|

市场调查报告书

商品编码

1910428

欧洲堆垛机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Palletizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

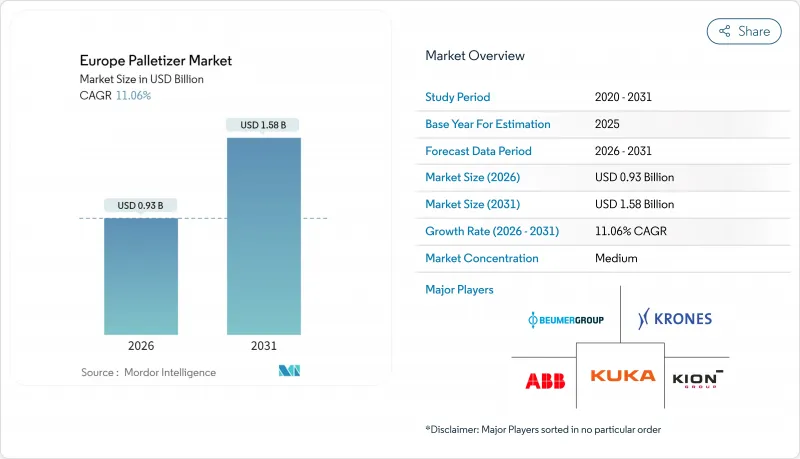

欧洲堆垛机市场预计将从 2025 年的 8.4 亿美元成长到 2026 年的 9.3 亿美元,预计到 2031 年将达到 15.8 亿美元,2026 年至 2031 年的复合年增长率为 11.06%。

这一两位数的成长轨迹反映了该地区向自动化包装的果断转型,旨在应对劳动力严重短缺、工资上涨和更严格的安全法规等挑战。节能自动化与碳中和物流目标相契合,进一步加速了采购决策,尤其是在各国政府将奖励与永续性成果挂钩的情况下。製造商也将码垛视为工业4.0广泛部署的基础技术。这是因为机器能够收集生产数据,为预测性维护模型提供信息,并能轻鬆整合到仓库管理系统(WES)中。竞争日益激烈,全球机器人製造商、欧洲专业整合商以及采用新型租赁模式的参与企业都将目标瞄准了传统上依赖人工堆迭的中型工厂。最后,随着电子商务履约中心和温控药品分销网路对高吞吐量的需求,欧洲堆垛机市场正从传统的工厂车间扩展到物流环境。

欧洲堆垛机市场趋势与洞察

食品饮料加工产业自动化包装生产线的扩建

食品饮料製造商正将堆迭定位为一个整合流程,而非下游附加环节。码垛线直接与上游灌装机对接,在不增加人工干预的情况下提高了产量。这种方法既能保障产品卫生,又能满足零售商对大批量混合包装的需求。设备製造商也积极回应,推出了符合卫生标准的不銹钢卫生夹具和易于清洁的表面。视觉模组可在出货前采集箱码,进而增强可追溯性。堆垛机收集的数据还有助于管理产品召回,并提高工厂的合规性。由于托盘是根据即时订单而非固定批次时间发货,操作人员反映瓶颈现象减少。

西欧人事费用上升和劳动短缺

西欧劳动力老化导致重复性包装工作的空缺率达到历史新高,迫使工厂竞相提高工资以争夺稀缺劳动力。管理人员现在将生产损失纳入投资回收期计算,结果显示,机器人码垛机可以在18到24个月内收回成本,而不是传统的三年。早期采用者享受了更高的运转率和稳定的产量,这转化为客户交货评分的提高。劳动力短缺正在促使经营团队主管讨论自动化的重点从“需要”转向“实施速度”,从而缩短了决策週期。培训供应商正在帮助采购商克服人才短缺问题,并确保重复订单。

全自动系统需要高额资本投入。

具备输送机装载、拉伸包装和贴标功能的全系列堆垛机价格可能超过一条完整的填充线,令许多中小型工厂望而却步。东欧企业的高昂借贷成本进一步拉大了与西方同行之间的差距。为了因应这一局面,供应商开始推出租赁和设备即服务(EaaS)模式,推动企业从资本支出转向营运支出。与工人共用空间的协作单元也透过避免安保和土建费用来降低计划成本。虽然这些方案扩大了设备的普及范围,但它们缺乏顶级系统的纯粹吞吐量,因此对于高产量工厂而言,这需要权衡取舍。

