|

市场调查报告书

商品编码

1850192

资料中心机柜:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Data Center Rack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

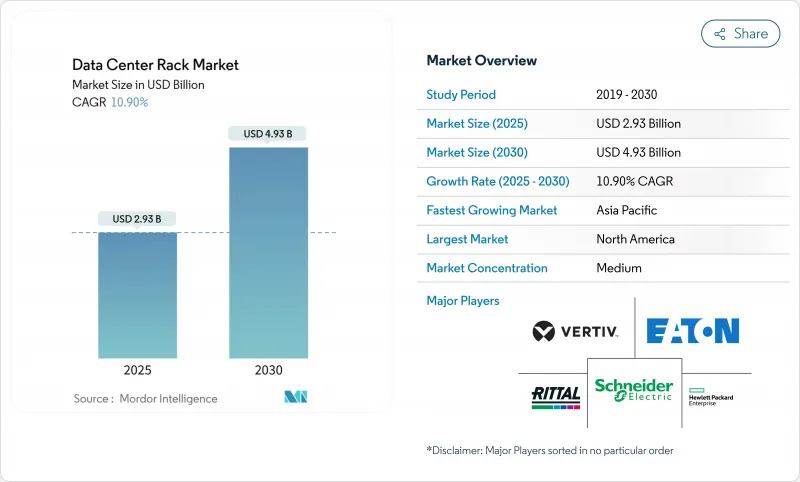

预计全球资料中心机柜市场规模到2025年将达到29.3亿美元,到2030年将达到49.3亿美元,复合年增长率为10.9%。

随着超大规模营运商、云端服务供应商和边缘配置将支援 40kW 及以上负载的机架级液体冷却和电力输送系统标准化,资料中心机柜市场正在不断扩张。营运商将机架基础设施视为人工智慧 (AI) 工作负载、高效能运算丛集和延迟敏感型边缘节点的实体基础。随着企业寻求最大化运算密度并改善温度控管,48U 高配置、机柜式存储和支援液体冷却的结构设计正成为主流。全部区域转向自主人工智慧、可再生能源安装和加强能源效率法规,进一步推动了对能够满足监管、永续性和可服务性目标的先进机架解决方案的需求。

全球资料中心机柜市场趋势与洞察

超大规模和主机託管建设激增

预计到2025年,美国超大规模资料中心的资本支出将超过270亿美元,年增69%,证实了资料中心建设是成长最快的非住宅领域。目前,单一GPU集群每机架需要10-140kW的功率,这迫使营运商重新设计围绕液体歧管而非传统空气处理系统的閒置频段布局。像Digital Realty这样的主机託管领导者正在部署支援AI的套件,每个机柜可维持70kW的功率,这表明高阶机架基础设施是其竞争优势。由于风冷机房的维修成本可能远远超过新建预算,此类扩建导致机柜级机架的订购週期长达数年。这一趋势也预示着超大规模资料中心营运商将转向超大规模资料中心业者自己的设施,以保持对训练和推理环境的控制。

云和边缘的采用将推动对机架的需求

企业越来越多地在工厂、仓库和零售店附近安装运算节点,这迫使供应商设计坚固耐用的机架。由于戴尔和 Switch 的合作,联邦快递在其物流中心内部署了边缘运算模组,这需要抗振机壳和远端管理的 PDU。像 Etisalat 这样的通讯业者正在部署安装在街道设施中的封闭式机柜中的紧凑型边缘运算伺服器,这表明 5G 将推动机架外形规格超越传统资料中心。像 3M 这样的製造商正在工业地板上使用 Azure SQL Edge,并要求使用符合 NEMA 标准的机架,以抵御灰尘和温度波动。因此,资料中心机柜市场正在加速发展,各个细分市场提供适用于数千个分散式站点的预先整合模组化解决方案。

能源效率法规(欧盟行为准则/ASHRAE)

欧盟能源效率指令修订版要求IT负载超过100kW的设施每年进行报告,并为PUE低至1.03的液体冷却系统提供奖励。美国暖气、冷气与空调工程师学会(ASHRAE)提高了允许的进气温度,并在机架保持气流密封的情况下启用了冷却器节热器模式。德国能源效率法案要求资料中心重复利用废热,并建议使用可将高等级热能传输到区域供热迴路的后门液体冷却器。随着营运商竞相在揭露截止日期前完成资讯揭露,整合合规机架的供应商正在享受更快的采购週期。

