|

市场调查报告书

商品编码

1850081

智慧型穿戴装置:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Smart Wearable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

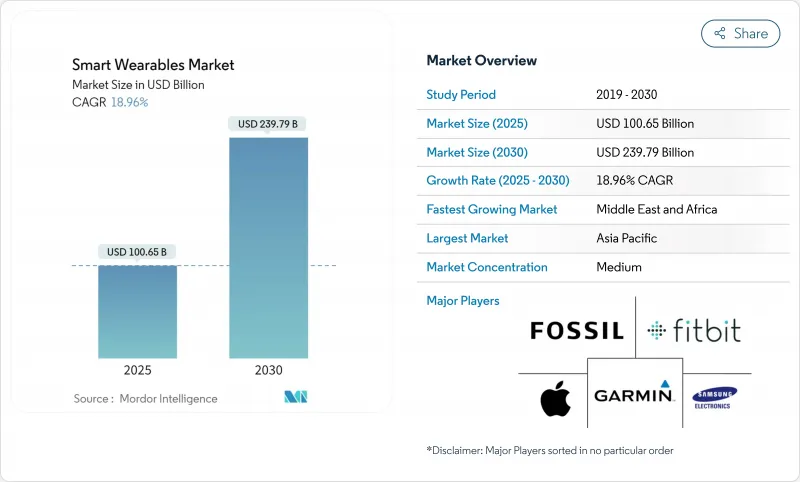

预计到 2025 年智慧穿戴装置市场规模将达到 1,006.5 亿美元,到 2030 年将达到 2,397.9 亿美元,复合年增长率为 18.96%。

感测器创新加速、设备端人工智慧改进以及行动电话用例的不断扩展,正在将用例从休閒健康扩展到受监管的医疗保健。远端监控保险报销额度的提高、企业安全要求的不断提高以及 5G 独立部署的不断推进,正在开闢新的潜在细分市场。虽然硬体仍然占据主导地位,但经常性服务收入正在重塑供应商的经济效益。在整个智慧穿戴装置市场,以平台为中心的策略和跨装置生态系统正在成为用户留存和终身价值的驱动力。

全球智慧穿戴装置市场趋势与洞察

用于心臟远端监测的可穿戴设备在北美获得保险核准

2025年医师收费标准中远端患者监护规范的快速采用,正在推动基层医疗诊所开立心电图级穿戴装置的处方。每位患者每月15至110美元的报销额度降低了医疗服务提供者的成本门槛,医院报告称,郁血性心臟衰竭入院率降低了15%。近三分之一的美国诊所已将持续监测纳入其慢性病照护工作流程,反映出资料收集方式从偶发性到纵向的显着转变。由于不受束缚的外形规格和即时的临床医生回馈机制,患者用药依从性得到提高,这进一步增强了智慧型穿戴装置市场的成长前景。

「健康中国2030」规划下的两用智慧型手錶补贴计划

政府推出的奖励措施,对经认证兼俱生活和医疗功能的设备提供部分零售价返还,正在刺激本地研发和国内需求。小米和华为等品牌已利用该计划扩大出货量,并加快了血氧饱和度 (SpO2) 级感测器和心律不整侦测演算法的上市时间。该政策也协调了消费性电子产品和医疗设备的标准,减少了亚太市场出口的监管摩擦。

资料驻留要求限制欧洲的云端伴侣应用

欧盟监管机构目前规定医疗资料必须存放在区域范围内,这迫使供应商建构本地处理堆栈,否则将面临功能降级的风险。中小企业面临合规成本上升的风险,而使用者共用敏感资料的意愿仍然较低,这限制了网路效应的效益。分散化的架构可能导致较长的更新周期和复杂的跨区域发布,从而限制了欧洲智慧穿戴装置市场的短期扩张。

細項分析

智慧型手錶将在2024年保持领先地位,销售额占比达46.5%。旗舰机型将多频段GPS、心电图和医疗级光电血压监测功能与低温多晶硅OLED面板结合,以延长电池寿命。双感测器阵列支持符合FDA II类要求的心房颤动警报,增强了智慧穿戴市场临床效用的提案。

