|

市场调查报告书

商品编码

1844514

地工砖:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Geofoams - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

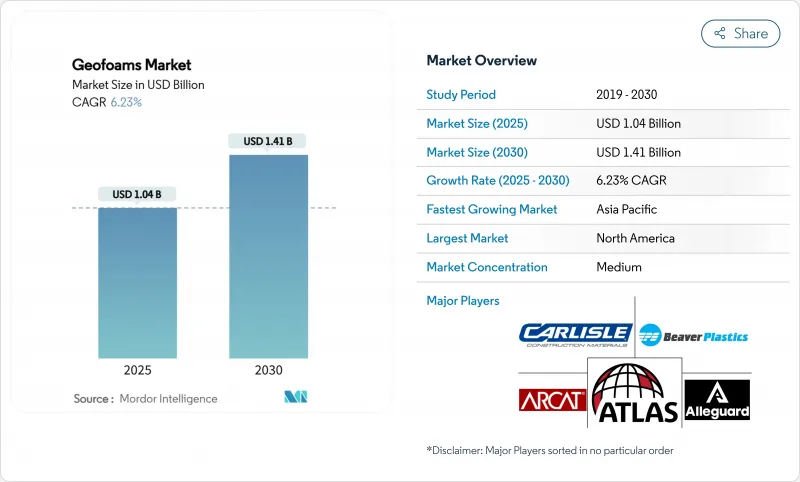

地工砖市场规模预计在 2025 年为 10.4 亿美元,预计到 2030 年将达到 14.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.23%。

基础设施更新、轻量化建筑趋势和日益增长的永续性要求支撑了整体需求,而发泡和押出成型聚苯乙烯技术正在重新定义传统的填土方法。亚太地区和北美地区对高速公路、桥樑和城市交通系统的资本投资不断增加,直接推动了对地工砖块的竞标增加,特别是在软土地基和地震风险限制传统回填的地区。设计建造商越来越欣赏地工砖的工厂控制一致性和快速应用时间,这减少了高流量走廊的车道封闭。同时,监管机构也越来越关注碳排放揭露,这加强了地工砖相对于颗粒填充材的生命週期成本优势。竞争差异化依赖聚苯乙烯供应、再生材料开发和阻燃化学的垂直整合。

全球地工砖市场趋势与洞察

道路和桥樑路堤需求增加

交通运输机构正在采用地工砖泡沫块来减轻不均匀沉降、缩短施工进度并避免昂贵的地面改良项目。在科罗拉多的一项紧急公路修復项目中,地工砖取代了传统的挡土结构,将进度缩短了 30%。挪威的一项公路计划展示了地工砖在冻融循环下的弹性,350 个安装案例显示其耐用性可达 100 年。桥樑引桥坡道尤其有益,因为即使在没有深基础的软土地基中它们也能保持形状。由于其密度为土壤的 1%,因此安装后几天而不是几週就可以恢復交通。长期监测证实,地震和热事件期间的载重分布与设计模型一致。

传统轻型路堤的经济高效替代方案

地工砖的吸引力远不止于单价。预製块料可减少高达40%的边坡修復工时,避免现场搅拌及保养。当骨材供应地距离数百公里时,运输成本的节省将非常显着。这些块料可手工搬运,所需工人更少,设备更轻,从而降低燃料和租赁成本。其密度和抗压强度在工厂控制,省去了与现场混合方案相关的品质保证成本。这些综合特性可以释放计划预算,用于资助排水系统改进等辅助领域。

极易受到石油基溶剂和碳氢化合物的影响

聚苯乙烯对碳氢化合物溶剂的亲和性限制了其在燃料处理区域附近的使用。美国国家海洋暨大气总署化学物质资料库指出,EPS 与汽油接触时体积会迅速缩小,因此需要使用高密度聚乙烯 (HDPE)地工止水膜屏障,这会使安装成本增加 5-10%。高溢油风险的道路必须设置监测井和紧急衬垫,使其设计更加复杂。工业蓄水池也面临类似的风险,因此设计师需要考虑替代填充材和复合封装系统。虽然涂层技术正在进步,但长期现场检验仍然有限,这促使设计师在关键设施的设计上谨慎行事。

