|

市场调查报告书

商品编码

1850160

气凝胶:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030)Aerogel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

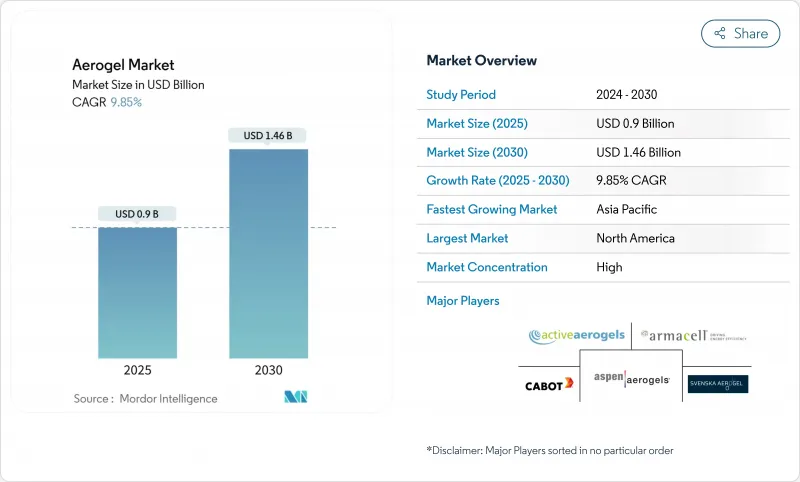

预计气凝胶市场规模到 2025 年将达到 9 亿美元,到 2030 年将成长到 14.6 亿美元,2025 年至 2030 年的复合年增长率为 9.85%。

高性能隔热材料的持续需求,以及电气化和碳减排政策的加速推进,正推动气凝胶市场呈现强劲成长动能。由于严格的能源效率法规和强劲的油气维修周期,北美目前占据40%的市场份额,占据市场主导地位。市场整合正在加剧,Aspen Aerogels和卡博特公司成为全球收益的主要驱动力。

全球气凝胶市场趋势与洞察

可重复使用性和可回收性提高了气凝胶的采用率

製造商正在优先考虑能够最大限度地提高再利用潜力并最大限度减少废弃物产生的生产路线。新型二氧化硅气凝胶在75公斤/立方公尺的低密度下仍维持95%的孔隙率,可达到多个使用週期且无热损失。 ENERSENS扩大了其电脑控制的蒸发微波製程的规模,将产量提高了60%,同时实现了材料回收,并降低了最终用户的总拥有成本。生命週期分析证实,与隔热材料相比,工业规模的气凝胶合成可减少对环境的影响,这使得这种材料对净零排放路径具有吸引力。随着各大品牌量化绿色建筑标籤的二氧化碳减排量,可重复使用的气凝胶隔热材料正成为日益重要的规范优先事项,尤其是对于需要长使用寿命的建筑幕墙维修。

建筑业对高性能隔热材料的需求快速成长

日益严格的建筑标准,包括2021年国际能源效率标准和类似的欧盟标准,要求降低外墙的U值。气凝胶板的R值是矿棉的两到四倍,同时占用的空腔更薄,使其成为空间受限的都市区维修的必备材料。 2024年创纪录的热浪加速了人们对气凝胶填充结构玻璃系统的兴趣,这种系统可以在不牺牲阳光的情况下限制太阳能增益。新型防火「变形」气凝胶目前正在保护火灾易发地区的建筑结构,凸显了其除了节能之外更广泛的韧性优势。

製造成本高

超临界干燥仍然是主要的生产工艺,需要在高温高压下运行的专用容器。资本密集度导致单位成本高于主流隔热材料,阻碍了其在成本敏感的住宅领域的应用。常温干燥的研究前景广阔,但尚未达到商业规模。近期的缓解措施着重于提高产量和溶剂回收率,以降低变动成本。在这些技术成熟之前,高昂的定价将限制气凝胶的应用,仅限于那些对性能有严格要求且碳减排奖励能够证明前期投资合理性的计划。

細項分析

预计到2024年,二氧化硅等级将占据气凝胶市场72%的份额,并将以10.11%的强劲复合年增长率进一步扩大其领先地位,直至2030年。这一领先地位归功于其广泛的应用领域,包括油气管道、建筑幕墙隔热材料和电动车电池模组。大量的研发成果已研发出二氧化硅/聚酰亚胺「石榴」复合材料,其抗压强度提高了12倍,且热值保持不变,从而消除了机械处理方面的历史障碍。

