|

市场调查报告书

商品编码

1846266

抗菌包装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Antimicrobial Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

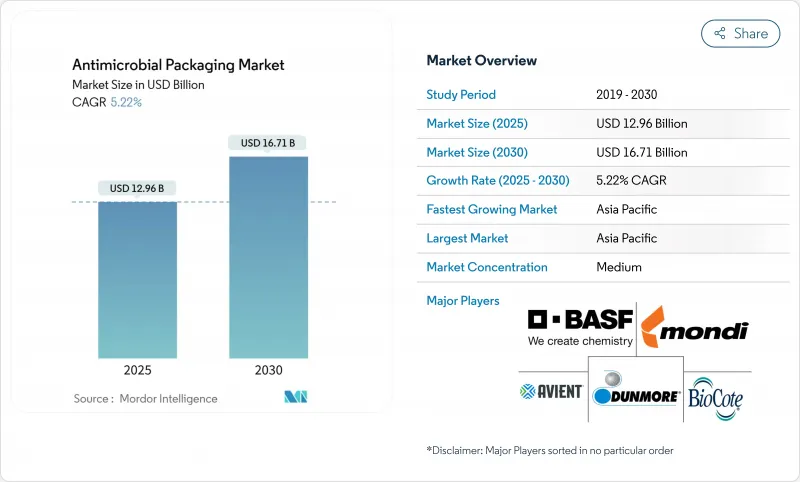

根据目前的数据,抗菌包装市场预计在2025年价值为129.6亿美元,到2030年将达到167.1亿美元,复合年增长率为5.22%。

更严格的食品接触法规、PFAS物质的逐步淘汰以及企业永续性将抗菌功能提升到主流包装要求,这些因素推动了需求成长。监管势头促使人们转向生物基抗菌剂,以平衡微生物功效与环保要求。在不断完善的卫生法规、蓬勃发展的电子杂货行业以及快速升级的低温运输的推动下,亚太地区继续成为成长的支点。控制释放奈米银薄膜、天然化合物的整合以及与智慧感测器的组合等平行技术进步正在改变竞争创新的重点。因此,抗菌包装市场在材料、技术和最终用途领域持续呈现多元化发展。

全球抗菌包装市场趋势与洞察

后疫情时代食品安全监理趋严

全球食品接触监测的重启正在推动抗菌解决方案的推广。美国人类食品计划署目前正在重新评估其遗留的PFAS通知,并探索更安全的替代抗菌剂。欧洲机构也同时发布了关于李斯特菌等持久性病原体的警告,鼓励加工者采用增加微生物屏障的包装。这些规定正在刺激对符合安全性和「洁净标示」要求的天然抗菌剂的投资。对于能够证明其功效和可回收性的供应商来说,加强监管将为抗菌包装市场带来明显的成长潜力。

加速对电子杂货低温运输的投资

线上食品杂货需求的激增给温控物流带来了前所未有的压力。亚太地区数千个微型仓配仓库需要能够在漫长的最后一哩运输过程中保持品质的包装。当冷藏性能下降时,抗菌层可作为关键的二次保障,减少腐败索赔。新型智慧包装融合了时间-温度指示器和抗菌剂,使平台能够根据数据管理新鲜度。随着当日送达时限的缩短,零售商越来越多地将抗菌功能作为采购的先决条件,尤其是对于高风险生鲜食品。这种电子商务动能正在巩固抗菌包装市场的短期成长。

欧盟除生物剂法规(BPR)对奈米金属构成障碍

欧洲除生物剂产品法规要求,奈米银和奈米铜进入食品接触管道前必须提供大量文件。目前尚无任何奈米金属获准直接用于食品或饲料,这使得创新者面临多年的毒理学研究计画。大量的数据要求延长了产品上市时间,促使一些公司转向能够更快通过监管批准的植物来源活性成分。这种阻碍因素正在限制抗菌包装市场金属解决方案的短期成长。

