|

市场调查报告书

商品编码

1846161

结构电子学:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Structural Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

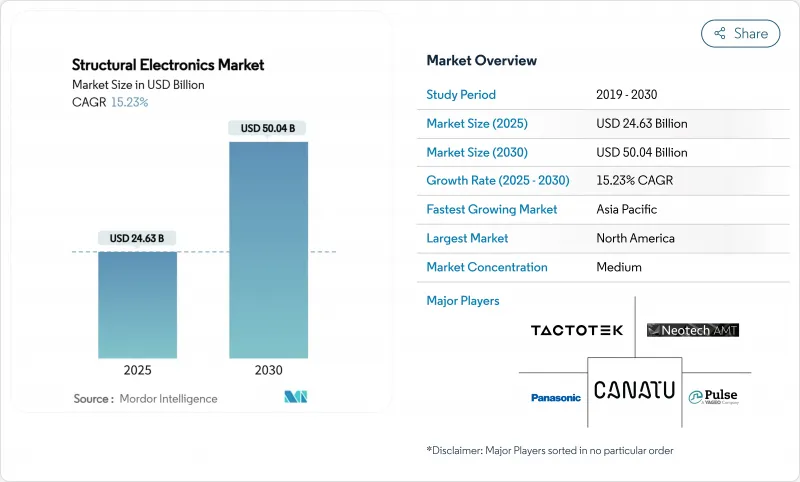

预计到 2025 年,结构电子市场规模将达到 246.3 亿美元,到 2030 年将达到 500.4 亿美元,复合年增长率为 15.23%。

这种加速成长反映了汽车轻量化法规的快速推进、半导体政策激励措施的出台以及3D套模电子技术的突破性进展——该技术可将电路直接嵌入承重部件中。汽车製造商目前将感测器蒙皮和结构电池整合到座舱面板中,以减轻重量并延长电动车的续航里程;亚太地区的消费性电子工厂正在扩大曲面触控外壳的量产规模。诸如欧洲的《晶片法案》和美国的《晶片与科学法案》等法规正在为先进封装中心注入资金,从而简化结构整合。亚太地区製造业的深厚实力将继续支撑地理成长,而中东地区的国防和智慧基础设施计划将推动未来的需求。

全球结构电子市场趋势与洞察

汽车轻量化和以电动车为中心的车内电子设备正在蓬勃发展

欧洲汽车製造商正面临日益严格的车队排放法规,这些法规优先考虑采用整合电力电子设备的轻量化车辆。 Synonus AB 的碳纤维结构电池实现了 70% 的续航里程提升和 50% 的重量减轻,展示了单一复合材料零件如何同时实现储能和承载机械负载。该设计还透过以半固体化学物质取代易燃的液态电解质,有效降低了热失控的风险。大众汽车等汽车製造商正将这些电池与安森美半导体的碳化硅逆变器配合使用,以减少组件数量并提高动力传动系统的效率。围绕钢铝超高速铸造技术的争议进一步凸显了将电路整合到任何结构材料中的价值。因此,结构电子技术正在迅速发展,并在底盘、车门和仪表板等领域中广泛应用。

亚太地区消费性设备中3D套模电子技术的广泛应用

中国、韩国和越南的消费性设备契约製造製造商正在将3D套模电子技术标准化,该技术将导电油墨、薄膜和树脂整合于单一模塑製程。 TactoTek的射出成型结构电子(IMSE)製程检验,与传统组装相比,可减少60%的温室气体排放和70%的塑胶用量。科思创的Makrofol聚碳酸酯薄膜可在超薄外壳内实现触控照明和触觉回馈。区域性研究,例如香港大学的有机电化学晶体管,正在推动下一波穿戴式装置和感测器运算的发展。东南亚的PCB产业产值已超过20亿美元,为这些结构外壳提供多层背板。加速的模具週期支援智慧型手机、穿戴式耳机和智慧家庭中心等产品的上市,从而推动了个人电子产品结构电子市场的发展。

亚洲以外地区供不应求

奈米碳管油墨和浆料主要集中在少数几家中国工厂,占全球产量的40%以上。飓风摧毁了北卡罗来纳州的高纯度石英矿藏,暴露了半导体基板关键原料基板的脆弱性。近期美国和欧洲生产商宣布的碳奈米管产能扩张计画仍无法满足市场需求成长预期。因此,汽车和航太的买家将面临更长的前置作业时间和更高的价格,这将限制结构电子市场的扩张,直到实现多元化采购。

