|

市场调查报告书

商品编码

1849842

扩增实境:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Augmented Reality - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

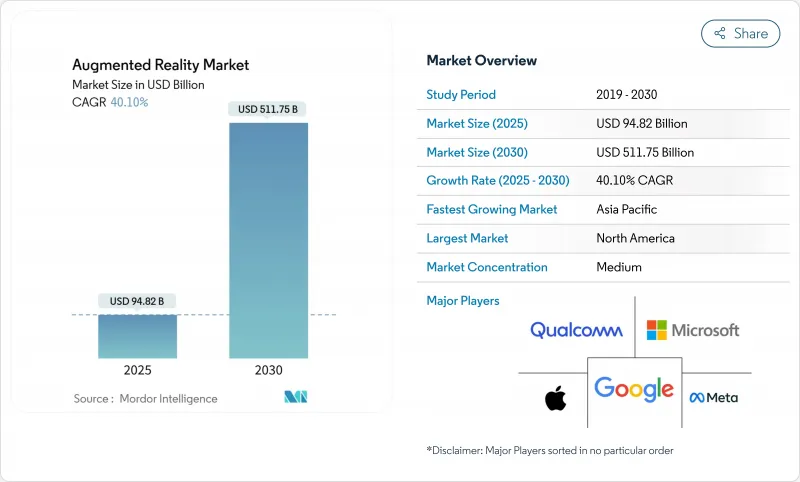

扩增实境市场规模预计将在 2025 年达到 948.2 亿美元,到 2030 年将增至 5,117.5 亿美元,复合年增长率为 40.1%。

随着 5G 网路消除延迟障碍、自主 AI 政策推动装置端推理,以及 Apple Vision Pro检验空间运算用例,需求将加速成长。製造业、医疗保健业和能源业的公司正在标准化数位双胞胎迭加,以缩短决策週期,而生成式 AI 工具则将内容开发时间从数月缩短至数天。波导和 MicroLED 领域的硬体创新仍在持续,以云端为中心的软体平台发展更为迅速,使企业无需繁重的基础设施即可将试点计画扩展到全球工厂。随着企业将敏感资料从消费级智慧型手机迁移到託管的工业终端,安全增强的 AR 堆迭和边缘优化的渲染正成为预设需求。

全球扩增实境市场趋势与洞察

相容5G的低延迟行动网络

独立 5G 可实现低于 20 毫秒的往返时间,从而实现共用全像图的即时位置更新。爱立信报告称,当设备透过边缘运算切片连接时,AR 会话持续时间更长,因为边缘运算切片优先处理空间资料流量。采用私人 5G 的製造工厂(例如捷克共和国的核能发电厂)在引导式检查期间的效率和安全性均有所提高。通讯业者将扩增实境市场视为一种高端附加提升销售,以抵消语音收入的下滑,鼓励开发人员投资于能够提供不同服务品质等级的网路 API。 6G 已准备就绪,目标是实现Terabit吞吐量,这将使轻量级眼镜能够无需网络共享即可传输大容量视频,从而增强了两位数增长的预测。

智慧型手机普及率和 AR 应用不断提升

2024年,亚太地区将新增1.3亿行动用户,普及率将达51%,为AR商务创造丰富的装置量。 IKEA和欧莱雅的零售试点计画表明,顾客能够以真人大小的视觉比例观看产品,从而将停留时间延长至10分钟以上。智慧型手机的光学系统在室内导航方面仍有问题,大阪大学也观察到了由漂移引起的晕动症。即便如此,智慧型手机仍然是许多首次使用AR用户的入门平台,在大众市场眼镜上市之前,它已经培育了一个开发者生态系统。

头戴式显示器的电池寿命和人体工学

目前的设备重量接近100克,续航时间很少超过两小时。苹果的Vision Pro凸显了microOLED的高亮度会快速耗尽电池的弊端。东京大学的研究人员提案了一种外置「光束显示器」的方案,以将电力消耗转移给头戴装置。 HoloLens 2的能耗分析表明,显示器亮度占功耗的62%,而软体调光和场景感知渲染可以将使用时间延长多达五分之一。虽然工业用户在执行有限任务时可以接受更重的设备,但大众消费者的普及将取决于真正的全天候穿戴式装置。

