|

市场调查报告书

商品编码

1849961

零售中的手势姿态辨识:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)Gesture Recognition In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

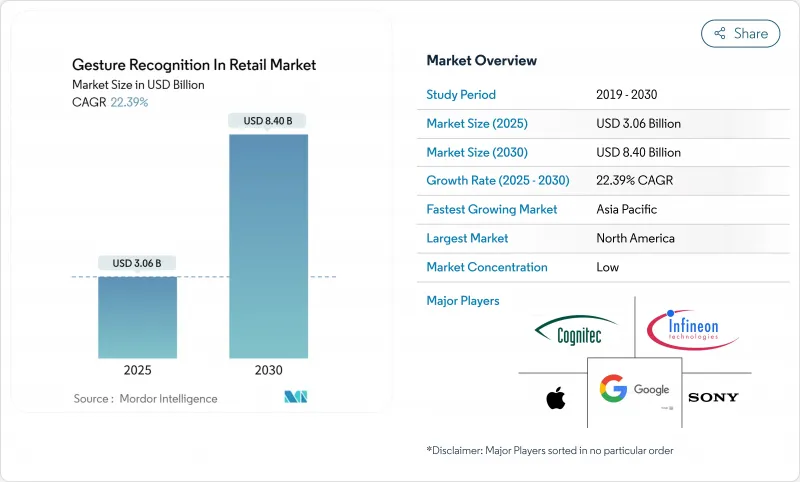

零售手势姿态辨识市场预计在 2025 年达到 30.6 亿美元,到 2030 年将成长到 84 亿美元,复合年增长率为 22.4%。

日益严重的人手不足、持续增长的非接触式出行需求,以及边缘人工智慧 (AI) 与毫米波雷达的结合,使得无需摄影机即可在货架上进行手势识别。零售商获得了更丰富的货架内分析数据,而消费品品牌则可以将由此产生的行为数据收益。随着 3D 感测和 AI 晶片组被整合到主流 POS 设备中,硬体成本持续下降。主要市场的监管明确性和日益成熟的隐私保护架构进一步降低了大规模部署的风险。综合来看,这些动态将使零售手势姿态辨识市场在未来十年保持两位数的成长。

全球零售手势姿态辨识市场趋势与洞察

非接触式购物体验的需求不断增加

疫情期间的消费行为巩固了消费者对无接触购物的期望。一家欧洲大型杂货店检验一家占地超过1000平方米的全尺寸电脑视觉超级市场。该零售商报告称,平均结帐时间显着缩短,顾客吞吐量提升,从而增加了购物量并增加了回头客。竞争压力甚至促使中阶连锁店也在评估支援手势辨识的前端重新设计。随着越来越多的营运商采用保护隐私的边缘架构,该技术的普及将在无需额外云端费用的情况下加速。这些发展增强了手势姿态辨识在零售市场的短期成长前景。

3D 感测和 AI 晶片在零售设备中的应用日益增多

边缘晶片如今可在本地执行即时手势推理,从而消除频宽限制并降低延迟。近期推出的原型产品将3D深度感测器与专用机器学习核心结合,即使在不同的光照条件下,也能在18个类别中实现99.8%的手势辨识准确率。凭藉大规模生产,亚洲OEM厂商正将单位成本降至20美元以下,从而进军本地杂货店和便利商店。由于拥有成本较低且易于改造现有通道,零售手势姿态辨识市场正在不断扩张。此外,晶片供应商和解决方案整合商提供的联合参考设计,为内部工程资源有限的零售商减少了整合工作量。

即时商店环境中演算法的复杂性和准确性变化

与实验室结果相比,零售环境中的遮蔽、反射表面和人群密度会降低手势辨识的准确性。电脑视觉模型仍然存在基于年龄层和移动性的偏差,这引发了包容性方面的担忧。持续的再训练和更大的註释资料集增加了部署成本。商家必须根据每家门市调整感测器布局以保持可接受的性能,这使得多格式部署变得复杂。在中介软体平台能够抽象化这些复杂性之前,一些连锁店仍持谨慎态度,这限制了零售手势姿态辨识市场的短期扩张。

