|

市场调查报告书

商品编码

1849892

北美企业资源规划:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)North America Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

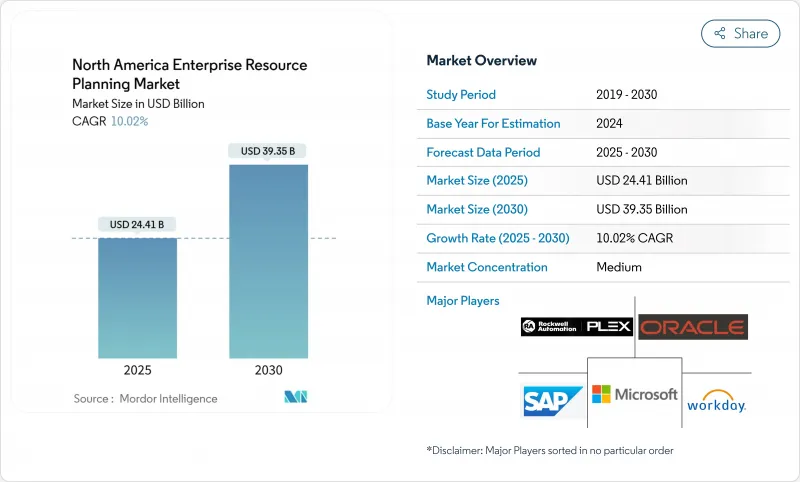

预计到 2025 年北美企业资源规划市场规模将达到 244.1 亿美元,到 2030 年将达到 393.5 亿美元,复合年增长率高达 10.0%。

这项扩张反映了全部区域从传统的本地套件向云端原生平台的转变,这些平台为企业提供了敏捷性、即时洞察和基于消费的成本结构。此外,强制性的环境、社会和管治(ESG) 资讯揭露也迫使企业对其财务合併流程进行现代化改造。Oracle将在 2024 年超越 SAP,成为该地区最大的 ERP 应用供应商,营收将达到 87 亿美元,市占率为 6.63%(北美企业资源规划),这凸显了一级供应商之间日益激烈的竞争。美国正在持续推进州和地方系统的现代化,加拿大的数位化应用计画正在津贴製造业的 ERP 投资,墨西哥正在利用 USMCA 的数位贸易条款来简化跨境资料流。

北美企业资源规划市场趋势与洞察

快速转向云端优先 ERP 部署模式

成本、扩充性和远端工作支援正在推动本地部署的采用,使云端采用成为新 ERP 实施的常态。华盛顿州克拉克县在迁移到 Workday 后,薪资核算速度加快了 60%,核准的支出减少了 15%。混合架构仍然很常见,因为受到严格监管的公司将敏感资料保留在本地,同时在公共云端中扩展边缘和专用功能。製造公司的安全投资正在激增,订阅定价使财务团队能够将资本预算分配给策略创新,而不是硬体更新周期。资讯长(CIO) 正在优先考虑相关人员培训和技术升级,以使文化采用与架构转型保持一致。

用于即时决策的人工智慧嵌入式分析的激增

生成模型和预测模型正在将 ERP 从交易记录器再形成为智慧编配引擎。 IBM 和Oracle目前正在合作开发自主代理,为财务、供应链和人力资源工作流程推荐符合政策的行动。 NetSuite 基于机器学习的应付应付帐款流程。製造企业正在将人工智慧融入工厂级模组,以实现预测性维护,从而帮助 95% 已实施智慧工厂技术的企业减少非计画性停机时间。医疗保健提供者正在利用分析技术来协调临床数据和财务数据,以提高报销准确性和合规性报告。所有倡议都依赖强有力的管治,因为演算法偏差和陈旧数据会削弱人们对自动化决策的信任。