细分市场分析

到2024年,感测器和天线类别将贡献34.7%的收入,这主要得益于ADAS(高级驾驶辅助系统)和飞机安全监控的强制性要求。光纤阵列正被整合到飞行复合材料面板中,雷达和电容式触控技术正被整合到乘用车仪錶板中。到2030年,太阳能光电发电将以17.5%的复合年增长率实现最高增长,这主要得益于可弯曲以适应建筑内部结构的柔性钙钛矿组件和可穿戴标籤的普及。结构整合技术无需单独的外壳即可实现发电,从而降低了组装成本,并为资产追踪和室内农业等领域开闢了新的应用。

结构电池和微型超级电容器正超越原型阶段,MXene墨水装置已实现611 F cm⁻³的体积电容,便是最好的证明。显示器也正顺应汽车设计潮流,采用OLED和microLED薄膜,朝着连续曲线的方向发展。互连材料面临铜的挥发性问题,但银奈米线和MXene能够在可弯曲的形态中保持导电性。这些转变将拓展结构电子市场,将感测、能量和显示功能整合于单一层压板中。

套模电子技术将薄膜、油墨和树脂熔合在一起,製成可直接安装的轻量化零件,预计到2024年,该技术的收入将增加51.3%。汽车门饰板现在采用背光控制,无需单独的PCB,从而减轻了线束的重量。消费级穿戴装置也采用相同的製程製造IP68防护等级的外壳。在DARPA的AMME计画的推动下,积层製造技术将以18.2%的复合年增长率快速发展,直接在3D基板上列印复杂的微电路。 MXene油墨的喷墨列印技术可以製造高能量密度电容器,而多光子微影术则开创了可列印有机生物电子元件的先河。

网版印刷和柔版印刷能够经济高效地在电器面板上印刷大面积加热器和天线。喷墨平台则可在模具转移到大量生产之前製作精细原型。这项技术的广泛应用将拓宽结构电子市场的准入管道,并加速其在大量生产和客製化生产中的应用。

区域分析

亚太地区预计到2024年将占全球销售额的37.9%,这主要得益于该地区庞大的半导体、PCB和模具製造生态系统。中国正朝着垂直整合的方向发展,而泰国和马来西亚也在增加其全球供应供给能力。日本供应全球一半以上的积层陶瓷电容,而像村田製作所和QuantumScape这样的伙伴关係正向固态电池陶瓷领域拓展业务。

欧洲的结构电子市场正受惠于汽车电气化进程的里程碑以及800亿欧元(940.6亿美元)的晶片法案基金,该基金的目标是到2030年占据全球半导体市场20%的份额。德国原始设备製造商正在改进其嵌入式电路的千兆铸件,而法国建设公司正在维修建筑幕墙面上试用太阳能感测器皮肤。

中东和非洲地区将以15.7%的复合年增长率实现最快成长,主要受国防现代化和智慧城市发展驱动。阿联酋的EDGE集团正在探索人工智慧卫星链路,这需要共形天线和轻型电源。儘管地方政府正透过抵销贸易计画吸引供应商,扶持国内组装线,但该地区仍依赖进口大部分奈米材料,这一缺口可能在未来十年后半段限製成长。

北美地区在新的《晶片技术创新法案》(CHIPS Act)拨款支持下,航太计划和先进封装代工厂持续保持发展势头。波音公司收购Spirit公司旨在加强感测器整合到飞机机身部件的应用。联邦法规鼓励国内供应,促使结构电子市场参与企业将材料、印刷和成型能力集中布局。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧洲的轻量化汽车和以电动车为中心的车内电子设备的激增

- 亚太地区消费性电子产品大规模采用3D模内套模电子技术

- 美国联邦航空管理局(FAA)推广复合美国联邦复合材料整合感测器蒙皮(北美)

- 用于智慧建筑中无电池物联网节点的印刷光伏电池

- 边缘人工智慧穿戴装置推动医疗保健领域伸缩性结构的形成

- 以色列和美国对共形天线和智慧表面的国防需求

- 市场限制

- 航太结构电子元件的复杂鑑定週期

- 积层製造生产线的週期时间和吞吐量有限

- 高温聚合物基板的分层风险 - 汽车

- 亚洲以外地区供不应求

- 产业生态系分析

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方和消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场规模及成长预测(金额)

- 由 Integrants 提供

- 太阳能发电

- 电池/超级电容

- 感测器和天线

- 显示器(OLED/微型LED)

- 导体和互连线

- 依製造技术

- 套模电子(IME)

- 积层製造/3D列印

- 气溶胶喷射和喷墨列印

- 丝网/柔版印刷

- 按材质

- 导电油墨(银、铜、碳、奈米材料)

- 基板(聚合物、玻璃、复合材料、热固性材料)

- 封装和黏合剂

- 透过使用

- 汽车-内装和外观

- 航太与国防 - 机身、智慧蒙皮

- 消费性电子产品-白色家电、手持设备

- 医疗保健/医疗设备

- 工业和楼宇自动化

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家(丹麦、瑞典、挪威、芬兰)

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 东南亚

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东

- 波湾合作理事会成员国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- TactoTek Oy

- Molex LLC

- Panasonic Holdings Corp.