細項分析

目前,塑胶在抗菌包装市场占据主导地位,得益于可扩展的挤出生产线和强大的阻隔性能,到2024年将占据60.32%的收入份额。然而,受2030年强制全面回收的政策目标推动,生物聚合物的复合年增长率将达到8.32%,成为所有材料中最快的。聚乳酸和聚羟基烷酯的混合物,透过几丁聚醣或精油增强,其微生物杀灭率现已与石化薄膜相当,同时支持可堆肥的报废处理方式。

封闭式收集方案的投资正在加速,旨在回收生物聚合物边角料,同时不牺牲抗菌活性。研究还表明,涂有富含酚的多醣的纸纤维保持了可回收性,并具有广谱抗菌活性。这种先进的包装将使生物聚合物继续蚕食塑胶的市场份额,并重塑抗菌包装市场的供应商组合。

由于监管合规性和成本效益,有机酸将在2024年占销售额的45.63%。然而,细菌素和酵素的复合年增长率将达到7.53%,这反映出人们正转向消费者可识别且标籤友好的添加剂。细菌素与奈米银的协同体係可使消毒剂功效加倍,同时减少金属用量。

环糊精键结保护的精油可透过控制蒸气释放来抑制潮湿农产品中的腐败菌。随着除生物剂受到越来越严格的审查,植物来源的杀菌剂正日益受到策略重视,天然活性剂已成为未来抗菌包装市场差异化的关键。

抗菌包装市场按材料(塑胶、生物聚合物等)、抗菌剂类型(有机酸、细菌素和酵素等)、技术(活性表面涂层等)、包装类型(袋和包、薄膜和包装纸等)、终端用户行业(食品饮料、医疗保健和医疗设备等)和地区细分。市场预测以美元计算。

区域分析

2024年,亚太地区将以41.22%的营收引领全球市场,至2030年,复合年增长率最高,达8.96%。中国修订的《食品安全法》和印度食品安全监督管理局(FSSAI)的卫生法规均要求采取微生物安全措施,这推动资本转向先进包装。日本加工商正在为高端水产品出口添加智慧指示器和控制释放抗菌剂,以提高单位利润率。地方政府为因应抗菌素抗药性所倡议将进一步影响亚太地区抗菌包装市场。

欧盟包装废弃物法规强制要求遵守可回收性和再生成分标准,欧洲正在塑造其发展轨迹。德国和法国在生物基界面活性剂的研发方面处于领先地位,地中海出口商正在引入抗菌纸盒,以确保农产品跨境运输时的保质期。虽然生物基废弃物法规减缓了奈米金属的推广,但它加速了植物来源创新,使欧洲处于技术领导的中心。

在FDA监管和强劲的医疗保健需求的支持下,北美市场保持稳定成长。美国正在向PFAS替代品提供津贴,间接扩大了天然界面活性剂抗菌包装的市场规模。一家加拿大研究机构正在试验注入酵素混合物的纤维素基薄膜,目标是水产品供应链。墨西哥正利用近岸外包趋势,扩大为国内品牌和美国零售商生产的抗菌包装袋。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 后疫情时代食品安全监理趋严

- 加速对电子杂货低温运输的投资

- 控制释放奈米银薄膜的突破

- 将抗菌功能纳入 ESG 记分卡

- 医院开始使用可重复使用的医疗设备托盘

- 生鲜食品出口采用可食用抗菌涂层

- 市场限制

- 欧盟除生物剂法规(BPR)对奈米金属的阻碍

- 银和铜原料价格波动

- 消费者对合成包装防腐剂的强烈反对

- 生物基抗菌聚合物的扩大挑战

- 供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模及成长预测

- 按材质

- 塑胶

- 生物聚合物

- 纸和纸板

- 玻璃

- 金属

- 按抗菌剂类型

- 有机酸

- 细菌素和酶

- 银和铜奈米颗粒

- 精油和植物萃取物

- 依技术

- 活性表面涂层

- 控制释放系统

- 按包装类型

- 袋子和包包

- 薄膜和包装

- 托盘和盖子

- 纸箱包装

- 按最终用户产业

- 饮食

- 肉类、家禽、鱼贝类

- 烘焙和糖果甜点

- 水果和蔬菜

- 医疗保健和医疗设备

- 个人护理和化妆品

- 饲料和宠物食品

- 其他最终用户产业

- 饮食

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议和发展

- 市占率分析

- 公司简介

- Amcor Plc

- Mondi Group

- Sealed Air Corporation

- BASF SE

- Avient Corporation

- BioCote Limited

- Sciessent LLC

- Microban International

- Covestro AG

- Takex Labo Co., Ltd.