实施和变更管理的领先成本和生命週期成本

综合 ERP计划除了许可证和订阅费用外,还会产生各种成本。正如浸信会医疗 (Baptist Health) 历时多年的现代化改造计画所示,资料迁移、业务流程重组和员工培训费用往往使医院和公共机构的原始预算翻倍。中小企业缺乏专业的 IT 能力,因此需要外部顾问,但人才短缺意味着高昂的每日津贴和紧张的工期。云端传输虽然可以降低资本支出,但无法消除流程标准化所需的文化转变。如果没有强大的变革领导结构,昂贵的平台可能会无法充分利用,导致投资报酬率低落。

細項分析

到2024年,云端原生套件将占北美企业资源规划市场总收入的60.5%,这意味着北美企业资源规划市场拥有基准功能丰富的平台。然而,随着企业寻求消费级使用者体验,社交/协作型ERP将成长最快,到2030年的复合年增长率将达到11.4%。知识型员工将在财务和供应链交易中采用活动动态、共用仪表板和即时聊天功能,从而提高系统使用率并缩短核准週期。整合式行动应用程式将在现场和客户现场提供相同的功能,增强始终在线的工作流程。供应商蓝图越来越多地将社交元素预设捆绑,而不是作为可选模组,凸显了其战略价值。最终,内建在这些管道的人工智慧助理将推荐操作并标记异常情况,从而加深参与度和营运效率之间的连结。

到 2024 年,财务和会计将占据北美企业资源规划市场规模的 55.7%,这反映了强制性的报告和审核要求。儘管如此,供应链和营运模组仍将以 10.8% 的复合年增长率扩张。边缘运算和物联网将即时现场资料输入规划演算法,从而提高物料供给能力并降低营运成本。出货预测 ETA 支持全通路承诺,自动品质检查可降低退货率。同时,对于面临劳动力短缺和离职率上升的製造公司来说,人力资本模组是当务之急。客户商务附加附加元件将订单量与库存连结起来,从而实现准确的交货日期承诺,从而提高转换率。虽然财务仍然充当记录系统的作用,但营运资料集越来越多地推动损益结果。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 快速过渡到云端优先 ERP 部署模式

- 用于即时决策的人工智慧嵌入式分析的激增

- 实施双层 ERP 系统,协调总部与子公司之间的运营

- 中小企业对价格实惠的模组化 SaaS 套件的需求不断增长

- ESG报告要求推动系统升级

- 边缘/物联网数据集成,实现闭合迴路运营

- 市场限制

- 实施和变更管理的初始成本和生命週期成本

- 多租户云端中的网路安全和资料主权问题

- 北美ERP人才和计划能力短缺

- 内部支援週期缩短,增加了供应商锁定的风险

- 价值链分析

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章市场规模及成长预测

- 按类型

- 云端原生套件

- 行动优先 ERP

- 社交/协作 ERP

- 2层/边缘ERP

- 按业务功能

- 财会

- 供应炼和营运

- 人力资源管理

- 客户关係和商业交易

- 製造执行和品质

- 按部署模型

- 本地部署

- 云

- 按组织规模

- 大公司

- 小型企业

- 按行业

- 製造业

- 零售与电子商务

- BFSI

- 政府和公共部门

- 资讯科技和通讯

- 医疗保健和生命科学

- 其他的

- 按国家

- 美国

- 加拿大

- 墨西哥

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Workday Inc.

- Infor Inc.

- Epicor Software Corporation

- IBM Corporation

- The Sage Group plc

- Plex Systems Inc.(Rockwell Automation)

- FinancialForce.com Inc.

- Unit4 NV

- Deltek Inc.

- Deacom Inc.

- Acumatica Inc.

- IFS AB

- Syspro USA Inc.

- QAD Inc.

- Oracle NetSuite

- SAP Business One

- Odoo SA

第七章 市场机会与未来展望

The North America enterprise resource planning market size stands at USD 24.41 billion in 2025 and is projected to reach USD 39.35 billion by 2030, reflecting a sturdy 10.0% CAGR.