細項分析

到2024年,硬体将占扩增扩增实境市场收入的67.5%。组件供应商正在提升波导管效率和MicroLED亮度,延长电池寿命并实现户外使用。三星的LEDoS蓝图目标是到2027年实现量产,并承诺推出适用于企业级和生活级眼镜的纤薄光学元件。虽然硬体仍然至关重要,但云端优先平台使企业能够在现有行动装置上试行扩增现实,从而降低小型工厂和诊所的门槛。因此,预计软体的复合年增长率将达到42.0%,到2030年缩小收益差距。允许第三方原始设备製造商预先安装成熟作业系统的授权策略,可以效仿PC生态系统,加速应用程式跨装置的可移植性。

云端编配工具整合了生成式AI模组,可自动将CAD元件转换为有序的全像指令,从而将部署时间缩短三分之二。订阅定价将投资从资本支出转移到营运预算,这与企业数位化的要求一致。设备成本的下降和平台复杂性的提升,共同支撑着扩增实境市场的持续扩张。

到2024年,波导管和衍射光学元件将占市场收益的51.3%。肖特公司新建的克利姆工厂将提升玻璃毛坯产能,但MicroLED创新正在蚕食现有的市场份额。 Mojo Vision的单晶片RGB阵列效能优于传统显示器,像素密度达到6,350 PPI,同时功耗减半。富士康与Polotek合作,将于2025年开始晶圆加工,显示供应链正在为量产做准备。随着产量比率的提高,MicroLED模组将从开发套件转向消费级眼镜产品,从而改变成本结构并提高户外可视度。

製造商正在将 MicroLED 面板与薄饼透镜和多层涂层相结合,以增强对比度。对于廉价头戴式设备而言,液晶硅)仍然是一个可行的选择,尤其是在培训亭中,因为紧凑性比日间可视性更重要。在预测期内,MicroLED 的快速效率提升预计将首先改变高端用例,然后蔓延至中端产品,从而重塑整个扩增实境市场的技术蓝图。

区域分析

北美将主导扩增实境市场,到2024年将占总收入的38.6%。国防和公共机构的政府合约将为坚固耐用的头显提供稳定的需求,而可预测的FDA核准途径将加速临床部署。创投集中在硅谷和西雅图,为平台型新兴企业随后将在墨西哥和加拿大拓展製造伙伴关係关係,从而增强区域生态系统。

亚太地区的复合年增长率最高,达40.8%,其中中国投入3.33兆元人民币的研发资金,用于津贴零件代工厂和软体研究实验室。日本的富岳超级电脑正在支援即时空间映射的演算法训练,这将使国内光学供应商受益。韩国的「元宇宙蓝图」计画获得了55亿韩元的激励,旨在2026年培育220家身临其境型科技公司。该地区的行动经济将为GDP贡献8,800亿美元,确保庞大的面向消费者的市场,并促进扩增实境市场硬体的规模化发展。

欧洲保持平衡的发展轨迹。德国正在利用扩增实境技术优化其汽车和机械组装,实现了两位数的品质提升。欧盟要求遵守《一般资料保护规范》(GDPR),这迫使供应商采用保护隐私的设计实践,这些实践日后将成为全球规范。法国和荷兰的智慧城市基金正在资助公共交通的扩增实境导航试点项目,使其为市民所熟悉。儘管亚太地区的成长滞后,但欧洲製造业的严谨性支撑了扩增实境市场的很大一部分,并正在塑造全球采用的安全标准。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 相容5G的低延迟行动网络

- 智慧型手机普及率和 AR 应用不断提升

- 提高企业培训和现场服务的效率

- 用于快速创建 AR 内容的生成式 AI 工具

- 用于即时物联网资料的工业数位双胞胎迭加

- 推动Apple Vision-Pro主导的空间运算生态系统

- 市场限制

- 头戴式显示器的电池寿命和人体工学

- 隐私和资料安全问题

- 光波导玻璃供应瓶颈

- 开发人员标准分散和跨平台问题

- 价值链分析

- 监管格局

- 技术展望

- 云端运算

- 人工智慧

- 网路安全

- 数位服务

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

- 评估宏观经济趋势对市场的影响

第五章市场规模及成长预测

- 按报价

- 硬体

- 独立式 HMD

- 系留式 HMD

- 无萤幕检视器

- 软体

- 硬体

- 核心技术

- OLED/微型OLED

- 微型 LED

- 波导管与衍射光学

- 液晶硅(LCOS)