細項分析

预计到2024年,发泡聚苯乙烯 (EPS) 将占据地工砖市场65.12%的份额,而押出成型聚苯乙烯年增长率预计将达到6.58%,直至2030年。发泡聚苯乙烯 (EPS) 在成本敏感的堤防领域蓬勃发展,这些领域以数量为主导筹资策略,从而支撑了整个地工砖市场。然而,XPS 吸水率低且抗压强度高,使其非常适合用于桥樑、隧道和寒冷气候下的地基,这些地方需要较长的使用寿命。杜邦测试表明,XPS 的厚度可以减少30-40%,以实现相同的热阻值,这对于寻求无需过度开挖即可实现基层保温的设计师来说极具吸引力。

蒸汽膨胀所需能量和苯乙烯投入较少,单位成本比XPS低15-20%。相反,XPS的连续挤压可产生均匀的泡孔尺寸,从而抗蠕变,支援设计寿命超过75年的高端应用。 EPS回收基础设施青睐EPS,因为块状边角料可以轻鬆製成颗粒并蒸煮成新的珠粒,而XPS的再挤压则需要更严格的熔体过滤。展望未来,随着市政当局采用绿色建筑计划,并因其耐湿性而减少维护预算,XPS的市场份额可能会进一步上升。然而,EPS的价格优势很可能在大规模散装填料应用中继续保持其地位。

区域分析

受大型公路维修和桥樑引桥严格的沉降控制标准推动,北美地区到2024年将占全球销售额的35.19%。科罗拉多、明尼苏达州和安大略省的计划证明了控制差异沉降可以实现生命週期成本的节省。加拿大北极走廊正在利用地工砖的隔热性能来稳定永久冻土,防止融水在跑道和管道下方下沉。

预计到2030年,亚太地区将以6.92%的复合年增长率位居全球首位,这得益于每年1.7兆美元的基础设施需求。中国和印度的大型铁路走廊正在采用地工砖来处理软弱的冲积土,而无需进行深基坑开挖。日本的地震标准认可使用轻质堤防来减轻惯性荷载,而EPS砌块则是韩国高速公路匝道拓宽计划的标准配备。

在欧洲,循环经济政策和沿海气候挑战正在推动泡沫塑胶的稳定应用。德国和法国正在将再生地工砖纳入防洪工程,以符合欧盟的废弃物减量目标。英国的智慧高速公路升级工程正在使用地工砖来最大限度地缩短封闭时间,并支持与降低用户延误成本相关的承包商奖励。北欧国家正在利用30年来检验地工砖在零下温度下韧性的现场数据,以核准公众信任并获得监管机构的批准,从而扩大地工砖的使用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 道路、桥樑和堤防的需求不断增加

- 传统轻型路堤的经济高效替代方案

- 亚太地区基础建设投资快速成长

- 利用 EPS地工砖土工布加速模组化桥樑项目

- 透过重复使用回收的 EPS地工砖来促进循环经济

- 市场限制

- 极易受到石油溶剂和碳氢化合物的影响

- 新兴国家的设计知识有限

- 防火标准更加严格导致成本上升

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按类型

- 发泡聚苯乙烯(EPS)

- 挤塑聚苯乙烯(XPS)

- 按最终用户产业

- 路

- 大楼

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Airfoam

- Alleguard

- ARCAT, Inc.

- Atlas Roofing Corporation

- BASF SE

- Beaver Plastics Ltd.

- Benchmark Foam Inc.

- Carlisle Construction Materials LLC

- FMI-EPS LLC

- Harbor Foam Inc.

- NOVA Chemicals Corporate

- Plasti-Fab Ltd

- Poly Molding LLC

- Styro Insulations Mat. Ind. LLC.

- ThermaFoam, LLC

- Universal Foam Products

第七章 市场机会与未来展望

The Geofoams Market size is estimated at USD 1.04 billion in 2025, and is expected to reach USD 1.41 billion by 2030, at a CAGR of 6.23% during the forecast period (2025-2030).

