|

市场调查报告书

商品编码

1849930

端点安全:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Endpoint Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

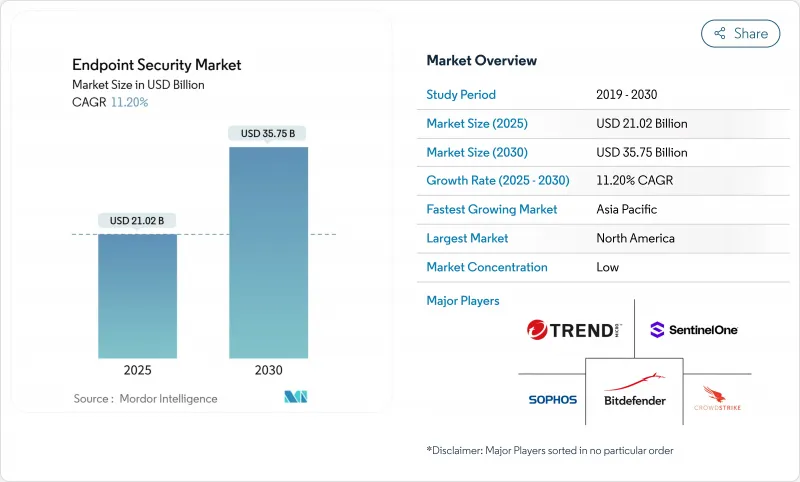

预计端点安全市场规模将在 2025 年达到 210.2 亿美元,到 2030 年达到 357.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 11.20%。

强劲的需求源于远端办公和混合办公模式的稳步转变、自带设备办公 (BYOD) 政策的扩展以及勒索软体即服务套件包的日益复杂。企业也面临物联网 (IoT) 不断扩张的威胁,这模糊了资讯科技和操作技术网路之间的界限,使关键工业资产面临与传统办公设备相同的威胁。因此,云端交付的控制、零信任存取策略和人工智慧主导的行为分析正在成为现代端点保护策略的预设组成部分。平台提供者正在透过将晶片级安全功能以及端点保护平台 (EPP) 和端点检测与回应 (EDR) 功能捆绑到其安全存取服务边缘 (SASE) 产品中来简化分散式用户的策略实施。

全球端点安全市场趋势与洞察

BYOD 和行动工作人员的激增

BYOD 政策已将约 47 亿个行动终端暴露在传统防火墙之外,推动了行动装置管理工具的快速普及,这些工具将企业资料与个人应用隔离。鑑于目前 70% 的攻击都涉及身分洩露,企业正倾向于采用零信任框架,在授予网路存取权限之前检验设备状态。高阶主管越来越多地将网路安全视为董事会层面的优先事项,91% 的高阶主管表示网路安全是一项策略资产,而非合规性问题。现代终端套件内建的人工智慧功能可执行即时行为分析,并标记多样化设备生态系统中的危险行为。

勒索软体即服务的演变

基于服务的勒索软体降低了进入门槛,导致2024年初感染数量激增50%。医疗保健产业资料外洩目前平均造成1,010万美元损失,迫使医院部署先进的侦测和回应平台,将端点和网路遥测资料关联起来。双重和三重勒索手段也针对备份,迫使企业重新考虑资料復原计画。分析师预测,到2031年,勒索软体每年造成的损失将超过2,650亿美元,这将导致主动端点防御方面的支出增加。

SOC 和事件回应团队的技能短缺

全球整体网路专业人员短缺 300 万,近一半的首席资讯安全安全长担心覆盖范围不足,因此託管检测和响应 (MDR) 的采用正在加速,预计到 2025 年,一半的组织将外包全天候监控。在人才管道改善之前,用于分类警报和脚本遏制操作的自动化和人工智慧工具被视为一种实用的权宜之计。

