|

市场调查报告书

商品编码

1850129

ADAS(高级驾驶辅助系统):市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Advanced Driver Assistance Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

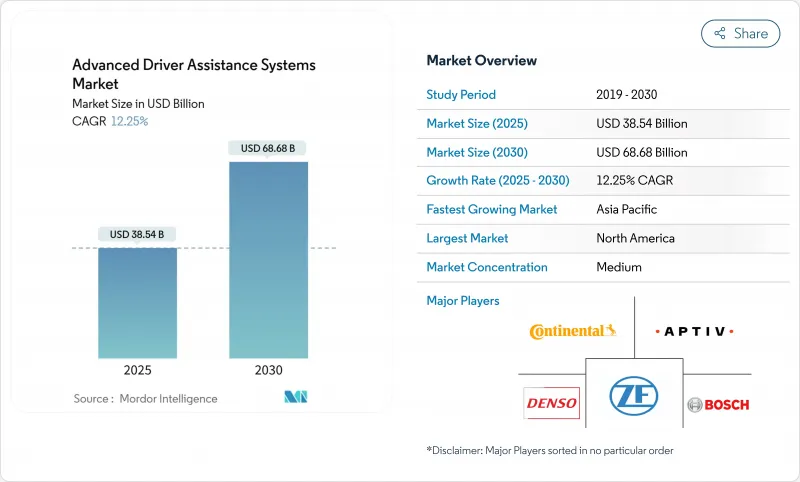

全球高级驾驶辅助系统 (ADAS) 市场预计到 2025 年收入将达到 385.4 亿美元,到 2030 年将达到 686.8 亿美元,复合年增长率为 12.25%。

美国、欧盟和中国强而有力的监管政策、雷达、摄影机和光达感测器成本的快速下降,以及汽车产业向软体定义车辆(SDV)平台的转型,都是推动这一成长的关键因素。汽车製造商正在将L2+功能整合到中阶车型中,而空中下载(OTA)升级途径则带来了持续的软体收入。同时,亚洲半导体产能的提升与新型4奈米汽车系统晶片的出现,提高了感测器融合的精度,并推动ADAS市场向量产车型迈进。竞争格局正向垂直平台模式转变,一级供应商、云端超大规模资料中心业者和无晶圆厂晶片设计商携手合作,共同掌控感知堆迭、训练资料和可获利的软体服务。

全球高阶驾驶辅助系统 (ADAS) 市场趋势与洞察

严格的安全法规支持市场成长

目前,驾驶辅助系统已被法规视为必要的基础设施。美国国家公路交通安全管理局 (NHTSA) 将要求自 2029 年 9 月起,美国所有新生产的轻型车辆都必须配备自动紧急煞车系统,目标年安装量约为 1,700 万辆。欧洲的《通用安全法规 II》(GSRR II) 也强制要求自 2024 年 7 月起,所有新车都必须配备智慧速度援助、车道维持援助和紧急煞车系统,这将迫使汽车製造商重新设计其电气架构,以实现 ADAS 功能的标准化。中国已将 ADAS 性能纳入新车评估体系,将五星安全评级与感测器配置和演算法精度挂钩。这些法规将消除消费者的随意购买决策,并将 ADAS 市场转变为以合主导性和销售量为导向的市场,加速各个价格分布的安装速度。

基于人工智慧的感应器融合解锁功能商品搭售

片上神经网路技术的进步使得低成本处理器也能实现高阶感知功能。 Mobileye 的 EyeQ6 Lite 将八个摄影机资料流和 4D 雷达输入整合到单一 5 瓦设备中,从而降低了 L2+ 高速公路自动驾驶套件的物料成本。博世整合了微软的生成式人工智慧服务,实现了预测性路径规划,能够预判驾驶员意图和横向交通操作。这些发展使得原始设备製造商 (OEM) 可以将主动式车距维持定速系统、车道居中保持和交通标誌识别功能打包到单一订阅服务中,从而减少每个功能的硬体冗余,并提高软体利润率。

高昂的感测器套件成本仍然是一大障碍。

即使价格大幅下降,一套完整的L2+感测器套件也将使B级掀背车的製造成本增加2000至4000美元。保险业数据显示,轻微碰撞后更换雷达的费用超过每辆车900美元,而摄影机重新校准的平均费用为450美元。这些成本抑制了高端价格分布以外的消费者购买意愿,并削弱了维修基础设施有限的新兴经济体的售后市场需求。

