|

市场调查报告书

商品编码

1849879

亚太地区绿色资料中心:市场占有率分析、产业趋势、统计资料和成长预测(2025-2030 年)APAC Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

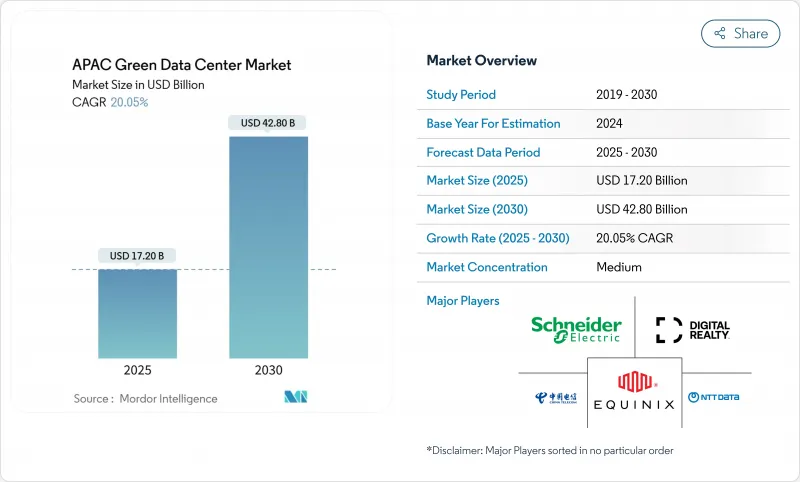

亚太地区绿色资料中心市场目前在 2025 年的价值为 172 亿美元,预计到 2030 年将达到 428 亿美元,年复合成长率为 20.05%。

超大规模配置的兴起、严格的净零排放政策以及云端运算的快速普及,正推动资本流向中国、印度、日本和东南亚等地的节能设施。液冷和混合冷却平台、企业购电协议的扩展以及绿色金融带来的加权平均资本成本下降,都在推动计划建设。企业也重新配置其电力架构以适应100kW以上的机架,政府则鼓励企业在可再生能源丰富的二线城市位置。託管服务商、云端超大规模资料中心业者和基础设施房地产投资信託基金正在竞相争夺稀缺的土地、电网存取和熟练劳动力。

亚太地区绿色资料中心市场趋势与洞察

高密度人工智慧主导的工作负载需要液冷和混合冷却

GPU密集型伺服器的机架密度正从10kW飙升至100kW以上,推动直接式、浸没式和精密液冷系统的普及。 SK Telecom等业者正与硬体製造商合作,将下一代热感解决方案商业化,与风冷相比,这些方案可降低高达30%的能耗。 Equinix已在包括新加坡在内的100多个设施中部署了液冷系统,以在保持AI服务性能的同时减少用水量。早期采用者可以获得成本优势,因为更高的机架密度可以减少占地面积,并提高每平方英尺的收益。

东南亚新兴城市超大规模和託管资料中心建设激增

泰国已累计27亿美元用于建设三个超大规模资料中心园区;印尼将从Digital Realty获得1亿美元投资,用于其雅加达的扩张;马来西亚将从谷歌获得20亿美元投资,其中包括建设一个现场水处理设施。对于在新加坡和东京面临电力和土地短缺的超大规模资料中心业者而言,在这些市场设立新址将加快部署速度,但也会对开关设备、变压器和专业供应链带来压力。

成熟枢纽地区的土地和电力供应暂停

新加坡于2024年解除了为期四年的电力开发禁令,但仅允许新增80兆瓦的装置容量,迫使开发人员必须满足严格的能源效率和人工智慧相关规定。东京也面临类似的挑战:其电网无法满足需求,迫使计划迁往千叶和北海道。有限的授权推高了地价,导致计划延期开工,并将资金推向吉隆坡、雅加达和曼谷。

细分市场分析

到2024年,解决方案将占据亚太绿色资料中心市场62.1%的份额,因为企业正在采用可快速部署到人工智慧丛集的整合式电力、冷却和自动化堆迭。虽然电力设备仍然是最大的细分市场,因为资料中心正在重新布线以提高密度,但随着液冷技术的日益普及,先进的冷却系统正经历两位数的成长。服务虽然目前规模较小,但其复合年增长率高达22.1%,超过了所有其他类别,这主要得益于对设计建造工程、可再生能源整合和认证咨询的需求。预计亚太绿色资料中心服务市场将随着复杂维修的增加而成长,到2030年将达到154亿美元。能够将软体定义能源管理平台与液冷硬体捆绑在一起的供应商,正在将自己定位为超大规模资料中心的一站式解决方案合作伙伴。