Infrastructure renewal, lightweight construction trends and growing sustainability mandates collectively underpin demand, while expanded and extruded polystyrene technologies redefine conventional earth-fill approaches. Accelerated capital expenditure on highways, bridges and urban transit systems in Asia-Pacific and North America is translating directly into larger bid volumes for geofoam blocks, especially where weak soils or seismic risk constrain traditional backfills. Design-build contractors increasingly value geofoam's factory-controlled consistency and fast installation times, reducing lane-closure periods on heavily trafficked corridors. Meanwhile, heightened regulatory interest in embodied-carbon disclosure is elevating the material's lifecycle cost advantages relative to granular fills. Competitive differentiation now hinges on vertical integration into polystyrene supply, recycled-content development and fire-retardant chemistry.

Global Geofoams Market Trends and Insights

Rising Demand from Roadway & Bridge Embankments

Transportation agencies are turning to geofoam blocks to mitigate differential settlement, shorten construction schedules and avoid costly ground-improvement programs. Colorado's emergency highway repair demonstrated 30% schedule compression when geofoam replaced traditional earthwork. Norwegian highway projects show 100-year durability across 350 installations, proving the material's resilience under freeze-thaw cycles. Bridge approach ramps gain particular benefit, maintaining geometry over weak soils without deep foundations. The 1% density versus soil allows traffic to reopen days, not weeks, after placement. Long-term monitoring confirms load distribution that matches design models during seismic and thermal events.

Cost-Effective Alternative to Traditional Lightweight Fills

Geofoam's attraction extends beyond unit price. Prefabricated blocks bypass on-site mixing and curing, trimming labor hours by up to 40% in slope repair works. Transport savings are pronounced where aggregate sources lie hundreds of kilometers away. Because blocks can be manually maneuvered, smaller crews and lighter equipment reduce fuel and rental costs. Factory-controlled density and compressive strength slash quality-assurance outlays tied to field-mixed solutions. Together, these attributes reposition project budgets, freeing capital for ancillary scope such as drainage upgrades.

High Vulnerability to Petroleum Solvents & Hydrocarbons

Polystyrene's affinity for hydrocarbon solvents constrains deployment near fuel handling zones. NOAA's chemical database cites rapid volumetric loss when EPS contacts gasoline, necessitating HDPE geomembrane barriers that add 5-10% to installed cost. Roadways with high spill risk must incorporate monitoring wells and contingency liners, complicating designs. Industrial storage yards face similar exposure, pushing specifiers toward alternative fills or composite encapsulation systems. Although coating technologies are advancing, long-term field validation remains limited, keeping designers cautious in critical facilities.

Other drivers and restraints analyzed in the detailed report include:

- Surging Infrastructure CAPEX in Asia-Pacific

- Accelerated Modular Bridge Programs Using EPS Geofoam Blocks

- Stricter Fire-Resistance Standards Driving Cost Up

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Expanded polystyrene retained 65.12% of geofoams market share in 2024, while extruded polystyrene is forecast to grow at a 6.58% CAGR to 2030. EPS thrives in cost-sensitive roadway embankments where volume rules procurement strategies, sustaining the overall geofoams market. Yet XPS's lower water absorption and superior compressive strength satisfy bridge, tunnel and cold-climate foundations demanding long service life. DuPont tests reveal XPS can deliver the same thermal R-value with 30-40% thinner sections, appealing to designers seeking subgrade insulation without over-excavation.

Production economics illustrate why EPS dominates volume: steam expansion uses less energy and input styrene, keeping unit costs 15-20% below XPS. Conversely, XPS's continuous extrusion yields uniform cell size that resists creep, supporting premium applications where design life exceeds 75 years. Recycling infrastructure favors EPS because block off-cuts can be readily granulated and steamed into new beads, whereas XPS re-extrusion demands stricter melt-filtering. Looking forward, municipalities with aggressive green-building codes may tilt share further toward XPS as moisture durability lessens maintenance budgets, but EPS will stay entrenched in large-scale bulk fills owing to its price advantage.

The Geofoams Market Report is Segmented by Type (Expanded Polystyrene (EPS), Extruded Polystyrene (XPS)), End-User Industry (Roadways, Buildings), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.19% of global revenue in 2024, underpinned by extensive highway rehabilitation and stringent settlement-control criteria in bridge approaches. Projects in Colorado, Minnesota and Ontario testify to lifecycle cost savings once differential settlement is curtailed. Canadian Arctic corridors leverage geofoam's insulating value to stabilize permafrost, preventing thaw settlement beneath runways and pipelines.