细分市场分析

高级驾驶辅助系统 (ADAS) 系统级解决方案的市场规模主要由主动式车距维持定速系统驱动,预计到 2024 年,自适应巡航控制将贡献 22.41% 的收入,这得益于其与现有电子煞车模组的兼容性以及消费者在远距旅行中的广泛接受度。自动紧急煞车系统 (AEB) 的复合年增长率 (CAGR) 为 16.21%,这主要受法规要求所有新车配备前向碰撞缓解系统的推动。供应商目前正将行人侦测和骑乘者侦测功能整合到同一控制单元中,从而在各个细分市场实现规模经济。预计到 2030 年,原始设备製造商 (OEM) 将把城市紧急煞车系统扩展到摩托车和轻型商用车,从而扩大安全覆盖范围并增加安装数量。

从历史资料来看,该细分市场2020年至2024年的复合成长率为8.5%,但美国国家公路交通安全管理局(NHTSA)和欧盟的强制规定将使这项成长率在预测期内翻倍。入门级预警功能,例如车道偏离预警和前碰撞警报,在低价位车型中得以保留,而高级配置包则集成了360度全景摄像头、高清地图和人工智能辅助的十字路口转弯预测制动系统。这种渐进式升级路径能够带来持续的空中下载收入,并增强拥有感知技术堆迭的一级供应商的平台用户黏性。

雷达46.07%的市占率凸显了其在雨、雾、雪等恶劣天气条件下的出色表现,巩固了其作为自动紧急煞车主要触发因素的地位。 ADAS市场正受惠于77GHz前角雷达模组的普及,这些模组目前采用28nm射频CMOS製程生产。配备10nm以下影像讯号处理器的摄影机感测器也紧跟其后,以经济高效的方式支援深度学习感知架构。

雷射雷达的市场份额虽然仍然较小,但成长迅速,预计复合年增长率将达到21.35%。固态、无移动部件架构和晶圆级光学技术已将变动成本降至350美元,使中型SUV成为下一个目标市场。为了在ADAS(高级驾驶辅助系统)市场占据更大的份额,光达供应商正与OEM(原始设备製造商)设计工作室合作,将感测器嵌入头灯丛集,从而避免在车顶安装影响美观的灯罩。超音波和红外线在泊车和夜视领域仍然占据着一定的市场份额。集中融合讯号处理技术正在兴起,它减少了布线,并支援基于空中下载(OTA)的演算法改进,从而延长硬体週期。

区域分析

美国正透过降低第三人意外责任险和提高NCAP碰撞测试评分来增加对ADAS(高级驾驶辅助系统)普及的奖励,而加拿大则正使其汽车安全法规与美国标准接轨,以确保跨境车型的一致性。领先的供应商正在亚利桑那州、密西根州和安大略省开展检验车队,以收集极端情况下的数据,从而改进针对雪地和眩光等恶劣天气条件的感测器融合演算法。

亚太地区是成长最快的地区,到2030年复合年增长率将达到14.55%,这主要得益于中国雄心勃勃的「智慧汽车」蓝图。该路线图在2023年第三季发放了超过30万张L2+级智慧汽车牌照。北京方面关于众包高清地图的指导方针将促进资料网路效应,使比亚迪和小鹏等国内汽车製造商受益。针对印度半导体工厂和电子元件的生产奖励将鼓励本地ADAS ECU(高级驾驶辅助系统ECU)的生产,从而降低材料成本并加快其在小型掀背车的应用。

欧洲在通用安全法规II的指导下持续保持稳定成长,该法规要求汽车製造商在所有新车中整合九项安全功能。德国联邦参议院核准了限速60公里/小时的高速公路脱手驾驶,加速了L3级自动驾驶的推出。法国和西班牙优先为重型卡车车队的维修提供津贴,以满足「零愿景」事故目标。在南美洲,巴西强制所有新车配备电子稳定控制系统,并计画在2027年(可能提前至2030年)开始评估车道偏离预警系统。智利和哥伦比亚正在推出与安装自动紧急煞车系统相关的道路税减免政策,并鼓励进口商在入门级车型上标配雷达。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国、欧盟和中国都有严格的安全法规。