由于微型 MCU 封装和固态电池以 3 克的外形规格支援连续的 SpO2 和心率跟踪,智慧戒指和珠宝将实现最快的增长。高阶型号瞄准睡眠优化,而大众市场型号则强调不引人注目的活动记录。可听设备将透过整合温度和认知负荷感测器来拓宽该类别的覆盖范围,为职场安全计画创建音讯优先的网关。健身追踪器将发展成为恢復分析和基于 VO2 的训练准备,而头戴式显示器将在手术指导和现场维护方面获得关注。早期的智慧纺织品结合了可拉伸电极,用于姿势矫正和压力检测,这预示着智慧穿戴式装置市场未来将扩展到日常穿戴领域。

2024年,核心硅片、光学模组和电池将占总收入的74.1%。供应商开发了具有神经加速功能的6奈米晶片组,可实现心律不整和血氧异常的设备内分类。柔性AMOLED面板和低损耗射频前端提高了效率,使旗舰手錶的单次充电续航时间延长至7天。

在高级分析、个人化指导和电子健康檔案 (EHR) 整合的推动下,订阅服务蓬勃发展。供应商将基于人工智慧的睡眠改善计划和营养指导捆绑到月费中,从而提高了每位用户平均收益,并平滑了升级週期。软体仍然是黏合层,支援无线增强功能,从而延长设备使用寿命,并增强智慧型穿戴装置市场的生态系统锁定。

区域分析

2024年,亚太地区将占销售额的34.9%。垂直整合的供应链能够快速降低成本,并每两个月更新一次型号。政府对心电图穿戴装置的补助计画将推动首次购买者和慢性疾病患者的普及。

北美仍然是高端市场的中心,这得益于早期医疗认证和强大的支付方参与。远端患者监护的保险报销扩大了设备的普及范围,机构调查检验了预测模型,增强了人们对智慧型穿戴装置市场的信心。

欧洲正在平衡强劲的需求和严格的资料主权规则,供应商部署边缘特定分析和区域资料湖以遵守 GDPR,而企业安全要求则加速可听设备的部署。

中东和非洲的复合年增长率最高,达到20.7%,这得益于5G的高普及率以及国家电子医疗蓝图,这些蓝图利用穿戴式装置将医疗服务扩展到服务匮乏的社区。由于外汇波动和5G成本,南美洲的普及率将不均衡,但在地化伙伴关係和健康补贴正在推动巴西和墨西哥的发展。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 北美地区保险核准的心臟远距监护穿戴设备

- 中国透过「健康中国2030」计画对两用(消费+医疗)智慧型手錶进行补贴

- 欧盟混合工作安全标准推动企业采用可听设备(后疫情时代)

- 用于无针连续血糖值监测的晶片人工智慧穿戴装置的兴起

- 美国士兵杀伤力计画下的国防外骨骼采购

- 东南亚建筑业的计量型付费工业外骨骼租赁

- 市场限制

- 欧洲的资料驻留规定限制了云端配套应用

- 超薄智慧型手錶手錶高密度电池引发热失控担忧

- 与手势智慧戒指相关的专利许可诉讼费用

- 拉丁美洲较低的 ARPU 将限制 5G 独立穿戴式装置的部署

- 产业生态系统分析

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资与资金筹措分析

第五章市场规模与成长预测(价值)

- 按产品

- 智慧型手錶

- 可听设备(戴在耳朵里的智慧耳机)

- 健身和活动追踪器

- 头戴式显示器(AR/VR/MR)

- 智慧服饰和纺织品

- 随身摄影机

- 智慧戒指和珠宝

- 穿戴式医疗贴片和生物感测器

- 动力外骨骼

- 按组件

- 硬体

- 软体和应用程式

- 服务和订阅

- 透过连接技术

- Bluetooth

- 蜂窝网路 (3G/4G/LTE-M)

- 5G独立组网

- NFC/RFID

- Wi-Fi/无线区域网

- 其他(UWB、ANT+)

- 按用途

- 家电与生活方式

- 医疗保健和医学

- 健身与运动

- 工业和企业安全

- 军事和国防

- 按分销管道

- 线上(品牌电子商店、市场)

- 线下(电子产品量贩店、专卖店、诊所)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 东南亚

- 其他亚太地区

- 南美洲

- 巴西

- 南美洲其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Apple Inc.