細項分析

到2024年,触控平台将占据零售手势姿态辨识市场份额的78.1%。然而,预计到2030年,非接触式平台的复合年增长率将达到24.1%,这标誌着人们将转向更卫生、无缝整合的购物体验。一家大型俱乐部在出口处试点使用摄影机辨识技术为会员结帐,这表明非接触式技术正在取代人工收据检查。硬体供应商现在正在将雷达感测器与RGB-D摄影机集成,以降低材料成本,并填补曾经青睐触控面板的精度差距。随着应用越来越可靠,预计到2030年,零售业中与非接触式产品相关的手势姿态辨识市场规模将超过30亿美元,是2024年规模的两倍。

零售商越来越多地将非接触式手势姿态辨识视为提升品牌体验的差异化因素,尤其是在奢侈品时尚和消费性电子产品展示室等高利润领域。同时,基于触控的平台仍然适用于需要精确定位的用例,例如手势识别和按订单订单的自助服务终端。这两种方式代表着一种共存模式,而非完全替代,这使得供应商能够定位可根据客户需求扩展的模组化解决方案。神经处理单元的持续改进将使延迟降低到30毫秒以下,同时保持直观的互动,并有望进一步渗透零售领域的手势姿态辨识市场。

手部和手指输入仍占据主导地位,占2024年手势姿态辨识市场规模的66.8%。然而,到2030年,全身系统的复合年增长率将达到23.4%,因为边缘盒中的高速GPU可以解码骨骼运动,以实现身临其境型显示墙和过道级分析。以头部为中心的微手势技术已在便利商店和加油站率先采用。结合语音和手势的研究原型在意图准确度方面取得了更高的分数,这表明零售手势姿态辨识市场将呈现多模态轨迹。

穿戴式腕带能够捕捉神经和肌肉讯号,为身心障碍购物者带来全新的互动,拓展了无障碍消费者的可及性。零售商正在利用全身热力图识别热点并重新设计货架,这表明手势数据可以释放前端结帐以外的营运价值。用例范围的不断扩大凸显了为什么儘管需要强大的运算能力,但业界仍在持续投资先进的姿势估算演算法。

区域分析

到2024年,北美将占据零售手势姿态辨识市场规模的36.5%,这得益于早期采用该技术的大型连锁店和相对宽鬆的生物辨识制度。联邦指导方针不如欧洲严格,允许在全连锁店范围内进行试点,一旦投资回报率得到验证,即可迅速扩大规模。目前,已有超过500家杂货店采用仅使用摄影机的出口结帐系统,这巩固了该地区的领先地位。

随着中国的支付生态系统和日本的无人驾驶营运将手势姿态辨识融入端到端的门市自动化,到2030年,亚太地区将达到最高的复合年增长率,达到22.8%。政府对数位化的补贴降低了初始成本门槛,同时提高了消费者对生物辨识流程的接受度。本地硬体製造密度的提高将缩短供应链并加快迭代周期,从而进一步推动生物辨识技术的普及。

在欧洲,为了满足欧盟人工智慧立法的要求,人们正在采用融合边缘处理和加密云端同步的隐私合规架构。跨国杂货商正在德国、法国和北欧测试支援手势识别的大型超市,为在欧盟范围内推广提供蓝图。拉丁美洲和中东等新兴地区的起步基数较小,但随着全球供应商推出针对中型超级市场集团的承包方案,预计这些地区的采用率将达到两位数。这些连锁效应正在使零售业的手势姿态辨识市场在地理分布上更加多样化。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 非接触式购物体验的需求不断增加

