|

市场调查报告书

商品编码

1850981

Gigabit乙太网路测试设备:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Gigabit Ethernet Test Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

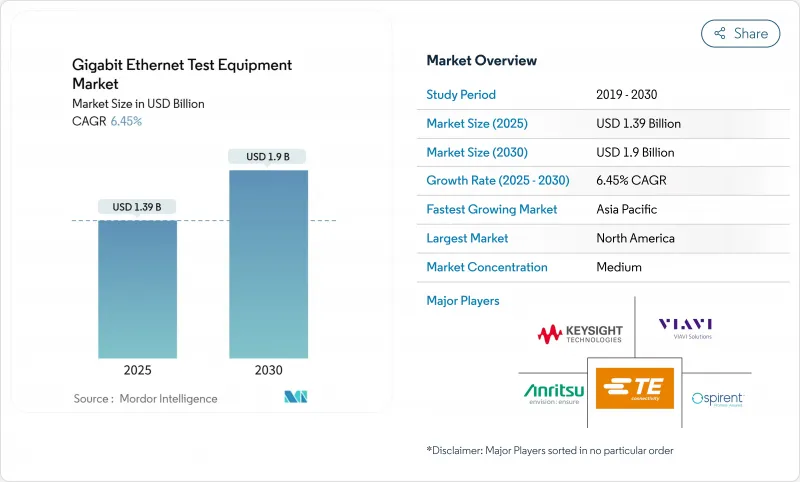

预计到 2025 年,Gigabit乙太网路测试设备市场规模将达到 13.9 亿美元,到 2030 年将达到 19 亿美元,年复合成长率为 6.45%。

随着人工智慧工作负载的日益普及和频宽需求的不断变化,检验团队不得不超越 400G,拥抱新兴的 800G 和 1.6T 标准。资料中心营运商正将预算从传统的误码率测试工具转向高精度解决方案,以评估资料包喷射、前向纠错和 RoCEv2 在真实网路拥塞环境下的延迟。超大规模资料中心营运商现在需要能够结合流量产生、网路模拟和机器学习主导分析的全自动化测试平台,以缩短开发週期。 PAM4 光模组的供应瓶颈和 224Gbps 通道设计专家的短缺导致交货前置作业时间延长,价格居高不下,但能够保证儘早提供 1.6T 功能的供应商将获得高合约。

全球Gigabit乙太网路测试设备市场趋势与洞察

AI集群基础设施推动800G测试需求

主要亮点

- 人工智慧训练正频宽需求超越传统的 400G,迫使营运商采用 800G 和 1.6T 链路,这需要新的检验策略。目前的丛集每个 xPU 需要 1Tbps 的频宽,这给 SerDes 设计带来了压力,因为它们正从 NRZ 调变过渡到 PAM4 调变。供应商现在将自动去嵌入软体与高速示波器捆绑在一起,使工程师能够在几分钟内(而不是几天)表征小于 10 ps 的单元间隔。超乙太网路联盟 (Ultra Ethernet Consortium) 最终确定了超越 IEEE 802.3 的 v1.0 规范,增加了传统乙太网路中没有的壅塞管理测试。率先提供 1.6T 容量的参与企业已与渴望使其 AI 架构面向未来的超大规模资料中心营运商签订了多年框架合约。此类计划能够加速那些将光通讯、流量产生和分析整合到单一编配层的公司的收入成长。

云端服务的扩展加速了多速测试

云端服务供应商正在部署 100G、400G 和 800G 等多种拓扑结构,以平衡效能和成本,应对不断变化的工作负载,这需要能够同时检验多种速度的测试平台。由于前向纠错(尤其是 RS-FEC)在这些速度下至关重要,因此解决方案必须即时监控奇偶校验区块,同时避免掩盖潜在缺陷。目前的模拟引擎会重播数天的流量日誌,以模拟微突发拥塞,同时维持亚微秒的延迟指标。营运商需要可程式 API,以便与 CI/CD 工具链集成,并支援每日对网路升级进行回归测试。因此,市场对能够提供确定性效能基准并降低硬体资本支出的虚拟化测试实验室的需求日益增长。

