|

市场调查报告书

商品编码

1849887

北美炭黑:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)North America Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

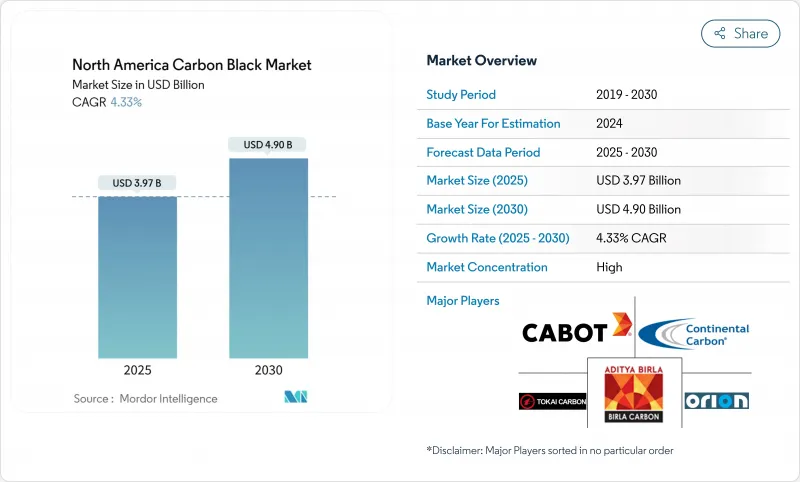

预计北美炭黑市场规模到 2025 年将达到 39.7 亿美元,并以 4.33% 的复合年增长率成长,到 2030 年将达到 49 亿美元。

这一成长轨迹反映出该行业成熟且富有韧性,受益于轮胎产业持续向电动车转型、稳定的塑胶需求以及该地区持续的基础设施投资。美国墨西哥湾沿岸充足的原料供应以及降低能源强度的製程改进,正在提升生产商的利润率,并促使其对特种等级产品进行有针对性的投资。同时,加拿大的监管利好和墨西哥的主导需求分别推动了优质化和最终用途多元化。竞争策略集中在回收炭黑的规模化、专有的表面改质以及与轮胎和电池製造商的一体化供应协议上,这将使北美炭黑市场在2030年之前实现均衡成长。

北美炭黑市场趋势与洞察

宽基电动车轮胎需求激增,需要高表面积炉黑

宽基电动车轮胎每条轮胎使用的炭黑比标准乘用车轮胎更多。轮胎製造商正在采用高比表面积炉法炭黑,以降低滚动阻力并保持耐用性。固特异的示范轮胎采用永续炭黑前驱配方,在不牺牲抓地力的情况下降低了滚动阻力,检验了这项材料策略。电动车专用轮胎的原始设备製造商(OEM)组装目标预计将加速专门食品炭黑的普及,并提高北美炭黑市场的平均售价。因此,拥有先进粒度控制技术的供应商在与主要电动车轮胎製造商达成长期供应协议方面处于有利地位。即使在传统轮胎销售量停滞不前的情况下,电动车性能标准所创造的高端市场也预计将提升毛利率。

美国墨西哥湾沿岸炼油厂供应的低成本澄清油提高了生产商的利润率

预计到2025年,原油产量将增加至1,350万桶/日,这将确保澄清油(炉黑生产的关键原料)的稳定供应。墨西哥湾沿岸炼油厂的生产商享有比欧洲和亚洲同行更低的原料交付成本,从而形成了可持续的成本优势。这种差异使北美供应商拥有资本弹性,可以用能源回收系统维修反应器,并为回收炭黑中试线提供资金,而不会危及短期盈利。因此,产能合理化压力仍然较低,北美炭黑市场继续受益于竞争激烈且稳定的定价环境,有利于高效的营运商。这种成本缓衝也支持对生物基和循环原料的探索,使区域生产商走在永续性创新的前沿。

沿岸地区供应中断导致原物料价格波动

飓风活动和炼油厂维修中断会定期限制澄清油的流动,导致现货价格上涨并侵蚀非综合炭黑生产商的利润。美国能源资讯署指出,即使是墨西哥湾沿岸的短暂中断也会迅速波及区域原料市场,迫使一些工厂降低运转率。虽然供应商正在扩大储存槽并采用商品对冲计划来缓衝波动,但库存增加会增加营运资金需求。缺乏资产负债表能力的小型企业面临营运成本分散加剧的问题,这可能会加速北美炭黑市场的整合。从长远来看,对多原料灵活性的投资(允许使用替代油浆)应该可以缓解价格波动,但在短期内,不可预测性仍然是一个阻力。