- 按用途

- 远端援助与维护

- 产品视觉化和配置

- 导航和地图绘製

- 社交和沟通过滤器

- 其他用途

- 按最终用户

- 游戏和娱乐

- 教育

- 卫生保健

- 零售

- 汽车和运输

- 其他最终用户领域

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Microsoft Corporation

- Google LLC(Alphabet)

- Meta Platforms Inc.

- Apple Inc.

- Snap Inc.

- Niantic Inc.

- PTC Inc.

- Vuzix Corporation

- Magic Leap Inc.

- Seiko Epson Corporation

- RealWear Inc.

- Lenovo Group Ltd.

- Fujitsu Ltd.

- Kopin Corporation

- Qualcomm Technologies Inc.

- Unity Technologies

- Dynabook Europe GmbH

- Optinvent SA

- Immersion Corporation

第七章 市场机会与未来展望

The Augmented Reality market size reached USD 94.82 billion in 2025 and is projected to climb to USD 511.75 billion by 2030, reflecting a 40.1% CAGR.

Demand accelerates as 5G networks remove latency barriers, sovereign AI policies push on-device inference, and Apple's Vision Pro validates spatial-computing use cases. Enterprises in manufacturing, healthcare, and energy are standardizing digital-twin overlays to shorten decision cycles, while generative-AI tools shrink content-development time from months to days. Hardware innovation in waveguides and MicroLEDs continues, yet cloud-centric software platforms are growing even faster, enabling organizations to scale pilots across global plants without heavy infrastructure. Security-hardened AR stacks and edge-optimized rendering are becoming default requirements as companies move sensitive data off consumer smartphones and into managed industrial endpoints.

Global Augmented Reality Market Trends and Insights

5G-enabled Low-latency Mobile Networks

Sub-20 millisecond round-trip times now achievable on standalone 5G allow real-time positional updates for shared holograms. Ericsson reports higher AR session durations when devices connect through edge-computing slices that prioritize spatial data traffic. Manufacturing sites adopting private 5G-such as nuclear plants in the Czech Republic-have documented efficiency lifts and safety gains during guided inspections. Operators view the Augmented Reality market as a premium upsell that offsets shrinking voice revenues, prompting investment in network APIs that expose quality-of-service tiers to developers. Preparations for 6G, targeting terabit throughput, will enable lightweight glasses to stream volumetric video without tethering, reinforcing double-digit growth forecasts.

Rising Smartphone Penetration and AR-ready Apps

Asia-Pacific added 130 million mobile subscribers in 2024, bringing penetration to 51% and creating a fertile install base for AR commerce. Retail pilots from IKEA and L'Oreal show dwell-time gains exceeding 10 minutes when customers visualize products in real scale. Smartphone optics still struggle in indoor navigation, where Osaka University observed drift-induced motion sickness; research points to ultra-wideband anchors as a remedy. Nevertheless, the handset remains the on-ramp for many first-time AR users, nurturing developer ecosystems ahead of mass-market glasses.

Battery-life and Ergonomics of Head-mounted Displays

Current devices weigh near 100 grams and seldom exceed two hours of operation. Apple's Vision Pro highlights the trade-off: high micro-OLED brightness drains batteries quickly. University of Tokyo researchers propose off-board "beaming displays" to shift power draw away from the headset. Energy profiling of HoloLens 2 shows display brightness accounts for 62% of consumption, implying software dimming and scene-aware rendering can stretch sessions by one-fifth. Industrial users accept heavier gear for limited tasks, yet mass-consumer uptake hinges on true all-day wearables.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Training and Field-service Efficiency Gains

- Generative-AI Tools for Rapid AR Content Creation

- Privacy and Data-security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 67.5% of Augmented Reality market revenue in 2024 on the strength of stand-alone and tethered head-mounted displays. Component vendors push waveguide efficiency and MicroLED brightness to extend battery life and enable outdoor use. Samsung's LEDoS roadmap targets mass production before 2027, promising slimmer optics that suit both enterprise and lifestyle glasses. While hardware remains indispensable, cloud-first platforms now let firms pilot AR with existing mobile devices, lowering barriers for smaller factories and clinics. As a result, software is set to post a 42.0% CAGR and will narrow the revenue gap by 2030. Licensing strategies that let third-party OEMs preload mature operating systems mirror the PC ecosystem and accelerate application portability across devices.