企业也开始寻求碳计量审核、绿色债券结构设计和购电协议谈判等专业服务。亚马逊的低碳水泥替代品使东京一栋建筑的体积碳排放量减少了64%,凸显了组件创新与咨询服务之间的关联。电气、机械和IT系统整合的专家能够降低试运行风险,并缩短投资者的收益实现週期。

到2024年,託管超大规模资料中心业者提供者将占据36.1%的市场份额,对于那些寻求可扩展容量但又不想前期投资的企业而言,託管服务提供者仍然至关重要。然而,受人工智慧模型训练和自主云端合约的驱动,超大规模资料中心供应商才是主要的成长引擎,其复合年增长率高达24.4%。与超大规模资料中心供应商相关的亚太地区绿色资料中心市场预计到2030年规模将成长三倍以上。随着TikTok等公司承诺在五年内向泰国託管计画投资88亿美元,雅加达、柔佛和巴淡岛的土地竞争日益激烈。

託管服务商正透过提供可直接用于液态储存的閒置频段、晶片级冷却通道以及每机架超过 40kW 的高密度电力供应来应对这项挑战。同时,超大规模资料中心营运商正在其建置进度超过需求的准入区域扩展託管服务。通讯业者部署又增加了一层需求,需要在 5G基地台附近部署微型站点以支援即时分析。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- AI驱动的高密度工作负载需要液冷和混合冷却

- 东南亚新兴大都市地区超大规模资料中心和託管资料中心的快速建设

- 政府净零排放指示及环境税收优惠政策

- 电网脱碳和企业购电协议加速可再生能源采购

- 通报不足:小型模组化反应器(SMR)零碳基本负载试验

- 低估:房地产投资信託基金式的绿色融资降低了华盛顿特区开发商的加权平均资本成本

- 市场限制

- 成熟枢纽城市(如新加坡、东京)的土地和电力开发暂停令

- 三级及以上永续建筑的资本投资溢价较高(15-20%)

- 先进冷却和资料中心互连(DCIM)技术方面的技术纯熟劳工短缺

- 漏报:水资源紧张法规限制了蒸发冷却

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章 市场规模及成长预测(数值)

- 按组件

- 服务

- 系统整合

- 监控服务

- 专业服务

- 其他服务

- 解决方案

- 电力

- 冷却

- 伺服器

- 网路装置

- 管理软体

- 其他解决方案

- 服务

- 依资料中心类型

- 託管服务提供者

- 超大规模资料中心业者/云端服务供应商

- 企业和边缘运算

- 依层级类型

- 一级和二级

- 三级

- 第四级

- 按行业

- 卫生保健

- 金融服务

- 政府

- 通讯/IT

- 製造业

- 媒体与娱乐

- 其他行业

- 按国家/地区

- 中国

- 印度

- 日本

- 马来西亚

- 澳洲

- 印尼

- 泰国

- 新加坡

- 韩国

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Fujitsu Limited

- Cisco Systems Inc.

- HP Inc.

- Dell Technologies Inc.

- Hitachi Ltd.

- Schneider Electric SE

- IBM Corporation

- Eaton Corporation plc

- Vertiv Holdings Co

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT DATA Group Corp.

- China Telecom Corp. Ltd.

- ST Telemedia Global Data Centres

- Keppel DC REIT

- AirTrunk Operating Pty Ltd.

- Huawei Technologies Co. Ltd.

- Amazon Web Services Inc.

- Microsoft Corp.

- Alibaba Cloud Computing Co. Ltd.

第七章 市场机会与未来展望

The Asia-Pacific green data center market is currently valued at USD 17.2 billion in 2025 and is forecast to reach USD 42.8 billion by 2030, advancing at a 20.05% CAGR.

Rising hyperscale deployments, strict net-zero policies, and rapid cloud adoption are steering capital toward energy-efficient facilities across China, India, Japan, and Southeast Asia. Liquid and hybrid cooling platforms, wider corporate power-purchase agreements, and lower weighted-average cost of capital from green financing are accelerating project pipelines. Companies are also re-engineering power architectures to support racks that now exceed 100 kW, while governments push location decisions toward secondary cities with abundant renewable energy. Competitive intensity is mounting as colocation specialists, cloud hyperscalers, and infrastructure real-estate investment trusts compete for scarce land, grid access, and skilled labor.

APAC Green Data Center Market Trends and Insights

AI-Driven High-Density Workloads Require Liquid and Hybrid Cooling

Rack densities have ballooned from 10 kW to beyond 100 kW for GPU-rich servers, prompting a shift toward direct, immersion, and precision liquid cooling systems. Operators such as SK Telecom are partnering with hardware manufacturers to commercialize next-generation thermal solutions that can trim energy use by up to 30% compared with air cooling. Equinix is rolling out liquid cooling in more than 100 facilities, including Singapore, to maintain performance for AI services while curbing water usage. Early adopters gain a cost advantage because higher rack density reduces floor space requirements and accelerates revenue per square foot.

