|

市场调查报告书

商品编码

1850359

客户分析:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Customer Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

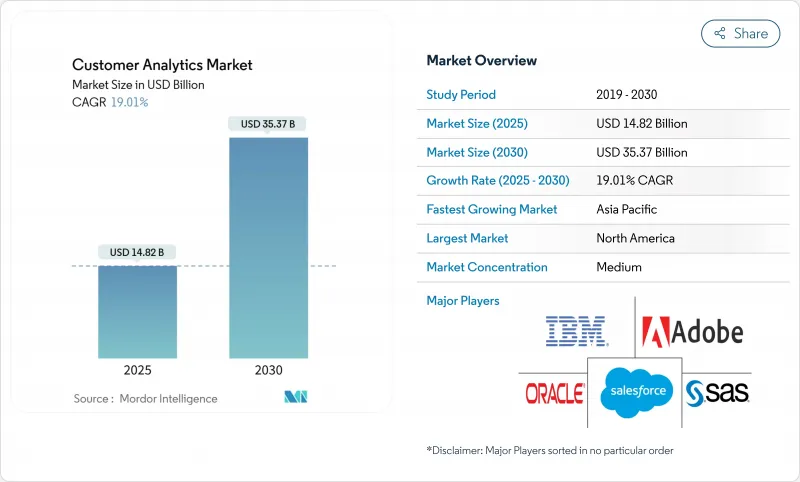

客户分析市场预计到 2025 年将达到 148.2 亿美元,到 2030 年将达到 353.7 亿美元,复合年增长率为 19.01%。

随着企业转向数据主导互动,取代高成本的大众行销并整合分散的数位接点,扩充性正在加速提升。云端部署仍然是主流架构,因为企业倾向于采用可扩展的按需付费模式,从而避免计量收费支出。然而,随着企业寻求自动化洞察生成,人工智慧驱动的模组正日益受到关注。垂直领域的扩张仍在继续,不仅在零售业,而且在医疗保健等高度监管的行业也是如此,在这些行业中,分析技术支援合规性和个人化医疗服务。随着平台供应商将分析功能嵌入现有应用程式以锁定客户并保护市场份额免受规模较小的专业竞争对手的衝击,竞争日趋激烈。同时,资料主权法规和人才短缺迫使企业重新架构或寻求外部专家支持,从而限制了短期业务扩张。

全球客户分析市场趋势与洞察

对高度个人化客户体验的需求日益增长

不断攀升的获客成本迫使企业将客户留存置于首位,个人化也从行销目标提升为核心营运原则。 Adobe 的一项研究发现,71% 的消费者希望品牌能预测他们的需求,但只有不到 40% 的企业能够大规模地做到这一点。串流媒体服务供应商正在展现这种影响:Netflix 将约 80% 的用户参与度归功于其数据驱动的建议引擎,该引擎能够根据即时行为讯号进行调整。饭店业者也正在响应这一转变,近九成饭店正在实施人工智慧增强的客户互动,以获取更高的住宿。高品质洞察与收益提升之间的联繫正在推动各行业对高级细分、倾向性建模和最佳行动引擎的投资,从而推动整个客户分析市场的成长。

云端原生分析降低中小企业的总拥有成本

中小企业正越来越多地采用云端服务,因为订阅模式可以省去大笔资本支出并缩短引进週期。美国调查发现,许多中小企业每年在技术方面的支出在 1 万至 4.9 万美元之间,这使得可扩展的计量收费分析服务在经济上极具吸引力。公共云端供应商预测,到 2028 年,支出将超过 1 兆美元,企业架构师报告称,到 2025 年,85% 的新工作负载将遵循云端优先原则。 40% 的欧洲中型企业表示,财务问题是数位化计划的障碍,而云端平台正在透过将固定成本转化为营运费用来弥合这一差距。

数据主权法划分了全球运营

各国政府正收紧对个人资料储存和跨境传输的管控,迫使跨国公司建构区域特定的技术堆迭和重复的资料管道。美国司法部禁止从相关国家存取美国敏感资料的规定便是这项转变的例证。企业架构师必须权衡GDPR、云端法规以及亚太地区不同的居住义务,通常选择在地化处理而非集中式处理。这延缓了统一客户视图计划的推进,也阻碍了客户分析在复杂营运模式下的市场普及。

细分市场分析

预计到2024年,云端解决方案将占总营收的62%,并在2030年之前以21.40%的复合年增长率成长。云端采用市场呈现细分趋势,预计2030年,各细分市场的规模将超过250亿美元。儘管金融和公共部门机构仍然固守本地部署环境,对延迟和资料驻留进行严格控制,但它们也在投资混合云方案,将敏感资料保留在本地,同时将繁重的运算任务卸载到公共云端。微软报告称,Azure在2025年第三季实现了35%的成长,其中近一半的营收成长归功于支援即时细分和趋势建模的人工智慧服务。 Oracle与Oracle的多重云端协定表明,曾经的竞争对手平台正在相互融合,以满足企业对灵活分析迁移路径的需求。