Asia-Pacific is projected to expand at a 6.92% CAGR to 2030, the fastest globally, on the back of USD 1.7 trillion yearly infrastructure needs. Mega-rail corridors in China and India favor geofoam to manage weak alluvial soils without deep excavation. Japanese seismic codes reward lightweight fills that reduce inertial loads, while South Korean expressways have standardized EPS blocks for ramp widening projects.

Europe demonstrates steady adoption driven by circular-economy mandates and coastal climate challenges. Germany and France integrate recycled-content geofoam into flood-defense works, aligning with EU waste-reduction targets. The United Kingdom's smart-motorway upgrades specify geofoam to minimize closure times, supporting contractor incentives tied to user delay cost savings. Nordic countries capitalize on three decades of field data validating geofoam resilience in sub-zero conditions, reinforcing public trust and regulatory approval for expanded use.

- Airfoam

- Alleguard

- ARCAT, Inc.

- Atlas Roofing Corporation

- BASF SE

- Beaver Plastics Ltd.

- Benchmark Foam Inc.

- Carlisle Construction Materials LLC

- FMI-EPS LLC

- Harbor Foam Inc.

- NOVA Chemicals Corporate

- Plasti-Fab Ltd

- Poly Molding LLC

- Styro Insulations Mat. Ind. LLC.

- ThermaFoam, LLC

- Universal Foam Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from roadway and bridge embankments

- 4.2.2 Cost-effective alternative to traditional lightweight fills

- 4.2.3 Surging infrastructure CAPEX in Asia-Pacific

- 4.2.4 Accelerated modular bridge programs using EPS geofoam blocks

- 4.2.5 Circular-economy push for recycled-EPS geofoam reuse

- 4.3 Market Restraints

- 4.3.1 High vulnerability to petroleum solvents and hydrocarbons

- 4.3.2 Limited design know-how in emerging economies

- 4.3.3 Stricter fire-resistance standards driving cost up

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Expanded Polystyrene (EPS)

- 5.1.2 Extruded Polystyrene (XPS)

- 5.2 By End-user Industry

- 5.2.1 Roadways

- 5.2.2 Buildings

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airfoam

- 6.4.2 Alleguard

- 6.4.3 ARCAT, Inc.

- 6.4.4 Atlas Roofing Corporation

- 6.4.5 BASF SE

- 6.4.6 Beaver Plastics Ltd.

- 6.4.7 Benchmark Foam Inc.

- 6.4.8 Carlisle Construction Materials LLC

- 6.4.9 FMI-EPS LLC

- 6.4.10 Harbor Foam Inc.

- 6.4.11 NOVA Chemicals Corporate

- 6.4.12 Plasti-Fab Ltd

- 6.4.13 Poly Molding LLC

- 6.4.14 Styro Insulations Mat. Ind. LLC.

- 6.4.15 ThermaFoam, LLC

- 6.4.16 Universal Foam Products

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

全球地工砖市场规模、份额、趋势和成长分析报告(2026-2034年)

全球地工砖市场规模、份额、趋势和成长分析报告(2026-2034年) 地工砖市场按产品类型、最终用户、分销管道和应用划分-全球预测,2025-2032年

地工砖市场按产品类型、最终用户、分销管道和应用划分-全球预测,2025-2032年 土工泡沫市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

土工泡沫市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 地工砖市场规模、份额和成长分析(按类型、最终用途、应用和地区)- 产业预测 2025-2032

地工砖市场规模、份额和成长分析(按类型、最终用途、应用和地区)- 产业预测 2025-2032 全球地工砖市场,2024-2028

全球地工砖市场,2024-2028 到 2030 年地工砖市场预测:按类型、应用、最终用户和地区分類的全球分析

到 2030 年地工砖市场预测:按类型、应用、最终用户和地区分類的全球分析 土工泡沫市场,按土工泡沫类型、密度、应用、国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

土工泡沫市场,按土工泡沫类型、密度、应用、国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测