Rapid Hyperscale and Colocation Build-Outs Across Emerging Southeast Asia Metros

Thailand has earmarked USD 2.7 billion for three hyperscale campuses, while Indonesia is receiving USD 100 million from Digital Realty for a Jakarta expansion. Malaysia has attracted a USD 2 billion pledge from Google that includes on-site water-treatment plants. New sites in these markets shorten deployment timelines for hyperscalers facing power and land caps in Singapore and Tokyo, though they strain regional supply chains for switchgear, transformers, and specialist contractors.

Land and Power Moratoriums in Mature Hubs

Singapore lifted its four-year moratorium in 2024 but released only 80 MW of new capacity, pushing developers to meet strict efficiency and AI-readiness rules. Tokyo faces similar challenges as grid upgrades lag demand, forcing projects to relocate to Chiba or Hokkaido. Limited permits inflate land prices and slow project starts, redirecting capital toward Kuala Lumpur, Jakarta, and Bangkok.

Other drivers and restraints analyzed in the detailed report include:

- Government Net-Zero Mandates and Green-Tax Incentives

- Grid Decarbonization and Corporate PPAs Accelerating Renewable Sourcing

- Skilled-Labour Shortage for Advanced Cooling and DCIM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 62.1% share of the Asia-Pacific green data center market in 2024 as enterprises favor integrated power, cooling, and automation stacks that can be deployed quickly for AI clusters. Power equipment remains the largest subsegment because facilities are re-wiring electrical backbones for higher density, while advanced cooling systems record double-digit growth as liquid technologies spread. Services are smaller today yet outpace all other categories with a 22.1% CAGR, fueled by demand for design-build engineering, renewable-energy integration, and certification consulting. The Asia-Pacific green data center market size for Services is projected to reach USD 15.4 billion by 2030, expanding alongside complex retrofits. Vendors able to bundle software-defined energy-management platforms with liquid cooling hardware position themselves as single-throat-to-choke partners for hyperscalers.

Enterprises also turn to professional services for carbon-accounting audits, green-bond structuring, and power-purchase agreement negotiations. Low-carbon materials, such as Amazon's cement replacements that cut embodied carbon by 64% in Tokyo builds, underscore how component innovation dovetails with service advisory. Integration specialists who can orchestrate electrical, mechanical, and IT systems reduce commissioning risk, shortening revenue realization cycles for investors.

Colocation operators held a 36.1% share in 2024 and remain vital for enterprises seeking scalable capacity without upfront capital. Yet hyperscalers, propelled by AI model training and sovereign-cloud contracts, are registering a 24.4% CAGR, making them the primary growth locomotive. The Asia-Pacific green data center market size tied to hyperscalers is projected to more than triple by 2030. Competition for land bank parcels in Jakarta, Johor, and Batam is intensifying as companies like TikTok pledge USD 8.8 billion over five years for Thailand hosting.

Colocation firms respond by offering liquid-ready white space, direct-to-chip cooling corridors, and high-density power feeds exceeding 40 kW per rack. Hyperscalers, in turn, expand colocation usage for on-ramp regions where self-build timelines exceed demand. Edge deployments by telecom operators add another layer, requiring micro-sites near 5G base stations to support real-time analytics.

Asia Pacific Green Data Center Market Report is Segmented by Services (System Integration, Monitoring Services, and More), Solutions (Power, Servers, Management Software, and More), Users (Colocation Providers, Cloud Service Providers, Enterprises), End-User Industries (Healthcare, Financial Services, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Fujitsu Limited

- Cisco Systems Inc.

- HP Inc.

- Dell Technologies Inc.

- Hitachi Ltd.

- Schneider Electric SE

- IBM Corporation

- Eaton Corporation plc

- Vertiv Holdings Co

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT DATA Group Corp.

- China Telecom Corp. Ltd.

- ST Telemedia Global Data Centres

- Keppel DC REIT

- AirTrunk Operating Pty Ltd.

- Huawei Technologies Co. Ltd.

- Amazon Web Services Inc.

- Microsoft Corp.