- Dunmore Corporation

- Sonoco Products Company

- Constantia Flexibles

- Toppan Printing Co., Ltd.

- Toyochem Co., Ltd.

- Nissen Chemitec Corporation

- Parx Materials NV

- Tekni-Plex Inc.

- Plastipak Holdings Inc.

第七章 市场机会与未来展望

Current data indicate the antimicrobial packaging market is valued at USD 12.96 billion in 2025 and is forecast to reach USD 16.71 billion by 2030, expanding at a 5.22% CAGR.

Demand is propelled by stricter food-contact regulations, the phase-out of PFAS substances, and corporate sustainability mandates that elevate antimicrobial functionality to a mainstream packaging requirement. Regulatory momentum has sparked a pivot toward bio-based antimicrobial agents that balance microbial efficacy with environmental credentials. Asia-Pacific remains the fulcrum of growth, driven by evolving sanitation laws, a booming e-grocery sector, and rapid cold-chain upgrades. Parallel advances in controlled-release nano-silver films, natural compound integration, and smart-sensor pairing are reshaping competitive innovation priorities. As a result, the antimicrobial packaging market continues to diversify across materials, technologies, and end-use sectors.

Global Antimicrobial Packaging Market Trends and Insights

Stringent Post-COVID Food-Safety Regulations

The global reset of food-contact oversight is amplifying uptake of antimicrobial solutions. The United States Human Foods Program now reassesses legacy PFAS notifications, creating an opening for safer antimicrobial alternatives. European agencies simultaneously flag persistent pathogens such as Listeria monocytogenes, compelling processors to adopt packaging that adds an extra microbial barrier. These converging mandates accelerate investment in naturally-derived agents that fulfil both safety and "clean-label" expectations. For suppliers able to document efficacy and recyclability, regulatory tightening translates into clear growth runway within the antimicrobial packaging market.

Acceleration of E-Grocery Cold-Chain Investments

Explosive demand for online groceries places unprecedented stress on temperature-controlled logistics. In Asia-Pacific, thousands of micro-fulfilment warehouses now require packaging that maintains quality over extended last-mile journeys. When refrigeration falters, antimicrobial layers serve as a critical secondary safeguard, reducing spoilage claims. Emerging smart packs pair time-temperature indicators with embedded antimicrobials, giving platforms data-driven control over freshness. As same-day delivery windows shrink, retailers increasingly make antimicrobial functionality a procurement prerequisite, particularly for high-risk perishables. This e-commerce momentum solidifies near-term gains for the antimicrobial packaging market.

EU Biocide Regulation (BPR) Hurdles for Nano-Metals

Europe's Biocidal Products Regulation requires exhaustive dossiers before nano-silver or nano-copper can enter food-contact channels. With no nano-metal yet authorised for direct food or feed applications, innovators face multi-year toxicology programs. Wide-ranging data demands inflate time-to-market, prompting some firms to pivot toward plant-based actives that clear regulatory pathways more swiftly. The deterrent effect narrows near-term growth for metallic solutions inside the antimicrobial packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in Controlled-Release Nano-Silver Films

- Inclusion of Antimicrobial Features in ESG Scorecards

- Price Volatility in Silver and Copper Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics currently anchor the antimicrobial packaging market size, capturing 60.32% revenue share in 2024 due to scalable extrusion lines and robust barrier performance. Yet policy targets that mandate full recyclability by 2030 propel biopolymers to an 8.32% CAGR, the fastest among materials. Poly-lactic acid and polyhydroxyalkanoate blends enhanced with chitosan or essential oils now match microbial kill rates seen in petrochemical films while supporting compostable end-of-life routes.