第二代二氧化硅系统也着重防潮性和易涂饰性。客製化疏水涂层如今可保持超过120°的接触角,使建筑幕墙能够在潮湿气候下使用。同时,负责人正在探索低醇盐溶胶-凝胶工艺,以减少溶剂消费量、降低成本和二氧化碳排放。这些多方面的创新巩固了二氧化硅在气凝胶市场的地位,而技术进步很可能将决定该行业必须达到的整体性能标准。

由于毯子易于安装且与能源基础设施中使用的管道绝缘涂层相容,因此它在 2024 年占据了气凝胶市场 64% 的收益。最新产品的热导率低至 0.0143 W/mK,可在 10 分钟内达到热平衡,从而缩短了施工时间。

颗粒形态是一个突破性的类别,随着配方师将气凝胶粉末融入涂料、锂离子隔膜和聚合物复合材料中,预计到2030年,该类别的复合年增长率将达到10.34%。卡博特的ENTERA颗粒可作为电动车电池阴极的嵌入式热调节器,无需厚厚的屏障即可缓解失控现象。

区域分析

到2024年,北美将以40%的收益份额引领气凝胶市场。联邦和各州的能源效率要求,以及强劲的石油和天然气资本投资,支撑着强劲的需求。卡博特公司获得美国能源部5000万美元的拨款,用于其电池级导电添加剂的本地化,这肯定了政策主导对与气凝胶具有直接协同效应的温度控管材料的投资。美国国家科学基金会的津贴也为下一代建筑隔热材料的研究提供了种子资金,北美在性能突破方面处于领先地位。

预计亚太地区将成为成长最快的地区,到2030年,复合年增长率将达到10.25%。液化天然气基础设施的快速部署、住房建设的蓬勃发展以及电动车生产的加速成长将推动该地区的消费量飙升。中国科研机构研发出能够承受极端温度并承受结构负荷的碳气凝胶复合材料,将为中国的高温工业提供支援。

欧洲保持强大的监管领导力,利用《欧洲建筑规范》(EPBD) 修正案,鼓励深度节能维修,采用薄型高阻材料系统。一项在社会住宅区开展的试点项目展示了建筑幕墙气凝胶面板,在保持美观的同时,减少了 40% 的空间供暖。中东和非洲地区继续在炼油和石化升级领域采用气凝胶,而南美洲液化天然气进口和绿色建筑认证的不断增长势头也推动了气凝胶的应用成长。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 可重复使用性和可回收性推动气凝胶的采用

- 建筑业对高性能隔热材料的需求快速成长

- 能源效率法规刺激欧盟和北美的需求

- 扩大亚洲液化天然气基础设施

- 石油和天然气产业主导气凝胶需求

- 市场限制

- 生产成本高

- 原料供应有限

- 建筑业中高性能聚合物泡沫的竞争

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场规模及成长预测

- 按类型

- 二氧化硅

- 碳

- 氧化铝

- 其他类型

- 按形式

- 毯子

- 粒子

- 堵塞

- 控制板

- 按用途

- 隔热材料

- 隔音材料

- 催化剂和吸附剂

- 电池和储能

- 日光和半透明面板

- 其他用途

- 按最终用户产业

- 石油和天然气

- 建造

- 车

- 海洋

- 航太

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Acoustiblok, Inc.

- Active Aerogels

- Aerogel Technologies, LLC

- aerogel-it

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Blueshift Materials Inc.

- Cabot Corporation

- ENERSENS

- Guangdong Alison Technology Co., Ltd.

- Knauf Insulation

- Nano Tech Co., Ltd.

- Ningbo Surnano Aerogel Co., Ltd

- Porex

- Sino Aerogel

- Svenska Aerogel AB

- TAASI Corporation

- Thermablok Aerogels Ltd.

第七章 市场机会与未来展望

The aerogel market is valued at USD 0.90 billion in 2025 and is projected to grow to USD 1.46 billion by 2030, advancing at a 9.85% CAGR in the 2025-2030 period.

Sustained demand for high-performance thermal insulation, coupled with accelerating electrification and carbon-reduction mandates, is placing the aerogel market on a strong growth trajectory. North America leads today with a 40% share, supported by strict energy-efficiency codes and an active oil-and-gas retrofit cycle. High market consolidation prevails; Aspen Aerogels and Cabot Corporation anchor global revenue, yet a host of regional specialists compete aggressively in formulation niches.

Global Aerogel Market Trends and Insights

Rise in Adoption of Aerogel Due to Reusability and Recyclability

Manufacturers are prioritizing production routes that maximize re-use potential and minimize waste generation. New silica aerogels now preserve 95% porosity at a low 75 kg/m3 density, allowing multiple service cycles without thermal loss. ENERSENS scaled a computer-controlled evaporation microwave process that lifts output 60% while enabling material recovery, lowering total cost of ownership for end users. Life-cycle analysis confirms industrial-scale aerogel synthesis slashes environmental burdens versus conventional insulants, making the material attractive in net-zero pathways. As brands quantify CO2 savings for green-building labels, reusable aerogel insulation is gaining specification priority, particularly in facade retrofits seeking long service life.