迁移到云端的公司正在经历更快的实验週期。资料团队推出沙盒环境,并在模型检验完成后解锁。订阅定价模式将前期投资转化为营运成本,从而简化了预算核准流程,尤其对中小企业而言更是如此。随着供应商采用特定产业的合规蓝图,受监管行业的分析工作负载也在转变,这进一步扩大了客户分析市场。

到2024年,仪錶板彙报软体将占总收入的27%。然而,人工智慧驱动的模组到2030年将以24.60%的复合年增长率成长,成为客户分析市场中成长最快的部分。这些引擎能够自动完成特征工程、模型选择和场景分析,从而缩短从原始资料到可执行洞察的路径。 Adobe已在其数位体验套件中整合了生成式人工智慧,预计到2024年将创造53.7亿美元的收入。

客户之声、社群媒体和网路分析应用仍在不断发展各自的专业应用场景,但它们正逐渐整合到更广泛的客户资料平台之下,这些平台集中处理模式、授权和身分解析。 ETL 工具正从批量整合演变为即时管道,可在数秒内刷新特征存储,使内容和定价引擎能够在即时互动中根据客户情境做出回应。在这些流程中直接实现资料品质和管治自动化的供应商,将在日益严格的隐私审查下脱颖而出。

客户分析市场按部署类型(本地部署、云端部署)、解决方案(社交媒体分析工具、网站分析工具等)、组织规模(中小企业、大型企业)、服务(託管服务、专业服务)、最终用户行业(通讯和IT、旅游和酒店等)以及地区进行细分。市场预测以美元(USD)计价。

区域分析

北美地区在人工智慧领域的支出占据主导地位,这得益于其高度普及的云端运算、成熟的资料科学人才储备以及强劲的创业投资资金——预计到2024年,人工智慧新创公司将获得超过1091亿美元的投资。供应商利用遍布美国和加拿大的密集资料中心,为即时个人化宣传活动提供低延迟推理。监管政策相对灵活,但各州的隐私权法要求区域性的使用者同意管理。随着零售商寻求深入了解全通路购物者的行为,墨西哥新兴的电子商务生态系统也带来了日益增长的需求。

在欧洲,各组织机构正在遵守GDPR并采用基于隐私设计的分析架构。德国和英国在製造业和金融服务业现代化的推动下走在前列,而法国和义大利则在政府支持下加速数位转型。强制性资料本地化迫使供应商运作跨区域丛集,这虽然增加了营运成本,但也提升了注重隐私的客户的信任度。欧盟围绕可信任云端标籤和安全分析沙箱的措施正在进一步影响架构决策。

亚太地区是成长最快的区域,43% 的公司计划在未来一年内将人工智慧预算增加 20% 以上。中国正在扩大国内大规模语言模型的规模,以符合当地法规,从而建构一个与西方平台截然不同的平行生态系统。印度的银行、金融服务和保险 (BFSI) 以及通讯业正在大力投资数据平台,以触及行动优先用户。日本和韩国优先发展全通路零售分析,而澳洲则凭藉强大的云端基础设施和有利的外汇走势保持稳定成长。总体而言,到 2028 年,亚太地区的人工智慧支出可能超过 1,100 亿美元,这将为客户分析市场带来强劲的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对高度个人化客户体验(主流)的需求日益增长

- 云端原生分析降低中小企业(主流)的总拥有成本

- 利用人工智慧驱动的自助式分析实现洞察民主化(主流)

- 客户数据平台与行销技术套件(主流)捆绑在一起。

- 零售媒体网路悄悄开放第一方资料通道

- 在 SaaS 工作流程中嵌入分析(非侵入式)

- 市场限制

- 资料主权法引发全球分歧(主流观点)

- 可配置数据产品人才短缺(主流)

- 影子IT现象猖獗,会在你不知情的情况下创造重复的客户身分。

- 由于移除第三方 Cookie 而导致的广告技术讯号遗失(不明显)

- 价值/供应链分析

- 监管格局

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争的激烈程度

第五章 市场规模与成长预测

- 依部署类型

- 本地部署

- 云端基础

- 透过解决方案

- 社群媒体分析工具

- 网路分析工具

- 仪錶板和报告工具

- 客户之声(VoC)

- ETL(提取、转换、载入)

- 进阶分析模组

- 按公司规模

- 小型企业

- 大公司

- 按最终用户产业

- 通讯/IT

- 旅游与饭店

- 零售

- BFSI

- 媒体与娱乐

- 卫生保健

- 运输/物流

- 製造业

- 其他行业

- 透过服务

- 託管服务

- 专业服务

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adobe

- Alteryx

- Angoss Software Corp.