Investment is accelerating in closed-loop collection schemes that recover biopolymer offcuts without sacrificing antimicrobial potency. Research also evidences that paper fibres coated with phenolic-rich polysaccharides retain recyclability and deliver broad-spectrum bacterial inhibition. These advances ensure biopolymers will continue eroding plastic share, reshaping supplier portfolios throughout the antimicrobial packaging market.

Organic acids command 45.63% of 2024 revenue owing to regulatory familiarity and cost efficiency. However, bacteriocins and enzymes accelerate at 7.53% CAGR, mirroring consumer migration to recognizable, label-friendly additives. Synergistic systems marry bacteriocins with nano-silver, doubling kill efficiency while curbing metal dosage.

Essential oils protected within cyclodextrin cages provide controlled vapor release that suppresses spoilage organisms in high-moisture produce. As biocide scrutiny intensifies, plant-derived agents gain strategic heft, positioning natural actives as pivotal to future differentiation in the antimicrobial packaging market.

Antimicrobial Packaging Market is Segmented by Material (Plastics, Biopolymers, and More), Antimicrobial Agent Type (Organic Acids, Bacteriocins and Enzymes, and More), Technology (Active Surface Coating, and More), Pack Type (Pouches and Bags, Films and Wraps, and More), End-User Industry (Food and Beverages, Healthcare and Medical Devices, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific tops the global leaderboard, holding 41.22% revenue in 2024 and registering the highest 8.96% CAGR to 2030. China's Food Safety Law amendments and India's FSSAI hygiene codes mandate microbiological safeguards that funnel capital toward advanced packs. Japanese converters add smart indicators and controlled-release antimicrobials to premium seafood exports, elevating unit margins. Regional government initiatives to counter antimicrobial resistance further incentivise adoption, reinforcing Asia-Pacific's pull on the antimicrobial packaging market.

Europe follows, its trajectory shaped by the EU Packaging and Packaging Waste Regulation that forces recyclability and recycled-content compliance. Germany and France spearhead R&D into bio-based actives, whereas Mediterranean exporters deploy antimicrobial cartons to secure shelf life during cross-border produce shipments. While the BPR slows nano-metal roll-outs, it simultaneously accelerates botanical innovation, keeping Europe central to technology leadership.

North America sustains steady gains anchored by FDA oversight and robust healthcare demand. The United States channels grant funding toward PFAS alternatives, indirectly uplifting antimicrobial packaging market size for natural actives. Canadian institutes pilot cellulose-based films infused with enzyme cocktails, targeting seafood supply chains. Mexico, leveraging near-shoring trends, scales antimicrobial pouch production for both domestic brands and US retailers.

- Amcor Plc

- Mondi Group

- Sealed Air Corporation

- BASF SE

- Avient Corporation

- BioCote Limited

- Sciessent LLC

- Microban International

- Covestro AG

- Takex Labo Co., Ltd.

- Dunmore Corporation

- Sonoco Products Company

- Constantia Flexibles

- Toppan Printing Co., Ltd.

- Toyochem Co., Ltd.

- Nissen Chemitec Corporation

- Parx Materials N.V.

- Tekni-Plex Inc.

- Plastipak Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent post-COVID food-safety regulations

- 4.2.2 Acceleration of e-grocery cold-chain investments

- 4.2.3 Breakthroughs in controlled-release nano-silver films

- 4.2.4 Inclusion of antimicrobial features in ESG scorecards

- 4.2.5 Shift to reusable medical-device trays in hospitals

- 4.2.6 Adoption of edible, antimicrobial coatings for fresh-produce export

- 4.3 Market Restraints

- 4.3.1 EU biocide regulation (BPR) hurdles for nano-metals

- 4.3.2 Price volatility in silver and copper feedstocks

- 4.3.3 Consumer push-back on synthetic preservatives in packaging

- 4.3.4 Scale-up challenges for bio-based antimicrobial polymers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Biopolymers

