|

市场调查报告书

商品编码

1851107

5G连结:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030年)5G Connection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

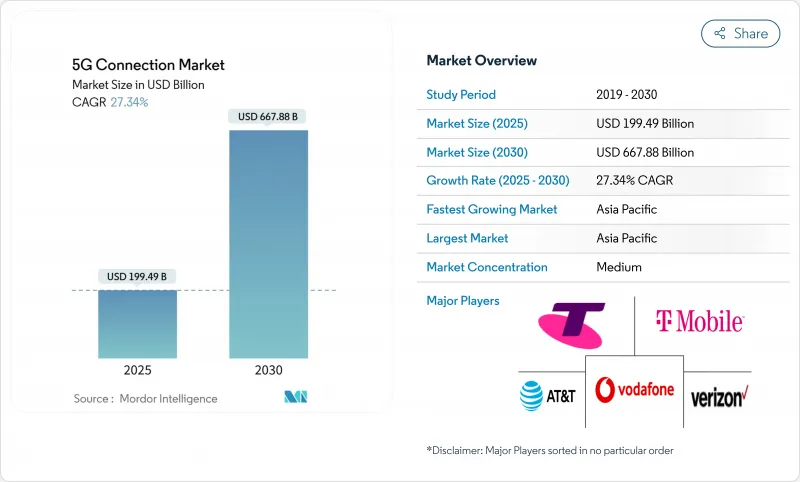

5G 连接市场目前创造的收入为 1,994.9 亿美元,预计到 2030 年将达到 6,678.8 亿美元,年复合成长率为 27.34%。

商业部署正从覆盖范围扩大转向网路密集化,从而推动了切片、边缘运算和RedCap设备等先进功能的快速普及。亚太地区占全球52%的5G用户,这主要得益于中国440万基地台和印度全国范围内的独立组网建设;而北美则在固定无线接入(FWA)的普及方面处于领先地位。通讯业者正在加速从非独立组网(NSA)核心网向独立组网(SA)核心网的迁移,因为后者能够释放更高的获利潜力,尤其是在企业级应用和超可靠低延迟(URLLC)场景中。製造业、医疗保健和汽车行业的专用5G网路正在快速扩展,网路API市场预计将在不久的将来带来更多收入来源。然而,不断上涨的中频段频谱价格、农村地区的覆盖成本以及光纤价格战仍然限制某些地区的成长。

全球5G连结市场趋势与洞察

行动资料流程量的快速成长需要高容量网络

每个5G连线的月均数据使用量将接近70GB,是4G的四倍。中国440万个5G基地台的规模足以支撑如此庞大的流量,而中频段频谱仍然至关重要,目前中国以外地区仅部署了四分之一的中频段频谱。随着流量模式的转变,通讯业者正优先推动载波聚合、大规模MIMO升级和动态频谱共享等技术。这些投资将推动5G连结市场的营收成长,同时也促使营运商更加重视优化网路能源效率。

固定无线存取(FWA)正逐渐成为主流宽频替代方案。

美国营运商总合提供1,150万条固定无线存取(FWA)线路,并预测到2028年这一数字将达到2,000万,届时平均下载速度将超过200Mbps。印度营运商利用光纤部署成本优势,目标在2027年实现3000万FWA用户。 Verizon在2024年第一季累计4.52亿美元的FWA收入,显示其近期盈利前景良好。整体而言,这些市场发展将提高每位用户平均收入,并扩大5G连结市场的潜在用户群。

高昂的资本支出和中频段频谱成本

预计2022年至2025年间,全球基础建设投资将超过6,000亿美元,但欧洲竞标的资金筹措负担分配不均,拥有独立核心网的区域通讯业者仅能获得2%的资金,而中国业者则可获得80%。新兴市场通讯业者正在推迟竞标,并探索铁塔共享模式以缓解槓桿率上升的问题。北欧经济体的网路共享模式树立了一个正面的榜样,但资金压力仍然限制它们全面进入5G连结市场。

细分市场分析

到2024年,行动宽频将占据5G连接市场62%的份额,这主要得益于智慧型手机的普及和影片消费的成长。同时,在智慧工厂、医院和物流中心等场所部署专用5G网路的推动下,机器对机器(M2M)和物联网(IoT)链路正以28.63%的复合年增长率快速增长。尤其值得一提的是,关键任务通讯和固定无线存取(FWA)用户正在推动流量成长,显着扩大了网路切片的5G连接市场规模,而企业级应用的需求也起到了关键作用。硬体厂商推出的RedCap晶片组能够降低工业感测器的耗电量,加速M2M计划的可行性。随着即时分析成为製造业竞争的关键挑战,边缘原生架构将进一步促进M2M的商业化。