細項分析

到2024年,炉法炭黑将占据北美炭黑市场85%的份额,其灵活的反应器配置可适应多种原料,并在大批量应用中提供一致的品质。炉法炭黑85%的份额预计复合年增长率为4.71%,超过北美炭黑市场的整体成长速度,并得益于能源回收升级,从而降低了单位成本和排放。热感炭黑、气黑和灯黑共同占据着细分市场,供应特殊塑胶、油墨和电池组件,而这些应用都需要独特的粒度和纯度。受轮胎和机械橡胶产品製造商强劲需求的推动,产能扩张仍将集中在炉法技术上。

持续的炉内创新实现了更紧密的粒度分布和定制的表面化学性质,使生产商能够定制用于先进电池和轻量化复合材料部件的牌号。轮胎热热解油等回收原料正在试验使用,以在不影响产量的情况下实现炉内脱碳。这些进步增强了炉黑的结构优势,并确保该工艺在行业将永续性要求与性能要求相结合的过程中保持领先地位。

2024年,标准级电池占总销售量的78%,而特种级电池的利润份额则更高,预计复合年增长率为5.22%,高于基准市场成长率。导电级和静电耗散级电池的市场规模虽然仍然较小,但正在迅速扩张,因为导电性在锂离子电池中起着关键作用,它决定了充电速度和循环寿命。

《电源杂誌》发表的一项研究发现,最佳导电炭黑微观结构与更高的电池能量密度相关,从而鼓励电池製造商签订长期供应协议。这种技术依赖性增加了转换壁垒,并增强了定价弹性。随着原始设备製造商追求更高的回收率,将再生炭黑与原生专门食品炭黑混合的混合配方有望扩大北美炭黑产业的价值创造。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 宽基电动车轮胎需求激增,需要高表面积炉黑

- 美国墨西哥湾沿岸炼油厂供应的低成本澄清油提高了生产商的利润率

- 加拿大轮胎标籤法规推动特种轮胎的普及

- 原始设备製造商实现 ESG 目标推动对回收炭黑 (rCB) 的需求

- 墨西哥建设业復苏刺激塑胶和涂料需求

- 市场限制

- 墨西哥湾沿岸供应中断导致原物料价格波动

- 乘用车胎面胶中的二氧化硅-硅烷替代物

- 与轮胎热解衍生填料的竞争

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

第五章市场规模和成长预测(价值和数量)

- 依流程类型

- 炉黑

- 气黑

- 灯黑

- 热感炭黑

- 按年级

- 标准级炭黑

- 特种炭黑

- 导电防静电炭黑

- 按用途

- 轮胎和工业橡胶製品

- 塑胶

- 碳粉和印刷油墨

- 涂层

- 纤维

- 其他用途

- 按最终用户产业

- 汽车和运输

- 包裹

- 建筑/施工

- 电机与电子工程

- 纺织品和服装

- 其他的

- 按地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons SA

- Continental Carbon Company

- Tokai Carbon Co., Ltd.(incl. Cancarb)

- Mitsubishi Chemical Corporation

- OMSK Carbon Group

- PCBL Limited

- Imerys

- Monolith Inc.

- Pyrolyx AG

- Koppers Inc.

- Sid Richardson Carbon & Energy Co.

- International China Rubber Investment Holding Co., Ltd.

第七章 市场机会与未来展望

The North America carbon black market stands at USD 3.97 billion in 2025 and is projected to advance at a 4.33% CAGR to reach USD 4.90 billion by 2030.

This growth trajectory reflects a mature but resilient sector that benefits from the tire industry's ongoing shift toward electric mobility, steady plastics demand, and continued infrastructure spending in the region. Robust feedstock availability along the United States Gulf Coast and process improvements that lower energy intensity are bolstering producer margins and enabling targeted investments in specialty grades. Meanwhile, regulatory tailwinds in Canada and construction-led demand in Mexico are driving premiumization and end-use diversification, respectively. Competitive strategies increasingly center on recovered carbon black scale-up, proprietary surface modifications, and integrated supply agreements with tire and battery makers, positioning the North America carbon black market for balanced growth through 2030.

