|

市场调查报告书

商品编码

1844569

汽车侧气帘:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Automotive Curtain Airbags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

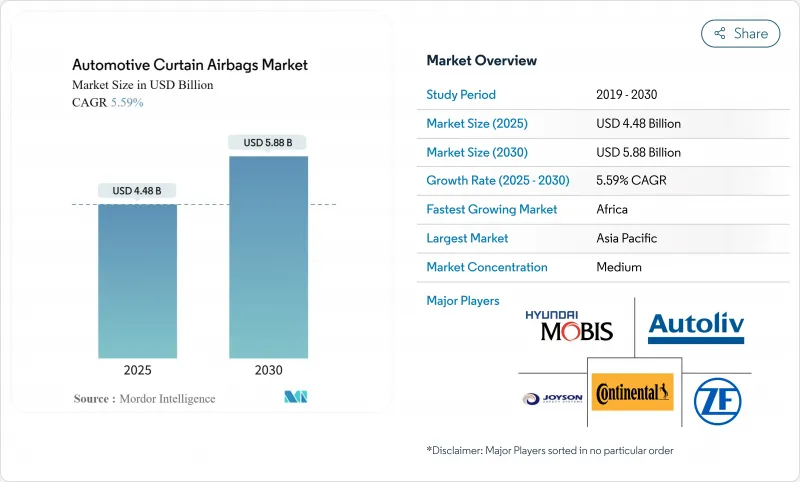

预计到 2025 年汽车侧气囊市场规模将达到 44.8 亿美元,到 2030 年将达到 58.8 亿美元,复合年增长率为 5.59%。

这一势头反映了全球侧面碰撞法规趋于严格、运动休旅车(SUV) 出货量激增以及电动车 (EV) 滑板平台带来的包装自由等因素的共同作用。强制符合 FMVSS 214、欧洲新车安全评鑑协会 (Euro NCAP) 远端通讯协定和 GTR 14 迫使所有大众市场原始设备製造商 (OEM) 在已开发市场和新兴市场都采用车顶导轨安全气帘,从而加快了标准安装率。印度、巴西和东协地区消费者对五星级碰撞评分的需求加剧了 OEM 对全长安全气帘的关注,而像 Toyobo-Indorama 在泰国的尼龙-6,6织造厂这样的合资企业正在缓解之前阻碍生产的布料压力。面向侧翻的 SUV 系列和广泛的跨界车产品组合构成了全球汽车车顶安全气帘市场最大的吸收管道。

全球汽车侧气帘市场趋势与洞察

严格的侧面碰撞和翻车法规促进全球采用

第 14 号全球技术法规统一了各个市场的头部伤害标准,并强制原始设备製造商在所有平台上指定使用侧气帘,而不仅仅是出口装饰。澳洲新的侧面碰撞法规在强制使用侧气帘时将乘员死亡率降低了 30%。先前,NHTSA 预测强制使用侧气帘每年将挽救 311 人的生命,现在透过对经验碰撞资料库的审查检验了这一目标。由于印度强制使用六个安全气囊,巴西的 NCAP 将星级评定与车顶导轨侧气帘挂钩,供应商受益于监管层迭,取消了侧气帘的可选状态。因此,织物、气体发生器和引发器的产量承诺提前数年锁定,即使在景气衰退时期也能确保生产能力。

全球范围内SUV和CUV的流行导致车顶导轨安装率的增加。

SUV是成长最快的轻型车类别,这一趋势直接增加了每辆车的头部安全帘数量。福特15英尺长的第五排安全气囊展现了保护拉伸厢型车和三排跨界车乘员所需的工程技术飞跃。美国公路安全保险协会(IHS)的数据证实,使用头部安全帘后,驾驶死亡率可降低37%。美国国内SUV的蓬勃发展以及印度从掀背车向紧凑型SUV的转变,将确保头部安全帘的销量在未来几年持续增长,进一步巩固其在全球需求曲线中的地位。

气囊缺陷导致召回和诉讼,从而提高风险溢价

美国国家公路交通安全管理局 (NHTSA) 宣布,由于侧面安全气囊充气帘存在破裂风险,将于 2024 年召回 298,700 辆克莱斯勒和道奇轿车,这再次引发了公众对弹片伤亡的担忧。法律和解导致供应商保险费上涨,并迫使原始设备製造商延长检验通讯协定,从而导致成本增加和车型发布延迟。 BMW、起亚和丰田在 2024-2025 年也面临类似的与侧气帘相关的召回,这加剧了投资者对汽车侧气帘产业的谨慎态度。

