|

市场调查报告书

商品编码

1851066

受众分析:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Audience Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

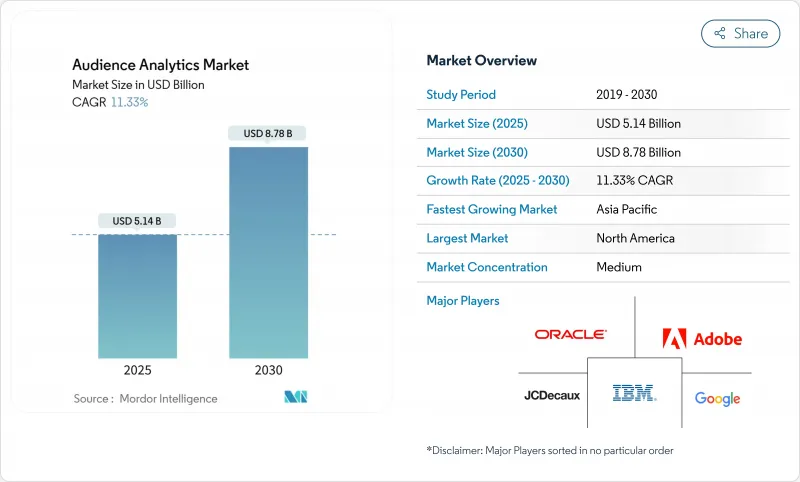

预计到 2025 年,受众分析市场规模将达到 51.4 亿美元,到 2030 年将达到 87.8 亿美元,年复合成长率为 11.3%。

对基于用户许可的身份解析、强大的AI套件以及零售媒体网路中第一方数据快速变现的需求日益增长,正在推动这一领域的扩张。企业正越来越多地采用基于边缘的即时分析技术,在用户互动点产生可执行的洞察,同时保护用户隐私。儘管解决方案仍然是最大的收入来源,但随着企业寻求扩充性和成本优化,云端原生服务正以最快的速度成长。同时,儘管大型企业占据了支出主导地位,但降低高阶分析进入门槛的无程式码介面和基于使用量的定价模式正在加速中小企业采用这些技术。

全球受众分析市场趋势与洞察

全通路第一方资料收集正在蓬勃发展

品牌正围绕自有互动点重建资料架构,整合来自店内行为、行动装置互动和连网装置的讯号。零售商如今经营着复杂的媒体网络,将线上线下体验无缝衔接,从而开闢了曾经由第三方数据仲介主导的、以美元为单位的收入管道。整合线上线下洞察的能力提升了客户终身价值建模水平,并提高了客户细分的精确度。

利用人工智慧/机器学习进行预测分析的快速普及

如今,机器学习演算法已在主流平台上为行为建模、转换预测和自动用户群组创建提供支援。 Google Analytics 4 和 Adobe Experience Cloud 展示的 AI 引擎可将预测准确率提高 30% 以上,同时将洞察延迟从数週缩短至数分钟。云端传输使这些功能得以惠及先前受制于基础设施成本和人才短缺的中型企业。

日益注重隐私的监管

GDPR、CPRA 和《数位市场法案》迫使企业重组资料流,通常需要将 15% 到 20% 的分析预算用于合规工作。诸如无 cookie 网路分析之类的隐私权保护解决方案,既能减少对个人识别资讯的依赖,又能维持行为洞察的品质。供应商正在大力推广情境定向和边缘处理技术,以平衡法规要求和商业性目标。

细分市场分析

解决方案仍将是受众分析市场的支柱,预计到 2024 年将占总收入的 67.8%。这些解决方案包括资料整合中心、客户资料平台和人工智慧推理引擎,能够实现跨通路洞察。企业需要对可扩展的基础设施进行大量前期投资,承担高昂的转换成本,并建立强大的供应商关係。然而,身分解析、模型管治和合规性审核方面的外包专业知识将推动服务以 12.7% 的复合年增长率成长。託管服务能够实现持续优化并弥补资料工程人才缺口,从而提高整体计划成功率。

分析即服务 (AaaS) 的兴起标誌着策略模式正从永久授权转向基于使用量的合约。顾问公司和系统整合商正在将咨询支援服务整合到其技术堆迭中,使业务目标能够驱动实施方案的选择。日益严格的隐私保护条例正在推高诸如同意管理和边缘配置等专业服务的定价,加速收入结构向经常性专业支援的转变。

