|

市场调查报告书

商品编码

1844711

高强度贴合黏剂:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)High Strength Laminated Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

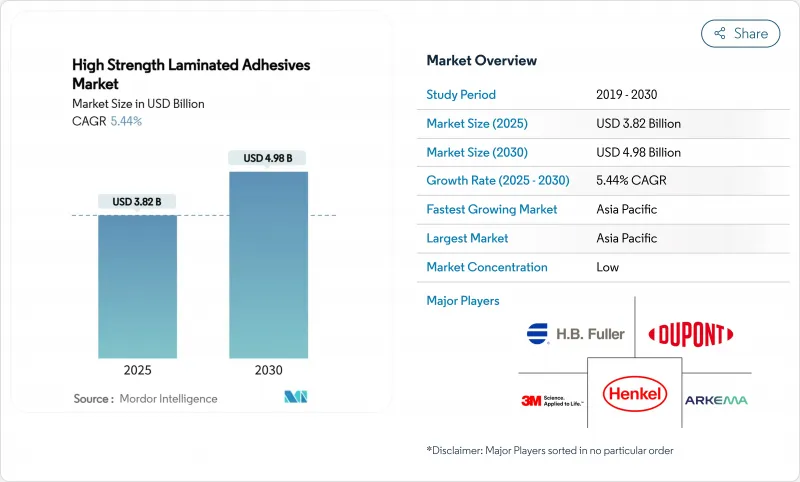

高强度贴合黏剂市场规模预计在 2025 年达到 38.2 亿美元,预计到 2030 年将达到 49.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.44%。

儘管环境法规日益严格,但对软包装的强劲需求、汽车轻量化的加速以及电子产品的快速小型化正在推动市场的成长轨迹。开发商正在竞相透过采用低VOC化学品、开发生物基原料和在亚太地区实现生产在地化来获取增加的下游产能。策略性资产剥离,例如陶氏出售其软包装贴合黏剂生产线,标誌着该行业围绕高价值利基市场的合理化,即使原材料波动继续挤压净利率。虽然技术向紫外光固化和水性系统的迁移正在加速,但溶剂型产品仍在关键的高性能层压领域占据主导地位,凸显了市场的转型。领先公司之间的整合受到大量区域专家的支持,这些专家支持靠近转换器和汽车工厂的供应。

全球高强度贴合黏剂市场趋势与洞察

对柔性和轻质包装的需求不断增加

随着品牌商追求降低成本、提升消费者便利性,软包装的产量持续成长。预计到2028年,该产业的产值将达到3,416亿美元,这将推动依赖高性能黏合剂系统的多层复合膜产量的成长。欧洲绿色新政强制要求使用单一材料包装袋和可回收阻隔膜,这需要支援封闭式回收的黏合剂,这为产品配方师开闢了高端市场。电子商务也变得越来越紧迫,Packsize和汉高报告称,使用Eco-Pax生物基热熔胶解决方案,3.4亿箱货物的温室气体排放量减少了32%。能够证明其食品接触安全性、低迁移性和脱墨释放性能的供应商正在贴合黏剂市场中获得价格优势。

汽车轻量化替代机械紧固件

现代汽车平均使用的黏合剂长度超过400线性英尺(约120公尺),而20年前仅为30英尺(约9公尺),这凸显了从铆钉和焊接到黏合线的结构性转变。白色混合材料车身、电池组封装和降噪层压板都提高了剪切强度和热循环耐久性的技术门槛。墨西哥汽车产业占GDP的6%,预计产量将成长13%,这将扩大北美供应链的在地化需求。随着原始设备製造商优先考虑错乱型和报废汽车回收,热塑性聚氨酯配方的市场份额正在扩大。

原物料价格波动

BASF将把包括1,4-丁二醇和N-Methyl Pyrrolidone在内的关键聚氨酯前驱物的价格上调0.08美元至0.10美元/磅,自2025年4月起生效。 79%的复合材料製造商表示树脂短缺,导致复合材料生产商的前置作业时间难以预测。对石油的依赖导致聚氨酯投入受原油波动影响,而生物基原料的供应规模有限。供应商正在透过季度定价条款和双重筹资策略来应对,但不确定性仍然限制了贴合黏剂市场的利润成长。