- Canatu Oy

- Neotech AMT GmbH

- Pulse Electronics(Yageo)

- Optomec Inc.

- Odyssian Technology LLC

- Aconity3D GmbH

- T-ink Inc.

- Boeing Co.

- Henkel AG and Co. KGaA

- DuPont de Nemours Inc.

- 3D Systems Corp.

- Teijin Ltd.

- PPG Industries Inc.

- Flex Ltd.

- General Electric Co.

- Samsung Electro-Mechanics

- Continental AG

第七章 市场机会与展望

- 閒置频段与未满足需求评估

The structural electronics market reached USD 24.63 billion in 2025 and is forecast to rise to USD 50.04 billion by 2030, translating to a 15.23% CAGR.

This acceleration reflects fast-moving vehicle lightweighting mandates, semiconductor policy incentives, and fresh breakthroughs in 3-D in-mold electronics that embed circuitry directly into load-bearing parts. Automotive manufacturers now fold sensor skins and structural batteries into cabin panels to trim weight and extend electric-vehicle range, while Asia-Pacific consumer-electronics plants scale volume production of curved, touch-activated housings. Regulations such as the European Chips Act and the U.S. CHIPS and Science Act pump capital into advanced packaging hubs that simplify structural integration. Geographic growth remains anchored in Asia-Pacific manufacturing depth, but defense and smart-infrastructure projects in the Middle East lift future demand.

Global Structural Electronics Market Trends and Insights

Automotive light weighting and EV-centric cabin electronics surge

European automakers face firm fleet-emission rules that prioritize lighter vehicles equipped with integrated power electronics. Sinonus AB's carbon-fiber structural battery shows a 70% range boost coupled with 50% weight reduction, illustrating how a single composite part can both store energy and carry mechanical loads. The design also mitigates thermal-runaway concerns by replacing flammable liquid electrolytes with semi-solid chemistries. Automakers such as Volkswagen link these batteries with silicon-carbide inverters from onsemi to shrink component count and raise drivetrain efficiency. The debate around steel versus aluminum gigacasting further underscores the value of embedding circuitry into any structural material. The result is a rapid uptick in structural electronics market adoption across chassis, doors, and instrument panels.

Mass adoption of 3-D in-mold electronics in Asia-Pacific consumer devices

Consumer-device contract manufacturers in China, South Korea, and Vietnam are standardizing 3-D in-mold electronics that combine conductive inks, films, and resins in a single molding step. TactoTek's injection-molded structural electronics (IMSE) process has verified a 60% drop in greenhouse-gas emissions and 70% less plastic usage versus traditional assembly. Covestro's Makrofol polycarbonate films enable touch lighting and haptic feedback inside ultrathin shells. Regional research, such as organic electrochemical transistors from the University of Hong Kong, drives the next wave of wearable, on-sensor computing. Southeast Asia's PCB sector, already above USD 2 billion in output, supplies multilayer backplanes that mate with these structural housings. Accelerated tooling cycles support product launches in smartphones, hearables, and smart-home hubs, lifting the structural electronics market across personal electronics.

Shortage of conductive nanomaterial supply outside Asia

Carbon-nanotube inks and pastes are concentrated in a handful of Chinese plants that together command over 40% of global output. Hurricanes that disrupted high-purity quartz in North Carolina exposed parallel weaknesses in raw-material chains essential for semiconductor substrates. Recent CNT scale-up announcements from U.S. and European producers remain short of demand growth projections. Automotive and aerospace buyers consequently face longer lead times and price spikes, constraining structural electronics market expansion until diversified sourcing becomes available.