- Alibaba Cloud Computing Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven high-density workloads require liquid and hybrid cooling

- 4.2.2 Rapid hyperscale and colocation build-outs across emerging SE-Asia metros

- 4.2.3 Government net-zero mandates and green-tax incentives

- 4.2.4 Grid decarbonisation and corporate PPAs accelerating renewable sourcing

- 4.2.5 Under-reported: SMR (Small Modular Reactor) pilots for zero-carbon baseload

- 4.2.6 Under-reported: REIT-style green financing lowering WACC for DC developers

- 4.3 Market Restraints

- 4.3.1 Land and power moratoriums in mature hubs (e.g., Singapore, Tokyo)

- 4.3.2 High capex premium (15-20 %) for Tier III+ sustainable builds

- 4.3.3 Skilled-labour shortage for advanced cooling and DCIM

- 4.3.4 Under-reported: Water-stress regulations limiting evaporative cooling

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Service

- 5.1.1.1 System Integration

- 5.1.1.2 Monitoring Services

- 5.1.1.3 Professional Services

- 5.1.1.4 Other Services

- 5.1.2 Solution

- 5.1.2.1 Power

- 5.1.2.2 Cooling

- 5.1.2.3 Servers

- 5.1.2.4 Networking Equipment

- 5.1.2.5 Management Software

- 5.1.2.6 Other Solutions

- 5.1.1 Service

- 5.2 By Data Center Type

- 5.2.1 Colocation Providers

- 5.2.2 Hyperscalers/Cloud Service Providers

- 5.2.3 Enterprise and Edge

- 5.3 By Tier Type

- 5.3.1 Tier 1 and 2

- 5.3.2 Tier 3

- 5.3.3 Tier 4

- 5.4 By Industry Vertical

- 5.4.1 Healthcare

- 5.4.2 Financial Services

- 5.4.3 Government

- 5.4.4 Telecom and IT

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Other Verticals

- 5.5 By Country

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Malaysia

- 5.5.5 Australia

- 5.5.6 Indonesia

- 5.5.7 Thailand

- 5.5.8 Singapore

- 5.5.9 South Korea

- 5.5.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fujitsu Limited

- 6.4.2 Cisco Systems Inc.

- 6.4.3 HP Inc.

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Hitachi Ltd.

- 6.4.6 Schneider Electric SE

- 6.4.7 IBM Corporation

- 6.4.8 Eaton Corporation plc

- 6.4.9 Vertiv Holdings Co

- 6.4.10 Equinix Inc.

- 6.4.11 Digital Realty Trust Inc.

- 6.4.12 NTT DATA Group Corp.

- 6.4.13 China Telecom Corp. Ltd.

- 6.4.14 ST Telemedia Global Data Centres

- 6.4.15 Keppel DC REIT

- 6.4.16 AirTrunk Operating Pty Ltd.

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Amazon Web Services Inc.

- 6.4.19 Microsoft Corp.

- 6.4.20 Alibaba Cloud Computing Co. Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球绿色资料中心市场规模、份额、趋势和成长分析报告(2026-2034年)

全球绿色资料中心市场规模、份额、趋势和成长分析报告(2026-2034年) 全球可再生能源资料中心市场预测(至2034年):按组件、能源来源、资料中心类型、最终用户和地区划分全球碳中和资料中心市场预测(至2034年):按组件、资料中心类型、能源来源、最终用户和地区划分全球绿色资料中心市场预测(至2034年):按软体、基础设施、服务、公司规模、最终用户和地区划分

全球可再生能源资料中心市场预测(至2034年):按组件、能源来源、资料中心类型、最终用户和地区划分全球碳中和资料中心市场预测(至2034年):按组件、资料中心类型、能源来源、最终用户和地区划分全球绿色资料中心市场预测(至2034年):按软体、基础设施、服务、公司规模、最终用户和地区划分 2026年全球绿色资料中心市场报告

2026年全球绿色资料中心市场报告 碳中和资料中心市场-全球产业规模、份额、趋势、机会和预测:资料中心类型、碳中和解决方案、最终用户、地区和竞争格局(2021-2031)

碳中和资料中心市场-全球产业规模、份额、趋势、机会和预测:资料中心类型、碳中和解决方案、最终用户、地区和竞争格局(2021-2031) 日本绿色资料中心市场规模、份额、趋势及预测(按组件、资料中心类型、产业垂直领域和地区划分,2026-2034年)

日本绿色资料中心市场规模、份额、趋势及预测(按组件、资料中心类型、产业垂直领域和地区划分,2026-2034年) 绿色资料中心市场规模、份额和成长分析(按组件、资料中心规模、垂直产业和地区划分)-2026-2033年产业预测

绿色资料中心市场规模、份额和成长分析(按组件、资料中心规模、垂直产业和地区划分)-2026-2033年产业预测 碳中和资料中心市场规模、份额和成长分析(按资料中心类型、应用、碳中和解决方案和地区划分)-2026-2033年产业预测

碳中和资料中心市场规模、份额和成长分析(按资料中心类型、应用、碳中和解决方案和地区划分)-2026-2033年产业预测 按资料中心类型、产品、最终用户产业和部署规模分類的碳中和资料中心市场—2025-2032年全球预测

按资料中心类型、产品、最终用户产业和部署规模分類的碳中和资料中心市场—2025-2032年全球预测