細項分析

到2024年,聚氨酯 (PU) 将占全球市场收入的43.18%,这突显了其在高柔性包装袋层压和高弹性汽车内装表皮方面的多功能性。预计到2030年,该细分市场的复合年增长率将达到6.41%,并将继续保持其在贴合黏剂市场的领先地位,因为加工商更青睐不同基材之间的强黏合。二异氰酸酯的监管压力正在加速向非异氰酸酯聚氨酯 (PU) 和生物基多元醇的转变,这些产品在不牺牲黏合强度的情况下减少了危险品标籤的使用。

生物基聚氨酯(Biocontent)的发展势头强劲,其前身源自木质素、大豆和蓖麻,可实现部分可再生的聚氨酯链。研究表明,非异氰酸酯聚氨酯(NIPU)的成功合成,其耐水解性与现有等级相当。丙烯酸系统在紫外光(UV)固化电子层压领域的市场份额正在不断扩大,因为该领域对光学清晰度和快速生产线速度至关重要。环氧树脂系统继续用于利基航太应用和风力叶片织物,这些领域需要卓越的化学稳定性,但其相对市场份额仍然较小。总体而言,聚氨酯创新正在推动贴合黏剂市场朝向低碳高性能解决方案迈进。

区域分析

预计到 2024 年,亚太地区将占全球需求的 44.18%,到 2030 年的复合年增长率将达到 6.04%。该地区的主要企业,包括中国的加工商和印度的新乐泰工厂,正在实现供应本地化、缩短前置作业时间并降低跨国公司的外汇风险。

北美仍然是一个高价值地区,汽车轻量化和食品接触安全标准推动创新。路博润在北卡罗来纳州斥资2000万美元扩建丙烯酸乳液项目,标誌着其特种级产品产能持续扩张。

欧洲更严格的排放法规正在推动技术变革,并扩大生产者责任制度,优先考虑可回收复合材料,促使该地区的复合材料生产商转向低单体聚氨酯和水性配方。拉丁美洲和中东地区正在成为新兴的需求中心,这些地区与工业化计划相关,并在私人消费方面正在迎头赶上,但基数较低。从区域来看,靠近下游包装和汽车製造商是贴合黏剂市场成功的关键。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 对柔性和轻质包装的需求不断增加

- 更换机械紧固件以减轻车辆重量

- 对低VOC(挥发性有机化合物)和无溶剂化学品的监管更加严格

- 全球製造地中电子产品的小型化

- 用于按需短版包装的紫外线 (UV) 固化生产线

- 市场限制

- 原物料价格波动

- 严格的溶剂排放法规

- 生物基聚氨酯原料供应瓶颈

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 依树脂类型

- 聚氨酯

- 丙烯酸纤维

- 环氧树脂

- 其他树脂类型(例如醋酸乙烯酯)

- 依技术

- 水性

- 溶剂型

- 热熔胶

- UV固化型

- 按用途

- 包装

- 车

- 工业

- 其他用途(电子、电气、建筑等)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Daubert Chemical Company

- DIC Corporation

- DuPont

- Franklin International

- HB Fuller Company

- Henkel AG and Co. KGaA

- Huntsman Corporation llc

- Jowat SE

- SAPICI SpA

第七章 市场机会与未来展望

The High Strength Laminated Adhesives Market size is estimated at USD 3.82 billion in 2025, and is expected to reach USD 4.98 billion by 2030, at a CAGR of 5.44% during the forecast period (2025-2030).

Robust flexible-packaging demand, accelerating automotive lightweighting and rapid electronics miniaturization keep the market firmly on a growth track despite tighter environmental rules. Producers are racing to introduce low-VOC chemistries, develop bio-based feedstocks and localize production in Asia-Pacific to capture rising downstream output. Strategic divestments, such as Dow's sale of its flexible-packaging laminating adhesives line, illustrate an industry streamlining around high-value niches while raw-material volatility pressures margins. Technology migration toward UV-curable and water-borne systems is gathering pace, yet solvent-based products still dominate critical high-performance laminations, highlighting a market in transition. Consolidation among tier-one players is tempered by a long tail of regional specialists that anchor supply close to converters and car plants.