This expansion mirrors the region-wide migration from legacy on-premise suites to cloud-native platforms that give firms agility, real-time insights, and consumption-based cost structures. Heightened interest in AI-embedded analytics is reshaping implementation roadmaps, while mandatory environmental, social, and governance (ESG) disclosures push companies to modernize their financial consolidation processes. Oracle overtook SAP as the region's largest ERP application supplier in 2024 with USD 8.7 billion in revenue and 6.63% North America enterprise resource planning market share, underscoring a sharpening rivalry among tier-1 vendors. Governments also catalyze uptake: the United States continues to modernize state and local systems, whereas Canada's Digital Adoption Program subsidizes manufacturing ERP investments, and Mexico leverages USMCA digital-trade provisions to streamline cross-border data flows.

North America Enterprise Resource Planning Market Trends and Insights

Rapid Shift Toward Cloud-First ERP Deployment Models

Cloud adoption is now the baseline for new ERP rollouts as cost, scalability, and remote-work support eclipse entrenched on-premise preferences. Clark County, Washington, recorded 60% faster payroll runs and cut unapproved spending by 15% after moving to Workday. Hybrid architectures remain common because highly regulated firms keep sensitive data on-premise while extending edge or specialty functionality in public clouds. Security investments rose sharply in manufacturing corridors, and subscription-pricing lets finance teams reallocate capital budgets to strategic innovation rather than hardware refresh cycles. Alongside technology upgrades, chief information officers prioritize stakeholder training so cultural adoption matches architectural transformation.

Surge in AI-Embedded Analytics for Real-Time Decision-Making

Generative and predictive models are reshaping ERP from transaction recorders to intelligent orchestration engines. IBM and Oracle now co-develop autonomous agents that recommend policy-compliant actions across finance, supply chain, and HR workflows. NetSuite's machine-learning accounts-payable module reduces manual invoice entry and speeds reconciliation, easing month-end close pressure. Manufacturers embed AI in plant-level modules for predictive maintenance, driving shorter unplanned downtime across the 95% of firms that already deploy smart-factory technologies. Healthcare providers leverage analytics to reconcile clinical and financial data, improving reimbursement accuracy and compliance reporting. All initiatives rely on robust governance because algorithmic bias or stale data can erode trust in automated decisions.

Up-Front and Life-Cycle Costs of Implementation and Change-Management

Comprehensive ERP projects absorb expenses that extend well beyond license or subscription fees. Data migration, business-process re-engineering, and staff training frequently double original budgets for hospitals and public agencies, as seen in multi-year modernizations at Baptist Health. SMEs rely on external consultants because they lack dedicated IT capacity, but scarce talent drives day-rates higher and stretches timelines. Cloud delivery softens capital expenditure yet does not eliminate the cultural shifts required for process standardization. Without robust change-leadership structures, expensive platforms risk under-utilization and diminished ROI.

Other drivers and restraints analyzed in the detailed report include:

- Two-Tier ERP Adoption to Harmonize HQ and Subsidiary Operations

- Rising SMB Demand for Affordable, Modular SaaS Suites

- Cyber-Security and Data-Sovereignty Concerns in Multitenant Clouds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites accounted for 60.5% revenue in 2024, ensuring the North America enterprise resource planning market retains a strong baseline of broad-function platforms. Social/collaborative ERP, however, will grow fastest at 11.4% CAGR through 2030 as corporations seek consumer-grade user experiences. Knowledge workers adopt activity feeds, shared dashboards, and real-time chat inside finance and supply-chain transactions, lifting system usage rates and shortening approval cycles. Integrated mobile apps deliver the same capabilities at job sites or customer locations, reinforcing always-connected workflows. Vendor roadmaps increasingly bundle social elements by default rather than as optional modules, underscoring their strategic value. Over time, artificial-intelligence assistants embedded in these channels will recommend actions or flag exceptions, deepening the linkage between engagement and operational efficiency.

Finance and accounting maintained 55.7% of the North America enterprise resource planning market size in 2024, reflecting mandatory reporting and audit requirements. Nonetheless, supply-chain and operations modules will expand at a 10.8% CAGR. Edge computing and the Internet of Things feed real-time shop-floor data into planning algorithms, improving material availability and lowering working capital. Predictive shipment ETAs support omnichannel commitments, while automated quality-checks cut return rates. Human-capital modules meanwhile gain priority as manufacturers confront labour shortages and rising voluntary turnover. Customer-commerce add-ons connect order capture to inventory, letting firms promise exact delivery windows that boost conversion rates. Finance still acts as the system-of-record, but operational datasets increasingly drive profit-and-loss outcomes.

The North America Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Industry Vertical (Manufacturing, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Workday Inc.

- Infor Inc.

- Epicor Software Corporation

- IBM Corporation

- The Sage Group plc

- Plex Systems Inc. (Rockwell Automation)

- FinancialForce.com Inc.

- Unit4 NV

- Deltek Inc.

- Deacom Inc.

- Acumatica Inc.

- IFS AB

- Syspro USA Inc.

- QAD Inc.

- Oracle NetSuite

- SAP Business One

- Odoo SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift toward cloud-first ERP deployment models

- 4.2.2 Surge in AI-embedded analytics for real-time decision-making

- 4.2.3 Two-tier ERP adoption to harmonise HQ and subsidiary operations

- 4.2.4 Rising SMB demand for affordable, modular SaaS suites

- 4.2.5 ESG-linked reporting mandates accelerating system upgrades

- 4.2.6 Edge/IoT data integration for closed-loop operations

- 4.3 Market Restraints

- 4.3.1 Up-front and life-cycle costs of implementation and change-management

- 4.3.2 Cyber-security and data-sovereignty concerns in multitenant clouds

- 4.3.3 Shortage of North America-based ERP talent and project bandwidth

- 4.3.4 Vendor lock-in risk amid shrinking on-premise support windows

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cloud-native Suite

- 5.1.2 Mobile-first ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Workday Inc.

- 6.4.5 Infor Inc.

- 6.4.6 Epicor Software Corporation

- 6.4.7 IBM Corporation

- 6.4.8 The Sage Group plc

- 6.4.9 Plex Systems Inc. (Rockwell Automation)

- 6.4.10 FinancialForce.com Inc.

- 6.4.11 Unit4 NV

- 6.4.12 Deltek Inc.

- 6.4.13 Deacom Inc.

- 6.4.14 Acumatica Inc.

- 6.4.15 IFS AB

- 6.4.16 Syspro USA Inc.

- 6.4.17 QAD Inc.

- 6.4.18 Oracle NetSuite

- 6.4.19 SAP Business One

- 6.4.20 Odoo SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球ERP和ECM整合市场报告2026年企业资源规划(ERP)区块链全球市场报告

2026年全球ERP和ECM整合市场报告2026年企业资源规划(ERP)区块链全球市场报告 2026-2030年全球企业资源规划系统整合与咨询市场

2026-2030年全球企业资源规划系统整合与咨询市场 2026-2030年全球私立教育机构教育ERP市场

2026-2030年全球私立教育机构教育ERP市场 供应链ERP市场规模、份额和成长分析:依实施模式、最终用户产业、职能、组织规模和地区划分-2026-2033年产业预测

供应链ERP市场规模、份额和成长分析:依实施模式、最终用户产业、职能、组织规模和地区划分-2026-2033年产业预测 企业资源规划软体包市场按部署模式、组织规模、组件、垂直产业和服务类型划分-全球预测,2026-2032年

企业资源规划软体包市场按部署模式、组织规模、组件、垂直产业和服务类型划分-全球预测,2026-2032年 企业资源规划 (ERP) 软体市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、模组和功能划分服务资源规划 (SRP) SaaS 解决方案市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分

企业资源规划 (ERP) 软体市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、模组和功能划分服务资源规划 (SRP) SaaS 解决方案市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和解决方案划分 全球基于SaaS的企业资源规划(ERP)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球基于SaaS的企业资源规划(ERP)市场规模、份额、趋势和成长分析报告(2026-2034年) 亚太地区农业ERP市场:按应用、产品和国家分類的分析和预测(2025-2035年)

亚太地区农业ERP市场:按应用、产品和国家分類的分析和预测(2025-2035年)