- Samsung Electronics Co. Ltd

- Alphabet Inc.(Fitbit and Google Pixel)

- Garmin Ltd

- Huawei Technologies Co. Ltd

- Xiaomi Corp.

- BOBOVR

- Sony Corp.

- Microsoft Corp.

- Meta Platforms Inc.(Oculus)

- Huami Corp.(Zepp Health)

- Withings SA

- Omron Healthcare Inc.

- Cyberdyne Inc.

- Ekso Bionics Holdings Inc.

- GoPro Inc.

- Fossil Group Inc.

- Nuheara Ltd.

- Bragi GmbH

- Sensoria Inc.

- AIQ Smart Clothing Inc.

- Polar Electro Oy

- Coros Wearables Inc.

第七章 市场机会与未来展望

The smart wearable market size stands at USD 100.65 billion in 2025 and is forecast to reach USD 239.79 billion by 2030, advancing at an 18.96% CAGR.

Accelerating sensor innovation, better on-device AI, and broader cellular coverage are expanding use cases from casual wellness to regulated healthcare. Growing insurer reimbursement for remote monitoring, rising enterprise safety mandates, and 5G Stand-Alone roll-outs are opening new addressable segments. Hardware remains dominant, yet recurring services revenue is reshaping vendor economics. Platform-centric strategies and cross-device ecosystems are becoming decisive for user retention and lifetime value across the smart wearable market.

Global Smart Wearable Market Trends and Insights

Insurance-approved wearables for cardiac remote monitoring in North America

Rapid adoption of remote patient monitoring codes under the 2025 Physician Fee Schedule is motivating primary-care practices to prescribe ECG-class wearables. Monthly reimbursements of USD 15-110 per patient lower cost barriers for providers, and hospitals report 15% fewer readmissions for congestive heart failure.] Nearly one-third of US clinics have already embedded continuous monitoring into chronic-care workflows, reflecting a material shift from episodic to longitudinal data capture. Higher patient adherence stems from untethered form factors and real-time clinician feedback loops, reinforcing the growth outlook of the smart wearable market.

China's dual-use smartwatch subsidies under Healthy China 2030

Government incentives that reimburse part of the retail price for devices certified to deliver both lifestyle and medical functions are stimulating local R&D and domestic demand. Brands such as Xiaomi and Huawei leveraged the program to scale unit shipments, accelerating time-to-market for SpO2-grade sensors and arrhythmia detection algorithms. The policy is also harmonizing consumer electronics and medical device standards, reducing regulatory friction for exports across the wider Asia-Pacific smart wearable market.

Data-residency mandates limiting cloud companion apps in Europe

EU regulators now require health data to reside within regional borders, compelling vendors to build local processing stacks or risk feature downgrades. Smaller players face higher compliance costs, while user willingness to share sensitive data remains low, curbing network-effect benefits. Fragmented architectures can lengthen update cycles and complicate multi-region releases, tempering the near-term expansion of the smart wearable market in Europe.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise-grade hearables shaped by EU hybrid-work norms

- Rise of AI-on-chip wearables enabling non-invasive glucose monitoring

- High-density battery thermal-runaway concerns in ultra-slim smartwatches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smartwatches retained clear leadership in 2024 with a 46.5% revenue share. Flagship models combine multi-band GPS, ECG, and medical-grade photoplethysmography while improving battery life through low-temperature poly-silicon OLED panels. Dual-sensor arrays support atrial-fibrillation alerts that comply with FDA Class II requirements, strengthening the clinical utility proposition across the smart wearable market.

Smart rings and jewelry record the fastest growth as miniaturized MCU packages and solid-state batteries support continuous SpO2 and heart-rate tracking in a 3-gram form factor. Premium variants target sleep optimization, whereas mass-market models emphasize discreet activity logging. Hearables broaden the category footprint by integrating temperature and cognitive-load sensors, creating an audio-first gateway into workplace safety programs. Fitness trackers move upscale into recovery analytics and VO2-based training readiness, while head-mounted displays gain traction in surgical guidance and field maintenance. Early-generation smart textiles embed stretchable electrodes for posture correction and stress detection, hinting at future expansion of the smart wearable market into everyday apparel.

Core silicon, optical modules, and batteries accounted for 74.1% of 2024 revenue. Suppliers advance 6-nanometer chipsets with neural acceleration to enable on-device classification for arrhythmia and blood-oxygen anomalies. Flexible AMOLED panels and low-loss RF front ends improve efficiency, extending single-charge endurance to seven days on flagship watches.

Recurring services are growing on the back of premium analytics, personalized coaching, and EHR integration. Vendors bundle AI-based sleep improvement plans or nutrition guidance into monthly tiers, lifting average revenue per user and smoothing upgrade cycles. Software remains the glue layer, supporting over-the-air feature extensions that lengthen device lifetimes and fortify ecosystem lock-in in the smart wearable market.

The Smart Wearable Market Report is Segmented by Product (Smartwatches, Hearables, and More), Component (Hardware, Software and Apps, and Services and Subscriptions), Connectivity Technology (Bluetooth/BLE, Cellular, and More), Application/End-use (Consumer Electronics and Lifestyle, Healthcare and Medical, and More), Distribution Channel (Online, Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 34.9% of 2024 revenue. Vertically integrated supply chains enable rapid cost declines and two-month model refreshes. Government programs subsidize ECG-enabled wearables, raising adoption among first-time buyers and chronic-disease patients.

North America remains the premium epicenter, underpinned by early medical credentialing and robust payer engagement. Reimbursement for remote patient monitoring widens device access, and institutional research validates predictive models, reinforcing trust in the smart wearable market.

Europe balances strong demand with strict data-sovereignty rules. Vendors deploy edge-only analytics and in-region data lakes to comply with GDPR, while corporate safety mandates accelerate hearables roll-outs.

The Middle East and Africa post the highest growth at 20.7% CAGR, catalyzed by 5G Advanced coverage and national e-health blueprints that leverage wearables to extend care to under-served communities. South America sees uneven uptake due to currency swings and 5G cost, but localization partnerships and wellness subsidies in Brazil and Mexico provide momentum.

- Apple Inc.

- Samsung Electronics Co. Ltd

- Alphabet Inc. (Fitbit and Google Pixel)

- Garmin Ltd

- Huawei Technologies Co. Ltd

- Xiaomi Corp.

- BOBOVR

- Sony Corp.

- Microsoft Corp.

- Meta Platforms Inc. (Oculus)

- Huami Corp. (Zepp Health)

- Withings SA

- Omron Healthcare Inc.

- Cyberdyne Inc.

- Ekso Bionics Holdings Inc.

- GoPro Inc.

- Fossil Group Inc.

- Nuheara Ltd.

- Bragi GmbH

- Sensoria Inc.

- AIQ Smart Clothing Inc.

- Polar Electro Oy

- Coros Wearables Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Insurance-approved Wearables for Cardiac Remote Monitoring in North America

- 4.2.2 China's Dual-Use (Consumer + Medical) Smartwatch Subsidies through Healthy China 2030

- 4.2.3 Enterprise-grade Hearables Adoption Driven by EU's Hybrid-Work Safety NormsPost-COVID

- 4.2.4 Rise of AI-on-Chip Wearables Enabling Continuous Glucose Monitoring without Needles

- 4.2.5 Defense Exoskeleton Procurements under United States Soldier Lethality Program

- 4.2.6 Pay-as-you-Lift Industrial Exoskeleton Leasing in South-East Asia's Construction Sector

- 4.3 Market Restraints

- 4.3.1 Data-Residency Mandates Limiting Cloud Companion Apps in Europe

- 4.3.2 High-Density Battery Thermal Runaway Concerns in Ultra-Slim Smartwatches

- 4.3.3 Patent-Licensing Litigation Costs for Gesture-Based Smart Rings

- 4.3.4 Low ARPU in LATAM Limiting 5G Stand-alone Wearable Roll-outs

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product

- 5.1.1 Smartwatches

- 5.1.2 Hearables (Ear-Worn/Smart Earbuds)

- 5.1.3 Fitness and Activity Trackers

- 5.1.4 Head-Mounted Displays (AR/VR/MR)