- 基于人工智慧的传感器融合实现了L2+功能的整合。

- SDV/OTA架构释出售后收入潜力

- 快速降低感测器成本并实现模组化集成

- SUV和豪华车在新兴市场的渗透率不断提高

- 基于使用量的保险折扣加快了原厂配件的适配速度

- 市场限制

- 光达/雷达系统高成本

- 恶劣天气或光线造成的功能限制

- 网路安全责任与资料隐私风险

- 毫米波晶片组和基板供应瓶颈

- 价值链/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依系统类型

- 停车辅助系统

- 主动式转向头灯

- 夜视系统

- 盲点侦测

- 自动紧急制动

- 前方碰撞警报

- 驾驶员疲劳警告

- 交通标誌识别

- 车道偏离警示

- 主动车距控制巡航系统

- 依感测器类型

- 雷达

- LiDAR

- 相机

- 超音波

- 红外线的

- 按车辆类型

- 摩托车

- 搭乘用车

- 中型和重型商用车辆

- 依自主程度

- L1

- L2

- L3

- L4

- L5

- 按销售管道

- 原厂适配

- 售后改装

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 印尼

- 亚太其他地区

- 中东和非洲

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Valeo SA

- Hyundai Mobis

- Aisin Corporation

- Mobileye(Intel)

- NVIDIA Corporation

- NXP Semiconductors

- Infineon Technologies

- Renesas Electronics

- ON Semiconductor

- STMicroelectronics

- Hitachi Astemo

- Autoliv Inc.

第七章 市场机会与未来展望

The global ADAS market posted USD 38.54 billion in revenue in 2025 and is on course to reach USD 68.68 billion by 2030, expanding at a 12.25% CAGR.

Robust regulatory mandates in the United States, the European Union, and China, rapid cost deflation in radar, camera, and LiDAR sensors, and the auto sector's migration to software-defined vehicle (SDV) platforms are the prime forces sustaining this growth. Automakers are bundling Level 2+ features on mid-segment vehicles while over-the-air (OTA) upgrade pathways increasingly generate recurring software revenue. Simultaneously, the expansion of semiconductor capacity in Asia and new 4-nanometer automotive system-on-chips enable higher sensor fusion accuracy, pushing the ADAS market deeper into mass-volume models. Competitive dynamics are shifting toward vertical platform plays in which Tier-1 suppliers, cloud hyperscalers, and fabless chip designers collaborate to control perception stacks, training data, and monetisable software services.

Global Advanced Driver Assistance Systems Market Trends and Insights

Stringent Safety Mandates Anchor Market Growth

Regulations now treat driver-assistance as mandatory infrastructure. The NHTSA requires automatic emergency braking on all new US light vehicles from September 2029, setting a baseline of roughly 17 million units per year. Europe's General Safety Regulation II has required intelligent speed assistance, lane-keeping assistance, and emergency braking on every new model since July 2024, forcing OEMs to redesign electrical architectures for standardised ADAS functions. China integrated ADAS performance into its New Car Assessment Programme, linking five-star safety scores to sensor configuration and algorithm accuracy. These rules remove discretionary purchasing decisions and transform the ADAS market into a compliance-driven volume business, accelerating fitment rates across all price points.

AI-Based Sensor Fusion Unlocks Feature Bundling

Advances in on-chip neural networks now permit high-level perception on inexpensive processors. Mobileye's EyeQ6 Lite combines eight camera streams and 4-D radar inputs on a single 5-Watt device, lowering bill-of-materials costs for L2+ highway pilot packages. Bosch's integration of Microsoft's generative AI services enables predictive path planning that anticipates driver intent and cross-traffic manoeuvres. These developments allow OEMs to package adaptive cruise control, lane centering, and traffic sign recognition under one subscription, reducing per-feature hardware redundancy and increasing software margins.

High Sensor Suite Cost Remains a Barrier

Even with steep price declines, a complete L2+ sensor pack adds USD 2,000-4,000 to build cost for a B-segment hatchback. Insurance-sector data show radar replacement after minor collisions exceeding USD 900 per unit, while camera recalibration averages USD 450. These costs dampen consumer uptake outside premium tiers and slow retrofit demand in developing economies lacking repair infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- SDV Architectures Redefine Revenue Models

- Sensor Cost Deflation Broadens Mass-Market Access

- Weather Vulnerabilities Challenge Reliability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The ADAS market size for system-level solutions remains anchored by adaptive cruise control, which generated 22.41% of 2024 revenue thanks to its compatibility with existing electronic braking modules and consumer acceptance during long-distance travel. Automatic emergency braking is accelerating at a 16.21% CAGR, propelled by regulations that demand forward collision mitigation on all new vehicles. Suppliers now integrate pedestrian and cyclist detection in the same control unit, creating cross-segment economies of scale. Over the period to 2030, OEMs are expected to extend urban emergency braking to two-wheelers and light commercial vans, broadening safety coverage and raising fitment volumes.

