|

市场调查报告书

商品编码

1849888

活动管理软体:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Event Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

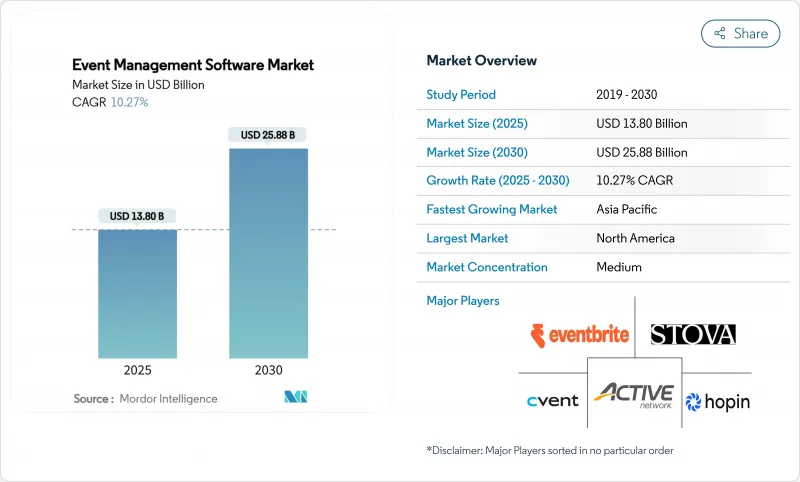

预计活动管理软体市场规模到 2024 年将达到 138 亿美元,到 2030 年将达到 258.8 亿美元,2025 年至 2030 年的复合年增长率为 10.27%。

虚拟和混合活动中对人工智慧个人化的强劲需求、向云端交付的快速转变以及对永续性报告日益增加的监管压力正在推动成长势头。供应商正在透过收购来加速扩张,将规划、行销和分析功能捆绑到整合套件中,从而提高进入门槛。随着中小型企业 (SMB) 大规模采用自助票务工具,竞争日益激烈,迫使现有供应商改善其定价和整合策略。在亚太地区,5G 和光纤到府 (FTTX) 等基础设施升级正在实现即时富媒体互动并扩大可寻址用户群,支援两位数成长。然而,大型企业旧有系统整合挑战和 SaaS 订阅疲劳正在抑制整体成长。

全球活动管理软体市场趋势与洞察

人工智慧驱动的个人化改变虚拟和混合活动

北美平台整合了一个行为分析引擎,可以即时汇总客製化议程、会议提案和网路配对。 Bizzabo 的人工智慧活动助理于 2024 年 12 月推出,可自动执行重复的规划任务,同时提高与会者的参与度分数,展示了 Bizzabo 超个人化旅程对收益的影响。早期采用者报告虚拟与会者转化为合格潜在客户的转换率更高,促使行销团队将与数据丰富的体验相关的活动预算翻倍。这种转变也加速了註册、内容和社群模组与机器学习管道的集成,重塑了供应商蓝图。随着生成工具变得更加实惠,小型供应商正在迅速将它们纳入其中以避免客户流失。结果是,各方竞相透过更深入的即时个人化来实现核心物流能力以外的差异化,竞争日益激烈。

自助票务系统在欧洲中小企业中越来越受欢迎

欧洲中小企业越来越多地采用低代码票务平台,以消除对IT的依赖并加快产品上市时间。根据Verizon的一项调查,77%的中小企业认为高速连线是提高生产力的关键槓桿,这促使供应商提供简化的分级定价和直觉的使用者介面。敏捷挑战者市场份额的不断增长,正迫使现有企业扩展免费增值模式,并整合入门嚮导以保持竞争力。由于中小企业占该地区就业人口的大多数,它们的采用曲线将显着影响活动管理软体市场。能够在功能丰富性和易用性之间取得平衡的供应商正在获得不成比例的市场份额,从而强化产品反馈和快速迭代的良性循环。

整合旧有系统的挑战阻碍了广泛采用

新兴经济体的许多场馆仍然依赖缺乏现代 API 的专有物业管理系统。整合现代平台需要繁琐的中间件,从而延长引进週期并增加整体拥有成本。资料同步滞后会减慢自动化速度,并让期待统一仪表板的规划人员感到沮丧。儘管领先的供应商提供旨在连接传统资料库和云端架构的连接器市场和专业服务,但发展中地区的成本敏感度减缓了采用速度。政府对数位化现代化的补贴将有助于推动采用,但这在短期内仍将阻碍希望实现地理扩张的供应商。