Cloud orchestration tools embed generative-AI modules that auto-convert CAD assemblies into sequenced holographic instructions, trimming deployment time by two-thirds. Subscription pricing shifts investment from capital expenditure to operating budgets, aligning with enterprise digitization mandates. This blend of falling device costs and rising platform sophistication underpins sustained expansion across the Augmented Reality market.

Waveguide and diffractive optics controlled 51.3% market revenue in 2024, reflecting incumbent manufacturing depth. SCHOTT's new Kulim facility lifts glass-blank capacity, yet MicroLED innovations are eroding incumbent share. Mojo Vision's monolithic RGB array delivered 6,350 PPI while halving power draw, marking a leap over traditional displays. Foxconn's partnership with Porotech to start wafer processing in 2025 signals that supply chains are preparing for volume. As yields improve, MicroLED modules will move from developer kits into consumer eyewear, shifting cost structures and brightening outdoor legibility.

Manufacturers pair MicroLED panels with pancake lenses and multilayer coatings to enhance contrast. Liquid-Crystal-on-Silicon remains relevant for budget headsets, especially in training kiosks where compactness trumps daylight visibility. Over the forecast window, MicroLED's rapid efficiency gains are expected to convert high-performance use cases first, then cascade into mid-tier products, reshaping technical roadmaps across the Augmented Reality market.

The Augmented Reality Market Report is Segmented by Offering (Hardware and Software), Core Technology (OLED / Micro-OLED, Microled, Waveguide and Diffractive Optics, and More), Application (Remote Assistance and Maintenance, Product Visualisation and Configuration, and More), End-User Vertical (Gaming and Entertainment, Education, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated with 38.6% Augmented Reality market revenue in 2024 owing to deep enterprise adoption and robust 5G coverage. Government contracts from defense and public-safety agencies provide steady demand for ruggedized headsets, while the FDA's predictable approval pathway accelerates medical deployments. Venture investment concentrates in Silicon Valley and Seattle, funding platform startups that later expand manufacturing partnerships in Mexico and Canada, reinforcing the regional ecosystem.

Asia-Pacific posted the highest 40.8% CAGR outlook, fueled by China's 3.33 trillion-yuan R&D pool that subsidizes component foundries and software labs. Japan's Fugaku supercomputer supports algorithm training for real-time spatial mapping, benefitting domestic optical suppliers. South Korea's metaverse blueprint aims to nurture 220 immersive-tech firms by 2026, backed by 5.5 billion won in incentives. The region's mobile economy, adding USD 880 billion in GDP impact, ensures massive consumer addressable markets, smoothing hardware scale-up across the Augmented Reality market.

Europe maintains a balanced trajectory. Germany leverages AR to optimize automotive and machinery assembly lines, achieving double-digit quality gains. The EU's GDPR compliance pressure forces vendors to embed privacy-preserving designs that later become global norms. Smart-city funds in France and the Netherlands finance AR navigation pilots for public transportation, expanding citizen familiarity. Though growth lags Asia-Pacific, European manufacturing rigor sustains a sizable slice of the Augmented Reality market and shapes safety standards adopted worldwide.

- Microsoft Corporation

- Google LLC (Alphabet)

- Meta Platforms Inc.

- Apple Inc.

- Snap Inc.

- Niantic Inc.

- PTC Inc.

- Vuzix Corporation

- Magic Leap Inc.

- Seiko Epson Corporation

- RealWear Inc.

- Lenovo Group Ltd.

- Fujitsu Ltd.

- Kopin Corporation

- Qualcomm Technologies Inc.