Other drivers and restraints analyzed in the detailed report include:

- FAA push for integrated sensor skins in composite airframes

- Printed photovoltaics for battery-less IoT nodes in smart buildings

- Complex qualification cycles for structural electronics in aerospace

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The sensor and antenna category contributed 34.7% revenue in 2024, buoyed by mandates for advanced driver-assistance systems and aircraft safety monitoring. Flight composite panels now embed fiber-optic arrays, whereas passenger-vehicle dashboards integrate radar and capacitive touch in one molded insert. Photovoltaics post the strongest 17.5% CAGR through 2030, driven by flexible perovskite modules that curve around building interiors and wearable tags. Structural integration allows power generation without separate housing, shrinking assembly cost, and opening new applications in asset tracking and indoor agriculture.

Structural batteries and micro-super-capacitors move beyond prototypes, illustrated by MXene ink devices delivering 611 F cm-3 volumetric capacitance. Displays follow automotive styling trends toward continuous curved surfaces enabled by OLED and micro-LED films. Interconnect materials confront copper volatility yet gain from silver-nanowire and MXene alternatives that sustain conductivity in bendable formats. Together, these shifts expand the structural electronics market as designers combine sensing, energy, and display functions within a single laminate.

In-mold electronics captured 51.3% revenue in 2024 by fusing films, inks, and resin into lightweight parts that ship ready-to-install. Automotive door trims now host back-lit controls without separate PCBs, cutting wire harness weight. Consumer wearables adopt the same process for IP68-rated casings. Additive manufacturing records the highest 18.2% CAGR, supported by DARPA's AMME program that 3-prints complex micro-circuits directly onto three-dimensional substrates. Aerosol-jet printing of MXene inks scales energy-dense capacitors, while multiphoton lithography pioneers printable organic bioelectronics.

Screen and flexographic presses remain cost-effective for large-area heaters and antennas on appliance panels. Inkjet platforms supply fine-feature prototypes before tooling commits to mass molding. This technology spreads, widening entry options, accelerating structural electronics market adoption in both high-volume and bespoke production runs.

Structural Electronics Market Report is Segmented by Integrant (Photovoltaics, Batteries/Super-capacitors, and More), Manufacturing Technology (In-Mold Electronics, Additive Manufacturing/3-D Printing, and More), Material (Conductive Inks, Substrates, Encapsulation and Adhesives), Application (Automotive, Aerospace and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivered 37.9% of 2024 revenue by virtue of high-volume semiconductor, PCB, and molding ecosystems. China drives vertical integration, while Thailand and Malaysia add capacity that feeds global supply. Japan supplies over half the world's multilayer ceramic capacitors, and partnerships such as Murata with QuantumScape diversify into solid-state battery ceramics.

Europe's structural electronics market gains from automotive electrification milestones and EUR 80 billion (USD 94.06 billion) in Chips Act funds, targeting a 20% global semiconductor share by 2030. German OEMs refine giga casting with embedded circuits, whereas French construction firms pilot PV-powered sensor skins on retrofit facades.

The Middle East and Africa record the fastest 15.7% CAGR, propelled by defense modernization and smart-city rollouts. UAE's EDGE Group explores AI-enabled satellite links that demand conformal antennas and lightweight power sources. Local governments entice suppliers with offset programs that seed domestic assembly lines, yet the region still imports most nanomaterials, a gap that could temper late-decade growth.

North America keeps momentum through aerospace projects and fresh CHIPS Act subsidies for advanced packaging foundries. Boeing's acquisition of Spirit targets tighter integration of sensor-ready fuselage sections. Federal rules now favor home-grown supply, nudging structural electronics market participants to co-locate material, printing, and molding capabilities.

- TactoTek Oy

- Molex LLC

- Panasonic Holdings Corp.

- Canatu Oy

- Neotech AMT GmbH

- Pulse Electronics (Yageo)

- Optomec Inc.

- Odyssian Technology LLC

- Aconity3D GmbH

- T-ink Inc.

- Boeing Co.

- Henkel AG and Co. KGaA

- DuPont de Nemours Inc.

- 3D Systems Corp.

- Teijin Ltd.

- PPG Industries Inc.

- Flex Ltd.

- General Electric Co.

