|

市场调查报告书

商品编码

1850244

堆垛机:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Palletizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

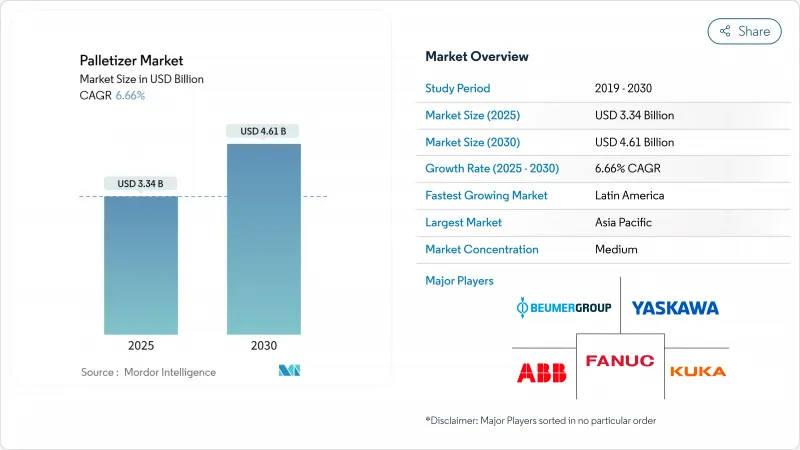

全球堆垛机市场预计到 2025 年将达到 33.4 亿美元,到 2030 年将达到 46.1 亿美元。

这一成长动能主要得益于托盘组装方式从人工转向自动化、软体主导系统的持续转变,这些转变解决了劳动力短缺问题,优化了拖车利用率,并满足了日益增长的电商处理容量要求。 SKU整合带来的溢价、人工智慧赋能的托盘堆迭、降低初始成本的租赁模式的快速普及,以及协作机器人在空间受限工厂中日益增长的吸引力,都进一步推动了成长。市场竞争强度仍然适中,没有一家公司的市占率超过15%,但随着区域整合商将机器人打包成订阅和机器人即服务(RaaS)协议,价格压力正在显现。南美洲正在经历最快的区域扩张,这得益于製造业回流和物流升级,以及政府的税收优惠政策。

全球堆垛机市场趋势与洞察

电子商务中 SKU 复杂性日益增加

目前,履约中心每年处理超过 1,800 亿箱货物,每个中心处理超过 5 万个 SKU。高阶平台可提供 30-40% 的更高利润率,同时由于优化了装载方式,减少了高达 30% 的空车厢空间,因此还能降低总运输成本。

劳动力短缺推动仓库自动化

中国41个工厂职位严重短缺,北美仓库15-20%的空缺率,使得自动化投资回报期缩短至18个月甚至更短。目前,中型工厂每小时仅能实现100台设备的自动化,而协作系统透过将员工重新部署到更安全、更高价值的岗位,正在释放堆垛机市场更大的潜力。

重型机械臂需要较高的初始投资。

重量超过150公斤的机械臂通常造价超过50万美元,对于日出货量低于500托盘的製造商来说,价格高昂,难以负担。像Formic这样的机器人即服务(RaaS)先驱企业正在透过每月3975美元的套餐来解决这一难题,但客製化和所有权方面仍然存在权衡取舍。

细分市场分析

到2024年,传统机器仍将维持48%的收入成长,因为每小时处理量超过1000箱的高速生产线依赖成熟的迭层设备。然而,协作式设备将以6.2%的复合年增长率超越堆垛机市场,吸引那些占地面积较小、渴望安全认证且无需围栏作业的待开发区的投资。多关节臂占据中等性能水平,兼顾吞吐量和换型灵活性,以适应混合产品系列。将迭层机与机器人拣选机结合的混合系统正在小众饮料和个人护理用品生产单元中涌现,但成本仍然过高。

供应商透过全端生态系统实现差异化竞争:斗山的 P 系列产品与 Rocketfarm 的 Pally 软体结合,可缩短部署时间并提高用户自主性。随着客户越来越重视单一来源的课责而非仅依赖硬件,供应商将视觉、模拟和生命週期服务捆绑在一起,从而扩大了堆垛机市场的潜在机会。

中型解决方案占了41.2%的市场份额,这反映出市场对50-150公斤消费品包装箱的偏好。然而,随着大批量货运商整合货物以降低人事费用,重型堆垛机系统的市场规模预计将以7.4%的复合年增长率成长。节能伺服架构和先进的安全扫描器使得180公斤级的协作机器人能够与员工协同工作,正如Bob's Red Mill的案例所示。这些功能使得重型协作机器人的价格比中型同类产品高出40-60%,但用户认为,减少堆高机作业次数和工伤赔偿索赔是物有所值的。

重量低于 50 公斤的轻型码垛单元适用于药品和电子产品行业,在这些行业中,无尘室合规性和精度比蛮力更为重要。针对堆垛机市场这一细分领域的供应商,采用 10 级洁净室和真空吸盘来保护高价商品,正经历着稳定但缓慢的成长。

区域分析

亚太地区将占2024年销售额的38%,光是中国一国到2022年就将安装全球52%的新机器人。目前,国内供应商占据了36%的国内市场份额,这推动了价格分布下降,并加速了其产品对二线工厂的渗透。日本生产了全球45%的机器人,并在393亿美元(437亿美元)政府供应链基金的支持下,已在2024年向物流、食品和製药业拨出73.5亿美元的订单。印度的生产连结奖励计划正在推动汽车和学名药工厂的自动化,但由于技能缺口,招聘仍然不均衡。

到2030年,南美洲的复合年增长率将达到8.1%,位居全球之首。巴西的食品和汽车产业正在推动托盘製造自动化,以满足出口合规要求。墨西哥积极拥抱近岸外包趋势,向美国市场供应免税商品,推动了对符合北美安全标准的机器人的需求。儘管宏观经济波动,阿根廷的谷物加工商仍在部署堆垛机,以稳定一吨重的散装袋,确保其在远洋运输中保持稳定。

北美和欧洲的成长主要由产能更新换代而非产能扩张所驱动。即将生效的欧盟法规2023/1230将促使供应商加强网路安全,并优先考虑拥有认证软体堆迭的供应商。在美国,製造业回流计画正在推动堆垛机市场的发展,中小製造商正在寻求灵活的协作机器人,以适应频繁的SKU轮换,并缓解农村地区劳动力老化带来的挑战。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务 SKU 复杂性日益增加

- 劳动力短缺推动仓库自动化

- 即插即用的协作机器人可提高包装线的投资报酬率

- 快速消费品产业日益增长的永续性需求推动了机器人混合货物码垛技术的发展。

- 利用人工智慧驱动的视觉系统提高堆垛机的运转率

- 将供应链迁回北美和欧盟以增强其韧性

- 市场限制

- 重型机械臂的初始投资较高

- 与传统MES/WMS整合的复杂性

- 欧盟协作机器人安全评估和认证出现延误

- 钢材和伺服马达的价格波动会延长投资回收期。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 定价分析

第五章 市场规模与成长预测

- 依产品类型

- 传统堆垛机

- 高位堆垛机

- 低位堆垛机

- 机器人堆垛机

- 直角坐标/龙门座标系

- 铰接式

- Scala

- 协作机器人(cobot)

- 混合式堆垛机

- 传统堆垛机

- 按负载容量

- 轻型(小于50公斤)

- 中型(50-150公斤)

- 重型(超过150公斤)

- 最终用户

- 食品/饮料

- 製药

- 个人护理和化妆品

- 化学品

- 电子商务与第三方物流

- 其他行业

- 按销售管道

- 直接OEM销售

- 系统整合商

- 售后改装与升级

- 出租/租赁

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- FANUC Corp.

- KUKA AG

- Yaskawa Electric Corp.

- BEUMER Group GmbH and Co. KG

- Honeywell Intelligrated

- Krones AG

- Sidel Group

- ABC Packaging

- Schneider Packaging

- Barry-Wehmiller(BW Packaging)

- Premier Tech Chronos

- MMCI Robotics

- Columbia Machine

- Fuji Yusoki

- Brenton Engineering

- Kawasaki Robotics

- Okura Yusoki

- Regal Rexnord Automation

- Sealed Air AUTOBAG

第七章 市场机会与未来展望

The global palletizer market stands at USD 3.34 billion in 2025 and is projected to reach USD 4.61 billion by 2030, reflecting a 6.66% CAGR over the forecast period.

Momentum comes from the sustained shift away from manual pallet building toward automated, software-driven systems that resolve labor shortages, optimize trailer utilization, and meet rising e-commerce throughput requirements. Growth is reinforced by the premium that mixed-SKU, AI-enabled palletizing commands, the rapid spread of rental models that lower upfront costs, and the expanding appeal of collaborative robots in space-constrained factories. Competitive intensity remains moderate: no single player holds more than 15% revenue, yet pricing pressure surfaces as regional integrators package robots with subscription or robotics-as-a-service contracts. South America registers the fastest regional expansion as reshoring and logistics upgrades intersect with government tax incentives; meanwhile APAC maintains volume leadership due to China's scale in robot production and deployme

Global Palletizer Market Trends and Insights

Growing e-commerce SKU complexity

Fulfilment centres now handle volumes that exceed 180 billion cases yearly, with single sites processing more than 50,000 SKUs-ten times the diversity typical of legacy retail hubs.Fixed-pattern equipment cannot keep up, prompting adoption of AI-powered systems such as the Lucas Warehouse Optimization Suite, which lifts palletizing efficiency 15-20% by balancing weight, fragility, and stackability in real time. Premium platforms fetch 30-40% higher margins but still lower total shipping cost as optimized loads cut empty trailer space by up to 30%.

Labor shortages accelerating warehouse automation

Critical staffing gaps across 41 factory occupations in China and 15-20% vacancy rates in North American warehouses have compressed automation payback to under 18 months. Mid-market plants now automate runs of just 100 units per hour, unlocking a broader palletizer market as collaborative systems redeploy employees to safer, higher-value roles.

High upfront CAPEX for heavy-payload robotic arms

Installations rated above 150 kg often top USD 500,000, a hurdle for manufacturers shipping fewer than 500 pallets daily. Robotics-as-a-service pioneers such as Formic counter this barrier with USD 3,975 monthly bundles, yet tradeoffs around customisation and ownership persist.

Other drivers and restraints analyzed in the detailed report include:

- Packaging-line ROI improvements from plug-and-play cobots

- Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing

- Integration complexity with legacy MES/WMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional machines retained 48% revenue in 2024 as high-speed lines exceeding 1,000 cases per hour depend on proven layer devices. Yet the palletizer market sees collaborative units outpace at 6.2% CAGR, capturing greenfield investments in small-footprint sites that crave safety-certified, fence-free operation. Robotic articulated arms occupy the mid-performance tier, balancing throughput against changeover flexibility for mixed product portfolios. Hybrid systems, blending layer formers with robotic pickers, emerge in niche beverage and personal-care cells but remain cost-intensive.

Vendors differentiate through full-stack ecosystems: Doosan's P-SERIES coupled with Rocketfarm's Pally software reduces deployment time and elevates user autonomy. As customers prioritise single-source accountability over stand-alone hardware, suppliers bundling vision, simulation, and lifecycle services widen addressable opportunities inside the palletizer market.

Medium-duty solutions dominated with 41.2% share, reflecting consumer goods' bias toward 50-150 kg boxes. However the palletizer market size for heavy-duty systems is slated to expand at a 7.4% CAGR as bulk shippers consolidate loads to curb labour and freight costs. Energy-efficient servo architectures and advanced safety scanners now let 180 kg cobots operate alongside staff, as seen in Bob's Red Mill installations. These capabilities command 40-60% price uplifts compared with mid-tier peers, yet users justify the premium through reduced forklift moves and lower workers' compensation claims.

Light-duty cells under 50 kg address pharmaceuticals and electronics, where cleanroom compliance and precision trump brute force. Vendors targeting this end of the palletizer market leverage class-10-rated enclosures and vacuum grippers to protect high-value items, maintaining a stable but slower growth profile.

The Palletizer Market is Segmented by Product (Conventional Palletizer, Robotic Palletizer), by Payload Capacity (Light-Duty, Medium-Duty, and Heavy-Duty), by End-User Vertical (Food & Beverages, Pharmaceuticals, Chemicals, E-Commerce and 3PL, and More), by Sales Channel (Direct OEM Sales, System Integrators, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

APAC held 38% of 2024 revenue, with China alone installing 52% of new global robots by 2022. Domestic suppliers now secure 36% of their home market, pushing price points lower and accelerating diffusion among tier-two factories. Japan built 45% of the world's robots and channelled USD 7.35 billion in 2024 orders into logistics, food, and pharma lines, backed by a USD 39.3 billion (USD 43.7 billion) government supply-chain fund . India's Production-Linked Incentive schemes spark automation across automotive and generics plants, though adoption pockets remain uneven due to skill gaps.

South America records the strongest 8.1% CAGR trajectory to 2030 as Brazil's food and auto sectors automate pallet building for export compliance. Mexico rides near-shoring trends to supply the US market with tariff-proof goods, intensifying demand for robots certified to North American safety codes. Argentina's grain processors install palletizers that stabilise 1-tonne bulk bags for long ocean voyages despite macroeconomic volatility.

North America and Europe show measured growth driven by replacement rather than capacity additions. Upcoming Regulation (EU) 2023/1230 compels vendors to harden cybersecurity, advantaging those with certified software stacks. US reshoring programs lift the palletizer market as SMB manufacturers seek flexible cobots that accommodate frequent SKU changeovers and mitigate labour constraints in ageing rural workforces.

- ABB Ltd.

- FANUC Corp.

- KUKA AG

- Yaskawa Electric Corp.

- BEUMER Group GmbH and Co. KG

- Honeywell Intelligrated

- Krones AG

- Sidel Group

- A-B-C Packaging

- Schneider Packaging

- Barry-Wehmiller (BW Packaging)

- Premier Tech Chronos

- MMCI Robotics

- Columbia Machine

- Fuji Yusoki

- Brenton Engineering

- Kawasaki Robotics

- Okura Yusoki

- Regal Rexnord Automation

- Sealed Air AUTOBAG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce SKU complexity

- 4.2.2 Labor shortages accelerating warehouse automation

- 4.2.3 Packaging-line ROI improvements from plug-and-play cobots

- 4.2.4 Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing

- 4.2.5 AI-driven vision systems boosting palletizer uptime

- 4.2.6 Resilience re-shoring of supply chains in North America and EU

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for heavy-payload robotic arms

- 4.3.2 Integration complexity with legacy MES/WMS

- 4.3.3 Safety-rating certification delays for cobots in EU

- 4.3.4 Volatile steel & servo-motor prices widening payback periods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Conventional Palletizer

- 5.1.1.1 High-Level Palletizer

- 5.1.1.2 Low-Level Palletizer

- 5.1.2 Robotic Palletizer

- 5.1.2.1 Cartesian/Gantry

- 5.1.2.2 Articulated

- 5.1.2.3 SCARA

- 5.1.2.4 Collaborative (Cobot)

- 5.1.3 Hybrid Palletizer

- 5.1.1 Conventional Palletizer

- 5.2 By Payload Capacity

- 5.2.1 Light-Duty (<50 kg)

- 5.2.2 Medium-Duty (50-150 kg)

- 5.2.3 Heavy-Duty (>150 kg)

- 5.3 By End-user Vertical

- 5.3.1 Food & Beverages

- 5.3.2 Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Chemicals

- 5.3.5 E-commerce and 3PL

- 5.3.6 Other Verticals

- 5.4 By Sales Channel

- 5.4.1 Direct OEM Sales

- 5.4.2 System Integrators

- 5.4.3 After-market Retrofits and Upgrades

- 5.4.4 Rental / Leasing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 ABB Ltd.

- 6.4.2 FANUC Corp.

- 6.4.3 KUKA AG

- 6.4.4 Yaskawa Electric Corp.

- 6.4.5 BEUMER Group GmbH and Co. KG

- 6.4.6 Honeywell Intelligrated

- 6.4.7 Krones AG

- 6.4.8 Sidel Group

- 6.4.9 A-B-C Packaging

- 6.4.10 Schneider Packaging

- 6.4.11 Barry-Wehmiller (BW Packaging)

- 6.4.12 Premier Tech Chronos

- 6.4.13 MMCI Robotics

- 6.4.14 Columbia Machine

- 6.4.15 Fuji Yusoki

- 6.4.16 Brenton Engineering

- 6.4.17 Kawasaki Robotics

- 6.4.18 Okura Yusoki

- 6.4.19 Regal Rexnord Automation

- 6.4.20 Sealed Air AUTOBAG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

堆垛机市场:依自动化程度、技术、包装材料类型、装载能力、最终用途产业和应用划分-2026-2032年全球市场预测

堆垛机市场:依自动化程度、技术、包装材料类型、装载能力、最终用途产业和应用划分-2026-2032年全球市场预测 自动化堆垛机和堆垛机市场规模、份额和成长分析(按设备类型、最终用户产业、操作模式、系统配置和地区划分)-2026-2033年产业预测

自动化堆垛机和堆垛机市场规模、份额和成长分析(按设备类型、最终用户产业、操作模式、系统配置和地区划分)-2026-2033年产业预测 2026年全球堆垛机市场报告

2026年全球堆垛机市场报告 欧洲堆垛机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲堆垛机:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 堆垛机市场规模、份额和成长分析(按技术、产品类型、装载能力、产业垂直领域、销售管道和地区划分)-2026-2033年产业预测

堆垛机市场规模、份额和成长分析(按技术、产品类型、装载能力、产业垂直领域、销售管道和地区划分)-2026-2033年产业预测 堆垛机:全球市场份额和排名、总收入和需求预测(2025-2031年)机器人码高机和卸载机:全球市场份额和排名、总收入和需求预测(2025-2031年)

堆垛机:全球市场份额和排名、总收入和需求预测(2025-2031年)机器人码高机和卸载机:全球市场份额和排名、总收入和需求预测(2025-2031年) 托盘搬运设备市场规模、份额和趋势分析报告:按产品类型、自动化程度、最终用途、地区和细分市场预测(2025-2033 年)

托盘搬运设备市场规模、份额和趋势分析报告:按产品类型、自动化程度、最终用途、地区和细分市场预测(2025-2033 年) 全球机器人堆垛机和堆垛机市场

全球机器人堆垛机和堆垛机市场 机器人码垛机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

机器人码垛机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测