- 5.1.3 Paper and Paperboard

- 5.1.4 Glass

- 5.1.5 Metals

- 5.2 By Antimicrobial Agent Type

- 5.2.1 Organic Acids

- 5.2.2 Bacteriocins and Enzymes

- 5.2.3 Silver and Copper Nanoparticles

- 5.2.4 Essential Oils and Plant Extracts

- 5.3 By Technology

- 5.3.1 Active Surface Coating

- 5.3.2 Controlled-Release Systems

- 5.4 By Pack Type

- 5.4.1 Pouches and Bags

- 5.4.2 Films and Wraps

- 5.4.3 Trays and Lids

- 5.4.4 Carton Packages

- 5.5 By End-user Industry

- 5.5.1 Food and Beverages

- 5.5.1.1 Meat, Poultry and Seafood

- 5.5.1.2 Bakery and Confectionery

- 5.5.1.3 Fruits and Vegetables

- 5.5.2 Healthcare and Medical Devices

- 5.5.3 Personal Care and Cosmetics

- 5.5.4 Animal Feed and Pet Food

- 5.5.5 Other End-User Industry

- 5.5.1 Food and Beverages

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor Plc

- 6.4.2 Mondi Group

- 6.4.3 Sealed Air Corporation

- 6.4.4 BASF SE

- 6.4.5 Avient Corporation

- 6.4.6 BioCote Limited

- 6.4.7 Sciessent LLC

- 6.4.8 Microban International

- 6.4.9 Covestro AG

- 6.4.10 Takex Labo Co., Ltd.

- 6.4.11 Dunmore Corporation

- 6.4.12 Sonoco Products Company

- 6.4.13 Constantia Flexibles

- 6.4.14 Toppan Printing Co., Ltd.

- 6.4.15 Toyochem Co., Ltd.

- 6.4.16 Nissen Chemitec Corporation

- 6.4.17 Parx Materials N.V.

- 6.4.18 Tekni-Plex Inc.

- 6.4.19 Plastipak Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

抗菌表面涂层市场分析及预测(至2035年):依类型、产品类型、应用、技术、材料类型、最终用户、形态、安装类型及製程划分

抗菌表面涂层市场分析及预测(至2035年):依类型、产品类型、应用、技术、材料类型、最终用户、形态、安装类型及製程划分 全球抗菌包装市场:市场规模、份额、成长和行业分析:按抗菌成分、产品类型、最终用途和区域预测(至2034年)

全球抗菌包装市场:市场规模、份额、成长和行业分析:按抗菌成分、产品类型、最终用途和区域预测(至2034年) 全球抗菌包装市场规模、份额、趋势和成长分析报告:2026-2034年

全球抗菌包装市场规模、份额、趋势和成长分析报告:2026-2034年 抗菌包装市场-全球产业规模、份额、趋势、机会、预测:按材料、类型、应用、地区和竞争格局划分,2021-2031年灭菌包装市场 - 2026-2031年预测

抗菌包装市场-全球产业规模、份额、趋势、机会、预测:按材料、类型、应用、地区和竞争格局划分,2021-2031年灭菌包装市场 - 2026-2031年预测 全球抗菌包装市场:预测(至2032年)-按材料、抗菌剂、包装类型、分销管道、最终用户和地区进行分析

全球抗菌包装市场:预测(至2032年)-按材料、抗菌剂、包装类型、分销管道、最终用户和地区进行分析 抗菌包装市场规模、份额及成长分析(按类型、材料、抗菌剂类型及地区划分)-2026-2033年产业预测2032 年抗菌表面市场预测:按材料类型、涂层形式、分销管道、最终用户和地区进行的全球分析全球抗菌表面涂层市场:预测至2032年-按产品类型、活性材料、应用方法、最终用户和地区分類的分析

抗菌包装市场规模、份额及成长分析(按类型、材料、抗菌剂类型及地区划分)-2026-2033年产业预测2032 年抗菌表面市场预测:按材料类型、涂层形式、分销管道、最终用户和地区进行的全球分析全球抗菌表面涂层市场:预测至2032年-按产品类型、活性材料、应用方法、最终用户和地区分類的分析 按应用、产品类型、包装材料、灭菌製程和最终用户分類的灭菌包装市场 - 全球预测 2025-2032

按应用、产品类型、包装材料、灭菌製程和最终用户分類的灭菌包装市场 - 全球预测 2025-2032