Historical data underline the regulatory inflection, between 2020-2024 the sub-segment posted 8.5% compound growth, but the NHTSA and EU mandates double that pace in the forecast window. Entry-level warning functions such as lane departure and forward collision alerts persist for low-cost trims, whereas advanced premium packages integrate 360-degree cameras, HD maps and AI-enabled predictive braking during intersection turns. This layered upgrade pathway encourages recurring OTA revenues and deepens platform stickiness for Tier-1 suppliers that own the perception stack.

Radar's 46.07% share underscores its robustness in rain, fog, and snow, attributes that secure its position as the primary trigger for automatic emergency braking. The ADAS market benefits from the commoditisation of 77 GHz front-corner radar modules now produced in 28-nanometer RF CMOS. Camera sensors, powered by sub-10 nm image-signal processors, are followed closely by enabling deep-learning perception architectures cost-effectively.

LiDAR, though still accounts for minimal market share, is the flash-growth element with a projected 21.35% CAGR. Solid-state, no-moving-parts architecture plus wafer-level optics lower variable cost to USD 350, making mid-segment SUVs the next target. For ADAS market share gains, LiDAR suppliers partner with OEM design studios to embed sensors into headlamp clusters, avoiding rooftop domes that hinder aesthetics. Ultrasonic and infrared retain niche duties for parking and night vision. A cross-trend of centrally fused signal processing is emerging, reducing wiring mass and enabling OTA-based algorithm improvements that prolong hardware cycles.

The Advanced Driver Assistance Systems Market Report is Segmented by System Type (Parking Assist Systems, Adaptive Front-Lighting, and More), Sensor Type (Radar, Lidar, and More), Vehicle Type (Two-Wheeler, and More), Level of Anatomy (L1, L2, and More), Sales Channel (OEM-Fitted and Aftermarket Retrofit), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America generated 34.33% of global revenue in 2024 as federal mandates, insurance incentives, and high SUV penetration created a receptive base for Level 2+ bundles. The United States incentivises ADAS deployment further through reduced liability premiums and positive NCAP scoring, while Canada aligns its Motor Vehicle Safety Regulations to US norms, ensuring cross-border model harmonisation. Major suppliers run validation fleets across Arizona, Michigan, and Ontario, collecting edge-case data that refines sensor-fusion algorithms for snow and glare conditions.

Asia-Pacific is the fastest-growing region at a 14.55% CAGR to 2030, propelled by China's aggressive "smart-vehicle" roadmap that awarded more than 300,000 L2+ licences in Q3 2023. Beijing's guidelines on HD map crowdsourcing encourage data-network effects that benefit domestic OEMs such as BYD and Xpeng. India's Production-Linked Incentive for semiconductor fabs and electronic components incentivises local ADAS ECU manufacturing, cutting bill-of-materials costs and quickening fitment among compact hatchbacks.

Europe continues at a steady growth rate under General Safety Regulation II, which obliges automakers to integrate nine safety functions on every new model. Germany's Bundesrat approved limited hands-off motorway driving at speeds up to 60 km/h, accelerating Level 3 debut timelines. France and Spain prioritise retrofit subsidies for heavy-duty truck fleets to meet Vision Zero accident targets. South America shows potential through 2030 as Brazil mandates electronic stability control on all new cars and evaluates lane departure alerts for 2027. Chile and Colombia roll out vehicle tax rebates tied to AEB fitment, spurring importers to specify radar on entry models.

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Valeo SA

- Hyundai Mobis

- Aisin Corporation

- Mobileye (Intel)

- NVIDIA Corporation

- NXP Semiconductors

- Infineon Technologies

- Renesas Electronics

- ON Semiconductor

- STMicroelectronics

- Hitachi Astemo

- Autoliv Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent safety mandates in United States, European Union, China

- 4.2.2 AI-based sensor fusion enabling L2+ feature bundling

- 4.2.3 SDV/OTA architectures unlocking post-sale revenue

- 4.2.4 Rapid sensor-cost deflation & module integration

- 4.2.5 Growing SUV & premium-car penetration in Emerging Markets

- 4.2.6 Usage-based-insurance discounts accelerating OEM fitment

- 4.3 Market Restraints

- 4.3.1 High LiDAR/Radar system cost

- 4.3.2 Functional limitations in poor weather & lighting

- 4.3.3 Cyber-security liability & data-privacy risk

- 4.3.4 mmWave chipset & substrate supply bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By System Type