技术专家短缺阻碍了市场扩张

从NRZ到PAM4的过渡需要精通斜校正、符号误差绘图和224Gbps频道建模的工程师,然而这些技能在全球范围内仍然十分稀缺。儘管许多服务提供者依赖自动化演算法来解读眼图高度和抖动预算,但复杂的故障仍需要人工分析。 「连接前检查」等光纤检测宣传活动表明,技能短缺正在推高安装错误率。培训流程落后于技术蓝图,迫使供应商引入人工智慧主导的嚮导程序,以最少的使用者输入配置设备。然而,PAM4串扰、时延和FEC裕量的高阶故障排除仍需要手动完成,这使得计划进度容易受到人才短缺的影响。

细分市场分析

到2024年,10GbE类别将维持Gigabit乙太网路测试设备市场42%的份额,凸显了其在企业交换骨干网路中的地位。然而,预计到2030年,800GbE和1.6TbE钻机的复合年增长率将达到21.5%,高于其他任何速度等级。是德科技的AresONE平台可传输6.4Tbps的测试流量,是德科技预计,到2030年,超高速Gigabit乙太网路测试设备市场规模将达4.9亿美元。同时,25/40/50GbE和100GbE提供了经济高效的过渡方案,尤其是在传统光元件生态系统能够降低迁移风险的情况下。像Marvell这样的半导体供应商正在加速这一转变,他们提供的3nm PAM4 DSP样品可将模组功耗降低20%,从而扩大高密度底盘的散热空间。

买家正在权衡升级时机与标准的成熟度。 400GbE 拥有成熟的 RS-FEC 规范,因此仍然是寻求快速回报计划的首选。相反,正在评估 1.6T 的工程实验室订购的是混合速度底盘,这种机箱将满足当前需求的 800G 刀片与预留的空笼相结合,以便将来安装 1.6T 可插拔线缆。这种灵活性有助于稳定资本规划,并保护早期采用者免受过时的影响。随着超大规模资料中心业者每六个月进行一次网路升级,提供现场可升级硬体和永久软体授权的供应商可以创造持续的收入来源。这种转变缩短了产品生命週期,并将竞争重点从硬体物料材料清单转向可程式功能的速度。

由于5G回程传输的部署,通讯将在2024年占据36.5%的收入份额,但资料中心和云端服务供应商到2030年将以18%的复合年增长率成长,并在2027年超越通讯的绝对支出。人工智慧工作负载密度将迫使资料中心同时检验无损资料包喷射、亚微秒级抖动和RoCEv2拥塞控制,所有这些都超过了传统通讯业者的指标。汽车和交通运输原始设备製造商(OEM)正在加强乙太网路合规性,以支援驾驶辅助和自动驾驶协议栈,这催生了对能够进行10GBASE-T1特性分析的坚固型示波器和电磁干扰测试室的需求。

同时,製造业正在加速推进危险区域的乙太网路APL试点项目,这需要兼具本质安全测试仪和电源迴路分析仪功能的设备。航空航太与国防整合商需要能够承受振动、极端温度和电磁脉衝的设备,迫使供应商采用军用级机壳。公共产业和医疗保健行业正在推动测试计划,这些计划规定了确定性故障安全通讯协定,并检验了零损耗保护开关和网路安全韧体。这些跨产业的细微差别迫使供应商提供模组化平台,以便根据需求插入特定产业的合规软体包,这种策略既能满足不同的监管框架,又能降低研发成本。

Gigabit乙太网路测试设备市场报告按类型(1GbE、10GbE、其他)、最终用户产业(通讯、资料中心、云端、其他)、应用(研发/实验室、製造/生产、其他)、测试类型(功能/流量产生、效能/压力、合规性/一致性、其他)和地区进行细分。