細項分析

活动策划应用程式创造了最大的收入,占2024年活动管理软体市场的29.97%。此细分市场的复合年增长率预测为两位数,达到13.12%,显示工作流程编配功能仍是数位转型的核心。在实践中,自动化任务清单、集中式资产库和相关人员协作区可以压缩生产计划并提高一致性。 RainFocus的活动基准评估工具使客户能够根据同侪基准评估其绩效,并指导优化策略,并将回馈回馈到策划模组。

随着相关模组(预算管理、内容管理、场地采购)整合到单一仪表板,活动管理软体市场中规划产品的规模预计将进一步成长。供应商正在分层添加预测分析功能,根据历史参与度评分推荐理想的会议形式和演讲者组合。由此形成了一个强化循环:更丰富的洞察推动了对更详细规划功能的需求,而更深入的采用则创建了资料集,从而提高了预测的准确性。

预计到 2024 年,云端解决方案将占据活动管理软体市场 75% 的份额,并以 13.10% 的稳健复合年增长率成长。快速部署、弹性扩展和无缝功能推出取代了对资料持久性和离线存取的担忧。随着人工智慧处理需求转向中央运算丛集而非本地伺服器,云端解决方案的活动管理软体市场规模将大幅成长。

虽然中小企业率先迈向云端,但大型企业出于环境和成本方面的考虑,正在加速从传统资料中心迁移。供应商纷纷推出单一租户和主权云端模式,以满足产业特定的合规性要求。边缘快取和渐进式 Web 应用程式等创新正在降低远端位置的连线风险,并扩大地理覆盖范围。

活动管理软体市场按软体类型(活动规划、活动行销、其他)、组织规模(中小型企业、大型企业)、部署类型(云端、本地)、最终用户垂直领域(企业、政府、其他)和地区细分。市场预测以美元计算。

区域分析

2024年,北美将占全球收入的39.85%,并将继续保持绝对支出最高的地区地位,这得益于其早期的技术采用、成熟的供应商总部以及成熟的讚助市场。 Eventbrite在2023年处理了3.02亿张门票,总票务价值达36亿美元,展现了其生态系统的规模。中小企业对生成式人工智慧的采用在一年内翻了一番,目前有40%的企业正在使用此类工具。日益增长的隐私预期将推动对SOC 2和欧盟-美国资料隐私框架认证的需求,使合规领导力成为竞争优势。

预计亚太地区将经历最快的成长速度,复合年增长率达14.30%,这得益于5G的广泛应用、数位支付的激增以及政府主导的智慧城市计画。 GSMA表示,该地区单场5G影院直播就吸引了250万远端观众,凸显了可靠的高清串流媒体所释放的潜在受众。由于消费者对集票务、串流媒体和社交商务于一体的超级应用的熟悉程度,预计韩国、日本和印度的表现将超越地区平均水平。对于寻求市场份额的国际供应商而言,本地化(货币、语言和监管细节)仍将至关重要。

儘管影响产品蓝图的法规日益复杂,欧洲仍是一个重要的市场。碳排放揭露要求和符合GDPR的资料处理要求,迫使供应商整合精细的同意管理和永续性仪表板。 Cvent与VOK DAMS合作,以加强其在DACH丛集的本地服务。同时,中小企业自助购票的普及正在加速,这重新分配了通路经济,并加剧了价格竞争。

随着各国政府投入大量资金建设与现有会议中心相媲美的大型场馆,中东和非洲地区的重要性日益凸显。巴林耗资2.2185亿美元的会展中心和杜拜展览中心的扩建项目,持续不断的活动行程表都离不开企业级业务编配平台Zawya。提供阿拉伯语介面、多币种支付和大容量徽章列印功能的供应商是早期成功的理想选择。虽然传统的PMS整合挑战仍然存在,但我们预计,新建场馆从一开始就采用现代化的饭店服务堆迭,可以缓解这些挑战。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 虚拟和混合活动中人工智慧个性化的兴起(北美)