North America Carbon Black Market Trends and Insights

Surging Demand for Wide-Base EV Tires Requiring High-Surface-Area Furnace Blacks

Wide-base electric vehicle tires use more carbon black per unit than standard passenger tires because higher torque and heavier battery loads accelerate tread wear. Tire makers are deploying high-surface-area furnace blacks that maintain durability while lowering rolling resistance, a balance essential for extending battery range. Goodyear's demonstration tires that blend sustainable carbon black precursors achieved reduced rolling resistance without sacrificing grip, validating this material strategy. OEM fitment targets for EV-specific tires are forecast to accelerate specialty black penetration, enhancing average selling prices across the North America carbon black market. Suppliers with advanced particle-size control technologies are therefore positioned to secure long-term supply contracts with leading EV tire producers. The premium segment created by EV performance standards is expected to lift gross margins even as traditional tire volumes plateau.

Low-Cost Decant Oil Availability from U.S. Gulf Coast Refiners Enhancing Producer Margins

Crude production growth to 13.5 million b/d in 2025 ensures a steady stream of decant oil, the principal feedstock for furnace black manufacturing. Producers near Gulf Coast refineries enjoy lower delivered-feedstock costs than European or Asian peers, creating a durable cost advantage. This differential affords North American suppliers the capital flexibility to retrofit reactors with energy recovery systems and to finance pilot lines for recovered carbon black without eroding near-term profitability. As a result, capacity rationalization pressure remains low, and the North America carbon black market continues to benefit from a competitive but stable pricing environment that favors efficient operators. The cost cushion also underwrites research into bio-based and circular feedstocks, keeping regional producers at the forefront of sustainability innovation.

Feedstock Price Volatility amid Gulf-Coast Supply Disruptions

Hurricane activity and refinery maintenance outages periodically constrain decant oil flow, driving spot price spikes that erode margins for non-integrated carbon black producers. The U.S. Energy Information Administration notes that even brief Gulf Coast disruptions ripple rapidly through regional feedstock markets, forcing some plants to run at reduced rates. Suppliers are expanding storage tanks and adopting commodity hedging programs to buffer volatility, but inventory build-ups raise working capital needs. Smaller firms lacking balance-sheet capacity face higher operating-cost dispersion, potentially accelerating consolidation in the North America carbon black market. Over time, investment in multi-feedstock flexibility, enabling the use of alternative slurry oils, should temper price swings, yet in the near term, unpredictability remains a headwind.

Other drivers and restraints analyzed in the detailed report include:

- Canadian Tire-Label Regulations Boosting Specialty Grade Adoption

- Recovered Carbon Black (rCB) Uptake Driven by OEM ESG Targets

- Silica-Silane Substitution in Passenger-Car Tread Compounds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Furnace black retained an 85% share of the North America carbon black market in 2024, leveraging flexible reactor configurations that accommodate diverse feedstocks and yield consistent quality across high-volume applications. The segment's 85% shares translates to a 4.71% CAGR outlook, outpacing the overall North America carbon black market size growth, supported by energy recovery upgrades that lower unit costs and emissions. Thermal black, gas black, and lamp black collectively occupy niche segments, supplying specialized plastics, inks, and battery components where unique particle size or purity is essential. Capacity expansions remain concentrated in furnace technology, underpinned by strong demand from tire and mechanical rubber goods producers.

Continued reactor innovation enables tighter particle size distribution and custom surface chemistry, allowing producers to tailor grades for advanced batteries and lightweight composite parts. Circular feedstocks such as tire pyrolysis oil are being piloted to decarbonize furnace operations without sacrificing throughput. These advancements reinforce furnace black's structural advantage, ensuring the process maintains leadership as the North America carbon black industry integrates sustainability imperatives with performance requirements.

Standard grades accounted for 78% of 2024 volume, but specialty grades generated a disproportionate share of profit, aided by a 5.22% CAGR projection that exceeds baseline market growth. Conductive and electrostatic-dissipative grades, while still a smaller slice, are scaling rapidly thanks to their critical role in lithium-ion batteries where conductivity dictates charge rates and cycle life.

Research in the Journal of Power Sources links optimal conductive carbon black micro-structure to higher battery energy density, prompting battery makers to lock in long-term supply contracts. This technical dependency elevates switching barriers and fortifies pricing resilience. As OEMs pursue higher recycled content, hybrid formulations that blend rCB with virgin specialty blacks are poised to extend value creation across the North America carbon black industry.

The North America Carbon Black Market Report Segments the Industry by Process Type (Furnace Black, Gas Black, Lamp Black, and Thermal Black ), Grade (Standard Grade Carbon Black, Specialty Carbon Black, and More), Application (Tires and Industrial Rubber Products, Toners and Printing Inks, and More), End-User Industry (Automotive and Transportation, Packaging, and More), and Geography (United States, Canada, and Mexico).

List of Companies Covered in this Report:

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons S.A.

- Continental Carbon Company

- Tokai Carbon Co., Ltd. (incl. Cancarb)

- Mitsubishi Chemical Corporation

- OMSK Carbon Group

- PCBL Limited

- Imerys

- Monolith Inc.

- Pyrolyx AG

- Koppers Inc.

- Sid Richardson Carbon & Energy Co.

- International China Rubber Investment Holding Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Wide-Base EV Tires Requiring High-Surface-Area Furnace Blacks

- 4.2.2 Low-Cost Decant Oil Availability from U.S. Gulf Coast Refiners Enhancing Producer Margins

- 4.2.3 Canadian Tire-Label Regulations Boosting Specialty Grade Adoption

- 4.2.4 Recovered Carbon Black (rCB) Uptake Driven by OEM ESG Targets

- 4.2.5 Infrastructure-Led Construction Rebound in Mexico Spurring Plastics and Coatings Demand

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility Amid Gulf-Coast Supply Disruptions

- 4.3.2 Silica-Silane Substitution in Passenger-Car Tread Compounds

- 4.3.3 Competition from Tire-Pyrolysis Derived Fillers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Process Type

- 5.1.1 Furnace Black

- 5.1.2 Gas Black

- 5.1.3 Lamp Black

- 5.1.4 Thermal Black

- 5.2 By Grade

- 5.2.1 Standard Grade Carbon Black

- 5.2.2 Specialty Carbon Black

- 5.2.3 Conductive and ESD Carbon Black

- 5.3 By Application

- 5.3.1 Tires and Industrial Rubber Products

- 5.3.2 Plastics

- 5.3.3 Toners and Printing Inks

- 5.3.4 Coatings

- 5.3.5 Textile Fibers

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Packaging

- 5.4.3 Building and Construction

- 5.4.4 Electrical and Electronics

- 5.4.5 Textile and Apparel

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cabot Corporation

- 6.4.2 Birla Carbon

- 6.4.3 Orion Engineered Carbons S.A.

- 6.4.4 Continental Carbon Company

- 6.4.5 Tokai Carbon Co., Ltd. (incl. Cancarb)

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 OMSK Carbon Group

- 6.4.8 PCBL Limited

- 6.4.9 Imerys

- 6.4.10 Monolith Inc.

- 6.4.11 Pyrolyx AG

- 6.4.12 Koppers Inc.

- 6.4.13 Sid Richardson Carbon & Energy Co.

- 6.4.14 International China Rubber Investment Holding Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth in the Adoption of Electric Cars

特种奈米碳管管粉末市场:依纯度、类型、生产方法、功能、最终用途和应用划分-全球预测,2026-2032年

特种奈米碳管管粉末市场:依纯度、类型、生产方法、功能、最终用途和应用划分-全球预测,2026-2032年 全球炭黑市场(2026-2036)

全球炭黑市场(2026-2036) 炭黑:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

炭黑:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球炭黑市场报告2026年全球石墨化炭黑(GCB)市场报告

2026年全球炭黑市场报告2026年全球石墨化炭黑(GCB)市场报告 炭黑市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年炭黑填充母粒市场按类型、等级、产品形式、加工技术、应用和分销管道划分,全球预测(2026-2032年)全球炭黑市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析、未来预测(2026-2034)标准炭黑市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034 年)

炭黑市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年炭黑填充母粒市场按类型、等级、产品形式、加工技术、应用和分销管道划分,全球预测(2026-2032年)全球炭黑市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析、未来预测(2026-2034)标准炭黑市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034 年) 炭黑市场规模、份额及成长分析(按应用、类型、等级及地区划分)-2026-2033年产业预测

炭黑市场规模、份额及成长分析(按应用、类型、等级及地区划分)-2026-2033年产业预测