|

市场调查报告书

商品编码

1844540

汽车转向:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Automotive Steering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

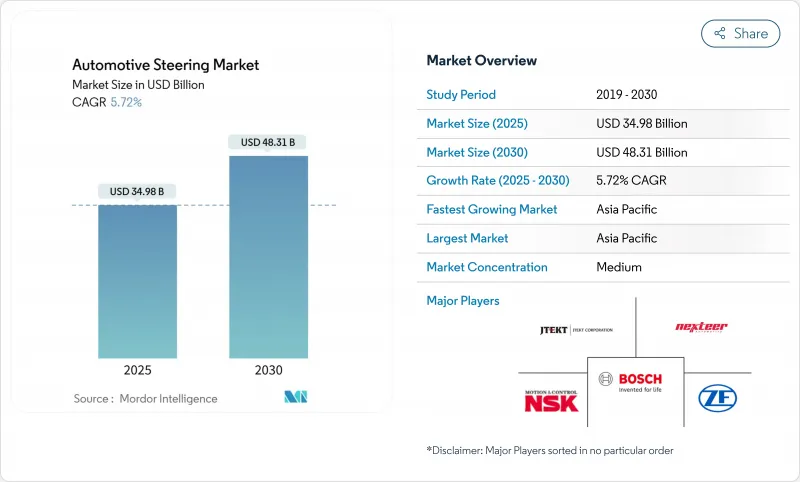

预计 2025 年汽车转向系统市场价值将达到 349.8 亿美元,到 2030 年将达到 483.1 亿美元,复合年增长率为 5.72%。

成长动力源自于液压辅助转向电子动力方向盘的快速转型,以及线控转向的首次商业化部署。此外,联合国欧洲经济委员会 R155 网路安全法规正在加速对软体定义电控系统的需求。由于中国的规模优势和日本在高精度零件领域的专业化,亚太地区维持了 48.67% 的收入份额。稀土元素供应商正在整合核心技术,以确保智慧财产权,并承担冗余「故障操作」架构所需的高额前期投资。对于能够消除稀土元素、减轻重量并在不增加材料成本的情况下提高功能安全性的马达和感测器专家来说,机会正在涌现。

全球汽车转向市场趋势与洞察

EPS 在 ICE 和 xEV 平台上的快速采用

电子动力方向盘在中国乘用车产业迅速普及,在欧洲和日本也日益普及。原始设备製造商可以解锁电力传动系统中再生煞车的兼容性,同时获得节油效益。采埃孚的商用车电动辅助转向系统无需液压油即可提供高达 8,000 牛顿米的扭矩,这使得该技术广泛应用于从紧凑型轿车到 8 级卡车的各种车型。虽然管柱辅助转向系统在 B-Class 中占据主导地位,但齿条辅助转向系统在对精度和路感要求更高的高阶车型中也逐渐占据了市场份额。快速换檔正在推动汽车转向系统市场的稳定成长。

线传系统将于 2025 年在高阶电动车中推出

继采埃孚 (ZF) 于 2025 年为蔚来 (NIO) ET9 推出该系统之后,梅赛德斯-奔驰 (Mercedes-Benz) 将于 2026 年推出欧洲首款量产线传系统。该系统取消了机械轴,实现了可变转向比,使停车更加便捷,并提高了高速公路行驶稳定性。丰田的「One Motion Grip」方向盘,其 200 度输入行程取代了传统的 540 度转弯,改善了人体工学和座舱布局。冗余马达、电源和触觉回馈可保持驾驶信心,但消费者接受度研究表明,学习曲线可能会延长推出时间,使其超越豪华品牌。

稀土磁铁价格波动推高EPS的BOM

中国控制全球约70%的稀土加工,钕的出口受到限制。磁铁成本已占到EPS马达材料清单的25%。福特汽车公司暂停Explorer的生产,为原始设备製造商的进度带来了风险。供应商正透过追求无稀土创新来应对这项挑战,例如ZF的I2SM马达和麦格纳对Niron Magnetics的铁氮清洁土磁铁的投资。