細項分析

到2024年,全机架将占据资料中心机柜市场的57.4%,超过其他尺寸,到2030年的复合年增长率为12.9%。这一份额代表了资料中心机柜市场规模的绝大部分,反映了超大规模资料中心营运商对42U机架的偏好,因为42U机架能够简化布线、气流和PDU标准化。人工智慧丛集将需要广泛的PCIe和NVLink互连,因此全机架对于保持100Gbps及以上讯号完整性的整洁布线至关重要。在改装机房中,更大的机架可以透过与现有冷通道几何形状对齐来最大限度地降低地砖重新配置的成本。

液体冷却扩展了全机架的优势,因为较高的垂直空间有利于冷却水的供水和回水分离。Schneider Electric的 GB200 NVL72 设计透过位于 42U 伺服器区域下方的客製化歧管,实现了每全机架 132kW 的功率。因此,资料中心机柜市场正在看到供应商在全高机柜中预先安装工厂整合的冷却迴路、冗余泵浦和快速断开接头。半机架和四分之一机架尺寸仍在边缘机柜和网路机房中使用,但由于这些环境很少需要复杂的 GPU 集群,其复合年增长率正在下降。

虽然42U机架在2024年占总营收的53.7%,但48U机架是成长最快的机架,到2030年的复合年增长率为12.1%。操作员看重6U的净空高度,因为它可以在不牺牲伺服器插槽的情况下容纳流体歧管、母线槽、架顶式交换器等设备。更高的高度减少了过道数量,在大型机房中最多可节省12%的占地面积。更高的机架也有助于平衡脚轮上的重量分布,当机柜在添加冷却剂后重量超过1,500公斤时,这一点至关重要。

Rittal 的 VX IT 系列允许 42U 和 48U 机架在通用导轨上混合使用,从而促进分阶段过渡以适应预算週期。客製化的 52U 和 54U 型号正在安装在具有充足垂直空间的高天花板仓库中,但其应用仍处于小众市场。随着液冷技术不断突破密度极限,资料中心机柜市场将 48U 视为兼顾传统相容性和麵向未来的容量的最佳选择。

资料中心机柜市场按机架尺寸(四分之一机架、半机架、全机架)、机架高度(42U、45U、其他)、机架类型(机柜(封闭式)机架、开放式机柜、壁挂式机架)、资料中心类型(主机和复合材料、超大规模和云端服务供应商资料中心、企业和边缘)、材料(复合钢和钢)、其他地区复合材料和其他地区。市场预测以美元计算。

区域分析

2024年,北美地区占总收入的32.6%,这得益于其深厚的超大规模生态系统、成熟的供应链和清晰的监管规定。 2025年,美国资料中心资本支出超过270亿美元,但公用事业拥挤限制了北维吉尼亚和硅谷的成长。加拿大正在加速利用水力发电的永续性型建设,而墨西哥则吸引近岸边缘节点来支持美国的延迟目标。本地製造业的扩张,例如Schneider Electric在田纳西州投资1.4亿美元的开关设备工厂,正在帮助供应商应对关税逆风。

亚太地区资料中心机柜市场的复合年增长率高达13.2%,是全球最快的地区。中国正在将其政府人工智慧基金投资于大型GPU基地;印度正在二线城市建设5-20MW的资料中心园区,以推动其数位服务业的蓬勃发展;日本则在支持工厂自动化的边缘丛集。区域製造中心缩短了机架的物流前置作业时间,但铜材短缺影响了成本波动。像Vertiv公司提供的iGenius人工智慧中心这样的计划,展现了国内供应生态系统如何努力满足区域运算需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 超大规模和主机託管激增

- 云端运算和边缘运算的兴起推动了机架需求

- 高密度伺服器部署(每个机架超过 40kW)

- 能源效率法规(欧盟行为准则/ASHRAE)

- AI优化的液冷机架架构

- 国家奖励国内货架製造

- 市场限制

- 高级橱柜需要较高的初始投资

- 刀片/片上伺服器模组的使用日益增多

- 大都会地区缺乏电力和空间

- 特殊钢和铝供应波动

- 供应链分析

- 监管格局

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争的激烈程度

- 替代品的威胁

- 评估市场中的宏观经济因素

第五章市场规模及成长预测

- 按机架尺寸

- 四分之一架

- 半架

- 全机架

- 按机架高度

- 42U

- 45U

- 48U

- 其他高度(52U 和定制)

- 按机架类型

- 机柜(封闭式)机架

- 开放式机柜

- 壁挂式置物架

- 依资料中心类型

- 主机代管设施

- 超大规模和云端服务供应商资料中心

- 企业和边缘

- 按材质

- 钢

- 铝

- 其他合金和复合材料

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Schneider Electric SE

- Vertiv Group Corp.

- Eaton Corp. plc

- Rittal GmbH and Co. KG

- Hewlett Packard Enterprise

- Dell Technologies Inc.

- Legrand SA

- IBM Corp.

- Chatsworth Products Inc.

- Panduit Corp.

- APC(by Schneider Electric)

- Tripp Lite(Eaton)

- Great Lakes Case and Cabinet

- Belkin International Inc.

- Kendall Howard LLC

- Martin International Enclosures

- Black Box Corp.

- Fujitsu Ltd.

- Oracle Corp.

- Cisco Systems Inc.

第七章 市场机会与未来展望

The global data center rack market size is expected to reach USD 2.93 billion in 2025 and is forecast to climb to USD 4.93 billion by 2030, advancing at a robust 10.9% CAGR.

The data center rack market is expanding because hyperscale operators, cloud service providers, and edge deployments are standardizing on rack-level liquid cooling and power delivery systems that support loads above 40 kW. Operators view rack infrastructure as the physical foundation for artificial intelligence (AI) workloads, high-performance computing clusters, and latency-sensitive edge nodes. Taller 48U configurations, cabinet-style containment, and liquid-ready structural designs are becoming mainstream as companies seek to maximize compute density while improving thermal management. The region-wide pivot toward sovereign AI, renewable-powered facilities, and stricter energy-efficiency rules further intensifies demand for advanced rack solutions capable of meeting regulatory, sustainability, and serviceability targets.

Global Data Center Rack Market Trends and Insights

Hyperscale and Colocation Build-outs Surge

Hyperscale capital spending topped USD 27 billion in the United States during 2025, reflecting 69% year-over-year growth that cements data-center construction as the fastest-expanding non-residential segment. Individual GPU clusters now demand 10-140 kW per rack, pushing operators to redesign white-space layouts around liquid manifolds versus legacy air handling. Colocation leaders such as Digital Realty introduced AI-ready suites that sustain 70 kW per cabinet, signalling that premium rack infrastructure is a competitive differentiator. Because retrofit costs for air-cooled halls can eclipse new-build budgets, these expansions fuel multiyear ordering cycles for cabinet-class racks. The trend also illustrates hyperscalers' shift toward owning facilities to preserve control of training and inference environments.

Rising Cloud and Edge Adoption Boosts Rack Demand

Enterprises are placing compute nodes next to factories, warehouses, and retail stores, compelling vendors to engineer ruggedized racks. FedEx deployed edge modules inside logistics hubs through a Dell-Switch collaboration that requires vibration-resistant enclosures and remote-management PDUs. Telecom operators like Etisalat are rolling out compact edge servers that mount in sealed cabinets installed on street furniture, illustrating how 5G pushes rack form factors beyond traditional data floors. Manufacturers such as 3M leverage Azure SQL Edge on industrial shop floors, demanding NEMA-rated racks that tolerate dust and temperature swings. Consequently, the data center rack market accelerates in segments that supply pre-integrated, modular solutions suitable for thousands of distributed sites.

Energy-Efficiency Regulations (EU Code of Conduct / ASHRAE)

The European Union's revised Energy Efficiency Directive mandates yearly reporting for facilities over 100 kW IT load, aligning incentives toward liquid cooling that can achieve PUE as low as 1.03. ASHRAE widened allowable inlet temperatures, enabling chiller-less economiser modes when racks maintain tight airflow containment. Germany's Energy Efficiency Act compels data centers to reuse waste heat, favouring rear-door liquid coolers that can transfer high-grade thermal energy to district-heating loops. Vendors integrating compliant racks enjoy accelerated procurement cycles as operators race to meet disclosure deadlines.