预计到2028年,蜂巢式物联网终端的持续成长将使设备数量翻一番,从而不断催生对成本优化模组和简化部署工具的需求。从美国FirstNet的扩展到韩国全国公共网络,关键任务通讯应用场景正在拓展服务差异化的机会。因此,一种新的平衡已经形成:儘管消费者流量仍然占据主导地位,但企业流量将在未来5G连接市场成长中占据主导地位。

随着串流媒体和游戏推动行动宽频流量成长,到2024年,消费者使用5G连线市场规模将维持76%的份额。然而,受汽车、医疗保健和能源等产业数位转型需求的驱动,企业连接市场到2030年将达到30.47%的复合年增长率。製造业尤为突出。超过1000个活跃计划报告称,在切换到专用5G网路后,连接效率提高了15-20%。新加坡和瑞典的医院在整合超低延迟视讯链路后,手术时间缩短,病患治疗效果也得到改善。

此外,智慧城市计画正在部署监视录影机、连网路灯和环境监测器,这些都推动了企业用户数量的成长。公共产业正在利用5G进行即时电网平衡,而石油和天然气营运商则优先考虑自主巡检无人机。这些因素正在使长期收入向企业倾斜,提高每个连接的平均收入,并加深5G连接市场的黏性。

5G 连线市场报告依连线类型(行动宽频、固定无线存取、其他)、最终用户(消费者、企业)、频谱频段(1 GHz 以下、1-6 GHz、其他)、网路架构(非独立组网、独立组网)、装置类别(智慧型手机、平板电脑、FWA CPE、其他) 、服务类型(增强型云端)、装置类别(智慧型手机、行动宽频电脑、FWA CPE.

区域分析

亚太地区将在2024年占据全球52%的5G用户份额,预计到2030年将以30.28%的复合年增长率增长,这主要得益于中国440万基地台的建设以及印度独立组网(SA)的快速扩张。预计到2030年,中国对数位经济的贡献将达到2兆美元,反映了5G平台在製造业、零售业和服务业的广泛应用。印度的Reliance Jio营运超过100万个云端原生行动通信基地台,预计到2027年,固定无线存取(FWA)线路数量将从500万个增加到3,000万条。日本和韩国透过率先推出先进的5G商用服务,维持了区域创新领先地位,预计到2030年,东南亚地区的GDP将因此受益1,300亿美元。

北美是一个日趋成熟且创新驱动的市场,98% 的人口已在使用 5G 网路。 T-Mobile 在全国范围内部署独立组网 (SA) 网络,并拥有 643 万条固定无线接入 (FWA) 线路,这体现了 5G 在消费者和企业用户中的多元化应用。 Verizon 正与 AST SpaceMobile 合作,利用卫星通讯来弥合农村地区的网路覆盖缺口;加拿大和墨西哥的通讯业者也在整合 RedCap 等 5G 先进功能。目前,5G 连接市场的重点在于如何将网路 API、边缘运算和人工智慧辅助服务编配商业化,从而提高每个站点的效益密度。

欧洲的进展喜忧参半:德国、丹麦和芬兰的5G人口覆盖率超过95%,但仅有2%的合约在运作频谱核心网投入使用。英国沃达丰和Three的合併已投入148.6亿美元用于网路升级,旨在提升农村地区的网路覆盖率;而北欧的频谱共用模式则以低成本实现了高可用性。目前,欧洲各地的通讯业者正呼吁监管机构简化竞标并降低牌照费用,以维持投资週期,弥合独立频谱覆盖缺口,并在5G连接市场释放更大的价值。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 行动资料流程量的快速成长需要高容量网络

- 固定无线存取(FWA)正逐渐成为主流宽频替代方案。

- 企业数位化和物联网将加速5G的普及应用。

- 生成式人工智慧主导的上行链路流量激增推动了5G-SA的早期部署

- 透过开放的API生态系统实现获利

- 市场限制

- 高昂的资本支出和中频段频谱成本

- 农村地区的健保覆盖经济效益仍不理想。

- 光纤价格战阻碍了固定无线接入在都市区的普及

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按连线类型

- 行动宽频

- 固定无线存取

- 机器对机器通讯和物联网

- 关键任务通讯

- 私人网路

- 最终用户

- 消费者

- 公司

- 製造业

- 卫生保健

- 汽车和运输设备

- 智慧城市与公共

- 能源与公共产业

- 零售和物流

- 按频宽

- 1 GHz 以下(低频段)

- 1-6 GHz(中频段)

- 24GHz 或更高(毫米波/高频段)

- 透过网路架构

- 非独立式(NSA)

- 独立版 (SA)

- 按设备类别

- 智慧型手机和平板电脑

- FWA CPE

- 物联网模组和网关

- 穿戴式装置和增强/虚拟实境设备

- 工业路由器和加固模组

- 按服务类型

- 增强型行动宽频(eMBB)

- 大规模机器通讯(mMTC)

- 超可靠、低延迟通讯(URLLC)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 其他南美洲

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AT&T Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- China Mobile Ltd.