細項分析

2024年,转向柱和齿条将主导汽车转向系统市场,占39.26%的收益份额。整合防倾倒装置、多功能开关和驾驶员安全气囊模组使该细分市场成为所有平台的必备组件。同时,随着无刷直流马达设计取代液压泵和皮带传动装置,电动马达将以最快的速度成长,到2030年复合年增长率达到8.91%。网路安全电控系统构成第三大市场,随着UNECE R155标准要求製造商确保每项新的无线功能,每辆车的网路安全电子控制单元的配置量都在增加。

扭矩、角度和位置感测器正与依赖毫秒级精确回馈的线传和ADAS功能同步发展。 TDK的四模HAL 39xy晶片展示了单封装解决方案如何在减轻线路重量的同时,有效抵御高压动力传动系统的磁噪声。能够将马达、感测器和ECU功能整合到紧凑的屏蔽外壳中的供应商,能够透过提高系统可靠性和缩短保固期,巩固其在汽车转向系统市场的地位。

乘用车将主导全球汽车转向系统市场,到2024年将占总收入的63.28%。同时,轻型商用车已成为成长最快的细分市场,复合年增长率高达7.56%。电商车队重视电动辅助转向系统 (EPS) 带来的精准低速操控和低维护成本,而自动驾驶配送概念则倾向于软体控制转向,以实现精准的路边停车。随着现代齿条驱动EPS 装置实现工业级扭力输出,重型商用车逐渐放弃液压转向。车主对燃油经济性的日益关注将使各类汽车转向系统市场受益。

在乘用车领域,纯电动车正在取代传统液压系统所使用的引擎真空源,使电动辅助转向系统 (EPS) 成为必需品。由于消费者偏好更高的驾驶位置,运动型多用途车 (SUV) 的市场份额正在不断增长,而其更大的占地面积意味着转向系统组件的数量也随之增加。多用途车和小型货车正在利用 EPS 封装来提供平地板座舱。由于这些复杂的变化,汽车转向系统产业的单位产量和销售量均保持着稳定的成长轨迹。

汽车转向系统市场按零件(液压帮浦、电动马达等)、车型(乘用车、商用车)、机构(电动动力方向盘(EPS)、液压动力方向盘(HPS)、电助力液压动力方向盘等)、销售管道(整车厂、售后市场)及地区细分。市场预测以金额(美元)和数量(单位)表示。

区域分析

预计到2024年,亚太地区将占据汽车转向系统市场的48.67%,到2030年将维持6.81%的强劲复合年增长率。中国庞大的电动车生产基地将推动电动辅助转向系统(EPS)的普及,而像HIVE Steering这样的本土企业则利用国内硅片和磁铁供应,以低于现有进口产品的价格竞争。日本则拥有丰富的专业知识,包括捷太JTEKT)的线传测试和日本精工(NSK)的低摩擦轴承技术。地方政府正在製定清晰的自动驾驶认证蓝图,进一步推动汽车转向系统市场对线传系统的需求。

在欧洲,欧7和联合国欧洲经济委员会(UNECE)网路安全法规鼓励采用先进的电子控制单元(ECU)、轻量化转向柱和冗余作动器,从而提高单车价值。采埃孚(ZF)和博世(Bosch)已开始大量出货线控转向系统,并利用当地技术中心为高端品牌调校转向手感。然而,如果钕金属短缺导致生产停产,原始设备製造商(OEM)面临的原料风险将更加凸显。这项风险加速了对无稀土马达技术的研究,使供应商无需等待新车型週期即可提高单车钕金属含量。

在北美,皮卡和运动型多用途汽车(销量最大的汽车细分市场)对电动辅助转向系统的采用率正在稳步上升。车队营运商密切关注总拥有成本,而电动辅助转向系统节省3-5%的燃油成本,正在推动其采用。美国也是免校准安装和安全无线软体(可在车辆使用期间更新转向逻辑)的研发中心。同时,南美、中东和非洲地区正采用电子转向系统作为工厂升级平台。这些市场通常会在新车型上直接过渡到电动辅助转向系统,从而为汽车转向系统市场带来长期的上涨空间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- EPS 在 ICE 和 Xev 平台上的快速采用