Rapidly Growing Construction Demand for High-performance Insulation

Building codes tightened under the 2021 International Energy Conservation Code and similar EU standards mandate lower envelope U-values. Aerogel panels deliver R-values 2-4 times times higher than mineral wool while occupying thinner cavities, critical for urban refurbishments where space is limited. Record heatwaves in 2024 accelerated interest in aerogel-filled glazing systems that limit solar gain without sacrificing daylight. Novel wildfire-resistant "morphing" aerogels now protect structures in fire-prone regions, highlighting broader resilience benefits beyond energy savings.

High Production Cost

Super-critical drying remains the dominant manufacturing route and demands specialized vessels operating at high pressure and temperature. Capital intensity keeps unit prices above mainstream insulation, discouraging uptake in cost-sensitive residential segments. Research into ambient pressure drying shows promise, but it is not yet commercial at scale. Short-term mitigation focuses on throughput gains and solvent recovery to lower variable costs. Until those techniques mature, premium positioning will constrain aerogel penetration to projects with stringent performance needs or carbon-reduction incentives that justify a higher upfront outlay.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Boosting EU and North American Demand

- Expansion of LNG Infrastructure Across Asia

- Limited Availability of Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silica grades commanded a 72% share of the aerogel market in 2024 and are expected to widen their lead by posting a robust 10.11% CAGR through 2030, a rare scenario where the largest slice also grows fastest. This leadership stems from broad applicability in oil-and-gas pipelines, facade insulation, and EV battery modules. Significant research and development produced silica/polyimide "pomegranate" composites that yield 12-fold higher compressive strength without sacrificing thermal values, removing a historic barrier to mechanical handling.

Second-generation silica systems are also targeting moisture resistance and easier finishing. Tailored hydrophobic coatings now sustain contact angles above 120°, allowing exterior facade usage in humid climates. Meanwhile, formulators are exploring low-alkoxide sol-gel routes that cut solvent consumption, reducing cost and CO2 footprint. Given this multi-pronged innovation, silica's hold on the aerogel market appears secure, and its technological progress will likely dictate overall performance benchmarks the sector must meet.

Blankets secured 64% of the aerogel market revenue in 2024, owing to installation ease and compatibility with pipe-insulation jacketing used in energy infrastructure. Recent iterations achieve thermal conductivity as low as 0.0143 W/mK and reach thermal equilibrium in 10 minutes, shortening construction schedules.

Particle form is the breakout category, forecast to log a 10.34% CAGR through 2030 as formulators incorporate aerogel powders into coatings, lithium-ion separators, and polymer composites. ENTERA particles from Cabot serve as drop-in thermal modifiers in EV battery cathodes, mitigating runaway events without thick barriers.

The Aerogel Market Report Segments the Industry by Type (Silica, Carbon, Alumina, and Other Types), Form (Blanket, Particle, Block, and Panel), Application (Thermal Insulation, Acoustic Insulation, Catalyst and Adsorbent, and More), End-User Industry (Oil and Gas, Construction, Automotive, Marine, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the aerogel market with a 40% revenue share in 2024. Federal and state efficiency mandates, alongside robust oil-and-gas capital expenditure, underpin solid demand. Cabot Corporation's USD 50 million Department of Energy award to localize battery-grade conductive additives affirms policy-driven investment in thermal-management materials with direct aerogel synergies. National Science Foundation grants are also seeding next-generation building insulation research, keeping North America at the forefront of performance breakthroughs.

Asia-Pacific is projected to register a 10.25% CAGR to 2030, making it the fastest-growing region. Rapid LNG infrastructure deployment, booming residential construction, and accelerating EV production converge to raise regional consumption sharply. Chinese institutes have introduced carbon-aerogel composites that withstand extreme temperatures while bearing structural loads, supporting domestic high-temperature industries.

Europe remains strong in regulatory leadership, leveraging EPBD revisions to encourage deep-energy retrofits that favor thin, high-R material systems. Pilot programs in social housing blocks showcase facade aerogel panels achieving 40% space-heating cuts while preserving exterior aesthetics. The Middle East and Africa continue to adopt aerogel in refining and petrochemical upgrades, while South America's growth is tied to LNG imports and rising green-building certification momentum.

- Acoustiblok, Inc.

- Active Aerogels

- Aerogel Technologies, LLC

- aerogel-it

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Blueshift Materials Inc.