- 零售设备中的 3D 感测和 AI 晶片越来越普遍

- 智慧零售与自主商店模式的兴起

- 毫米波和超宽频雷达的进步使手势控製成为可能

- 消费品品牌透过过道手势姿态分析收益

- AR智慧眼镜整合连接线上和店内购物体验

- 市场限制

- 实体环境中演算法的复杂性与准确性变化

- 隐私和监管对持续视觉追踪的强烈反对

- 边缘网路延迟导致结帐手势失灵

- 门市物联网密集部署带来的电磁干扰

- 价值链分析

- 监管格局

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

- 评估宏观经济趋势对市场的影响

第五章市场规模及成长预测

- 依技术

- 基于触摸的手势姿态辨识

- 非接触式手势姿态辨识

- 按互动方式

- 手势和手指

- 头部/点头手势

- 全身手势

- 多模态(手势和语音)

- 按功能

- 店内客户参与展示

- 结帐/销售点和付款

- 商店营运、库存和分析

- 按零售形式

- 超级市场和大卖场

- 便利商店

- 服装和百货公司

- 专业零售商

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Apple Inc

- Google LLC

- Microsoft Corporation

- Intel Corporation

- Infineon Technologies AG

- Sony Group Corp

- Omron Corporation

- Cognitec Systems GmbH

- Crunchfish AB

- Elliptic Labs ASA

- GestureTek Inc

- Ultraleap Ltd

- Synaptics Incorporated

- Qualcomm Technologies Inc

- PointGrab Ltd

- Neonode Inc

- Cipia Vision Ltd

- Samsung Electronics Co Ltd

- Microchip Technology Inc

- STMicroelectronics NV

第七章 市场机会与未来展望

The gesture recognition in retail market size reached USD 3.06 billion in 2025 and is forecast to climb to USD 8.40 billion by 2030, advancing at a 22.4% CAGR.

Rising labor shortages, sustained demand for contact-free journeys, and the pairing of edge AI with millimeter-wave radar now allow through-shelf gesture detection that works without a direct camera view. Retailers gain richer in-aisle analytics, while consumer packaged goods brands monetize the resulting behavioral data streams. Hardware costs continue to fall as 3-D sensing and AI chipsets integrate into mainstream point-of-sale devices. Regulatory clarity in major markets and maturing privacy-preserving architectures further de-risk large-scale roll-outs. Collectively, these dynamics support sustained double-digit expansion for the gesture recognition in retail market through the decade.

Global Gesture Recognition In Retail Market Trends and Insights

Rising Demand for Contact-Free Shopping Experiences

Pandemic-era behaviors solidified consumer expectations for touchless journeys, and major European grocers have validated full-scale computer-vision supermarkets exceeding 1,000 m2 footprints. Retailers report measurable reductions in average checkout time and greater customer throughput, translating into higher basket sizes and repeat visits. Competitive pressure now pushes even mid-tier chains to evaluate gesture-enabled front-end redesigns. As more operators deploy privacy-preserving edge architectures, adoption accelerates without added cloud fees. These developments reinforce the near-term growth outlook for the gesture recognition in retail market.

Increasing Penetration of 3-D Sensing and AI Chips in Retail Devices

Edge silicon now executes real-time gesture inference locally, removing bandwidth constraints and cutting latency. Recent prototypes pairing 3-D depth sensors with dedicated machine-learning cores showed 99.8% gesture accuracy across 18 classes, even under variable lighting. Asian OEMs leverage scale manufacturing to push unit prices below USD 20, opening access for regional grocers and convenience stores. Lower cost of ownership and ease of retrofitting existing lanes help broaden the reachable base of the gesture recognition in retail market. Joint reference designs from chip suppliers and solution integrators also reduce integration effort for retailers with limited in-house engineering talent.

Algorithmic Complexity and Accuracy Variance in Live-Store Environments

Retail settings introduce occlusions, reflective surfaces, and crowd density that cut gesture accuracy when compared with lab results, particularly for customers carrying bags or wearing gloves. Bias across age groups and body mobility still appears in computer-vision models, raising inclusion concerns. Continuous re-training regimes and larger annotated data sets drive deployment cost upward. Merchants must tune sensor layouts per store to preserve acceptable performance, complicating multi-format roll-outs. Until middleware platforms abstract this complexity, some chains remain cautious, tempering the short-term expansion of the gesture recognition in retail market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart-Retail and Autonomous-Store Formats

- Advancements in mm-wave and UWB Radar Enabling Through-Shelf Gestures

- Privacy and Regulatory Push-Back on Continuous Vision Tracking

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Touch-based platforms represented 78.1% of gesture recognition in retail market share in 2024 as retailers favored proven systems bolted onto legacy lanes. Even so, the touch-less segment is set to record a 24.1% CAGR through 2030, underscoring a shift toward hygienic and seamlessly integrated store journeys. Pilots by big-box clubs that clear members via camera recognition at exits illustrate how touch-less can replace manual receipt checks. Hardware vendors now integrate radar sensors alongside RGB-D cameras, trimming bill-of-materials and closing the precision gap that once favored touch-based panels. As deployment confidence rises, the gesture recognition in retail market size tied to touch-less offerings is projected to exceed USD 3 billion by 2030, doubling its 2024 base.

Retailers increasingly view touch-less gesture recognition as a brand differentiator that elevates experience, especially in high-margin segments such as luxury fashion and consumer electronics showrooms. Meanwhile, touch-based platforms remain relevant for use cases that demand pinpoint accuracy, such as signature capture or build-to-order kiosks. Those dual pathways indicate a coexistence model rather than outright substitution, allowing suppliers to position modular solutions that scale with client needs. Continued iterations of neural processing units will likely lower latency to sub-30 milliseconds, preserving intuitive interactions and encouraging further penetration of the gesture recognition in retail market.

Hand and finger inputs dominated, accounting for 66.8% of the gesture recognition in retail market size in 2024, thanks to consumers already conditioned by smartphones. Full-body systems, however, register a 23.4% CAGR to 2030 as faster GPUs in edge boxes decode skeletal movement for immersive display walls and aisle-level analytics. Head-centric micro-gestures found early adoption in convenience stores and petrol marts where hands are busy handling goods. Research prototypes combining voice and gesture score higher for intent accuracy, implying a multimodal trajectory for the gesture recognition in retail market.

Wearable bands that pick up neural or muscle signals bring an additional interaction layer for differently abled shoppers, broadening accessibility. Retailers use full-body heat maps to pinpoint hotspots and redesign aisles, demonstrating that gesture data can unlock operations value beyond front-end checkout. The expanding use-case set underscores why the gesture recognition in retail industry continues to invest in advanced pose estimation algorithms despite the higher compute requirement.

The Gesture Recognition in Retail Market Report is Segmented by Technology (Touch-Based Gesture Recognition and Touch-Less Gesture Recognition), Interaction Mode (Hand and Finger Gestures, Head / Nod Gestures, and More), Function (In-Store Customer Engagement Displays, and More), Retail Format (Supermarkets and Hypermarkets, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America, with 36.5% share of the gesture recognition in retail market size in 2024, benefits from early adopter big-box chains and a comparatively permissive biometric regime. Federal guidelines remain less restrictive than Europe's, enabling chain-wide pilots that rapidly scale when ROI is proven. Over 500 grocery sites now run camera-only exit checkout, reinforcing the region's leadership.

Asia-Pacific posts the highest 22.8% CAGR through 2030 as Chinese payment ecosystems and Japanese unmanned formats integrate gesture recognition into end-to-end store automation. Government retail-digitization grants lower upfront cost barriers, while consumers show strong acceptance of biometric processes. Local hardware manufacturing density shortens supply chains and accelerates iteration cycles, further catalyzing uptake.

Europe follows with privacy-compliant architectures that blend edge processing and encrypted cloud synchronization to satisfy the EU AI Act. Multinational grocers test gesture-enabled mega-stores across Germany, France, and the Nordics, providing blueprints for pan-EU roll-outs. Emerging regions in Latin America and the Middle East start from smaller bases but see double-digit adoption as global vendors introduce turnkey packages targeted at mid-sized supermarket groups. This cascade effect supports a geographically diversified enlargement of the gesture recognition in retail market.