区域分析

北美地区贡献了33%的收入,这主要得益于半导体研发的集中以及人工智慧丛集的快速部署,这些部署要求在创纪录的时间内完成800G认证。虽然云端服务供应商占据了美国订单的大部分,但加拿大正凭藉宽频復兴和工业乙太网升级推动成长。美国正利用近岸外包趋势扩大汽车线束製造,推动对T1合规套件的需求。部分州的低能源成本正在推动资料中心建设,但800G钻机的高能耗将导致永续性审核,这可能会影响采购週期。

亚太地区以10.25%的复合年增长率引领成长,这主要得益于中国超大规模资料中心的扩张和本地化的1.6T光元件供应链。日本汽车产业青睐需要严格EMC检验的确定性乙太网路协定栈,而韩国则将半导体晶圆厂推进至3nm製程水平,这需要超高速的抖动和串扰侦测设备。东南亚国协正在部署5G回程传输和智慧工厂试点项目,并因此获得了多速率手持分析仪的订单。印度的政策奖励促进了通讯设备製造和软体定义网路实验室的发展。

随着德国汽车製造商 (OEM) 正式製定汽车乙太网路测试计划,以及工业营运商在其流程工厂中采用乙太网路应用效能测试 (Ethernet-APL),欧洲市场呈现稳定成长态势。英国正在对其光纤骨干网路进行现代化改造,推动了对可携式光时域反射仪 (OTDR) 和误码率测试仪 (BERT) 的需求。法国和西班牙正在投资可再生能源电网升级,这需要对变电站进行确定性乙太网路测试。中东地区正将石油收入投入海湾地区待开发区资料中心,而非洲矿业公司则订购了适用于恶劣环境的坚固耐用型 PoE 测试仪。南美洲市场保持相对稳定,这主要得益于巴西通讯业者的升级改造和阿根廷汽车线束出口的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 行动回程成长

- 云端服务和巨量资料应用

- 乙太网路在製造业的应用日益广泛

- 适用于传统线缆的 2.5/5 GbE 升级

- 对用于 800G/1.6T 测试的 AI丛集的需求

- 基于 RoCEv2 的超低延迟检验

- 市场限制

- 缺乏技术专长

- 复杂的测量精度限制

- 800G钻机的能量和热力限制

- PAM-4光学元件供应链瓶颈

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 1GbE

- 10GbE

- 25/40/50GbE

- 100GbE

- 400GbE

- 800GbE 和 1.6TbE

- 按最终用户行业划分

- 通讯

- 资料中心和云

- 製造业

- 汽车与运输

- 航太与国防

- 其他(公共产业、医疗保健)

- 透过使用

- 研发/实验室

- 製造/生产

- 现场服务和安装

- 认证与合规

- 按测试类型

- 功能/流量生成

- 表现/压力

- 合规性/一致性

- 网路模拟

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Keysight Technologies Inc.

- Anritsu Corp.

- VIAVI Solutions Inc.

- Spirent Communications plc

- EXFO Inc.

- Rohde and Schwarz GmbH and Co KG

- Teledyne LeCroy(Xena)

- Yokogawa Test and Measurement

- VeEX Inc.

- GL Communications Inc.

- Trend Networks

- GigaNet Systems

- Xinertel Technology

- Apposite Technologies

- NetScout Systems Inc.

- Te Connectivity Ltd.

- Aquantia(Marvell)

- GAO Tek Inc.

- IDEAL Industries Inc.

- Veryx Technologies

第七章 市场机会与未来展望

The Gigabit Ethernet test equipment market reached USD 1.39 billion in 2025 and is forecast to climb to USD 1.90 billion by 2030, advancing at a 6.45% CAGR.

Rising adoption of artificial intelligence workloads is redefining bandwidth expectations, forcing validation teams to move beyond 400G and embrace emerging 800G and 1.6T standards. Data center operators are reallocating budgets from legacy bit error rate tools to high-precision solutions that evaluate packet spray, forward error correction, and RoCEv2 latency under real-world congestion. Hyperscalers now request fully automated test beds that blend traffic generation, network emulation, and machine-learning-driven analytics to shorten development cycles. Supply bottlenecks for PAM4 optics and a shortage of 224 Gbps channel-design experts keep delivery lead times long and price points high, yet vendors that can guarantee early access to 1.6T capability are commanding premium contracts.