Global High Strength Laminated Adhesives Market Trends and Insights

Escalating Demand for Flexible and Lightweight Packaging

Flexible packaging volumes keep rising as brand owners pursue down-gauging and consumer convenience. The sector is projected to hit USD 341.6 billion by 2028, lifting multilayer laminate output that relies on high-performance bonding systems . Mono-material pouches and recyclable barrier films mandated under the European Green Deal require adhesives compatible with closed-loop recycling, opening premium niches for product formulators. E-commerce adds urgency, with Packsize and Henkel reporting a 32% greenhouse-gas cut across 340 million shipper boxes when using Eco-Pax bio-based hot-melt solutions. Suppliers able to certify food-contact safety, low migration and de-inking debonding gain a pricing edge in the laminating adhesives market.

Automotive Lightweighting Replacing Mechanical Fasteners

Modern vehicles average more than 400 linear feet of adhesive versus 30 feet two decades ago, underscoring the structural shift from rivets and welds to bonding lines . Mixed-material bodies in white, battery-pack encapsulation and noise-damping laminates all raise the technical bar for shear strength and thermal-cycling durability. Mexico's auto sector, contributing 6% to national GDP, is on track for 13% production growth, amplifying localized demand in North American supply corridors. Thermoplastic polyurethane formulations gain share as OEMs prioritize dismantlability and end-of-life recycling.

Raw-Material Price Volatility

Raw material price volatility continues to pressure laminating adhesives manufacturers, with BASF implementing price increases of USD 0.08-0.10 per pound for key polyurethane precursors including 1,4-Butanediol and N-Methylpyrrolidone effective April 2025. Seventy-nine percent of composites fabricators cite resin shortages, exposing formulators to unpredictable lead times. Petroleum dependency keeps polyurethane inputs tethered to crude swings, while bio-based feedstocks face limited scale. Suppliers respond with quarterly pricing clauses and dual-sourcing strategies, yet the uncertainty still trims margin expansion in the laminating adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward Low-Volatile Organic Compound (VOC) and Solvent-Free Chemistries

- Electronics Miniaturization in Global Manufacturing Hubs

- Stringent Solvent-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane (PU) claimed 43.18% of global revenue in 2024, underscoring its versatility in high-flexibility pouch laminations and resilient automotive interior skins. The segment is projected to grow at a 6.41% CAGR through 2030, keeping its lead in the laminating adhesives market as converters favor robust adhesion across heterogeneous substrates. Regulatory pressure on diisocyanates accelerates migration to non-isocyanate polyurethane (PU) and bio-based polyol routes that curb hazard labeling without sacrificing bond strength.

Bio-content gains momentum with lignin-, soy-, and castor-derived precursors enabling partially renewable polyurethane chains. Research demonstrates successful Non-Isocyanate Polyurethane (NIPU) syntheses that retain hydrolysis resistance equal to incumbent grades. Acrylic systems pick up share in ultraviolet (UV)-curable electronics laminations where optical clarity and rapid line speed are paramount. Epoxies continue to serve niche aerospace and wind-blade fabrics demanding extreme chemical stability, yet their relative market slice stays modest. Overall, innovation in polyurethane keeps the laminating adhesives market moving toward lower-carbon yet high-performance solutions.

The High Strength Laminating Adhesives Market Report is Segmented by Resin Type (Polyurethane, Acrylic, Epoxy, Other Resin Types), Technology (Water-Borne, Solvent-Based, Hot-Melt, UV-Curable), Application (Packaging, Automotive, Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 44.18% of global demand in 2024 and is anticipated to expand at a 6.04% CAGR through 2030, fueled by chemical cluster investment and rising per-capita packaged-goods consumption. Regional heavyweights, including China's converters and India's new Loctite plant, localize supply, shorten lead times and cut currency risk for multinationals.

North America remains a high-value arena where automotive lightweighting and food-contact safety standards steer innovation. Lubrizol's USD 20 million acrylic-emulsion expansion in North Carolina illustrates continued capacity reinforcement for specialty grades.