细分市场分析

预计到2025年,机器人堆垛机将占据欧洲堆垛机市场50.85%的份额,年复合成长率(CAGR)为12.89%,这主要得益于安全人机协作技术的进步和编码工具的简化。无需机械改造即可灵活切换不同SKU的柔软性,对于产品系列多样化的工厂而言堪称理想之选。传统机器在超高产量饮料生产线中依然发挥着重要作用,其机械致动器能够实现无与伦比的每小时循环次数。混合平台将机械层压成型器与机器人角柱结合,在保持柔软性的同时,也满足了稳定性要求。预计在2025年进行试验的第二代协作机器人,其最大举重能力可达25公斤,从而开闢了以往需要大型封闭式机器人才能应用的新领域。随着服务模式的日趋成熟,机器人供应商开始提供打包式运作保证,从而降低营运风险,并推动欧洲堆垛机市场在独立买家群体中不断扩张。

部署速度也是一个重要因素。预製单元以即插即用的撬装形式交付,可在数天而非数月内试运行。智慧安全扫描器取代了硬质围栏,释放了宝贵的占地面积。机器人操作软体为生产线主管提供即时OEE分析。供应商目前正透过OT-IT融合实现差异化,将托盘与ERP发货数据关联起来,从而实现可追溯性。这些数位化连接能力使机器人系统成为工厂数位化的“特洛伊木马”,巩固了其在欧洲堆垛机行业的主导地位。

疫情暴露了人工作业的瓶颈,製药厂正转向自动化。在低温运输法规的推动下,从管瓶到托盘的整个流程都必须严格控制,预计到2031年,该行业将以12.95%的复合年增长率增长。机器人能够在冷藏室中可靠运作,并整合序列化摄影机,记录每个纸箱的ID。到2025年,食品饮料行业将占据欧洲堆垛机市场32.70%的最大份额,因为大批量瓶装生产商和零食製造商需要持续生产以满足零售货架的需求。肉类和乳製品行业的交叉污染预防法规也促使人们青睐能够承受高强度清洁的不銹钢机器人夹具。

个人护理和化妆品公司正在部署堆垛机来处理与电商促销相关的季节性组合包装。高阶产品需要投资温和的真空吸盘工具来防止纸箱磨损。在化学产业,为了满足安全标准,增加防爆外壳和防静电组件,从而催生了对专业整合商的利基市场需求。供应商根据不同的应用情境客製化承包单元,从而降低验证的复杂性,并扩大欧洲堆垛机市场的潜在客户群。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 食品饮料加工产业自动化包装生产线的扩张

- 西欧人事费用上升和劳动短缺

- 日益严格的职场安全法规推动了机器人堆垛机的应用

- 电子商务的快速成长正在推动对高容量仓库的需求。

- 在中型工厂引入协同式码垛单元

- 碳中和物流中心对节能型堆垛机的需求

- 市场限制

- 全自动系统需要高额资本投入。

- 由于复杂的机电一体化集成,存在停机风险。

- 多轴机器人熟练程式设计师短缺

- 托盘尺寸越来越多样化,使得标准单元设计更加复杂。

- 产业供应链分析

- 监管环境

- 宏观经济因素如何影响市场

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

第五章 市场规模与成长预测

- 按类型

- 传统的

- 机器人

- 按最终用户行业划分

- 食品/饮料

- 製药

- 个人护理及化妆品

- 化学品

- 透过系统配置

- 在线连续堆垛机

- 层压堆垛机

- 龙门式/机械臂堆垛机

- 按载重能力

- 10公斤或以下

- 11~30 kg

- 超过30公斤

- 按自动化级别

- 半自动

- 全自动

- 按国家/地区

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd

- Beumer Group GmbH and Co. KG

- KION Group AG(Dematic)

- Krones AG

- Kuka AG

- Honeywell International Inc.

- AetnaGroup SpA

- Concetti SpA

- Fuji Robotics Americas Inc.

- FANUC Europe Corporation SA

- Yaskawa Europe GmbH

- Sidel Group

- Ocme Srl

- Gebo Cermex

- Kawasaki Robotics GmbH

- Premier Tech Systems and Automation

- Columbia Machine Inc.

- MSK Verpackungs-Systeme GmbH

- Scott Automation NV

- Ehcolo A/S

- Bastian Solutions LLC

第七章 市场机会与未来展望

The Europe Palletizer market is expected to grow from USD 0.84 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at 11.06% CAGR over 2026-2031.

This double-digit trajectory mirrors the region's decisive shift toward automated packaging, which addresses acute labor shortages, rising wages, and tighter safety regulations that favor robotic over manual handling. Energy-efficient automation that aligns with carbon-neutral logistics goals further accelerates purchasing decisions, especially when governments link incentives to sustainability outcomes. Manufacturers also view palletizing as a gateway technology for broader Industry 4.0 rollouts because the machines collect production data, feed predictive maintenance models, and integrate easily with warehouse execution systems. Competitive intensity is rising as global robot makers, European specialist integrators, and new rental-model disruptors all target mid-sized factories that historically relied on manual stacking. Finally, e-commerce fulfillment hubs and temperature-controlled pharmaceutical chains create high-throughput requirements that expand the Europe Palletizer market into logistics environments beyond the traditional factory floor.