- China Telecommunications Corp.

- T-Mobile US Inc.

- Telstra Corp. Ltd.

- Telefonica SA

- Deutsche Telekom AG

- Reliance Jio Infocomm Ltd.

- SK Telecom Co. Ltd.

- NTT Docomo Inc.

- KT Corp.

- Orange SA

- KDDI Corp.

- Bharti Airtel Ltd.

- Saudi Telecom Company(stc)

- Rakuten Mobile Inc.

- Etisalat by eand

- MTN Group Ltd.

第七章 市场机会与未来展望

The 5G connections market currently generates USD 199.49 billion in revenue and is forecast to reach USD 667.88 billion by 2030, advancing at a 27.34% CAGR.

Commercial roll-outs have progressed from coverage expansion to network densification, enabling rapid adoption of advanced capabilities such as slicing, edge computing, and RedCap devices. Asia-Pacific accounts for 52% of global subscriptions thanks to China's 4.4 million base stations and India's nationwide standalone build-out, while North America leads in Fixed Wireless Access (FWA) penetration. Operators are accelerating the shift from non-standalone (NSA) to standalone (SA) cores as SA unlocks higher monetization potential, particularly for enterprise and ultra-reliable low-latency (URLLC) use cases. Private 5G networks in manufacturing, healthcare, and automotive are scaling quickly, and network-API marketplaces promise additional revenue streams in the near term. However, high mid-band spectrum prices, rural coverage economics, and fiber price wars continue to temper growth in selected regions.

Global 5G Connection Market Trends and Insights

Surge in mobile data traffic requiring higher-capacity networks

Monthly data usage per 5G line averages close to 70 GB-four times the 4G figure-fueled by cloud gaming and extended-reality services. China's 4.4 million 5G base stations illustrate the scale needed to carry this load, and mid-band spectrum remains vital, although only one quarter of non-Chinese sites currently deploy it. As traffic migrates, operators prioritize additional carrier aggregation, Massive MIMO upgrades, and dynamic spectrum sharing. These investments underpin revenue growth in the 5G connections market while raising the urgency to optimize network energy efficiency.

Fixed Wireless Access (FWA) emerging as mainstream broadband alternative

US operators collectively serve 11.5 million FWA lines, with projections of 20 million by 2028 as median download speeds exceed 200 Mbps. Operators in India aim for 30 million FWA subscribers by 2027 by exploiting cost advantages over limited fiber roll-outs. Verizon generated USD 452 million in Q1 2024 FWA revenue, demonstrating the format's near-term profitability. mmWave deployments increase urban capacity, and customer surveys show 44% preference for wireless home broadband. Collectively, these developments boost average revenue per user and broaden the 5G connections market addressable base.

High CAPEX and mid-band spectrum costs

Global infrastructure outlays will exceed USD 600 billion during 2022-2025, and European auctions drive disproportionate financing burdens that leave only 2% of regional operators with SA cores versus 80% in China. Emerging-market carriers postpone auctions and explore tower-sharing to mitigate rising leverage. Network sharing in Nordic economies shows positive examples, but capital pressures still curb full participation in the 5G connections market.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise digitization and IoT accelerating 5G adoption

- Generative-AI-driven uplink surge spurring early 5G-SA roll-outs

- Rural coverage economics remain unattractive

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile broadband accounted for 62% of the 5G connections market in 2024, underpinned by smartphone adoption and video consumption growth. At the same time, M2M and IoT links are expanding at a 28.63% CAGR, encouraged by private 5G network deployments across smart factories, hospitals, and logistics hubs. The enterprise tilt is materially increasing the 5G connections market size for network slicing, particularly as mission-critical communications and FWA subscriptions contribute incremental traffic. Hardware vendors have introduced RedCap chipsets that lower power draw for industrial sensors, accelerating M2M project viability. Edge-native architectures further catalyze M2M monetization as real-time analytics become table stakes in competitive manufacturing.