Europe's stringent emission rules catalyze technology pivots and extend producer-responsibility schemes that prioritize recycle-ready laminations, pushing regional formulators into low-monomer polyurethane and water-borne recipes. Latin America and the Middle East present emergent demand nodes linked to industrialization projects and consumer spending catch-up, albeit from lower bases. The geography split shows that proximity to downstream packagers and automakers remains decisive for success in the laminating adhesives market.

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Daubert Chemical Company

- DIC Corporation

- DuPont

- Franklin International

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Huntsman Corporation llc

- Jowat SE

- SAPICI S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Demand for Flexible and Lightweight Packaging

- 4.2.2 Automotive Lightweighting Replacing Mechanical Fasteners

- 4.2.3 Regulatory Push Toward Low-VOC (Volatile Organic Compound) and Solvent-Free Chemistries

- 4.2.4 Electronics Miniaturization in Global Manufacturing Hubs

- 4.2.5 Ultraviolet (UV)-Curable Lines for On-Demand Short-Run Packaging

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Stringent Solvent-Emission Regulations

- 4.3.3 Supply Bottlenecks in Bio-Based Polyurethane Feedstocks

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyurethane

- 5.1.2 Acrylic

- 5.1.3 Epoxy

- 5.1.4 Other Resin Types (Vinyl Acetate, etc.)

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-based

- 5.2.3 Hot-melt

- 5.2.4 UV-curable

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Other Applications (Electronics and Electrical, Construction, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Daubert Chemical Company

- 6.4.7 DIC Corporation

- 6.4.8 DuPont

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG and Co. KGaA

- 6.4.12 Huntsman Corporation llc

- 6.4.13 Jowat SE

- 6.4.14 SAPICI S.p.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Introduction of Nano-Adhesives

卫生黏合剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、形态、组成、功能、工艺智慧黏合剂技术市场分析及预测(至2035年):依类型、产品、技术、应用、材料类型、最终用户、功能、製程、形式及解决方案划分

卫生黏合剂市场分析及预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、形态、组成、功能、工艺智慧黏合剂技术市场分析及预测(至2035年):依类型、产品、技术、应用、材料类型、最终用户、功能、製程、形式及解决方案划分 东南亚黏合剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚黏合剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 胺甲酸乙酯黏合剂市场规模、份额和成长分析(按化学成分、应用领域、配方类型、固化机制和地区划分)-2026-2033年产业预测

胺甲酸乙酯黏合剂市场规模、份额和成长分析(按化学成分、应用领域、配方类型、固化机制和地区划分)-2026-2033年产业预测 纺织黏合剂市场-全球产业规模、份额、趋势、机会及预测(按应用、树脂类型、终端用户产业、盈利潜力、地区和竞争格局划分,2021-2031年)

纺织黏合剂市场-全球产业规模、份额、趋势、机会及预测(按应用、树脂类型、终端用户产业、盈利潜力、地区和竞争格局划分,2021-2031年) 2A 和 3A 薄膜市场:按材料组成、产品形式、应用、技术类型、薄膜厚度范围和粘合类型划分——2026 年至 2032 年全球预测低压成型黏合剂市场(按树脂类型、固化技术、设备类型、包装类型、应用和最终用途产业划分),全球预测,2026-2032年单组分聚氨酯接着剂市场:依包装、应用方法、最终用途和通路划分-2026-2032年全球预测双组分高导热凝胶市场按产品类型、基板类型、应用、终端用户产业和分销管道划分-2026-2032年全球预测双组分黏合剂市场按产品类型、形态、包装、应用、最终用户和分销管道划分,全球预测(2026-2032年)

2A 和 3A 薄膜市场:按材料组成、产品形式、应用、技术类型、薄膜厚度范围和粘合类型划分——2026 年至 2032 年全球预测低压成型黏合剂市场(按树脂类型、固化技术、设备类型、包装类型、应用和最终用途产业划分),全球预测,2026-2032年单组分聚氨酯接着剂市场:依包装、应用方法、最终用途和通路划分-2026-2032年全球预测双组分高导热凝胶市场按产品类型、基板类型、应用、终端用户产业和分销管道划分-2026-2032年全球预测双组分黏合剂市场按产品类型、形态、包装、应用、最终用户和分销管道划分,全球预测(2026-2032年)