Europe Palletizer Market Trends and Insights

Expansion of Automated Packaging Lines in Food and Beverage Processing

Food and beverage producers now treat palletizing as an integrated step rather than a downstream add-on. Lines link directly to upstream fillers, so throughput rises without extra human touches, an approach that protects product hygiene and matches retailer demand for high-volume mixed packs. Equipment builders respond with stainless-steel hygienic grippers and easy-wash surfaces that meet sanitation codes. Vision modules add traceability by capturing case codes before loads leave the plant. Data captured at the palletizer also supports recall management, providing factories with a compliance advantage. Operators report fewer bottlenecks because pallets exit in rhythm with real-time orders, rather than fixed batch windows.

Labor Cost Escalation and Scarcity Across Western Europe

Western Europe's aging workforce is pushing vacancy rates in repetitive packaging roles to record highs, forcing plants to compete for scarce labor at rapidly rising wages. Managers now factor lost production into payback calculations, revealing that robotic palletizers recoup their costs in 18-24 months, instead of the earlier three-year norm. Early adopters enjoy higher uptime and stable output, which translates into better customer delivery scores. The labor gap also shifts board-level conversations from "whether" to "how fast" to automate, shortening decision cycles. Vendors who bundle training help buyers overcome talent gaps and secure repeat orders.

High Capital Expenditure for Fully Automatic Systems

Full-line palletizers with conveyor in-feed, stretch wrapping, and labeling can exceed the price of an entire filling line, which places them out of reach for many small plants. Eastern European firms face higher borrowing costs, widening the gap with Western peers. In response, suppliers launch rental and equipment-as-a-service models that shift spend from capex to opex. Collaborative units that share space with workers also lower project costs because they avoid the costs of guarding and civil works. These options broaden access, yet cannot match the raw throughput of top-tier systems, leaving a trade-off at higher-volume sites.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Workplace Safety Regulations Favouring Robotic Palletizers

- E-Commerce Boom Driving High-Throughput Warehousing Needs

- Downtime Risk Due to Complex Mechatronic Integrations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Robotic palletizers accounted for 50.85% of the European palletizer market size in 2025 and are expected to grow at a 12.89% CAGR, driven by advances in safe human-robot collaboration and simplified coding tools. The flexibility to switch SKUs without mechanical changes suits plants with varied product portfolios. Conventional machines stay relevant in ultra-high-volume beverage lines where mechanical actuators deliver unmatched cycles per hour. Hybrid platforms now merge mechanical layer formers with robotic corner posts to meet stability demands while preserving flexibility. Second-generation cobots, tested in 2025, can lift to 25 kg, opening up new use cases that once required larger, fenced robots. As service models mature, robot suppliers bundle uptime guarantees that lower operational risk and expand the European Palletizer market among cautious buyers.

Implementation speed is another drawback. Pre-engineered cells arrive as plug-and-play skids, enabling commissioning within days instead of months. Smart safety scanners often replace hard fences, freeing up valuable floor space. Robot operating software also feeds line supervisors with live OEE analytics. Vendors now differentiate through OT-IT convergence by linking pallets to ERP dispatch data for traceability. These digital hooks make robotic systems a Trojan horse for wider factory digitalization, reinforcing their leadership in the European Palletizer industry.

Pharmaceutical plants have pivoted to automation after the pandemic exposed bottlenecks in manual handling. The segment is expected to advance at a 12.95% CAGR to 2031, driven by cold-chain regulations that mandate controlled handling from vial to pallet. Robots operate reliably in chilled rooms and integrate serialization cameras that record every carton ID. Food and beverage retained the largest 32.70% share of the European palletizer market size in 2025, as high-volume bottlers and snack makers require continuous output for retail shelves. Cross-contamination rules in the meat and dairy industries also favor stainless-steel robotic grippers that can withstand aggressive washdowns.

Personal care and cosmetics firms adopt palletizers to handle seasonal variety packs driven by e-commerce promotions. Their premium products justify investment in gentle vacuum tooling that prevents carton scuffing. The chemicals sector adds explosive-proof enclosures and antistatic components to meet safety codes, creating niche demand for specialized integrators. With each use case, suppliers tailor turnkey cells that reduce validation complexity and expand the addressable European palletizer market.

The Europe Palletizer Market Report is Segmented by Type (Conventional, Robotic), End-User Industry (Food and Beverages, Pharmaceuticals, and More), System Configuration (Inline, Layer, Gantry/Robotic Arm), Load Capacity (Up To 10 Kg, 11-30 Kg, Above 30 Kg), Automation Level (Semi-Automatic, Fully Automatic), and Geography (Germany, United Kingdom, Italy, Spain, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd

- Beumer Group GmbH and Co. KG

- KION Group AG (Dematic)

- Krones AG

- Kuka AG

- Honeywell International Inc.

- AetnaGroup SpA

- Concetti SpA

- Fuji Robotics Americas Inc.

- FANUC Europe Corporation S.A.

- Yaskawa Europe GmbH

- Sidel Group

- Ocme S.r.l.

- Gebo Cermex

- Kawasaki Robotics GmbH

- Premier Tech Systems and Automation

- Columbia Machine Inc.

- MSK Verpackungs-Systeme GmbH

- Scott Automation NV

- Ehcolo A/S

- Bastian Solutions LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of automated packaging lines in food and beverage processing

- 4.2.2 Labour cost escalation and scarcity across Western Europe

- 4.2.3 Heightened workplace safety regulations favouring robotic palletizers

- 4.2.4 E-commerce boom driving high-throughput warehousing needs

- 4.2.5 Adoption of collaborative palletizing cells in mid-sized plants

- 4.2.6 Carbon-neutral logistics hubs demanding energy-efficient palletizers

- 4.3 Market Restraints

- 4.3.1 High capital expenditure for fully automatic systems

- 4.3.2 Downtime risk due to complex mechatronic integrations

- 4.3.3 Shortage of skilled programmers for multi-axis robots

- 4.3.4 Rising pallet size diversity complicating standard cell design

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Conventional

- 5.1.2 Robotic

- 5.2 By End-user Industry

- 5.2.1 Food and Beverages

- 5.2.2 Pharmaceuticals

- 5.2.3 Personal Care and Cosmetics

- 5.2.4 Chemicals

- 5.3 By System Configuration

- 5.3.1 Inline Palletizers

- 5.3.2 Layer Palletizers

- 5.3.3 Gantry / Robotic Arm Palletizers

- 5.4 By Load Capacity

- 5.4.1 Up to 10 kg

- 5.4.2 11 - 30 kg

- 5.4.3 Above 30 kg

- 5.5 By Automation Level

- 5.5.1 Semi-automatic

- 5.5.2 Fully Automatic

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 France

- 5.6.3 United Kingdom

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Netherlands

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Beumer Group GmbH and Co. KG

- 6.4.3 KION Group AG (Dematic)

- 6.4.4 Krones AG

- 6.4.5 Kuka AG

- 6.4.6 Honeywell International Inc.

- 6.4.7 AetnaGroup SpA

- 6.4.8 Concetti SpA

- 6.4.9 Fuji Robotics Americas Inc.

- 6.4.10 FANUC Europe Corporation S.A.

- 6.4.11 Yaskawa Europe GmbH

- 6.4.12 Sidel Group

- 6.4.13 Ocme S.r.l.

- 6.4.14 Gebo Cermex

- 6.4.15 Kawasaki Robotics GmbH

- 6.4.16 Premier Tech Systems and Automation

- 6.4.17 Columbia Machine Inc.

- 6.4.18 MSK Verpackungs-Systeme GmbH

- 6.4.19 Scott Automation NV

- 6.4.20 Ehcolo A/S

- 6.4.21 Bastian Solutions LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

堆垛机市场:依自动化程度、技术、包装材料类型、装载能力、最终用途产业和应用划分-2026-2032年全球市场预测

堆垛机市场:依自动化程度、技术、包装材料类型、装载能力、最终用途产业和应用划分-2026-2032年全球市场预测 自动化堆垛机和堆垛机市场规模、份额和成长分析(按设备类型、最终用户产业、操作模式、系统配置和地区划分)-2026-2033年产业预测

自动化堆垛机和堆垛机市场规模、份额和成长分析(按设备类型、最终用户产业、操作模式、系统配置和地区划分)-2026-2033年产业预测 2026年全球堆垛机市场报告

2026年全球堆垛机市场报告 堆垛机市场规模、份额和成长分析(按技术、产品类型、装载能力、产业垂直领域、销售管道和地区划分)-2026-2033年产业预测

堆垛机市场规模、份额和成长分析(按技术、产品类型、装载能力、产业垂直领域、销售管道和地区划分)-2026-2033年产业预测 堆垛机:全球市场份额和排名、总收入和需求预测(2025-2031年)机器人码高机和卸载机:全球市场份额和排名、总收入和需求预测(2025-2031年)

堆垛机:全球市场份额和排名、总收入和需求预测(2025-2031年)机器人码高机和卸载机:全球市场份额和排名、总收入和需求预测(2025-2031年) 托盘搬运设备市场规模、份额和趋势分析报告:按产品类型、自动化程度、最终用途、地区和细分市场预测(2025-2033 年)

托盘搬运设备市场规模、份额和趋势分析报告:按产品类型、自动化程度、最终用途、地区和细分市场预测(2025-2033 年) 全球机器人堆垛机和堆垛机市场

全球机器人堆垛机和堆垛机市场 堆垛机:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

堆垛机:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 机器人码垛机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

机器人码垛机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测