細項分析

端点侦测与反应产品的复合年增长率高达15.8%,轻鬆超越传统防毒工具。儘管企业倾向于使用行为分析来发现零日漏洞,但防火墙/UTM设备凭藉与现有网路设备的深度集成,仍保持着20.02%的收入份额。託管侦测与回应订阅服务也正在兴起,这类服务提供专业知识,而非自行建构内部安全营运中心。

由于 GDPR 和 NIS2 等法规要求资料保护控制得到验证,监管审查正在推动加密和预防资料外泄模组的发展。由于安全更新平均需要 97 天才能发布,暴露了攻击面,修补程式管理实用程式正在吸引投资。阻止恶意软体的应用程式控制工具有助于降低企业网路上个人装置的影子 IT 风险。

2024年,云端平台将占端点安全市场规模的58.04%,预计2030年将以每年15.2%的速度成长。集中式策略引擎可以加速部署到全球分布的设备,并即时为人工智慧模型提供大量资料。对于面临资料主权法规和专业操作技术限制的企业来说,混合架构仍然很受欢迎。

在国防和关键基础设施等强製本地处理的领域,本地部署仍然强劲。即使在这些情况下,许多团队也在采用 SASE 覆盖,将软体定义网路与云端交付安全性结合,以简化管理。云端整合的 EDR 分析功能可缩短停留时间,并增强平均回应时间统计资料。

端点安全市场按解决方案类型(防毒/反恶意软体、防火墙/UTM 等)、部署模式(本地部署、云端部署、混合部署)、组织规模(大型企业、中小型企业)、最终用户垂直领域(金融服务、保险和保险业、政府、国防、医疗保健/生命科学等)和地区进行细分。市场预测以美元计算。

区域分析

2024年,北美将维持33.5%的收入份额。充足的安全预算、先进的威胁环境以及人工智慧的早期应用,正在刺激安全领域的持续升级。政府云端安全计画和密集的供应商网路正在形成良性创新循环。

欧洲的势头与2024年10月全面实施的NIS2指令息息相关,该指令将要求超过16万家组织实施经认证的端点控制,否则将面临最高1000万欧元的罚款。这项法规对关键基础设施、製造业和数位服务供应商提出了更高的要求。

亚太地区是成长最快的地区,复合年增长率高达12.4%。该地区各国都在大力投资网路弹性框架,针对通讯业者和金融机构的重大攻击事件也加剧了经营团队的关注。中国的安全团队将API暴露列为首要关注点,27%的受访者认为API暴露比恶意软体更受重视。在政府资金投入和本地供应商生态系统的推动下,日本、韩国、澳洲和东南亚国协的网路弹性框架应用正在加速。

在中东和非洲,网路保险费的上涨和隐私法的加强,促使银行和能源供应商升级其端点管理。在拉丁美洲,零售和数位银行公司越来越多地采用云端技术,并超越传统的本地部署环境。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- BYOD 和行动工作者的激增

- 勒索软体即服务的演变

- OT 网路中 IoT 端点的激增

- 边缘采用 SASE 捆绑 EPP/EDR 的情况日益增多

- OEM整合晶片级安全IP

- 认证 EDR 的网路保险折扣

- 市场限制

- SOC 和事件回应团队的技能短缺

- 中小企业的预算限制

- 持续端点遥测引发的隐私问题日益严重

- 第三方担保代理供应链风险

- 产业价值链分析

- 监管格局

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 影响市场的宏观经济因素

第五章市场规模与成长预测(价值)

- 按解决方案类型

- 防毒/恶意软体保护

- 防火墙/UTM

- 端点检测与响应 (EDR)

- 託管侦测和回应 (MDR)

- 加密和预防资料外泄

- 补丁和配置管理

- 应用程式和设备控制

- 其他的

- 依部署方式

- 本地部署

- 云

- 杂交种

- 按组织规模

- 大公司

- 小型企业

- 按最终用户产业

- BFSI

- 政府和国防

- 医疗保健和生命科学

- 製造业

- 能源和公共产业

- 零售与电子商务

- 资讯科技和通讯

- 教育

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 其他亚太地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Trend Micro Inc.