- 线传系统将于 2025 年起在高阶电动车中推出

- 轻型转向柱,符合欧盟 7/CAFE 法规

- OEM对支援ADAS的「故障运行」架构的需求

- UNECE R155 要求市场上必须使用网路安全 ECU

- OTA可升级扭力迭加软体销售

- 市场限制

- 稀土元素磁铁价格波动推高EPS的BOM

- 到2026年汽车MCU短缺

- 对转向系统的担忧导致线控转向系统普及速度缓慢

- 一级供应商整合限制了原始设备製造商的议价能力

- 价值/供应链分析

- 技术展望

- 监管状况

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按组件

- 液压泵浦

- 电动机

- 转向柱/转向架

- 感测器(扭矩、角度、位置)

- 电控系统(ECU)

- 其他组件

- 按车辆类型

- 搭乘用车

- 掀背车

- 轿车

- 运动型多用途车

- 多用途车辆

- 商用车

- 轻型商用车

- 中大型商用车

- 搭乘用车

- 按机制

- 电子动力方向盘(EPS)

- 液压动力方向盘(HPS)

- 电动液压动力方向盘(EHPS)

- 线控转向

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- JTEKT Corporation

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Nexteer Automotive Corporation

- NSK Ltd

- Mando Corporation

- Showa Corporation

- Hitachi Astemo

- Hyundai Mobis

- ThyssenKrupp Presta

- Schaeffler Group

- Denso Corporation

- Knorr-Bremse AG

- China Automotive Systems Inc

第七章 市场机会与未来展望

The Automotive Steering System market is valued at USD 34.98 billion in 2025 and is forecast to reach USD 48.31 billion by 2030, reflecting a 5.72% CAGR.

Growth is anchored in the rapid migration from hydraulic assistance to electronic power steering and the first commercial deployments of steer-by-wire. Tightening global emission limits and the rising share of battery-electric vehicles strengthen the business case for energy-efficient steering technologies, while cybersecurity rules under UNECE R155 accelerate demand for software-defined electronic control units. Asia-Pacific retains a 48.67% revenue share, helped by China's scale advantages and Japan's specialization in high-precision components. Tier-1 suppliers are consolidating core technologies to secure intellectual property and to fund the high up-front investment needed for redundant, "fail-operational" architectures. Opportunities emerge for motor and sensor specialists that can remove rare-earth content, cut weight, and improve functional safety without inflating the bill-of-materials.

Global Automotive Steering Market Trends and Insights

Rapid EPS Penetration in ICE & xEV Platforms

Electronic power steering is highly prevalent in China's passenger-car industry and is approaching ubiquity in Europe and Japan. OEMs gain fuel-saving benefits while unlocking regenerative braking compatibility for electric drivetrains. The technology now scales from compact cars to Class 8 trucks, as ZF's commercial-vehicle EPS delivers up to 8,000 Nm without hydraulic fluid. Column-assist units dominate the value B-segment, whereas rack-assist designs earn a share in premium cars that need higher precision and road feel. The accelerating shift keeps the automotive steering system market steadily growing.

Steer-by-wire Deployment in Premium EVs From 2025

Mercedes-Benz will introduce the first European production steer-by-wire system in 2026, following ZF's 2025 launch on NIO's ET9. Removing the mechanical shaft enables variable steering ratios that ease parking and enhance highway stability. Toyota's "One Motion Grip" wheel shows how 200-degree input strokes can replace the traditional 540-degree turn, improving ergonomics and cabin packaging. Redundant motors, power supplies, and haptic feedback maintain driver confidence, although consumer acceptance studies indicate a learning curve that may extend roll-out timelines beyond luxury nameplates.

Rare-earth Magnet Price Volatility Inflates EPS BOM

China controls roughly 70% of global rare-earth processing and has limited neodymium exports. Magnet costs already account for up to 25% of an EPS motor bill of materials. Ford's temporary halt of Explorer production exposed the risk to OEM schedules. Suppliers respond by advancing rare-earth-free innovations such as ZF's I2SM motor and Magna's investment in Niron Magnetics' iron-nitrogen Clean Earth Magnets.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Steering Columns to Meet Euro 7/CAFE Norms

- OEM Demand for ADAS-ready "Fail-operational" Architectures

- Automotive MCU Shortage Through 2026

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, steering columns and racks dominate the automotive steering system market, commanding a 39.26% revenue share. Integrated collapse mechanisms, multi-function switches, and driver-airbag modules keep the sub-segment essential across all platforms. In parallel, electric motors deliver the fastest expansion at an 8.91% CAGR through 2030 as brushless DC designs replace hydraulic pumps and belt-driven units. Cyber-secure electronic control units form the third-largest bucket, their content per vehicle climbing with every new over-the-air feature that UNECE R155 obliges manufacturers to secure.

Torque, angle, and position sensors advance in lockstep with steer-by-wire and ADAS features that depend on millisecond-accurate feedback. TDK's four-mode HAL 39xy chip illustrates how single-package solutions cut wiring weight while resisting magnetic noise from high-voltage powertrains. Suppliers able to merge motor, sensor, and ECU functions inside compact, shielded housings improve system reliability and lower warranty exposure, reinforcing their standing in the automotive steering system market.

In 2024, passenger cars dominated the global automotive steering system market, capturing 63.28% of the revenue. Meanwhile, light commercial vehicles emerged as the fastest-growing segment, boasting a robust 7.56% CAGR. E-commerce fleets value the precise low-speed maneuvering and lower maintenance that EPS provides, while autonomous delivery concepts lean on software-controlled steering for curb-side accuracy. Heavy commercial vehicles shift away from hydraulics as the latest rack-drive EPS units hit industrial torque outputs. Across classes, the automotive steering system market benefits from fleet owners' focus on fuel savings.

Within the passenger-car arena, battery electric models remove the engine vacuum source used by traditional hydraulics, making EPS mandatory. Sport utility vehicles secure a rising share as buyers favor higher ride positions, and their larger footprint translates into higher steering-system content. Multi-purpose vehicles and minivans leverage EPS packaging gains to offer flat-floor cabins. These combined shifts keep the automotive steering system industry on a stable path of unit and value growth.

The Automotive Steering System Market is Segmented by Component (Hydraulic Pump, Electric Motor, and More), Vehicle Type (Passenger Cars, Commercial Vehicles), Mechanism (Electronic Power Steering (EPS), Hydraulic Power Steering (HPS), Electrically Assisted Hydraulic Power Steering, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

In 2024, Asia-Pacific commands a 48.67% share of the automotive steering system market and is set to achieve a robust 6.81% CAGR through 2030. China's extensive electric-vehicle production base drives near-universal EPS fitment, while local challengers such as HIVE Steering undercut incumbent imports by bundling domestic silicon and magnet supply. Japan contributes specialized know-how, including JTEKT's steer-by-wire tests and NSK's low-friction bearing routes, even as NSK considers divesting its steering arm. Regional governments offer clear road maps for autonomous-driving certification, further enhancing demand for by-wire systems in the automotive steering system market.

Europe follows with high per-vehicle value as Euro 7 and UNECE cyber-rules reward advanced ECUs, lightweight columns, and redundant actuation. ZF and Bosch use local technical centers to tune steering feel for premium brands and are already shipping by-wire pilot volumes. OEMs, however, confront raw-material risks, which are highlighted when neodymium shortages force production pauses. That vulnerability fast-tracks research into rare-earth-free motor technology, allowing suppliers to raise content per vehicle without waiting for new model cycles.

North America sees steady take-up of EPS in pick-ups and sport utilities, the region's largest segments by volume. Fleet operators closely monitor the total cost of ownership, and the 3-5% fuel-saving edge of EPS helps underpin adoption. The United States is also a development hub for alignment-free installation and secure over-the-air software to update steering logic during ownership. Meanwhile, South America, the Middle East and Africa adopt electronified steering as factories upgrade platforms. These markets often leapfrog directly to EPS on new models, creating incremental upside for the automotive steering system market over the long run.