Continued proliferation of cellular IoT endpoints is projected to double device counts by 2028, creating relentless demand for cost-optimized modules and simplified onboarding tools. Mission-critical communication use cases, from FirstNet expansion in the US to nationwide public-safety networks in Korea, widen service differentiation opportunities. The resulting diversity cements a new equilibrium in which consumer traffic remains large, yet enterprise traffic captures the outsized share of future 5G connections market growth.

Consumer use retained 76% share of the 5G connections market size in 2024 as streaming and gaming sustained mobile broadband traffic. Nonetheless, enterprise lines will deliver a 30.47% CAGR through 2030, powered by digital-transformation mandates in automotive, healthcare, and energy. Manufacturing stands out: more than 1,000 active projects report 15-20% gains in line efficiency after switching to private 5G. Hospitals in Singapore and Sweden show reduced surgery times and enhanced patient outcomes once ultra-low-latency video links are integrated.

Smart-city programs are also deploying surveillance cameras, connected streetlights, and environmental monitors, each adding to the enterprise subscriber base. Utilities turn to 5G for real-time grid balancing, and oil-and-gas operators prioritize automated inspection drones. These converging drivers tilt long-term revenue concentration toward the enterprise, increasing average revenue per connection and deepening stickiness within the 5G connections market.

5G Connection Market Report is Segmented by Connection Type (Mobile Broadband, Fixed Wireless Access, and More), End-User (Consumer and Enterprise), Spectrum Band (Sub-1 GHz, 1-6 GHz, and More), Network Architecture (Non-Standalone and Standalone), Device Category (Smartphones and Tablets, FWA CPE, and More), Service Type (Enhanced Mobile Broadband (eMBB), Massive Machine-Type Communications (mMTC), and More), and Geography.

Geography Analysis

Asia-Pacific accounted for 52% of global subscriptions in 2024 and is forecast to grow at a 30.28% CAGR through 2030, led by China's 4.4 million base stations and India's rapid standalone expansion. China's digital-economy contribution is set to reach USD 2 trillion by 2030, reflecting widespread 5G platform adoption in manufacturing, retail, and services. India's Reliance Jio operates over 1 million cloud-native cell sites, while expected FWA lines could climb from 5 million to 30 million by 2027. Japan's and South Korea's early commercial 5G Advanced launches sustain regional innovation leadership, and Southeast Asia projects USD 130 billion in incremental GDP impact by 2030.

North America is a mature yet innovation-centric arena where 98% of the population already has 5G coverage. T-Mobile's nationwide SA deployment and 6.43 million FWA lines illustrate consumer and enterprise diversification. Verizon's satellite partnership with AST SpaceMobile seeks to close residual rural gaps, while Canadian and Mexican carriers integrate 5G Advanced features such as RedCap. Focus now turns to monetizing network APIs, edge compute, and AI-assisted service orchestration, driving higher revenue density per site across the 5G connections market.

Europe displays mixed progress: Germany, Denmark and Finland exceed 95% population coverage, yet only 2% of subscriptions run on SA cores. The United Kingdom's Vodafone-Three merger injects USD 14.86 billion into network upgrades aimed at rural inclusion, and Nordic spectrum-sharing models yield higher availability at lower cost. Continental operators now press regulators to streamline auctions and lower license fees to sustain investment cycles, seeking to close the SA gap and unlock greater value in the 5G connections market.

- AT&T Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- China Mobile Ltd.

- China Telecommunications Corp.

- T-Mobile US Inc.

- Telstra Corp. Ltd.

- Telefonica SA

- Deutsche Telekom AG

- Reliance Jio Infocomm Ltd.

- SK Telecom Co. Ltd.

- NTT Docomo Inc.

- KT Corp.

- Orange SA

- KDDI Corp.

- Bharti Airtel Ltd.

- Saudi Telecom Company (stc)

- Rakuten Mobile Inc.

- Etisalat by eand

- MTN Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in mobile data traffic requiring higher-capacity networks

- 4.2.2 Fixed Wireless Access (FWA) emerging as mainstream broadband alternative

- 4.2.3 Enterprise digitization and IoT accelerating 5G adoption

- 4.2.4 Generative-AI-driven uplink surge spurring early 5G-SA roll-outs

- 4.2.5 Monetization via Open-API ecosystems

- 4.3 Market Restraints

- 4.3.1 High CAPEX and mid-band spectrum costs

- 4.3.2 Rural coverage economics remain unattractive

- 4.3.3 Fiber price wars dampen urban FWA uptake

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connection Type

- 5.1.1 Mobile Broadband

- 5.1.2 Fixed Wireless Access

- 5.1.3 M2M and IoT

- 5.1.4 Mission-critical Communications

- 5.1.5 Private Networks

- 5.2 By End-user

- 5.2.1 Consumer

- 5.2.2 Enterprise

- 5.2.2.1 Manufacturing

- 5.2.2.2 Healthcare

- 5.2.2.3 Automotive and Transportation

- 5.2.2.4 Smart Cities and Public Safety

- 5.2.2.5 Energy and Utilities

- 5.2.2.6 Retail and Logistics

- 5.3 By Spectrum Band

- 5.3.1 Sub-1 GHz (Low-Band)