- 5.1.5 Smart Clothing and Textiles

- 5.1.6 Body-worn Cameras

- 5.1.7 Smart Rings and Jewelry

- 5.1.8 Medical Wearable Patches and Biosensors

- 5.1.9 Powered Exoskeletons

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software and Apps

- 5.2.3 Services and Subscriptions

- 5.3 By Connectivity Technology

- 5.3.1 Bluetooth/BLE

- 5.3.2 Cellular (3G/4G/LTE-M)

- 5.3.3 5G Stand-Alone

- 5.3.4 NFC/RFID

- 5.3.5 Wi-Fi/WLAN

- 5.3.6 Others (UWB, ANT+)

- 5.4 By Application/End-use

- 5.4.1 Consumer Electronics and Lifestyle

- 5.4.2 Healthcare and Medical

- 5.4.3 Fitness and Sports

- 5.4.4 Industrial and Enterprise Safety

- 5.4.5 Military and Defense

- 5.5 By Distribution Channel

- 5.5.1 Online (Brand E-store, Marketplaces)

- 5.5.2 Offline (Consumer Electronics Stores, Specialty, Clinics)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 South East Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd

- 6.4.3 Alphabet Inc. (Fitbit and Google Pixel)

- 6.4.4 Garmin Ltd

- 6.4.5 Huawei Technologies Co. Ltd

- 6.4.6 Xiaomi Corp.

- 6.4.7 BOBOVR

- 6.4.8 Sony Corp.

- 6.4.9 Microsoft Corp.

- 6.4.10 Meta Platforms Inc. (Oculus)

- 6.4.11 Huami Corp. (Zepp Health)

- 6.4.12 Withings SA

- 6.4.13 Omron Healthcare Inc.

- 6.4.14 Cyberdyne Inc.

- 6.4.15 Ekso Bionics Holdings Inc.

- 6.4.16 GoPro Inc.

- 6.4.17 Fossil Group Inc.

- 6.4.18 Nuheara Ltd.

- 6.4.19 Bragi GmbH

- 6.4.20 Sensoria Inc.

- 6.4.21 AIQ Smart Clothing Inc.

- 6.4.22 Polar Electro Oy

- 6.4.23 Coros Wearables Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

智慧型穿戴式打鼾侦测器市场规模、份额和成长分析:按产品类型、技术、价格范围、最终用户、销售管道、地区和产业预测,2026-2033年

智慧型穿戴式打鼾侦测器市场规模、份额和成长分析:按产品类型、技术、价格范围、最终用户、销售管道、地区和产业预测,2026-2033年 2026年全球智慧型穿戴式打鼾检测器市场报告

2026年全球智慧型穿戴式打鼾检测器市场报告 智慧型穿戴装置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分智慧生物识别穿戴装置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形式、最终用户和功能划分智慧袜市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、最终用户、功能、安装类型及解决方案划分2026年全球智慧穿戴装置市场报告

智慧型穿戴装置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户和功能划分智慧生物识别穿戴装置市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形式、最终用户和功能划分智慧袜市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材料类型、最终用户、功能、安装类型及解决方案划分2026年全球智慧穿戴装置市场报告 智慧型穿戴装置市场-全球产业规模、份额、趋势、机会及预测(依设备、产品类型、应用、地区及竞争格局划分,2021-2031年)

智慧型穿戴装置市场-全球产业规模、份额、趋势、机会及预测(依设备、产品类型、应用、地区及竞争格局划分,2021-2031年) 智慧健康袜市场按产品类型、技术、应用、分销管道和最终用户划分-2026年至2032年全球预测智慧型穿戴眼镜市场:按技术、产品类型、最终用户、应用和分销管道分類的全球预测(2026-2032年)

智慧健康袜市场按产品类型、技术、应用、分销管道和最终用户划分-2026年至2032年全球预测智慧型穿戴眼镜市场:按技术、产品类型、最终用户、应用和分销管道分類的全球预测(2026-2032年) 智慧型穿戴装置市场规模、份额和成长分析(按作业系统、连接方式、性别、产品类型、应用、销售管道、最终用户和地区划分)—2026-2033年产业预测

智慧型穿戴装置市场规模、份额和成长分析(按作业系统、连接方式、性别、产品类型、应用、销售管道、最终用户和地区划分)—2026-2033年产业预测