- CrowdStrike Holdings Inc.

- SentinelOne Inc.

- Sophos Ltd.

- Bitdefender LLC

- ESET Spol. s ro

- Kaspersky Lab JSC

- Trellix(Musarubra US LLC)

- OpenText(Cybersecurity & Carbonite Unit)

- WatchGuard Technologies Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Broadcom Inc.(Symantec Endpoint)

- Microsoft Corporation(Defender for Endpoint)

- Deep Instinct Ltd

- Cybereason Inc.

- BlackBerry Ltd(Cylance)

- Malwarebytes Inc.

- AhnLab Inc.

- F-Secure Corp.

- Elastic NV(Security)

- ReaQta BV(IBM)

- Comodo Security Solutions Inc.

- Seqrite(Quick Heal Technologies)

第七章 市场机会与未来趋势

- 閒置频段和未满足需求评估

The Endpoint Security Market size is estimated at USD 21.02 billion in 2025, and is expected to reach USD 35.75 billion by 2030, at a CAGR of 11.20% during the forecast period (2025-2030).

Strong demand stems from the steady shift toward remote and hybrid work, the expansion of bring-your-own-device (BYOD) policies, and the growing sophistication of ransomware-as-a-service toolkits. Enterprises also face an expanding Internet-of-Things (IoT) footprint that blurs the line between information-technology and operational-technology networks, exposing critical industrial assets to the same threats historically aimed at office devices. Cloud-delivered controls, zero-trust access policies, and AI-driven behavioural analytics are therefore becoming default components of modern endpoint protection strategies. Platform providers are responding by embedding chip-level security features and bundling endpoint protection platform (EPP) and endpoint detection and response (EDR) capabilities into secure-access-service-edge (SASE) offerings to simplify policy enforcement across distributed users.

Global Endpoint Security Market Trends and Insights

Surge in BYOD and Mobile Workforce

BYOD policies have exposed roughly 4.7 billion mobile endpoints that sit outside traditional firewalls, prompting rapid deployment of mobile-device-management tools that partition corporate data from personal apps. Identity compromise now appears in 70% of attacks, so firms lean on zero-trust frameworks that verify device posture before allowing network access. Executives increasingly view cybersecurity as a board-level priority, with 91% describing it as a strategic asset rather than a compliance exercise. AI features embedded in modern endpoint suites perform real-time behavioural analysis to flag risky actions across a diverse device ecosystem.

Escalating Sophistication of Ransomware-as-a-Service

Service-based ransomware lowered the barrier to entry, triggering a 50% spike in infections during early 2024. Healthcare breaches now cost USD 10.1 million on average, forcing hospitals to adopt extended-detection-and-response platforms that correlate endpoint and network telemetry. Double- and triple-extortion tactics also target backups, compelling enterprises to redesign data-recovery plans. Analysts expect ransomware damage to surpass USD 265 billion annually by 2031, funnelling more spend into proactive endpoint defences.

Skill Shortage in SOC and Incident-Response Teams

The global deficit of 3 million cyber professionals leaves roughly half of chief information security officers anxious about coverage gaps. Managed-detection-and-response (MDR) uptake is therefore accelerating, with half of organizations expected to outsource 24/7 monitoring by 2025. Automation and AI tools that triage alerts and script containment actions are seen as practical stopgaps until the workforce pipeline improves.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IoT Endpoints Across OT Networks

- Wider Adoption of SASE Bundling EPP/EDR at Edge

- Budget Constraints Among SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endpoint detection and response products are expanding at 15.8% CAGR, easily eclipsing legacy antivirus tools. Organizations favour behaviour analytics that spotlight zero-day exploits, while firewall/UTM appliances retain 20.02% revenue share thanks to deep integration with existing network gear. Managed-detection-and-response subscriptions are also gaining ground as firms lease expertise rather than build internal security operations centres.