Other drivers and restraints analyzed in the detailed report include:

- High-Density Server Deployment (Greater Than 40 kW/rack)

- High Upfront Capex for Advanced Cabinets

- Power and Space Scarcity in Tier-1 Metros

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full racks delivered 57.4% of the data center rack market in 2024 and will outpace other sizes with a 12.9% CAGR to 2030. That share equates to a commanding portion of the data center rack market size and reflects hyperscalers' preference for 42U footprints that streamline cabling, airflow, and PDU standardisation. AI clusters demand sprawling PCIe and NVLink interconnects, making full racks indispensable for clean cable routing that sustains signal integrity at 100 Gbps and higher. In retrofit halls, larger frames also minimise floor-tile reconfiguration costs by aligning with existing cold-aisle geometry.

Liquid cooling magnifies full-rack advantages because taller vertical spaces facilitate segregated supply-and-return coolant channels. Schneider Electric's GB200 NVL72 blueprint achieves 132 kW per full rack through bespoke manifolds positioned below a 42U server zone. The data center rack market thus rewards vendors that deliver factory-integrated coolant loops, redundant pumps, and quick-disconnect couplings pre-installed within full-height cabinets. Half- and quarter-rack formats still serve edge closets and network rooms, yet their CAGR trails because these environments seldom require lavish GPU clusters.

Although 42U frames dominated 2024 with 53.7% revenue share, 48U variants are the fastest-growing height, posting 12.1% CAGR through 2030. Operators value the extra 6U for housing liquid manifolds, busways, or top-of-rack switches without sacrificing server slots. The incremental height reduces aisle count, yielding up to 12% floor-space savings in large halls. Taller frames also balance weight distribution across casters, vital when cabinets surpass 1,500 kilograms once coolant is added.

Rittal's VX IT line lets technicians mix 42U and 48U frames on common rails, easing phased migrations that align with budget cycles. Custom 52U or 54U models appear in high-ceiling warehouses where vertical clearance is plentiful, but adoption remains niche. With liquid cooling pushing density ceilings higher, the data center rack market regards 48U as the sweet spot between legacy compatibility and forward-looking capacity.

Data Center Rack Market is Segmented by Rack Size(Quartely Rack, Half Rack, Full Rack), Rack Height (42U, 45U and More), Rack Type(Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Racks), Data Center Type(Colocation Facilities, Hyperscale and Cloud Service Provider DCs, Enterprise and Edge), Material(steel, Aluminum, Other Alloys and Composites) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 32.6% of 2024 revenue thanks to deep hyperscale ecosystems, well-established supply chains, and regulatory clarity. Data-center capital expenditure surpassed USD 27 billion in the United States during 2025, though utility congestion in Northern Virginia and Silicon Valley tempers growth. Canada accelerates sustainability-centric builds that leverage hydro generation, while Mexico attracts near-shoring edge nodes supporting U.S. latency targets. Local manufacturing expansions, such as Schneider Electric's USD 140 million Tennessee plant for switchgear, help suppliers dodge tariff headwinds.

Asia-Pacific is advancing at a 13.2% CAGR, the fastest regional clip in the data center rack market. China channels sovereign AI funds into massive GPU bases, India's digital-services boom propels 5- to 20-MW campuses across tier-2 cities, and Japan backs edge clusters to automate factories. Regional fabrication hubs slash logistics lead times for racks, yet copper deficits could add cost volatility. Projects such as Vertiv-equipped iGenius AI centers illustrate how domestic supply ecosystems are rising to meet localised compute mandates.

- Schneider Electric SE

- Vertiv Group Corp.

- Eaton Corp. plc

- Rittal GmbH and Co. KG

- Hewlett Packard Enterprise

- Dell Technologies Inc.

- Legrand SA

- IBM Corp.

- Chatsworth Products Inc.

- Panduit Corp.

- APC (by Schneider Electric)

- Tripp Lite (Eaton)

- Great Lakes Case and Cabinet

- Belkin International Inc.

- Kendall Howard LLC

- Martin International Enclosures

- Black Box Corp.

- Fujitsu Ltd.

- Oracle Corp.

- Cisco Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale and colocation build-outs surge

- 4.2.2 Rising cloud and edge adoption boosts rack demand

- 4.2.3 High-density server deployment (greater than 40 kW/rack)

- 4.2.4 Energy-efficiency regulations (EU Code of Conduct / ASHRAE)

- 4.2.5 AI-optimised liquid-cooled rack architectures

- 4.2.6 National incentives for local rack manufacturing

- 4.3 Market Restraints

- 4.3.1 High upfront capex for advanced cabinets

- 4.3.2 Growing use of blade/server-on-chip modules

- 4.3.3 Power and space scarcity in tier-1 metros

- 4.3.4 Specialty steel and aluminium supply volatility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Rack Size

- 5.1.1 Quarter Rack

- 5.1.2 Half Rack

- 5.1.3 Full Rack

- 5.2 By Rack Height

- 5.2.1 42U

- 5.2.2 45U

- 5.2.3 48U

- 5.2.4 Other Heights (52U and Custom)

- 5.3 By Rack Type

- 5.3.1 Cabinet (Closed) Racks

- 5.3.2 Open-Frame Racks

- 5.3.3 Wall-Mount Racks

- 5.4 By Data Center Type

- 5.4.1 Colocation Facilities

- 5.4.2 Hyperscale and Cloud Service Provider DCs

- 5.4.3 Enterprise and Edge

- 5.5 By Material

- 5.5.1 Steel

- 5.5.2 Aluminum

- 5.5.3 Other Alloys and Composites

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Vertiv Group Corp.

- 6.4.3 Eaton Corp. plc

- 6.4.4 Rittal GmbH and Co. KG

- 6.4.5 Hewlett Packard Enterprise

- 6.4.6 Dell Technologies Inc.

- 6.4.7 Legrand SA

- 6.4.8 IBM Corp.

- 6.4.9 Chatsworth Products Inc.

- 6.4.10 Panduit Corp.

- 6.4.11 APC (by Schneider Electric)

- 6.4.12 Tripp Lite (Eaton)

- 6.4.13 Great Lakes Case and Cabinet

- 6.4.14 Belkin International Inc.

- 6.4.15 Kendall Howard LLC

- 6.4.16 Martin International Enclosures

- 6.4.17 Black Box Corp.

- 6.4.18 Fujitsu Ltd.

- 6.4.19 Oracle Corp.

- 6.4.20 Cisco Systems Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球智慧机架式电源分配单元 (PDU) 市场预测至 2034 年:按 PDU 类型、功能、插座类型、资料中心类型、通讯介面、最终用户和地区划分

全球智慧机架式电源分配单元 (PDU) 市场预测至 2034 年:按 PDU 类型、功能、插座类型、资料中心类型、通讯介面、最终用户和地区划分 资料中心机柜配电单元市场 - 全球产业规模、份额、趋势、机会、预测:测量与监控、部署模式、功率容量、区域及竞争格局,2021-2031年

资料中心机柜配电单元市场 - 全球产业规模、份额、趋势、机会、预测:测量与监控、部署模式、功率容量、区域及竞争格局,2021-2031年 机架式伺服器市场 - 2026-2031 年预测机架式伺服器市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、价格范围、最终用户产业、地区和竞争格局划分,2021-2031 年预测

机架式伺服器市场 - 2026-2031 年预测机架式伺服器市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、价格范围、最终用户产业、地区和竞争格局划分,2021-2031 年预测 日本资料中心机架市场报告(按类型、机架单元、机架尺寸、框架尺寸、框架设计、服务、应用、最终用户和地区划分,2026-2034 年)

日本资料中心机架市场报告(按类型、机架单元、机架尺寸、框架尺寸、框架设计、服务、应用、最终用户和地区划分,2026-2034 年) 全球资料中心趋势(2026):机架式解决方案

全球资料中心趋势(2026):机架式解决方案 互联网资料中心(IDC)机柜:全球市场份额和排名、总收入和需求预测(2025-2031年)

互联网资料中心(IDC)机柜:全球市场份额和排名、总收入和需求预测(2025-2031年) IT 配电单元市场(按类型、额定功率、相位、安装类型和最终用户产业)—2025-2030 年全球预测ORV3 机架市场按产品类型、机架高度、组件、部署模型、应用和销售管道划分 - 2025-2030 年全球预测全球资料中心机架市场按机架类型、设计、负载能力、材料、应用、最终用户和分销管道分類的预测(2025 年至 2030 年)

IT 配电单元市场(按类型、额定功率、相位、安装类型和最终用户产业)—2025-2030 年全球预测ORV3 机架市场按产品类型、机架高度、组件、部署模型、应用和销售管道划分 - 2025-2030 年全球预测全球资料中心机架市场按机架类型、设计、负载能力、材料、应用、最终用户和分销管道分類的预测(2025 年至 2030 年)