- 中小型场馆快速采用自助售票系统(欧洲)

- 大规模 5G/FTTX 部署推动互动直播功能(亚洲)

- 企业活动中强制性的永续性报告推动了对分析的需求增加(欧盟)

- 海湾合作委员会各国政府(中东)积极投资会展基础设施

- 高等教育联盟越来越青睐校园范围的活动套房(大洋洲)

- 市场限制

- 发展中地区场馆与传统PMS整合的摩擦

- 大型企业客户对 SaaS 订阅的疲劳感日益加重

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争的激烈程度

第五章市场规模及成长预测

- 依软体类型

- 活动企划

- 活动行销

- 场地和票务管理

- 分析和报告

- 其他的

- 按部署

- 云

- 本地部署

- 按组织规模

- 小型企业

- 大公司

- 按最终用户

- 公司

- 政府

- 教育

- 媒体和娱乐

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他拉丁美洲地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 其他亚太地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- Strategic Developments

- Vendor Positioning Analysis

- 公司简介

- Cvent Inc.

- Stova(Aventri+MeetingPlay)

- Eventbrite Inc.

- Tripleseat

- ACTIVE Network

- Momentus Technologies

- Certain Inc.

- SignUpGenius

- EMS Software

- Hopin

- Bizzabo

- Whova

- vFairs

- Splash

- Eventzilla

- Brown Paper Tickets

- idloom

- TryBooking

- Hubb

- MeetApp

第七章 市场机会与未来展望

The event management software size market is valued at USD 13.80 billion in 2024 and is forecast to reach USD 25.88 billion in 2030, advancing at a 10.27% CAGR between 2025 and 2030.

Strong demand for AI-powered personalization in virtual and hybrid events, the rapid transition to cloud delivery, and rising regulatory pressure for sustainability reporting are reinforcing growth momentum. Vendors are accelerating capability expansion through acquisitions that bundle planning, marketing, and analytics features into unified suites, strengthening barriers to entry. Competitive intensity is rising as small and medium-sized businesses (SMBs) adopt self-service ticketing tools at scale, compelling incumbents to refine pricing and integration strategies. Infrastructure upgrades such as 5G and fiber-to-the-x (FTTX) in Asia-Pacific unlock real-time rich-media engagement, widening addressable user bases and underpinning double-digit regional growth. Meanwhile, legacy system integration issues and mounting SaaS subscription fatigue among large enterprises temper the overall trajectory.

Global Event Management Software Market Trends and Insights

AI-powered personalization transforms virtual and hybrid events

North American platforms now embed behavioral analytics engines that assemble bespoke agendas, session suggestions, and networking matches in real time. Bizzabo's AI-driven event assistant, launched in December 2024, automates repetitive planning tasks while raising attendee engagement scores, demonstrating the revenue impact of hyper-personalized journeys Bizzabo. Early adopters report higher conversion of virtual participants into qualified leads, encouraging marketing teams to double event budgets tied to data-rich experiences. The shift is also reshaping vendor roadmaps, prompting accelerated integration of machine learning pipelines with registration, content, and community modules. As generative tools become affordable, smaller providers rapidly embed them to avoid churn. The net effect is a competitive race toward deeper, real-time personalization that differentiates offerings beyond core logistics features.

Self-service ticketing systems gain traction among European SMBs

European SMBs increasingly deploy low-code ticketing platforms that remove IT dependence and compress go-to-market timelines. A Verizon survey shows that 77% of small businesses consider high-speed connectivity a key productivity lever, a figure that has pushed vendors to launch simplified, tiered pricing and intuitive user interfaces Verizon. Market share gains by agile challengers are pressuring incumbents to extend freemium models and embed onboarding wizards to sustain relevance. Because SMBs account for the majority of regional employment, their adoption curve exerts outsized influence on the event management software market. Providers able to balance feature depth with ease of use are capturing disproportionate wallet share, reinforcing a virtuous cycle of product feedback and rapid iteration.