- Apple Inc

- Google LLC

- Microsoft Corporation

- Intel Corporation

- Infineon Technologies AG

- Sony Group Corp

- Omron Corporation

- Cognitec Systems GmbH

- Crunchfish AB

- Elliptic Labs ASA

- GestureTek Inc

- Ultraleap Ltd

- Synaptics Incorporated

- Qualcomm Technologies Inc

- PointGrab Ltd

- Neonode Inc

- Cipia Vision Ltd

- Samsung Electronics Co Ltd

- Microchip Technology Inc

- STMicroelectronics N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for contact-free shopping experiences

- 4.2.2 Increasing penetration of 3-D sensing and AI chips in retail devices

- 4.2.3 Expansion of smart-retail and autonomous-store formats

- 4.2.4 Advancements in mm-wave and UWB radar enabling through-shelf gestures

- 4.2.5 Monetisation of in-aisle gesture analytics for CPG brands

- 4.2.6 Integration of AR smart-glasses bridging online and in-store journeys

- 4.3 Market Restraints

- 4.3.1 Algorithmic complexity and accuracy variance in live-store environments

- 4.3.2 Privacy and regulatory push-back on continuous vision tracking

- 4.3.3 Edge-network latency causing gesture misfires at checkout

- 4.3.4 Electromagnetic interference from dense in-store IoT deployments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Touch-based Gesture Recognition

- 5.1.2 Touch-less Gesture Recognition

- 5.2 By Interaction Mode

- 5.2.1 Hand and Finger Gestures

- 5.2.2 Head / Nod Gestures

- 5.2.3 Full-Body Gestures

- 5.2.4 Multimodal (Gesture and Voice)

- 5.3 By Function

- 5.3.1 In-Store Customer Engagement Displays

- 5.3.2 Checkout / Point-of-Sale and Payments

- 5.3.3 Store Operations, Inventory and Analytics

- 5.4 By Retail Format

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Apparel and Department Stores

- 5.4.4 Specialty Retailers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 Intel Corporation

- 6.4.5 Infineon Technologies AG

- 6.4.6 Sony Group Corp

- 6.4.7 Omron Corporation

- 6.4.8 Cognitec Systems GmbH

- 6.4.9 Crunchfish AB

- 6.4.10 Elliptic Labs ASA

- 6.4.11 GestureTek Inc

- 6.4.12 Ultraleap Ltd

- 6.4.13 Synaptics Incorporated

- 6.4.14 Qualcomm Technologies Inc

- 6.4.15 PointGrab Ltd

- 6.4.16 Neonode Inc

- 6.4.17 Cipia Vision Ltd

- 6.4.18 Samsung Electronics Co Ltd

- 6.4.19 Microchip Technology Inc

- 6.4.20 STMicroelectronics N.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

手势姿态辨识与非接触式感测市场:依技术、组件、应用、终端用户产业及外形规格-2025-2032年全球预测手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-2032汽车手势姿态辨识系统市场(依最终用户、车辆类型、组件、技术和应用划分)-2025-2032年全球预测

手势姿态辨识与非接触式感测市场:依技术、组件、应用、终端用户产业及外形规格-2025-2032年全球预测手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-2032汽车手势姿态辨识系统市场(依最终用户、车辆类型、组件、技术和应用划分)-2025-2032年全球预测 2025年手势姿态辨识与非接触式感应全球市场报告

2025年手势姿态辨识与非接触式感应全球市场报告 2032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析

2032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析 手势姿态辨识和非接触式感应市场规模、份额和成长分析(按技术、组织规模、应用、最终用户和地区):产业预测(2025-2032)

手势姿态辨识和非接触式感应市场规模、份额和成长分析(按技术、组织规模、应用、最终用户和地区):产业预测(2025-2032) 手势辨识和非接触式感测市场,按产品类型、按技术、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

手势辨识和非接触式感测市场,按产品类型、按技术、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年

手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年 智慧型电视手势姿态辨识市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

智慧型电视手势姿态辨识市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 手势姿态辨识:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

手势姿态辨识:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)