- Unity Technologies

- Dynabook Europe GmbH

- Optinvent SA

- Immersion Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G-enabled low-latency mobile networks

- 4.2.2 Rising smartphone penetration and AR-ready apps

- 4.2.3 Enterprise training and field-service efficiency gains

- 4.2.4 Generative-AI tools for rapid AR content creation

- 4.2.5 Industrial digital-twin overlays for real-time IoT data

- 4.2.6 Apple Vision-Pro-led spatial-computing ecosystem push

- 4.3 Market Restraints

- 4.3.1 Battery-life and ergonomics of head-mounted displays

- 4.3.2 Privacy and data-security concerns

- 4.3.3 Optical-waveguide glass supply bottlenecks

- 4.3.4 Fragmented developer standards and cross-platform issues

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Cloud Computing

- 4.6.2 Artificial Intelligence

- 4.6.3 Cyber-Security

- 4.6.4 Digital Services

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 Stand-alone HMDs

- 5.1.1.2 Tethered HMDs

- 5.1.1.3 Screenless Viewers

- 5.1.2 Software

- 5.1.1 Hardware

- 5.2 By Core Technology

- 5.2.1 OLED / Micro-OLED

- 5.2.2 MicroLED

- 5.2.3 Waveguide and Diffractive Optics

- 5.2.4 Liquid-Crystal-on-Silicon (LCOS)

- 5.3 By Application

- 5.3.1 Remote Assistance and Maintenance

- 5.3.2 Product Visualisation and Configuration

- 5.3.3 Navigation and Mapping

- 5.3.4 Social and Communication Filters

- 5.3.5 Other Applications

- 5.4 By End-user Vertical

- 5.4.1 Gaming and Entertainment

- 5.4.2 Education

- 5.4.3 Healthcare

- 5.4.4 Retail

- 5.4.5 Automotive and Transportation

- 5.4.6 Other End-User Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC (Alphabet)

- 6.4.3 Meta Platforms Inc.

- 6.4.4 Apple Inc.

- 6.4.5 Snap Inc.

- 6.4.6 Niantic Inc.

- 6.4.7 PTC Inc.

- 6.4.8 Vuzix Corporation

- 6.4.9 Magic Leap Inc.

- 6.4.10 Seiko Epson Corporation

- 6.4.11 RealWear Inc.

- 6.4.12 Lenovo Group Ltd.

- 6.4.13 Fujitsu Ltd.

- 6.4.14 Kopin Corporation

- 6.4.15 Qualcomm Technologies Inc.

- 6.4.16 Unity Technologies

- 6.4.17 Dynabook Europe GmbH

- 6.4.18 Optinvent SA

- 6.4.19 Immersion Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球空间运算软体开发工具包(SDK)市场报告

2026年全球空间运算软体开发工具包(SDK)市场报告 供应链市场中的扩增实境(AR)技术:按组件、应用和最终用户划分-2026年至2032年全球市场预测扩增实境(AR)市场:按组件、技术、互动方式、最终用途和应用划分-2026-2032年全球市场预测数位学习中的扩增实境(AR)市场:组件、技术、应用、部署模式与最终用途-2026-2032年全球市场预测2026年全球广告人工智慧市场报告航空领域扩增实境(AR)和虚拟实境(VR)市场:按技术、交付方式、部署方式、应用和最终用途划分-2026年至2032年全球市场预测2026年全球扩增实境(AR)射箭训练器市场报告2026年扩增实境全球市场报告

供应链市场中的扩增实境(AR)技术:按组件、应用和最终用户划分-2026年至2032年全球市场预测扩增实境(AR)市场:按组件、技术、互动方式、最终用途和应用划分-2026-2032年全球市场预测数位学习中的扩增实境(AR)市场:组件、技术、应用、部署模式与最终用途-2026-2032年全球市场预测2026年全球广告人工智慧市场报告航空领域扩增实境(AR)和虚拟实境(VR)市场:按技术、交付方式、部署方式、应用和最终用途划分-2026年至2032年全球市场预测2026年全球扩增实境(AR)射箭训练器市场报告2026年扩增实境全球市场报告 扩增实境(AR)市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、设备、部署和最终用户划分2026年全球空间计算市场报告

扩增实境(AR)市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、设备、部署和最终用户划分2026年全球空间计算市场报告