Regulatory scrutiny is breathing life into encryption and data-loss-prevention modules as rules such as GDPR and NIS2 demand demonstrable data-protection controls. Patch-management utilities attract spend because security updates still average a 97-day rollout window, leaving attack surfaces exposed. Application-control tools that block unauthorized software help limit shadow-IT risks for personal devices on corporate networks.

Cloud platforms already command 58.04% of the endpoint security market size in 2024 and will compound 15.2% annually to 2030. Centralized policy engines accelerate rollout across globally distributed devices and feed AI models with large data volumes in real time. Hybrid architectures remain popular for firms facing data-sovereignty rules or specialist operational-technology constraints.

On-premises deployments persist in defence and critical-infrastructure verticals where local processing is mandated. Even there, many teams adopt SASE overlays that couple software-defined networking with cloud-delivered security to simplify administration. Integrated EDR analytics in the cloud reduce dwell time and enhance mean-time-to-respond statistics.

Endpoint Security Market is Segmented by Solution Type (Antivirus/Anti-malware, Firewall/UTM, and More), Deployment Mode (On-Premises, Cloud, and Hybrid), Organization Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Government and Defense, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 33.5% revenue share in 2024. Deep security budgets, an advanced threat landscape, and early AI adoption fuel ongoing upgrades. Government cloud-security programs and a dense network of vendors create a virtuous innovation cycle.

Europe's momentum is tied to the full enforcement of the NIS2 directive in October 2024, which compels more than 160,000 organizations to deploy certified endpoint controls or face fines up to EUR 10 million. The regulation keeps demand high across critical infrastructure, manufacturing, and digital services providers.

Asia-Pacific is the fastest-growing territory at 12.4% CAGR. Nations across the region pour investment into cyber-resilience frameworks, and high-profile attacks on telecoms and financial institutions have sharpened executive focus. Chinese security teams rank API exposure as their top concern, with 27% putting it ahead of malware. Government funding and local vendor ecosystems accelerate adoption across Japan, South Korea, Australia, and the ASEAN bloc.

The Middle East and Africa notice rising cyber-insurance premiums and tougher privacy laws, nudging banks and energy operators to upgrade endpoint controls. Latin America expands cloud deployments that leapfrog legacy on-premises estates, particularly in retail and digital-banking firms.

- Trend Micro Inc.

- CrowdStrike Holdings Inc.

- SentinelOne Inc.

- Sophos Ltd.

- Bitdefender LLC

- ESET Spol. s r.o.

- Kaspersky Lab JSC

- Trellix (Musarubra US LLC)

- OpenText (Cybersecurity & Carbonite Unit)

- WatchGuard Technologies Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Broadcom Inc. (Symantec Endpoint)

- Microsoft Corporation (Defender for Endpoint)

- Deep Instinct Ltd

- Cybereason Inc.

- BlackBerry Ltd (Cylance)

- Malwarebytes Inc.

- AhnLab Inc.

- F-Secure Corp.

- Elastic NV (Security)

- ReaQta BV (IBM)

- Comodo Security Solutions Inc.

- Seqrite (Quick Heal Technologies)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in BYOD and mobile workforce

- 4.2.2 Escalating sophistication of ransomware-as-a-service

- 4.2.3 Proliferation of IoT endpoints across OT networks

- 4.2.4 Wider adoption of SASE bundling EPP/EDR at edge

- 4.2.5 Chip-level security IP integrated by OEMs

- 4.2.6 Cyber-insurance premium discounts for certified EDR

- 4.3 Market Restraints

- 4.3.1 Skill shortage in SOC & incident-response teams

- 4.3.2 Budget constraints among SMBs

- 4.3.3 Rising privacy backlash against continuous endpoint telemetry

- 4.3.4 Supply-chain risk of third-party security agents

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Solution Type

- 5.1.1 Antivirus / Anti-malware

- 5.1.2 Firewall / UTM

- 5.1.3 Endpoint Detection and Response (EDR)

- 5.1.4 Managed Detection and Response (MDR)

- 5.1.5 Encryption and Data Loss Prevention

- 5.1.6 Patch and Configuration Management

- 5.1.7 Application and Device Control

- 5.1.8 Others

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SME)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Energy and Utilities

- 5.4.6 Retail and e-Commerce

- 5.4.7 IT and Telecom

- 5.4.8 Education

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Malaysia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Trend Micro Inc.