- Cabot Corporation

- ENERSENS

- Guangdong Alison Technology Co., Ltd.

- Knauf Insulation

- Nano Tech Co., Ltd.

- Ningbo Surnano Aerogel Co., Ltd

- Porex

- Sino Aerogel

- Svenska Aerogel AB

- TAASI Corporation

- Thermablok Aerogels Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Adoption of Aerogel Due to Reusability and Recyclability

- 4.2.2 Rapidly Growing Construction Demand for High-performance Insulation

- 4.2.3 Energy-Efficiency Regulations Boosting EU and North-American Demand

- 4.2.4 Expansion of LNG Infrastructure Across Asia

- 4.2.5 Oil and Gas Industry Dominating the Aerogel Demand

- 4.3 Market Restraints

- 4.3.1 High Production Cost

- 4.3.2 Limited Availability of Raw Materials

- 4.3.3 Competition from High-performance Polymer Foams in Buildings

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Silica

- 5.1.2 Carbon

- 5.1.3 Alumina

- 5.1.4 Other Types

- 5.2 By Form

- 5.2.1 Blanket

- 5.2.2 Particle

- 5.2.3 Block

- 5.2.4 Panel

- 5.3 By Application

- 5.3.1 Thermal Insulation

- 5.3.2 Acoustic Insulation

- 5.3.3 Catalyst and Adsorbent

- 5.3.4 Battery and Energy Storage

- 5.3.5 Day-lighting and Translucent Panels

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Construction

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Aerospace

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Acoustiblok, Inc.

- 6.4.2 Active Aerogels

- 6.4.3 Aerogel Technologies, LLC

- 6.4.4 aerogel-it

- 6.4.5 Armacell

- 6.4.6 Aspen Aerogels, Inc.

- 6.4.7 BASF

- 6.4.8 Blueshift Materials Inc.

- 6.4.9 Cabot Corporation

- 6.4.10 ENERSENS

- 6.4.11 Guangdong Alison Technology Co., Ltd.

- 6.4.12 Knauf Insulation

- 6.4.13 Nano Tech Co., Ltd.

- 6.4.14 Ningbo Surnano Aerogel Co., Ltd

- 6.4.15 Porex

- 6.4.16 Sino Aerogel

- 6.4.17 Svenska Aerogel AB

- 6.4.18 TAASI Corporation

- 6.4.19 Thermablok Aerogels Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026年全球气凝胶市场报告

2026年全球气凝胶市场报告 全球热解凝胶绝缘材料市场按产品类型、材料成分、形态、应用、最终用途产业、分销管道和地区划分-市场规模、产业趋势、机会分析和预测(2026-2035年)

全球热解凝胶绝缘材料市场按产品类型、材料成分、形态、应用、最终用途产业、分销管道和地区划分-市场规模、产业趋势、机会分析和预测(2026-2035年) 气凝胶市场-全球产业规模、份额、趋势、机会及预测(按类型、形态、加工、应用、地区和竞争格局划分),2021-2031年

气凝胶市场-全球产业规模、份额、趋势、机会及预测(按类型、形态、加工、应用、地区和竞争格局划分),2021-2031年 二氧化硅气凝胶市场按产品类型、形态、干燥方法、应用和最终用途产业划分-2026-2032年全球预测二氧化硅气凝胶毯市场按产品类型、分销管道、终端用户产业和应用划分-2026-2032年全球预测气凝胶保温毯市场按形态、原料类型、最终用户、应用和分销管道划分-2026-2032年全球预测

二氧化硅气凝胶市场按产品类型、形态、干燥方法、应用和最终用途产业划分-2026-2032年全球预测二氧化硅气凝胶毯市场按产品类型、分销管道、终端用户产业和应用划分-2026-2032年全球预测气凝胶保温毯市场按形态、原料类型、最终用户、应用和分销管道划分-2026-2032年全球预测 全球气凝胶市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球气凝胶市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 气凝胶市场预测至2032年:按产品类型、形态、应用、最终用户和地区分類的全球分析

气凝胶市场预测至2032年:按产品类型、形态、应用、最终用户和地区分類的全球分析 气凝胶市场规模、份额和成长分析(按类型、形态、製造流程、应用、最终用途和地区划分)-2026-2033年产业预测全球生物基气凝胶市场:预测至2032年-按材料类型、应用、最终使用者和地区分類的分析

气凝胶市场规模、份额和成长分析(按类型、形态、製造流程、应用、最终用途和地区划分)-2026-2033年产业预测全球生物基气凝胶市场:预测至2032年-按材料类型、应用、最终使用者和地区分類的分析