- Samsung Electro-Mechanics

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive Lightweighting and EV-Centric Cabin Electronics Surge in Europe

- 4.2.2 Mass Adoption of 3-D In-Mold Electronics in Asia-Pacific Consumer Devices

- 4.2.3 FAA Push for Integrated Sensor Skins in Composite Airframes (North America)

- 4.2.4 Printed Photovoltaics for Battery-Less IoT Nodes in Smart Buildings

- 4.2.5 Edge-AI Wearables Driving Stretchable Structural Circuits in Healthcare

- 4.2.6 Defense Demand for Conformal Antennas and Smart Surfaces (Israel and US)

- 4.3 Market Restraints

- 4.3.1 Complex Qualification Cycles for Structural Electronics in Aerospace

- 4.3.2 Limited Cycle-Time Throughput of Additive Manufacturing Lines

- 4.3.3 Delamination Risks in High-Heat Polymer Substrates - Automotive

- 4.3.4 Shortage of Conductive Nanomaterial Supply Outside Asia

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Integrant

- 5.1.1 Photovoltaics

- 5.1.2 Batteries/Super-capacitors

- 5.1.3 Sensors and Antennas

- 5.1.4 Displays (OLED/Micro-LED)

- 5.1.5 Conductors and Interconnects

- 5.2 By Manufacturing Technology

- 5.2.1 In-Mold Electronics (IME)

- 5.2.2 Additive Manufacturing/3-D Printing

- 5.2.3 Aerosol Jet and Inkjet Printing

- 5.2.4 Screen/Flexographic Printing

- 5.3 By Material

- 5.3.1 Conductive Inks (Silver, Copper, Carbon, Nanomaterial)

- 5.3.2 Substrates (Polymer, Glass, Composite, Thermoset)

- 5.3.3 Encapsulation and Adhesives

- 5.4 By Application

- 5.4.1 Automotive - Interior and Exterior

- 5.4.2 Aerospace and Defense - Airframe, Smart Skins

- 5.4.3 Consumer Electronics - Whitegoods and Handhelds

- 5.4.4 Healthcare/Medical Devices

- 5.4.5 Industrial and Building Automation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Gulf Cooperation Council Countries

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TactoTek Oy

- 6.4.2 Molex LLC

- 6.4.3 Panasonic Holdings Corp.

- 6.4.4 Canatu Oy

- 6.4.5 Neotech AMT GmbH

- 6.4.6 Pulse Electronics (Yageo)

- 6.4.7 Optomec Inc.

- 6.4.8 Odyssian Technology LLC

- 6.4.9 Aconity3D GmbH

- 6.4.10 T-ink Inc.

- 6.4.11 Boeing Co.

- 6.4.12 Henkel AG and Co. KGaA

- 6.4.13 DuPont de Nemours Inc.

- 6.4.14 3D Systems Corp.

- 6.4.15 Teijin Ltd.

- 6.4.16 PPG Industries Inc.

- 6.4.17 Flex Ltd.

- 6.4.18 General Electric Co.

- 6.4.19 Samsung Electro-Mechanics

- 6.4.20 Continental AG

7 MARKET OPPORTUNITIES AND OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

3D列印半导体波导管市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程及最终用户划分印刷电子市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、材料、装置、製程及最终用户划分

3D列印半导体波导管市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程及最终用户划分印刷电子市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、材料、装置、製程及最终用户划分 全球印刷电子市场:按技术、材料、应用、最终用户、国家和地区分類的行业分析、市场规模、份额和2025-2032年预测

全球印刷电子市场:按技术、材料、应用、最终用户、国家和地区分類的行业分析、市场规模、份额和2025-2032年预测 2026年全球印刷电子市场报告2026年结构电子全球市场报告

2026年全球印刷电子市场报告2026年结构电子全球市场报告 印刷电子市场-全球产业规模、份额、趋势、机会与预测:印刷製程、材料、设备、终端用户、地区和竞争格局,2021-2031年

印刷电子市场-全球产业规模、份额、趋势、机会与预测:印刷製程、材料、设备、终端用户、地区和竞争格局,2021-2031年 印刷电子材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)

印刷电子材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年) 日本印刷电子市场报告(按材料(油墨、基材)、技术(喷墨、网版印刷、凹版印刷、柔版印刷)、设备(显示器、光伏、照明、RFID 及其他)和地区划分,2026-2034 年)

日本印刷电子市场报告(按材料(油墨、基材)、技术(喷墨、网版印刷、凹版印刷、柔版印刷)、设备(显示器、光伏、照明、RFID 及其他)和地区划分,2026-2034 年) 印刷电子市场规模、份额和成长分析(按技术、材料、装置类型、最终用途产业和地区划分)-2026-2033年产业预测印刷电子市场规模、份额和趋势分析报告:按材料、技术、装置、地区和细分市场预测(2026-2033 年)

印刷电子市场规模、份额和成长分析(按技术、材料、装置类型、最终用途产业和地区划分)-2026-2033年产业预测印刷电子市场规模、份额和趋势分析报告:按材料、技术、装置、地区和细分市场预测(2026-2033 年)