- 5.1.1 Parking Assist Systems

- 5.1.2 Adaptive Front-Lighting

- 5.1.3 Night Vision Systems

- 5.1.4 Blind-Spot Detection

- 5.1.5 Automatic Emergency Braking

- 5.1.6 Forward Collision Warning

- 5.1.7 Driver Drowsiness Alert

- 5.1.8 Traffic Sign Recognition

- 5.1.9 Lane Departure Warning

- 5.1.10 Adaptive Cruise Control

- 5.2 By Sensor Type

- 5.2.1 Radar

- 5.2.2 LiDAR

- 5.2.3 Camera

- 5.2.4 Ultrasonic

- 5.2.5 Infra-red

- 5.3 By Vehicle Type

- 5.3.1 Two-Wheelers

- 5.3.2 Passenger Cars

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Level of Autonomy

- 5.4.1 L1

- 5.4.2 L2

- 5.4.3 L3

- 5.4.4 L4

- 5.4.5 L5

- 5.5 By Sales Channel

- 5.5.1 OEM-Fitted

- 5.5.2 Aftermarket Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Indonesia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Turkey

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Nigeria

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Continental AG

- 6.3.2 Robert Bosch GmbH

- 6.3.3 DENSO Corporation

- 6.3.4 Aptiv PLC

- 6.3.5 ZF Friedrichshafen AG

- 6.3.6 Magna International

- 6.3.7 Valeo SA

- 6.3.8 Hyundai Mobis

- 6.3.9 Aisin Corporation

- 6.3.10 Mobileye (Intel)

- 6.3.11 NVIDIA Corporation

- 6.3.12 NXP Semiconductors

- 6.3.13 Infineon Technologies

- 6.3.14 Renesas Electronics

- 6.3.15 ON Semiconductor

- 6.3.16 STMicroelectronics

- 6.3.17 Hitachi Astemo

- 6.3.18 Autoliv Inc.

7 Market Opportunities & Future Outlook

汽车ADAS感测器市场:按车辆类型、自动驾驶等级、感测器类型和应用划分-2026-2032年全球市场预测

汽车ADAS感测器市场:按车辆类型、自动驾驶等级、感测器类型和应用划分-2026-2032年全球市场预测 即时碰撞预测系统市场预测至 2034 年:全球分析(按组件、车辆类型、部署模式、最终用户和地区划分)驾驶员在环模拟器市场:按模拟器类型、车辆类型、部署模式、应用和最终用户划分 - 全球预测,2026-2032 年汽车ADAS标定工具市场(按车辆类型、部署模式、标定类型、系统类型、标定方法、最终用户和销售管道),全球预测,2026-2032年汽车ADAS校准设备市场(按设备类型、校准方法、车辆类型和分销管道划分),全球预测(2026-2032年)

即时碰撞预测系统市场预测至 2034 年:全球分析(按组件、车辆类型、部署模式、最终用户和地区划分)驾驶员在环模拟器市场:按模拟器类型、车辆类型、部署模式、应用和最终用户划分 - 全球预测,2026-2032 年汽车ADAS标定工具市场(按车辆类型、部署模式、标定类型、系统类型、标定方法、最终用户和销售管道),全球预测,2026-2032年汽车ADAS校准设备市场(按设备类型、校准方法、车辆类型和分销管道划分),全球预测(2026-2032年) 驾驶辅助收发器市场规模、份额和成长分析:按技术类型、车辆类型、应用、分销管道、地区和行业预测,2026-2033年

驾驶辅助收发器市场规模、份额和成长分析:按技术类型、车辆类型、应用、分销管道、地区和行业预测,2026-2033年 驾驶辅助摄影机市场规模、份额和成长分析:按摄影机类型、技术、应用、最终用户、感测器整合和地区划分-2026-2033年产业预测

驾驶辅助摄影机市场规模、份额和成长分析:按摄影机类型、技术、应用、最终用户、感测器整合和地区划分-2026-2033年产业预测 ADAS模拟市场机会、成长要素、产业趋势分析及2026年至2035年预测

ADAS模拟市场机会、成长要素、产业趋势分析及2026年至2035年预测 自主半导体维护无人机市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、解决方案划分ADAS订阅市场机会、成长要素、产业趋势分析及2026年至2035年预测

自主半导体维护无人机市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型、解决方案划分ADAS订阅市场机会、成长要素、产业趋势分析及2026年至2035年预测