Global Gigabit Ethernet Test Equipment Market Trends and Insights

AI Cluster Infrastructure Drives 800G Testing Demand

Key Highlights

- Artificial intelligence training pushes bandwidth requirements beyond conventional 400G, compelling operators to adopt 800G and 1.6T links that demand fresh validation strategies. Current clusters need 1 Tbps per xPU, stressing SerDes designs that shift from NRZ to PAM4 modulation, which in turn mandates eye-opening precision for signal-to-noise ratio analysis. Vendors now bundle high-speed oscilloscopes with automated de-embedding software so engineers can characterize sub-10-ps unit intervals in minutes rather than days. The Ultra Ethernet Consortium is finalizing v1.0 specifications that extend beyond IEEE 802.3, adding congestion management tests never seen in legacy Ethernet. Early movers that deliver 1.6T capability are winning multi-year framework deals with hyperscalers eager to future-proof AI fabrics. These projects accelerate revenue for companies able to link optics, traffic generation, and analytics into a single orchestration layer.

Cloud Services Expansion Accelerates Multi-Speed Testing

Cloud providers deploy mixed 100G, 400G, and 800G topologies to balance performance and cost across variable workloads, creating a need for test rigs that validate several speeds concurrently. Forward error correction, particularly RS-FEC, is essential at those rates, so solutions must monitor real-time parity blocks without masking latent defects. Emulation engines now replay days of traffic logs to reproduce microburst congestion while maintaining sub-microsecond latency metrics. Operators request programmable APIs that integrate with CI/CD toolchains, enabling daily regression of network upgrades. The result is rising demand for virtualized test labs that cut hardware capex yet still provide deterministic performance baselines.

Technical Expertise Shortage Constrains Market Expansion

Moving from NRZ to PAM4 demands engineers competent in de-skewing, symbol error plotting, and 224 Gbps channel modeling, skills still rare across global labor pools. Many service providers rely on automated algorithms to interpret eye height and jitter budgets, yet complex failures still need human insight. Fiber inspection campaigns such as "Inspect Before You Connect" show how deficit skills inflate installation error rates. Training pipelines lag behind technology roadmaps, compelling vendors to embed AI-driven wizards that configure instruments based on minimal user input. Nevertheless, advanced troubleshooting of PAM4 crosstalk, skew, and FEC margin remains a manual discipline, keeping project timelines vulnerable to talent shortages.

Other drivers and restraints analyzed in the detailed report include:

- Manufacturing Ethernet Adoption Creates Industrial Testing Opportunities

- Legacy Infrastructure Upgrades Drive Multi-Gigabit Testing

- Measurement Accuracy Limitations Impede High-Speed Validation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 10 GbE category retained 42% of the Gigabit Ethernet test equipment market share in 2024, underscoring its entrenched presence in enterprise switching backbones. Yet 800 GbE and 1.6 TbE rigs are set to grow at 21.5% CAGR to 2030, the fastest pace of any speed grade, fueled by AI cluster architectures that need line-rate validation at 224 Gbps per lane. Keysight's AresONE platform streams 6.4 Tbps of test traffic, marking a leap that positions the Gigabit Ethernet test equipment market size for ultra-high-speed gear at USD 490 million by 2030, according to Keysight. Meanwhile 25/40/50 GbE and 100 GbE serve as cost-efficient stepping-stones, especially where legacy optics ecosystems lower migration risk. Semiconductor vendors such as Marvell accelerate the shift by sampling 3 nm PAM4 DSPs that drop module power by 20%, extending cooling envelopes inside dense chassis.

Buyers weigh upgrade timing against standards maturity. 400 GbE enjoys mature RS-FEC profiles, so projects chasing rapid returns still favor it. Conversely, engineering labs evaluating 1.6 T are ordering mixed-speed chassis that combine 800 G blades for immediate needs and empty cages ready for future 1.6 T pluggables. This flexibility stabilizes capital planning while protecting early adopters from obsolescence. As hyperscalers roll out fabric upgrades in six-month sprints, vendors that ship field-upgradeable hardware and perpetual software licenses gain recurring revenue streams. The transition compresses product lifecycles, shifting competitive focus from hardware bill-of-materials to programmable feature velocity.

Telecommunications captured 36.5% of 2024 revenue due to 5G backhaul rollouts, yet data centers and cloud providers are expanding at an 18% CAGR to 2030, overtaking telcos in absolute spending by 2027. AI workload density drives data centers to validate lossless packet spraying, sub-microsecond jitter, and RoCEv2 congestion control concurrently, all of which exceed traditional telco metrics. Automotive and transport OEMs ramp Ethernet compliance to support driver assistance and autonomous stacks, creating demand for rugged oscilloscopes and EMI chambers capable of 10GBASE-T1 characterization.

Meanwhile, manufacturing outfits accelerate Ethernet-APL pilots within hazardous zones, requiring intrinsically safe testers that double as power loop analyzers. A&D integrators need equipment that withstands vibration, temperature extremes, and electromagnetic pulse, compelling suppliers to adapt military-grade enclosures. Utilities and healthcare specify deterministic fail-safe protocols, pushing test plans to verify zero-loss protection switching and cyber-hardened firmware. These cross-sector nuances pressure vendors to offer modular platforms that slot vertical-specific compliance packages on demand, a strategy that tempers R&D overhead while addressing divergent regulatory frameworks.

The Gigabit Ethernet Test Equipment Market Report is Segmented by Type (1 GbE, 10 GbE, and More), End-User Industry (Telecommunications, Data Centers and Cloud, and More), Application (R&D/Lab, Manufacturing/Production, and More), Test Type (Functional / Traffic Generation, Performance / Stress, Compliance / Conformance, and More), and Geography.

Geography Analysis

North America holds 33% revenue thanks to concentrated semiconductor R&D and aggressive AI cluster deployments that mandate 800G qualification in record time. United States cloud providers anchor most orders, but Canada gains traction through broadband revitalization and industrial Ethernet upgrades. Mexico leverages nearshoring trends to expand automotive harness manufacturing, raising demand for T1 compliance kits. Low energy costs in some states attract additional data center builds, yet the high power draw of 800G rigs prompts sustainability audits that may influence procurement cycles.

Asia Pacific leads growth at 10.25% CAGR on the back of China's hyperscale expansion and localized 1.6 T optics supply chains. Japan's auto sector champions deterministic Ethernet stacks that require stringent EMC validation, while Korea pushes semiconductor fabs into 3 nm class, needing ultra-fast jitter and crosstalk probes. ASEAN states deploy 5G backhaul and smart factory pilots, generating orders for multi-rate handheld analyzers. India's policy incentives spur telco equipment manufacturing and software defined network labs, though patchy infrastructure and a talent shortfall temper near-term adoption.

Europe charts steady gains with German OEMs formalizing in-vehicle Ethernet test plans and industrial operators embracing Ethernet-APL inside process plants. The United Kingdom modernizes fiber backbone networks, fueling demand for portable OTDRs and BERTs. France and Spain invest in renewable energy grid upgrades that require deterministic sub-station Ethernet testing. The Middle East channels oil revenues into greenfield data centers in the Gulf, while African miners commission ruggedized PoE testers for harsh environments. South America remains modest but stable, driven by Brazilian telco upgrades and Argentine automotive wire harness exports.

- Keysight Technologies Inc.

- Anritsu Corp.

- VIAVI Solutions Inc.

- Spirent Communications plc

- EXFO Inc.

- Rohde and Schwarz GmbH and Co KG

- Teledyne LeCroy (Xena)

- Yokogawa Test and Measurement

- VeEX Inc.

- GL Communications Inc.

- Trend Networks

- GigaNet Systems

- Xinertel Technology

- Apposite Technologies

- NetScout Systems Inc.

- Te Connectivity Ltd.

- Aquantia (Marvell)

- GAO Tek Inc.