到2024年,本地部署系统将占据受众分析市场65.8%的份额,这反映出人们对高容量串流分析中资料主权和延迟问题的持续担忧。银行和政府机构等行业依赖自託管平台来保护敏感的个人识别资讯。然而,随着供应商推出区域性加密、主权云端选项和高级合规认证,云端实例将以13.1%的复合年增长率成长。 Adobe和AWS共同推出的云端解决方案是专为即时客户画像量身订製的解决方案。

混合架构正逐渐成为主流模式,它将关键客户画像保留在本地,同时将运算密集型工作负载迁移到云端。这不仅降低了基础设施资本支出,也为季节性宣传活动和突发资料撷取提供了弹性处理能力。随着人们对公共云端安全性的信心日益增强,预计从2030年起,基于云端的受众分析市场规模将超过本地部署市场的收入。

受众分析市场报告按组件(解决方案和服务)、部署类型(本地部署和云端部署)、组织规模(大型企业和中小企业)、应用程式(销售和行销优化、客户体验管理等)、最终用户垂直行业(媒体和娱乐、零售和电子商务等)以及地区进行细分。

区域分析

北美地区预计到2024年将占全球收入的40.3%,这得益于其成熟的广告生态系统、巨额技术投资以及对隐私优先工具的早期应用。在美国,沃尔玛和塔吉特等零售商在零售媒体产生收入处于领先地位,而加拿大则受益于进步的隐私法,这些法律引导企业采用合规的分析架构。墨西哥的电子商务普及率正在加速成长,可扩展的云端洞察引擎的用户群也不断扩大。

在GDPR和数位市场法规的推动下,欧洲正处于稳步成长阶段,这带动了对基于用户许可、最大限度减少个人资料依赖的解决方案的需求。德国和英国正在支援边缘处理试点项目,以确保资料本地化并降低跨境传输的复杂性。法国和义大利正在探索情境导向技术,以维持广告效率。能够与多种身分框架互通的独立供应商正在吸引寻求灵活合规性的中端市场用户。

亚太地区是成长最快的区域,年复合成长率高达12.2%,这得益于其8,800亿美元的行动经济规模和18亿行动用户。中国在社群商务分析领域处于领先地位,将影片、通讯和支付融合在一起,打造精细的即时洞察流。印度的金融科技蓬勃发展,交易资料集不断扩大;日本和韩国则将受众分析融入游戏生态系统,以优化用户留存率。澳洲和纽西兰正在采用企业分析来支援全通路零售和公共服务的现代化。在东南亚,智慧型手机普及率的不断提高和政府数位化政策的推进,进一步推动了市场需求,巩固了受众分析市场的长期发展势头。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全通路第一方资料收集的快速成长

- 快速采用人工智慧/机器学习驱动的预测分析

- 媒体和娱乐产业转向即时受众货币化

- 无 Cookie 行销推动了对基于使用者授权的身份图谱的需求

- 零售媒体网路拓展第一方消费者洞察

- 利用设备端边缘分析实现隐私保护洞察

- 市场限制

- 加强隐私优先法规(GDPR、CPRA、DMA)

- 中小企业用户缺乏数据工程技能

- Petabyte级分析工作负载的云端运算成本不断上涨

- 碎片化的身份解决方案阻碍了互通性

- 价值链分析

- 技术展望

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 透过部署模式

- 本地部署

- 云

- 按公司规模

- 大公司

- 中小企业

- 透过使用

- 销售和行销优化

- 客户体验管理

- 竞争/媒体讯息

- 产品和内容开发

- 诈欺和风险分析

- 按最终用户行业划分

- 媒体与娱乐

- 零售与电子商务

- BFSI

- 电讯和资讯技术

- 医疗保健与生命科学

- 政府和公共部门

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adobe Inc.

- Oracle Corporation

- Google LLC

- International Business Machines Corp.

- comScore, Inc.

- SAS Institute Inc.

- Microsoft Corp.

- Amazon Web Services, Inc.

- Salesforce, Inc.

- Nielsen Holdings Plc

- JCDecaux Group

- Akamai Technologies, Inc.