- Axtria

- Bridgei2i(Accenture)

- IBM

- Manthan Software

- Microsoft

- NGDATA

- Oracle

- Pitney Bowes

- Salesforce

- SAS Institute

- TEOCO

- Aruba Networks(HPE)

第七章 市场机会与未来展望

The customer analytics market size is valued at USD 14.82 billion in 2025 and is forecast to climb to USD 35.37 billion by 2030, advancing at a 19.01% CAGR.

Adoption accelerates as enterprises pivot toward data-driven engagement, replace high-cost mass marketing, and synchronize fragmented digital touchpoints. Cloud deployment remains the primary architecture because firms prefer scalable pay-as-you-go models that avoid capital outlays, while AI-augmented modules gain traction as organizations demand automated insight production. Vertical expansion continues beyond retail into highly regulated sectors such as healthcare, where analytics supports compliance and personalised care delivery. Competitive intensity rises as platform vendors embed analytics inside existing applications to lock in customers and defend share against smaller specialists. At the same time, data-sovereignty regulations and talent shortages temper short-term expansion by forcing businesses to re-engineer architectures and source external expertise.

Global Customer Analytics Market Trends and Insights

Rising Demand for Hyper-Personalised Customer Experience

Escalating acquisition costs force firms to prioritise retention, elevating personalisation from marketing goal to core operating principle. Adobe found 71% of consumers expect brands to anticipate needs, yet fewer than 40% of companies deliver at scale. Streaming providers illustrate impact: Netflix attributes roughly 80% of viewer engagement to its data-driven recommendation engine that adapts to real-time behavioural signals. Hospitality operators mirror this shift, with nearly nine in 10 hotels deploying AI-enhanced guest interactions that command premium room rates. The linkage between insight quality and revenue uplift encourages cross-industry investment in advanced segmentation, propensity modelling and next-best-action engines, fuelling growth across the customer analytics market.

Cloud-Native Analytics Lowers TCO for SMEs

Small and medium enterprises increasingly adopt cloud services because subscription models remove large capital outlays and shorten deployment cycles. US surveys show annual technology spending for many SMEs falls between USD 10,000 and USD 49,000, making scalable pay-per-use analytics financially attractive. Public cloud providers anticipate spending to top USD 1 trillion by 2028, and enterprise architects report that 85% of new workloads will follow cloud-first principles by 2025. For European mid-sized firms, 40% cite financial uncertainty as a barrier to digital projects-a gap that cloud platforms close by converting fixed costs into operating expenses.

Data-Sovereignty Laws Fragment Global Rollouts

Governments tighten control over personal data storage and cross-border transfers, forcing multinationals to build region-specific stacks and duplicate data pipelines. The US Department of Justice rule blocking access to sensitive American data by countries of concern exemplifies this shift and adds compliance overhead starting April 2025. Organisational architects must balance GDPR, the Cloud Act and divergent APAC residency mandates, often choosing to localise processing rather than centralise, which delays unified customer-view projects and slows customer analytics market adoption in complex operating models.

Other drivers and restraints analyzed in the detailed report include:

- AI-Augmented Self-Service Analytics Democratises Insights

- Customer Data Platforms Bundled into Mar-Tech Suites

- Shortage of Composable Data-Product Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions account for 62% of 2024 revenue and are projected to grow at a 21.40% CAGR through 2030 as firms prefer elastic scaling and reduced maintenance overhead. In many cases the customer analytics market size for cloud deployments is expected to exceed USD 25 billion by 2030 at segment level. On-premises environments persist in finance and public-sector contexts that enforce tight latency or residency controls, yet investment concentrates on hybrid approaches that keep sensitive data local while offloading heavy computation to public clouds. Microsoft reported Azure growth of 35% in Q3 2025, attributing almost half the incremental revenue to AI services that power real-time segmentation and propensity modelling. Oracle's multicloud pact with AWS demonstrates how previously rival platforms now interconnect to meet enterprise demand for flexible analytics migration paths.

Enterprises that shift to cloud note faster experimentation cycles: data teams spin up sandbox environments within minutes and de-commission them once models are validated, a process that once required weeks of procurement and installation when hardware was on-premises. Subscription pricing converts large upfront investments into operational expense, easing budget approvals especially for SMEs. As vendors introduce industry-specific compliance blueprints, regulated sectors increasingly migrate analytical workloads, further broadening the customer analytics market.

Dashboard and reporting software still represents 27% of 2024 revenue because visual summaries remain the gateway for non-technical managers. Yet AI-augmented modules are expanding at a 24.60% CAGR to 2030, positioning them as the fastest-growing layer of the customer analytics market. These engines automate feature engineering, model selection and scenario analysis, thereby shortening the path from raw data to actionable insight. Adobe integrated generative AI across its Digital Experience suite and generated USD 5.37 billion in 2024, validating appetite for embedded intelligence.