- IDEAL Industries Inc.

- Veryx Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in mobile backhaul

- 4.2.2 Adoption of cloud services and big data

- 4.2.3 Increased Ethernet use in manufacturing

- 4.2.4 2.5 / 5 GbE upgrades on legacy cabling

- 4.2.5 AI cluster demand for 800G/1.6T testing

- 4.2.6 RoCEv2-driven ultra-low-latency validation

- 4.3 Market Restraints

- 4.3.1 Lack of technical expertise

- 4.3.2 Complex measurement accuracy limits

- 4.3.3 Energy and thermal constraints in 800G rigs

- 4.3.4 Supply-chain bottlenecks for PAM-4 optics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 1 GbE

- 5.1.2 10 GbE

- 5.1.3 25/40/50 GbE

- 5.1.4 100 GbE

- 5.1.5 400 GbE

- 5.1.6 800 GbE and 1.6 TbE

- 5.2 By End-user Industry

- 5.2.1 Telecommunications

- 5.2.2 Data Centers and Cloud

- 5.2.3 Manufacturing

- 5.2.4 Automotive and Transport

- 5.2.5 Aerospace and Defense

- 5.2.6 Others (Utilities, Healthcare)

- 5.3 By Application

- 5.3.1 RandD/Lab

- 5.3.2 Manufacturing/Production

- 5.3.3 Field Service and Installation

- 5.3.4 Certification and Compliance

- 5.4 By Test Type

- 5.4.1 Functional / Traffic Generation

- 5.4.2 Performance / Stress

- 5.4.3 Compliance / Conformance

- 5.4.4 Network Emulation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Keysight Technologies Inc.

- 6.4.2 Anritsu Corp.

- 6.4.3 VIAVI Solutions Inc.

- 6.4.4 Spirent Communications plc

- 6.4.5 EXFO Inc.

- 6.4.6 Rohde and Schwarz GmbH and Co KG

- 6.4.7 Teledyne LeCroy (Xena)

- 6.4.8 Yokogawa Test and Measurement

- 6.4.9 VeEX Inc.

- 6.4.10 GL Communications Inc.

- 6.4.11 Trend Networks

- 6.4.12 GigaNet Systems

- 6.4.13 Xinertel Technology

- 6.4.14 Apposite Technologies

- 6.4.15 NetScout Systems Inc.

- 6.4.16 Te Connectivity Ltd.

- 6.4.17 Aquantia (Marvell)

- 6.4.18 GAO Tek Inc.

- 6.4.19 IDEAL Industries Inc.

- 6.4.20 Veryx Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

乙太网路测试设备市场:2026-2032年全球市场预测(按产品类型、技术、测试频率、应用和最终用户划分)

乙太网路测试设备市场:2026-2032年全球市场预测(按产品类型、技术、测试频率、应用和最终用户划分) Gigabit乙太网路测试设备市场规模、份额及成长分析(依产品类型、应用、介面类型、最终用户及地区划分)-2026-2033年产业预测

Gigabit乙太网路测试设备市场规模、份额及成长分析(依产品类型、应用、介面类型、最终用户及地区划分)-2026-2033年产业预测 乙太网路测试设备市场规模、份额和趋势分析报告:按类型、功能、最终用途、地区和细分市场预测,2025 年至 2033 年

乙太网路测试设备市场规模、份额和趋势分析报告:按类型、功能、最终用途、地区和细分市场预测,2025 年至 2033 年 全球十亿位元乙太网路网路测试设备市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

全球十亿位元乙太网路网路测试设备市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年) 2025-2029 年乙太网路测试设备市场

2025-2029 年乙太网路测试设备市场 十亿位元乙太网路网路测试设备市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

十亿位元乙太网路网路测试设备市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 全球乙太网路测试设备市场

全球乙太网路测试设备市场 全球乙太网路测试设备市场规模研究(按设备类型、应用、最终用途产业和 2022-2032 年区域预测)

全球乙太网路测试设备市场规模研究(按设备类型、应用、最终用途产业和 2022-2032 年区域预测)