細項分析

到2024年,头部专用帘式气囊将占据汽车帘式气囊市场份额的51.25%。监管机构将继续强调头部损伤标准,以确保持续的需求。组合式帘式气囊(单一模组覆盖头部和躯干)到2030年的复合年增长率将达到8.31%,在所需组件较少的高端三排SUV中将越来越受欢迎。

製造商正在改进编织密度和通风孔形状,以维持六秒的充气,从而在多滚事故中保护乘员免受二次碰撞。奥托立夫最新的三排座椅跨度为2.5米,可在35毫秒内展开。随着中国MPV平台不断发展以适应叫车服务,超长窗帘有望引领汽车窗帘式安全气囊市场的下一波应用浪潮。

到2024年,SUV将占据汽车侧气帘市场规模的44.36%,复合年增长率为9.12%。 SUV重心较高,更容易发生翻车事故,因此需要增加车顶导轨的覆盖范围。 B级和C级跨界车在中国、印度和美国市场销售良好,这促使供应商开发更薄的模组,以覆盖全景天窗框架。

虽然轿车销量正在逐渐下降,但日本和韩国等地区的偏好仍使紧凑型四门车对窗帘的需求保持稳定。福特商用厢型车的窗帘展现了在不影响展开时效的情况下覆盖五排座椅的复杂性。电动SUV引入了新的技术变数。地板电池加强了侧裙,并将侵入力向上传递,因此窗帘必须保持更长时间的充气状态,以防止头部接触碎玻璃。

区域分析

受中国庞大生产基地和印度六缸安全气囊法规收紧的推动,亚太地区将在2024年引领汽车侧气囊市场,营收份额达46.18%。吉利和玛鲁蒂等本土汽车製造商正在将全长侧气囊安装到售价低于1万美元的掀背车上,以实现出口目标。在日本,面向全球供应混合式气体发生器的DAICEL,其烟火技术专长正在推动推进剂化学领域的突破。韩国正在将ADAS演算法与被动系统结合,以优化其高阶电动车(EV)产品线的部署时机。

在FMVSS 214合规性和SUV强劲销售的推动下,北美持续发挥关键作用。美国正在L4级自动驾驶测试中推进低温混合气体发生器的应用,为供应商提供极端气候解决方案的试验场。墨西哥组装厂正在为跨境车型采用统一的气帘规格,从而简化一级供应商的工装流程。加拿大正在根据区域零件配置规则支援模组化子次组件,为汽车产业增值。

欧洲正在优先考虑永续性和技术整合。在德国,高端电动车的普及推动了先进的排气孔测量仪的应用;而法国和义大利则鼓励采用机械缝合技术,以便在碰撞后快速放气,从而方便紧急救援。非洲儘管起步较低,但却是成长最快的地区,到2030年的复合年增长率将达到6.18%。南非的CKD工厂正在根据欧盟出口认证标准整合双级安全帘。肯亚和奈及利亚正在启动二手车进口限制,鼓励销售捆绑全套安全套件的新车。海湾合作委员会国家正采用联合国R135标准,要求日本和美国进口的SUV在海关检查时安装头部保护帘。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 严格的侧面碰撞和翻车法规(FMVSS 214、Euro NCAP、GTR 14)

- 全球SUV和CUV的日益普及,推动了车顶横桿安全气囊安装率的上升

- 整合 ADAS/主动安全套件,增强被动安全内容

- 新兴国家消费者对五星 NCAP 评级的需求

- 电动车滑板平台为大型侧气帘提供了空间

- 低温混合充气机可实现自动驾驶计程车的安全 OOP 部署

- 市场限制

- 气体发生器缺陷召回和诉讼(Takata、ARC)推高了风险溢价

- 入门级车型的价格压力限制了低成本汽车的标准化

- 尼龙6,6织物和引发剂供不应求导致OEM生产延迟

- 电动车结构电池组提供替代侧面碰撞保护

- 价值/供应链分析

- 技术展望

- 监管状况

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 侧气帘类型

- 躯干侧气帘

- 头部帘式安全气囊

- 组合式侧气帘

- 按车辆类型

- 掀背车

- 轿车

- 运动型多用途车

- 皮卡和 MPV

- 按最终用户

- OEM

- 售后市场

- 由 Inflator Technology 提供

- 火药

- 储存的气体

- 混合/低温混合

- 按销售管道

- 传统零售商

- 线上/直接面向消费者

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 摩洛哥

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Autoliv Inc.