Voice-of-Customer, social-media and web-analytical applications continue carving out specialised use cases, but they are converging under broader customer-data-platform umbrellas that centralise schema, consent and identity resolution. ETL tools evolve from batch integrations into real-time pipelines that refresh feature stores in seconds, enabling content and pricing engines to react to customer context during live engagements. Suppliers that automate data quality and governance directly within these flows differentiate strongly amid growing privacy scrutiny.

Customer Analytics Market is Segmented by Deployment Type (On-Premises and Cloud-Based), Solution (Social-Media Analytical Tools, Web Analytical Tools and More), Organization Size (SMEs, Large Enterprises), Service (Managed Service, Professional Service), End-User Industry (Telecommunications and IT, Travel and Hospitality and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominates spending owing to deep cloud penetration, mature data-science talent pools and strong venture funding that topped USD 109.1 billion for AI start-ups in 2024. Vendors leverage dense data-centre footprints across the United States and Canada to deliver low-latency inference for real-time personalisation campaigns. Regulatory policy remains comparatively flexible, though state-level privacy acts require region-specific consent controls. Mexico's emerging e-commerce ecosystems create incremental demand as retailers seek insight into omnichannel buyer behaviour.

Europe follows closely as organisations comply with GDPR, driving uptake of privacy-by-design analytics frameworks. Germany and the United Kingdom lead adoption, supported by manufacturing and financial-services modernisation, while France and Italy accelerate digital programmes through government-backed stimulus. Data-localisation mandates compel vendors to operate multi-region clusters, increasing operating costs yet boosting trust among privacy-sensitive customers. EU initiatives around trusted-cloud labels and secure analytics sandboxes further influence architectural decisions.

APAC represents the fastest-expanding region, with 43% of enterprises planning >20% AI budget increases over the coming year. China scales domestic large-language models to serve local regulations, prompting parallel ecosystems distinct from Western platforms. India's BFSI and telecom sectors invest heavily in data platforms to reach mobile-first users. Japan and South Korea emphasise omnichannel retail analytics, and Australia maintains steady growth on the back of strong cloud infrastructure and favourable currency trends. Overall, regional AI expenditure could exceed USD 110 billion by 2028, sustaining robust expansion of the customer analytics market.

- Adobe

- Alteryx

- Angoss Software Corp.

- Axtria

- Bridgei2i (Accenture)

- IBM

- Manthan Software

- Microsoft

- NGDATA

- Oracle

- Pitney Bowes

- Salesforce

- SAS Institute

- TEOCO

- Aruba Networks (HPE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for hyper-personalised CX (mainstream)

- 4.2.2 Cloud-native analytics lowers TCO for SMEs (mainstream)

- 4.2.3 AI-augmented self-service analytics democratises insights (mainstream)

- 4.2.4 Customer Data Platforms bundled into mar-tech suites (mainstream)

- 4.2.5 Retail media networks opening first-party data pipes (under-the-radar)

- 4.2.6 Embedded analytics inside SaaS workflows (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty laws fragment global roll-outs (mainstream)

- 4.3.2 Shortage of composable data-product talent (mainstream)

- 4.3.3 Shadow-IT sprawl creates duplicate customer IDs (under-the-radar)

- 4.3.4 Ad-tech signal loss after third-party cookie deprecation (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud-based

- 5.2 By Solution

- 5.2.1 Social-Media Analytical Tools

- 5.2.2 Web Analytical Tools

- 5.2.3 Dashboard and Reporting Tools

- 5.2.4 Voice of Customer (VoC)

- 5.2.5 ETL (Extract-Transform-Load)

- 5.2.6 Advanced Analytical Modules

- 5.3 By Organisation Size

- 5.3.1 SMEs

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Telecommunications and IT

- 5.4.2 Travel and Hospitality

- 5.4.3 Retail

- 5.4.4 BFSI

- 5.4.5 Media and Entertainment

- 5.4.6 Healthcare

- 5.4.7 Transportation and Logistics

- 5.4.8 Manufacturing

- 5.4.9 Other Industries

- 5.5 By Service

- 5.5.1 Managed Service

- 5.5.2 Professional Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 UAE

- 5.6.5.1.4 Turkey

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Presence, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adobe

- 6.4.2 Alteryx

- 6.4.3 Angoss Software Corp.

- 6.4.4 Axtria

- 6.4.5 Bridgei2i (Accenture)

- 6.4.6 IBM

- 6.4.7 Manthan Software

- 6.4.8 Microsoft

- 6.4.9 NGDATA

- 6.4.10 Oracle

- 6.4.11 Pitney Bowes

- 6.4.12 Salesforce

- 6.4.13 SAS Institute

- 6.4.14 TEOCO

- 6.4.15 Aruba Networks (HPE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis