日本汽车执行器市场报告(依产品、执行器类型、车辆类型、销售通路(原厂配套、售后市场)及地区划分,2026-2034年)日本汽车气动执行器市场报告(按产品(节气门执行器、燃油喷射执行器、煞车执行器及其他)、车辆类型(乘用车、商用车)和地区划分,2026-2034年)日本汽车液压执行器市场规模、份额、趋势及预测(按车辆类型、应用类型和地区划分,2026-2034年)日本汽车电动执行器市场报告(按产品(油门执行器、座椅调节执行器、煞车执行器、车门关闭执行器及其他)、车辆类型(乘用车、商用车)和地区划分,2026-2034年)

日本汽车执行器市场报告(依产品、执行器类型、车辆类型、销售通路(原厂配套、售后市场)及地区划分,2026-2034年)日本汽车气动执行器市场报告(按产品(节气门执行器、燃油喷射执行器、煞车执行器及其他)、车辆类型(乘用车、商用车)和地区划分,2026-2034年)日本汽车液压执行器市场规模、份额、趋势及预测(按车辆类型、应用类型和地区划分,2026-2034年)日本汽车电动执行器市场报告(按产品(油门执行器、座椅调节执行器、煞车执行器、车门关闭执行器及其他)、车辆类型(乘用车、商用车)和地区划分,2026-2034年) 汽车致动器市场规模、份额和成长分析(按车辆类型、推进系统、类型和地区划分)-2026-2033年产业预测

汽车致动器市场规模、份额和成长分析(按车辆类型、推进系统、类型和地区划分)-2026-2033年产业预测