Legacy system integration challenges hinder adoption

Many venues in emerging economies still rely on proprietary property-management systems lacking modern APIs. Integrating contemporary platforms requires labor-intensive middleware that extends deployment cycles and inflates total cost of ownership. Data synchronization lags limit automation, frustrating planners who expect unified dashboards. Forward-thinking vendors offer connector marketplaces and professional services targeted at bridging archaic databases with cloud architectures, but cost sensitivity in developing regions slows uptake. Where governments subsidize digital modernization, adoption rebounds, yet the near-term drag remains material for vendors counting on geographic expansion.

Other drivers and restraints analyzed in the detailed report include:

- 5G/FTTX infrastructure enables interactive live-stream innovations

- Sustainability reporting requirements drive analytics demand

- SaaS subscription fatigue impacts enterprise clients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Event planning applications generated the largest revenue slice at 29.97% of the event management software market in 2024. The segment's double-digit 13.12% CAGR forecast shows that workflow orchestration capabilities remain the nucleus of digital transformation. In practice, automated task lists, centralized asset libraries, and stakeholder collaboration zones compress production schedules and elevate consistency. RainFocus' Event Benchmark Assessment tool lets customers evaluate performance against peer benchmarks, guiding optimization strategies that feed back into planning modules.

The event management software market size for planning products is projected to widen further as adjacent modules-budgeting, content management, and venue sourcing-are embedded into single dashboards. Vendors are layering predictive analytics that recommend ideal session formats or speaker mixes based on historical engagement scores. The result is a reinforcing loop: richer insights drive demand for more detailed planning features, and deeper adoption yields datasets that sharpen predictive accuracy.

Cloud options secured 75% share of the event management software market in 2024 and are growing at a healthy 13.10% CAGR. Fast deployment, elastic scalability, and seamless feature rollouts override residual concerns around data residency and offline access. The event management software market size for cloud solutions is set to surge as AI processing needs favor central compute clusters over on-premise servers.

SMBs spearheaded the migration, yet large enterprises now accelerate moves to sunset legacy data centers for environmental and cost reasons. Providers respond with single-tenant and sovereign-cloud variants that meet sector-specific compliance mandates. Innovations such as edge caching and progressive web applications mitigate connectivity risks at remote venues, widening addressable geographies.

Event Management Software Market Segments Into by Software Type (Event Planning, Event Marketing, and More), by Organization Size (Small and Medium Enterprises, Large Enterprises), by Deployment Type (Cloud, On-Premise), by End-User Vertical (Corporate, Government, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 39.85% of global revenue in 2024 and continues to command the highest absolute spend thanks to early technology adoption, entrenched vendor headquarters, and mature sponsorship markets. Eventbrite processed USD 3.6 billion in gross ticket value across 302 million passes in 2023, illustrating ecosystem scale Eventbrite. Generative AI penetration in small businesses doubled in a year, with 40% now using such tools, a statistic that drives aggressive feature launches in regional platforms . Heightened privacy expectations spur demand for SOC 2 and EU-U.S. Data Privacy Framework certifications, positioning compliance leadership as a competitive wedge.

Asia-Pacific registers the fastest trajectory at a 14.30% CAGR, supported by sweeping 5G coverage, surging digital payments, and government-led smart-city programs. The region attracted 2.5 million remote viewers to a single 5G-enabled theatre broadcast, highlighting latent audience pools unlocked by reliable high-definition streams GSMA. South Korea, Japan, and India are forecast to outpace regional averages, propelled by consumer familiarity with super-apps that bundle ticketing, streaming, and social commerce. Localization-currency, language, and regulatory nuances-remains decisive for foreign vendors targeting share capture.

Europe sustains meaningful volume amid regulatory complexity shaping product roadmaps. Mandatory carbon disclosure and GDPR-aligned data handling push vendors to embed granular consent controls and sustainability dashboards. Cvent's alliance with VOK DAMS deepens local service provision in the DACH cluster, signaling the importance of culturally attuned support vehicles for mid-market accounts Cvent. Meanwhile, self-service ticketing adoption among SMBs accelerates, redistributing channel economics and intensifying price competition.

The Middle East and Africa witness rising relevance as governments channel funds into mega-venue construction that rivals established convention hubs. Bahrain's USD 221.85 million center and Dubai Exhibition Centre's expansion will generate continuous event calendars that necessitate enterprise-grade orchestration platforms Zawya. Providers offering Arabic interfaces, multicurrency settlement, and high-volume badge printing are best placed to win early contracts. Legacy PMS integration challenges linger yet are expected to ease as newly built facilities deploy modern hospitality stacks from inception.

- Cvent Inc.

- Stova (Aventri+MeetingPlay)

- Eventbrite Inc.

- Tripleseat

- ACTIVE Network

- Momentus Technologies

- Certain Inc.

- SignUpGenius

- EMS Software

- Hopin

- Bizzabo

- Whova

- vFairs

- Splash

- Eventzilla

- Brown Paper Tickets

- idloom

- TryBooking

- Hubb

- MeetApp

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI-powered personalization across virtual and hybrid events (North America)

- 4.2.2 Rapid adoption of self-service ticketing systems by SMB venues (Europe)

- 4.2.3 Large-scale roll-out of 5G/FTTX driving interactive live-stream features (Asia)

- 4.2.4 Mandatory sustainability reporting for corporate events boosting analytics demand (EU)

- 4.2.5 Aggressive MICE infrastructure investments by GCC governments (Middle East)

- 4.2.6 Growing preference for campus-wide event suites in higher-education consortia (Oceania)

- 4.3 Market Restraints

- 4.3.1 Friction from venue-legacy PMS integrations in developing regions

- 4.3.2 Rising SaaS subscription fatigue among large enterprise clients

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Software Type

- 5.1.1 Event Planning

- 5.1.2 Event Marketing

- 5.1.3 Venue and Ticket Management

- 5.1.4 Analytics and Reporting

- 5.1.5 Others

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 Corporate

- 5.4.2 Government

- 5.4.3 Education

- 5.4.4 Media and Entertainment

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Cvent Inc.

- 6.3.2 Stova (Aventri+MeetingPlay)

- 6.3.3 Eventbrite Inc.

- 6.3.4 Tripleseat

- 6.3.5 ACTIVE Network

- 6.3.6 Momentus Technologies

- 6.3.7 Certain Inc.

- 6.3.8 SignUpGenius

- 6.3.9 EMS Software

- 6.3.10 Hopin

- 6.3.11 Bizzabo

- 6.3.12 Whova

- 6.3.13 vFairs

- 6.3.14 Splash

- 6.3.15 Eventzilla

- 6.3.16 Brown Paper Tickets

- 6.3.17 idloom

- 6.3.18 TryBooking

- 6.3.19 Hubb

- 6.3.20 MeetApp

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

事件管理软体市场按元件、功能、事件类型、部署类型、组织规模和应用程式划分 - 全球预测 2025-2032云端基础的事件管理市场(按格式、部署模型、应用程式和最终用户产业)—全球预测 2025-2032

事件管理软体市场按元件、功能、事件类型、部署类型、组织规模和应用程式划分 - 全球预测 2025-2032云端基础的事件管理市场(按格式、部署模型、应用程式和最终用户产业)—全球预测 2025-2032 2025年活动管理工俱全球市场报告

2025年活动管理工俱全球市场报告 全球活动管理软体市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球活动管理软体市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 日本活动管理软体市场报告(按组件、部署类型、组织规模、最终用户和地区)2025 年至 2033 年

日本活动管理软体市场报告(按组件、部署类型、组织规模、最终用户和地区)2025 年至 2033 年 事件管理软体市场规模、份额、成长分析(按组件、按事件类型、按部署、按公司规模、按应用、按地区)- 行业预测 2025-2032

事件管理软体市场规模、份额、成长分析(按组件、按事件类型、按部署、按公司规模、按应用、按地区)- 行业预测 2025-2032 全球活动管理软体市场(2025-2029)2025年云端基础的事件管理全球市场报告2025年活动管理平台全球市场报告

全球活动管理软体市场(2025-2029)2025年云端基础的事件管理全球市场报告2025年活动管理平台全球市场报告 事件管理软体市场规模、份额、趋势分析报告:按组件、部署、公司规模、应用、地区和细分市场预测,2025 年至 2030 年

事件管理软体市场规模、份额、趋势分析报告:按组件、部署、公司规模、应用、地区和细分市场预测,2025 年至 2030 年