- Cxense ASA

- Meltwater

- Audiense Ltd.

- Upwave

- Mixpanel, Inc.

- Amplitude, Inc.

- Chartbeat, Inc.

- Piwik PRO

第七章 市场机会与未来展望

The audience analytics market stands at USD 5.14 billion in 2025 and is expected to reach USD 8.78 billion by 2030, advancing at an 11.3% CAGR.

Heightened demand for consent-based identity resolution, powerful AI toolkits, and the rapid monetisation of first-party data in retail media networks underpin this expansion. Organisations increasingly deploy real-time, edge-based analytics that protect privacy while generating actionable insights at the point of engagement. Solutions remain the largest revenue contributor, yet cloud-native services record the quickest growth as firms seek scalability and cost optimisation. Meanwhile, large enterprises dominate spending, but small and medium enterprises accelerate adoption thanks to no-code interfaces and consumption-based pricing models that lower entry barriers to sophisticated analytics.

Global Audience Analytics Market Trends and Insights

Rapid Growth in Omnichannel First-Party Data Collection

Brands are rebuilding data architectures around owned interaction points, integrating in-store behaviour, mobile engagement, and connected-device signals. Retailers now operate sophisticated media networks that align physical and digital journeys, opening USD-level revenue channels once dominated by third-party data brokers. The ability to merge offline and online insights improves lifetime value modelling and elevates segmentation precision.

Surging Adoption of AI/ML-Powered Predictive Analytics

Machine-learning algorithms now underpin behavioural modelling, conversion prediction, and automated cohort creation across mainstream platforms. Google Analytics 4 and Adobe Experience Cloud showcase AI engines that slash insight latency from weeks to minutes while improving forecast accuracy by more than 30%. Cloud delivery makes these functions accessible to mid-market firms previously constrained by infrastructure costs and talent shortages.

Increasing Privacy-First Regulation

GDPR, CPRA, and the Digital Markets Act compel firms to re-engineer data flows, often diverting 15-20% of analytics budgets to compliance efforts. Privacy-preserving solutions, such as cookieless web analytics, reduce dependence on personal identifiers while sustaining behavioural insight quality. Vendors tout contextual targeting and edge processing to balance regulatory demands with commercial goals.

Other drivers and restraints analyzed in the detailed report include:

- Media and Entertainment Shift to Real-Time Audience Monetisation

- Cookieless Marketing Pushes Demand for Consent-Based Identity Graphs

- Data-Engineering Skill Shortages Among SME Users

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 67.8% of 2024 revenue and remain the backbone of the audience analytics market. They comprise data-integration hubs, customer data platforms, and AI inference engines that enable cross-channel insight generation. Organisations invest heavily at the outset in scalable infrastructures, creating high switching costs and entrenched vendor relationships. Services, however, achieve a 12.7% CAGR as firms outsource expertise in identity resolution, model governance, and compliance auditing. Managed offerings deliver continuous optimisation and bridge the data-engineering talent gap, elevating overall project success rates.

The rise of analytics-as-a-service signals a strategic shift from perpetual licences to consumption-based engagements. Consultancies and system integrators package technology stacks with advisory support, ensuring business objectives drive implementation choices. As privacy regulation tightens, specialised services in consent management and edge deployment command premium pricing, accelerating the revenue mix transition toward recurring professional support.

On-premises systems held 65.8% of the audience analytics market share in 2024, reflecting enduring concerns over data sovereignty and latency for high-volume streaming analyses. Sectors such as banking and government rely on self-hosted platforms to retain sensitive personally identifiable information. Nevertheless, cloud instances grow at a 13.1% CAGR as vendors implement region-specific encryption, sovereign-cloud options, and advanced compliance certifications. Adobe's joint offering with AWS exemplifies tailored cloud solutions for real-time customer profiling.

Hybrid architectures surface as the prevailing model, retaining golden customer profiles on-premises while bursting compute-intensive workloads to the cloud. This arrangement curbs infrastructure capital expenditure and unlocks elastic processing for seasonal campaigns and sudden surges in data ingestion. The audience analytics market size represented by cloud deployments is forecast to overtake on-premises revenue in the post-2030 horizon as confidence in public-cloud security matures.