- Joyson Safety Systems

- ZF Friedrichshafen AG

- Continental AG

- Hyundai Mobis Co. Ltd

- Toyoda Gosei Co. Ltd

- Daicel Corporation

- ARC Automotive Inc.

- iSi Automotive GmbH

- Ashimori Industry Co. Ltd

- Nihon Plast Co. Ltd

- Porcher Industries SA

- Toray Industries Inc.

- East Joy Long Motor

- Neaton Auto Products

- Sumitomo Corporation

- TRW Automotive Holdings Corp.

- Visteon Corporation

- Bosch Passive Safety Systems

第七章 市场机会与未来展望

The Automotive curtain airbags market size stands at USD 4.48 billion in 2025 and is projected to reach USD 5.88 billion by 2030, registering a 5.59% CAGR.

This momentum reflects the convergence of stringent global side-impact legislation, the boom in sport-utility vehicle (SUV) deliveries, and the packaging freedom created by electric-vehicle (EV) skateboard platforms . Mandatory compliance with FMVSS 214, Euro NCAP far-side protocols, and GTR 14 forces every volume carmaker to embed roof-rail curtains in both developed and emerging markets, accelerating standard fitment rates. Consumer demand for five-star crash scores across India, Brazil, and the ASEAN bloc intensifies OEM focus on full-length curtains, while joint ventures such as Toyobo-Indorama's nylon-6,6 weaving plant in Thailand mitigate fabric tightness that previously throttled production. Rollover-oriented SUV lines and expansive crossover portfolios thus become the single largest absorption channel for Automotive curtain airbags market deployments worldwide.

Global Automotive Curtain Airbags Market Trends and Insights

Stringent Side-Impact & Rollover Regulations Drive Global Adoption

Global Technical Regulation 14 aligns head-injury criteria across markets and forces OEMs to specify curtain airbags on every platform, not just export trims. Australia's new side-impact rule lowered occupant fatalities by 30% once curtain deployment became compulsory. Earlier, NHTSA projected its side-airbag mandate would save 311 lives per year-a target now verified through empirical crash-database reviews. With India moving toward mandatory six-airbag legislation and Brazil's NCAP tying star ratings to roof-rail curtains, suppliers benefit from a regulatory cascade that eliminates optional-equipment status for side curtains. Consequently, volume commitments for fabric, inflators, and initiators stay locked years in advance, safeguarding capacity utilization even in cyclical downturns.

Rising Global SUV & CUV Penetration Increases Roof-Rail Fitment

SUV deliveries represent the fastest-growing light-vehicle category, a trend that directly lifts per-vehicle curtain count. Ford's 15-ft-long, five-row airbag points to the engineering leap required to safeguard occupants in stretched vans and three-row crossovers. Insurance Institute for Highway Safety data corroborate a 37% drop in driver deaths when head-protecting curtains deploy. China's domestic SUV boom and India's migration from hatchbacks to compact SUVs assure a multi-year uplift in curtain volumes, further embedding this driver in global demand curves.

Recalls & Litigations from Inflator Defects Raise Risk Premium

NHTSA's 2024 recall of 298,700 Chrysler and Dodge sedans for Side Airbag Inflatable Curtain rupture risk revived public anxiety around shrapnel injuries. Legal settlements inflate supplier insurance premiums, while OEMs lengthen validation protocols, adding cost and delaying model launches. BMW, Kia, and Toyota faced similar curtain-related recalls in 2024-2025, reinforcing investor caution in the Automotive curtain airbags industry.

Other drivers and restraints analyzed in the detailed report include:

- Integration of ADAS with Passive Safety Suites

- Consumer Demand for 5-Star NCAP Ratings in Emerging Economies

- Price Pressure on Entry-Level Models Limits Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Head-only curtains secured 51.25% of the Automotive curtain airbags market share in 2024, supported by a proven 31% fatality reduction in side-impact crashes. Regulatory agencies continue to weigh head-injury criteria heavily, ensuring perennial demand. Combo curtains, which merge head and torso coverage in a single module, log an 8.31% CAGR through 2030 and gain traction in premium three-row SUVs seeking simpler bill-of-material counts.

Manufacturers refine weaving density and vent-hole geometry to sustain six-second inflation, protecting occupants against secondary hits in multi-roll incidents. Autoliv's latest three-row design spans 2.5 m and deploys in 35 ms, illustrating how suppliers address cabin length growth. As Chinese MPV platforms stretch to court ride-hailing services, ultra-long curtains promise the next adoption wave for the Automotive curtain airbags market.

SUVs accounted for 44.36% of the Automotive curtain airbags market size in 2024 and are on pace for a 9.12% CAGR. Their high center of gravity increases rollover exposure, necessitating extended roof-rail coverage. Crossovers in the B- and C-segments sell briskly in China, India, and the United States, pushing suppliers to develop low-profile modules that clear panoramic-sunroof frames.

Sedans decline gradually, yet regional tastes in Japan and South Korea maintain steady curtain demand for compact four-doors. Pickup trucks and MPVs create lucrative niches; Ford's commercial van curtain illustrates the complexity of spanning five seating rows without compromising deployment timing. EV SUVs bring new engineering variables: floor batteries stiffen side sills, transferring intrusion force upward, so curtains must remain inflated longer to prevent head contact with shattered glass.

The Global Automotive Curtain Airbags Market is Segmented by Curtain Airbag Type (Torso Curtain Airbags, Head Curtain Airbags and More), Vehicle Type (Hatchback, Sedan, Sports Utility Vehicles, and More), End User (OEM and Aftermarket), Inflator Technology (Pyrotechnic, Stored Gas, and More), Sales Channel (Traditional Dealerships and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads the Automotive curtain airbags market with 46.18% revenue share in 2024, driven by China's large production base and India's regulatory push for six airbags. Domestic OEMs such as Geely and Maruti embed full-length curtains even in sub-USD 10,000 hatches to meet export targets. Japan's pyrotechnic expertise propels propellant chemistry breakthroughs at Daicel, which supplies hybrid inflators worldwide. South Korea pairs ADAS algorithms with passive systems to refine deployment timing across premium electric vehicle (EV) lineups.

North America remains pivotal through FMVSS 214 compliance and strong SUV sales. United States Level-4 autonomy pilots promote low-temperature hybrid inflators, giving suppliers a proving ground for extreme-climate solutions. Mexico's assembly plants adopt identical curtain specifications for cross-border models, streamlining tier-one tooling. Canada supports module sub-assembly under regional parts-content rules, adding value to its auto sector.

Europe emphasizes sustainability and technology integration. Germany's premium EV expansion drives advanced vent-hole metering, while France and Italy encourage mechanical stitching that enables rapid post-crash deflation to aid emergency access. Africa, while starting from a lower base, is the fastest-growing region with a 6.18% CAGR through 2030. South African CKD plants integrate dual-stage curtains aligned with EU export homologation. Kenya and Nigeria launch used-vehicle import restrictions, compelling new-car sales that bundle full safety suites. GCC states adopt UN R135, obliging Japanese and US SUV imports to include head-protecting curtains at customs inspection.

- Autoliv Inc.

- Joyson Safety Systems

- ZF Friedrichshafen AG

- Continental AG

- Hyundai Mobis Co. Ltd

- Toyoda Gosei Co. Ltd

- Daicel Corporation

- ARC Automotive Inc.

- iSi Automotive GmbH

- Ashimori Industry Co. Ltd

- Nihon Plast Co. Ltd

- Porcher Industries SA

- Toray Industries Inc.

- East Joy Long Motor

- Neaton Auto Products

- Sumitomo Corporation

- TRW Automotive Holdings Corp.

- Visteon Corporation

- Bosch Passive Safety Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Side-Impact & Rollover Regulations (FMVSS 214, Euro NCAP, GTR 14)

- 4.2.2 Rising Global SUV & CUV Penetration Increasing Roof-Rail Airbag Fitment

- 4.2.3 Integration of ADAS/Active Safety Suites Boosting Passive Safety Content

- 4.2.4 Consumer Demand for 5-Star NCAP Ratings in Emerging Economies

- 4.2.5 EV Skateboard Platforms Freeing Packaging Space for Larger Curtain Airbags

- 4.2.6 Low-Temperature Hybrid Inflators Enabling Safe OOP Deployment in Robo-Taxis

- 4.3 Market Restraints

- 4.3.1 Recalls & Litigations From Inflator Defects (Takata, ARC) Raise Risk Premium

- 4.3.2 Price Pressure on Entry-Level Models Limits Standardisation in Low-Cost Cars

- 4.3.3 Nylon-6,6 Fabric & Initiator Supply Shortages Causing OEM Production Delays

- 4.3.4 Structural Battery Packs in EVs Offering Alternative Side-Impact Protection

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Curtain Airbag Type

- 5.1.1 Torso Curtain Airbags

- 5.1.2 Head Curtain Airbags

- 5.1.3 Combo Curtain Airbags

- 5.2 By Vehicle Type

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 Sports Utility Vehicle

- 5.2.4 Pick-up Trucks & MPVs

- 5.3 By End User

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Inflator Technology

- 5.4.1 Pyrotechnic

- 5.4.2 Stored Gas

- 5.4.3 Hybrid / Low-temperature Hybrid

- 5.5 By Sales Channel

- 5.5.1 Traditional Dealerships

- 5.5.2 Online & Direct-to-Consumer

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Morocco

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 Autoliv Inc.

- 6.4.2 Joyson Safety Systems

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Continental AG

- 6.4.5 Hyundai Mobis Co. Ltd

- 6.4.6 Toyoda Gosei Co. Ltd

- 6.4.7 Daicel Corporation

- 6.4.8 ARC Automotive Inc.

- 6.4.9 iSi Automotive GmbH

- 6.4.10 Ashimori Industry Co. Ltd

- 6.4.11 Nihon Plast Co. Ltd

- 6.4.12 Porcher Industries SA

- 6.4.13 Toray Industries Inc.

- 6.4.14 East Joy Long Motor

- 6.4.15 Neaton Auto Products

- 6.4.16 Sumitomo Corporation

- 6.4.17 TRW Automotive Holdings Corp.

- 6.4.18 Visteon Corporation

- 6.4.19 Bosch Passive Safety Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

安全气囊电子市场:按类型、车辆类型、技术和分销管道划分-2026-2032年全球预测安全气囊市场:按车辆类型、驱动方式、技术、销售管道和最终用户划分-2026-2032年全球预测软袋光检机市场:按技术、额定功率、应用和分销管道划分,全球预测(2026-2032年)

安全气囊电子市场:按类型、车辆类型、技术和分销管道划分-2026-2032年全球预测安全气囊市场:按车辆类型、驱动方式、技术、销售管道和最终用户划分-2026-2032年全球预测软袋光检机市场:按技术、额定功率、应用和分销管道划分,全球预测(2026-2032年) 安全气囊控制单元感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材质、安装方法、最终用户、功能和安装类型划分

安全气囊控制单元感测器市场分析及预测(至2035年):按类型、产品类型、技术、组件、应用、材质、安装方法、最终用户、功能和安装类型划分 全球安全气囊电子市场规模、份额、趋势和成长分析报告(2026-2034年)

全球安全气囊电子市场规模、份额、趋势和成长分析报告(2026-2034年) 商用车汽车安全气囊市场 - 全球产业规模、份额、趋势、机会及预测(按类型、销售管道、地区和竞争格局划分,2021-2031年)安全气囊感知器市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、地点、动力类型、地区和竞争格局划分,2021-2031年)汽车侧帘式气囊市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、需求类别、地区和竞争格局划分,2021-2031年

商用车汽车安全气囊市场 - 全球产业规模、份额、趋势、机会及预测(按类型、销售管道、地区和竞争格局划分,2021-2031年)安全气囊感知器市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、地点、动力类型、地区和竞争格局划分,2021-2031年)汽车侧帘式气囊市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、需求类别、地区和竞争格局划分,2021-2031年 汽车安全气囊市场机会、成长要素、产业趋势分析及2026年至2035年预测轻型汽车安全气囊市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、安全气囊类型、需求类别、纱线类型、地区和竞争格局划分,2021-2031年)

汽车安全气囊市场机会、成长要素、产业趋势分析及2026年至2035年预测轻型汽车安全气囊市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、安全气囊类型、需求类别、纱线类型、地区和竞争格局划分,2021-2031年)