- 6.4.2 CrowdStrike Holdings Inc.

- 6.4.3 SentinelOne Inc.

- 6.4.4 Sophos Ltd.

- 6.4.5 Bitdefender LLC

- 6.4.6 ESET Spol. s r.o.

- 6.4.7 Kaspersky Lab JSC

- 6.4.8 Trellix (Musarubra US LLC)

- 6.4.9 OpenText (Cybersecurity & Carbonite Unit)

- 6.4.10 WatchGuard Technologies Inc.

- 6.4.11 Fortinet Inc.

- 6.4.12 Cisco Systems Inc.

- 6.4.13 Palo Alto Networks Inc.

- 6.4.14 Broadcom Inc. (Symantec Endpoint)

- 6.4.15 Microsoft Corporation (Defender for Endpoint)

- 6.4.16 Deep Instinct Ltd

- 6.4.17 Cybereason Inc.

- 6.4.18 BlackBerry Ltd (Cylance)

- 6.4.19 Malwarebytes Inc.

- 6.4.20 AhnLab Inc.

- 6.4.21 F-Secure Corp.

- 6.4.22 Elastic NV (Security)

- 6.4.23 ReaQta BV (IBM)

- 6.4.24 Comodo Security Solutions Inc.

- 6.4.25 Seqrite (Quick Heal Technologies)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

终端安全市场:依组件、应用点(工作站、行动装置、伺服器、POS终端)、部署类型、产业规模和最终用户(航空航太与国防、政府、银行与金融保险、医疗保健、製造业) - 至2036年的全球预测

终端安全市场:依组件、应用点(工作站、行动装置、伺服器、POS终端)、部署类型、产业规模和最终用户(航空航太与国防、政府、银行与金融保险、医疗保健、製造业) - 至2036年的全球预测 端点安全市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

端点安全市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 全球终端安全市场规模、份额、趋势和成长分析报告(2026-2034)

全球终端安全市场规模、份额、趋势和成长分析报告(2026-2034) 终端安全市场 - 全球产业规模、份额、趋势、机会和预测(按解决方案、部署模式、组织规模、最终用户、地区和竞争格局划分,2021-2031 年)

终端安全市场 - 全球产业规模、份额、趋势、机会和预测(按解决方案、部署模式、组织规模、最终用户、地区和竞争格局划分,2021-2031 年) 全球终端安全市场:依组件、部署类型、组织规模、垂直行业和地区划分 - 市场规模、行业动态、机会分析和预测(2026-2035年)终端安全市场 - 2026-2031 年预测

全球终端安全市场:依组件、部署类型、组织规模、垂直行业和地区划分 - 市场规模、行业动态、机会分析和预测(2026-2035年)终端安全市场 - 2026-2031 年预测 日本终端安全市场报告:按组件、部署类型、组织规模、产业和地区划分(2026-2034 年)

日本终端安全市场报告:按组件、部署类型、组织规模、产业和地区划分(2026-2034 年) 端点安全市场规模、份额和成长分析(按解决方案、服务、部署类型、组织规模、垂直产业和地区划分)-2026-2033年产业预测

端点安全市场规模、份额和成长分析(按解决方案、服务、部署类型、组织规模、垂直产业和地区划分)-2026-2033年产业预测 终端备份软体:全球市场占有率和排名、总收入和需求预测(2025-2031年)

终端备份软体:全球市场占有率和排名、总收入和需求预测(2025-2031年) 终端安全市场(按产品、作业系统、应用程式、最终用户、部署和组织规模)—2025-2030 年全球预测

终端安全市场(按产品、作业系统、应用程式、最终用户、部署和组织规模)—2025-2030 年全球预测