- 5.3.2 1-6 GHz (Mid-Band)

- 5.3.3 above 24 GHz (mmWave / High-Band)

- 5.4 By Network Architecture

- 5.4.1 Non-Standalone (NSA)

- 5.4.2 Standalone (SA)

- 5.5 By Device Category

- 5.5.1 Smartphones and Tablets

- 5.5.2 FWA CPE

- 5.5.3 IoT Modules and Gateways

- 5.5.4 Wearables and AR/VR Devices

- 5.5.5 Industrial Routers and Rugged Modules

- 5.6 By Service Type

- 5.6.1 Enhanced Mobile Broadband (eMBB)

- 5.6.2 Massive Machine-Type Communications (mMTC)

- 5.6.3 Ultra-Reliable Low-Latency Communications (URLLC)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 UAE

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AT&T Inc.

- 6.4.2 Verizon Communications Inc.

- 6.4.3 Vodafone Group Plc

- 6.4.4 China Mobile Ltd.

- 6.4.5 China Telecommunications Corp.

- 6.4.6 T-Mobile US Inc.

- 6.4.7 Telstra Corp. Ltd.

- 6.4.8 Telefonica SA

- 6.4.9 Deutsche Telekom AG

- 6.4.10 Reliance Jio Infocomm Ltd.

- 6.4.11 SK Telecom Co. Ltd.

- 6.4.12 NTT Docomo Inc.

- 6.4.13 KT Corp.

- 6.4.14 Orange SA

- 6.4.15 KDDI Corp.

- 6.4.16 Bharti Airtel Ltd.

- 6.4.17 Saudi Telecom Company (stc)

- 6.4.18 Rakuten Mobile Inc.

- 6.4.19 Etisalat by eand

- 6.4.20 MTN Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

5G毫米波中继器-2026年至2032年全球市占率及排名、总收入及需求预测

5G毫米波中继器-2026年至2032年全球市占率及排名、总收入及需求预测 2026年全球5G网路人工智慧(AI)市场报告

2026年全球5G网路人工智慧(AI)市场报告 4G 和 5G 市场:按组件、网路技术、频段、频段所有权、网路架构、部署形式、部署模式和最终用户划分——2026 年至 2032 年全球市场预测5G非地面网路市场:依部署类型、安装位置、频段、最终用户和应用程式划分-2026-2032年全球市场预测LTE 和 5G 关键通讯市场:按技术、组件、终端用户产业、部署模式和应用划分-2026 年至 2032 年全球市场预测共用及免许可频宽LTE/5G网路生态系统市场:依组件、技术、部署模式、频段及最终用户产业划分-2026-2032年全球市场预测2026年全球资料仓储迁移市场报告2026年全球非地面网路(NTN)核心网路软体市场报告非地面网路(NTN)设备卫星 -行动电话策略控制全球市场报告 2026

4G 和 5G 市场:按组件、网路技术、频段、频段所有权、网路架构、部署形式、部署模式和最终用户划分——2026 年至 2032 年全球市场预测5G非地面网路市场:依部署类型、安装位置、频段、最终用户和应用程式划分-2026-2032年全球市场预测LTE 和 5G 关键通讯市场:按技术、组件、终端用户产业、部署模式和应用划分-2026 年至 2032 年全球市场预测共用及免许可频宽LTE/5G网路生态系统市场:依组件、技术、部署模式、频段及最终用户产业划分-2026-2032年全球市场预测2026年全球资料仓储迁移市场报告2026年全球非地面网路(NTN)核心网路软体市场报告非地面网路(NTN)设备卫星 -行动电话策略控制全球市场报告 2026 客户体验即服务 (CXaaS) 市场分析及至 2035 年预测:类型、产品类型、技术、组件、应用、部署模式、最终用户、解决方案、交付模式

客户体验即服务 (CXaaS) 市场分析及至 2035 年预测:类型、产品类型、技术、组件、应用、部署模式、最终用户、解决方案、交付模式