- JTEKT Corporation

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Nexteer Automotive Corporation

- NSK Ltd

- Mando Corporation

- Showa Corporation

- Hitachi Astemo

- Hyundai Mobis

- ThyssenKrupp Presta

- Schaeffler Group

- Denso Corporation

- Knorr-Bremse AG

- China Automotive Systems Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EPS Penetration In ICE & Xev Platforms

- 4.2.2 Steer-By-Wire Deployment In Premium Evs From 2025

- 4.2.3 Lightweight Steering Columns To Meet Euro 7/CAFE Norms

- 4.2.4 OEM Demand For ADAS-Ready "Fail-Operational" Architectures

- 4.2.5 Cyber-Secure ECU Mandates In UNECE R155 Markets

- 4.2.6 OTA-Upgradable Torque-Overlay Software Revenues

- 4.3 Market Restraints

- 4.3.1 Rare-Earth Magnet Price Volatility Inflates EPS BOM

- 4.3.2 Automotive MCU Shortage Through 2026

- 4.3.3 Steering-Feel Concerns Slowing Steer-By-Wire Rollout

- 4.3.4 Tier-1 Consolidation Limits OEM Bargaining Leverage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hydraulic Pump

- 5.1.2 Electric Motor

- 5.1.3 Steering Column / Rack

- 5.1.4 Sensors (Torque, Angle, Position)

- 5.1.5 Electronic Control Unit (ECU)

- 5.1.6 Other Components

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.1.1 Hatchback

- 5.2.1.2 Sedan

- 5.2.1.3 Sport Utility Vehicle

- 5.2.1.4 Multi-Purpose Vehicle

- 5.2.2 Commercial Vehicles

- 5.2.2.1 Light Commercial Vehicles

- 5.2.2.2 Medium and Heavy Commercial Vehicle

- 5.2.1 Passenger Cars

- 5.3 By Mechanism

- 5.3.1 Electronic Power Steering (EPS)

- 5.3.2 Hydraulic Power Steering (HPS)

- 5.3.3 Electro-hydraulic Power Steering (EHPS)

- 5.3.4 Steer-by-Wire

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 JTEKT Corporation

- 6.4.2 Robert Bosch GmbH

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Nexteer Automotive Corporation

- 6.4.5 NSK Ltd

- 6.4.6 Mando Corporation

- 6.4.7 Showa Corporation

- 6.4.8 Hitachi Astemo

- 6.4.9 Hyundai Mobis

- 6.4.10 ThyssenKrupp Presta

- 6.4.11 Schaeffler Group

- 6.4.12 Denso Corporation

- 6.4.13 Knorr-Bremse AG

- 6.4.14 China Automotive Systems Inc

7 Market Opportunities & Future Outlook

轻型车辆转向市场(按转向系统、机制、车辆类型、应用和销售管道)——2025-2032 年全球预测

轻型车辆转向市场(按转向系统、机制、车辆类型、应用和销售管道)——2025-2032 年全球预测 2032年汽车转向节市场预测:按车型、材料类型、製造流程、销售管道和地区进行的全球分析

2032年汽车转向节市场预测:按车型、材料类型、製造流程、销售管道和地区进行的全球分析 全球汽车转向节市场全球自我调整转向市场

全球汽车转向节市场全球自我调整转向市场 2025年全球机动车电气电子设备、转向及悬吊系统及内装市场报告2025年中重型卡车转向系统全球市场报告2025年全球汽车齿条齿轮转向系统市场报告2025年全球轻型卡车转向系统市场报告2025年转向装置全球市场报告汽车转向市场规模、份额和趋势分析:按组件、机制、车辆类型、地区和细分市场预测,2025 年至 2033 年

2025年全球机动车电气电子设备、转向及悬吊系统及内装市场报告2025年中重型卡车转向系统全球市场报告2025年全球汽车齿条齿轮转向系统市场报告2025年全球轻型卡车转向系统市场报告2025年转向装置全球市场报告汽车转向市场规模、份额和趋势分析:按组件、机制、车辆类型、地区和细分市场预测,2025 年至 2033 年