The Audience Analytics Market Report is Segmented by Component (Solutions and Services), Deployment Mode (On-Premises and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), Application (Sales and Marketing Optimisation, Customer Experience Management, and More), End-User Industry (Media and Entertainment, Retail and ECommerce, and More), and Geography.

Geography Analysis

North America held 40.3% revenue in 2024, anchored by a sophisticated advertising ecosystem, heavy technology investment, and early adoption of privacy-first tools. United States retailers such as Walmart and Target lead in retail media revenue generation, while Canada benefits from progressive privacy laws that nudge firms toward compliant analytics architectures. Mexico's accelerating e-commerce adoption widens the regional user base for scalable, cloud-delivered insight engines.

Europe sits in a steady growth phase shaped by GDPR and the Digital Markets Act, which elevate demand for consent-based solutions that minimise personal data dependence. Germany and the United Kingdom endorse edge-processing pilots that keep data resident, reducing cross-border transfer complexity. France and Italy explore contextual targeting to maintain advertising efficiency. Independent vendors that can interoperate across multiple identity frameworks attract mid-market adopters seeking flexible compliance.

Asia-Pacific is the fastest-growing region at a 12.2% CAGR, supported by a USD 880 billion mobile economy and 1.8 billion mobile subscribers. China pioneers social commerce analytics that blend video, messaging, and payments, creating granular, real-time insight streams. India's fintech boom expands transactional datasets, while Japan and South Korea integrate audience analytics into gaming ecosystems to optimise retention. Australia and New Zealand embrace enterprise analytics to support omnichannel retail and public-service modernisation. Rising smartphone penetration and government digital initiatives propel additional demand across Southeast Asia, reinforcing long-term momentum for the audience analytics market.

- Adobe Inc.

- Oracle Corporation

- Google LLC

- International Business Machines Corp.

- comScore, Inc.

- SAS Institute Inc.

- Microsoft Corp.

- Amazon Web Services, Inc.

- Salesforce, Inc.

- Nielsen Holdings Plc

- JCDecaux Group

- Akamai Technologies, Inc.

- Cxense ASA

- Meltwater

- Audiense Ltd.

- Upwave

- Mixpanel, Inc.

- Amplitude, Inc.

- Chartbeat, Inc.

- Piwik PRO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth in omnichannel first-party data collection

- 4.2.2 Surging adoption of AI/ML-powered predictive analytics

- 4.2.3 Media and entertainment shift to real-time audience monetisation

- 4.2.4 Cookieless marketing pushes demand for consent-based identity graphs

- 4.2.5 Retail media networks scaling first-party shopper insights

- 4.2.6 Edge analytics on devices enabling privacy-preserving insights

- 4.3 Market Restraints

- 4.3.1 Increasing privacy-first regulation (GDPR, CPRA, DMA)

- 4.3.2 Data-engineering skill shortages among SME users

- 4.3.3 Rising cloud-compute costs for petabyte-scale analytics workloads

- 4.3.4 Fragmentation of identity solutions hinders interoperability

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Application

- 5.4.1 Sales and Marketing Optimisation

- 5.4.2 Customer Experience Management

- 5.4.3 Competitive/Media Intelligence

- 5.4.4 Product and Content Development

- 5.4.5 Fraud and Risk Analytics

- 5.5 By End-user Industry

- 5.5.1 Media and Entertainment

- 5.5.2 Retail and eCommerce

- 5.5.3 BFSI

- 5.5.4 Telecom and IT

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Government and Public Sector

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 Google LLC

- 6.4.4 International Business Machines Corp.

- 6.4.5 comScore, Inc.

- 6.4.6 SAS Institute Inc.

- 6.4.7 Microsoft Corp.

- 6.4.8 Amazon Web Services, Inc.

- 6.4.9 Salesforce, Inc.

- 6.4.10 Nielsen Holdings Plc

- 6.4.11 JCDecaux Group

- 6.4.12 Akamai Technologies, Inc.

- 6.4.13 Cxense ASA

- 6.4.14 Meltwater

- 6.4.15 Audiense Ltd.

- 6.4.16 Upwave

- 6.4.17 Mixpanel, Inc.

- 6.4.18 Amplitude, Inc.

- 6.4.19 Chartbeat, Inc.

- 6.4.20 Piwik PRO

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment