|

市场调查报告书

商品编码

1851114

双向拉伸聚丙烯薄膜:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)BOPP Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

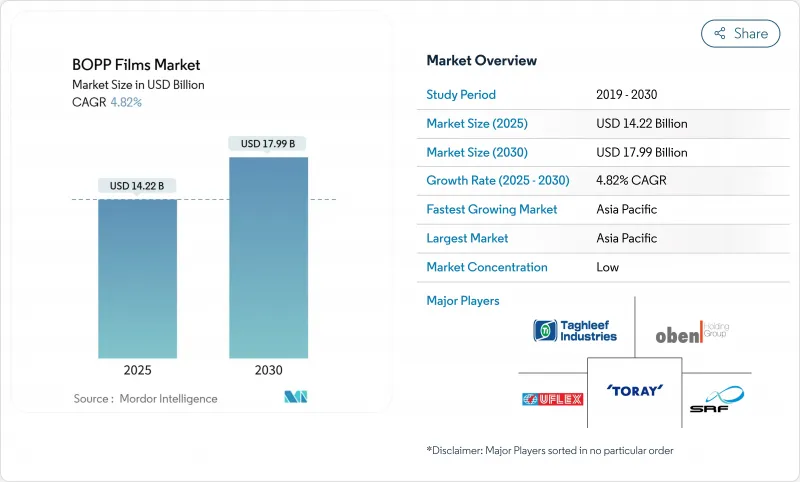

全球BOPP薄膜市场预计到2025年将达到142.2亿美元,到2030年将达到179.9亿美元,预测期内复合年增长率为4.82%。

成长的驱动力来自简化的监管流程,这些流程缩短了食品接触材料的核准週期,并加速了新型双轴延伸聚丙烯(BOPP) 配方在零食、药品和电商包装领域的应用。数位零售的兴起促使品牌所有者更倾向于轻巧、可热封的邮寄薄膜。同时,聚丙烯树脂价格的波动(预计2025年初北美地区每磅上涨4-5美分)持续挤压加工商的利润空间,促使企业进行垂直整合并采取避险策略。在政策方面,欧盟的《包装和包装废弃物法规》(PPWR) 要求到2030年所有包装都必须可回收利用,这将推动全球供应链对单一材料BOPP结构的需求。

全球双向拉伸聚丙烯薄膜市场趋势与洞察

开发中国家对高密封性零食包装的需求激增

都市区杂货店的扩张和区域零食品牌的优质化正推动双向拉伸聚丙烯薄膜(BOPP)市场向透明、高光泽等级发展。印度零食製造商如Haldiram's目前正利用透明BOPP将保质期延长高达20%,并提高产品在现代零售展示中的可见度。东南亚也出现了类似的转变,食品安全法规鼓励使用透明包装以便于检查。此举不仅在提供经济高效的阻隔性能的同时,还能透过防篡改密封减少废弃物。与PET相比,由于加工成本较低,新兴企业将继续成为主要采用者,以确保2030年市场需求持续成长。

品牌拥有者为实现永续性目标,从PVC包装膜转向BOPP包装膜

监管机构施压要求淘汰含卤材料,这加速了全球从PVC包装膜转向双向拉伸聚丙烯(BOPP)包装膜的转变。联合利华承诺在2026年前淘汰PVC,并于2024年做出承诺,因此在其食品和个人保健产品线的软包装中选择了BOPP薄膜。对于雀巢而言,此举简化了回收物流,从而节省了10-15%的成本。糖果甜点包装膜采用BOPP后,回收率也从23%飙升至87%。加工商正在投资新的封口钳和设备维修,但遵循成本的降低和品牌股权的提升抵消了资本投资的障碍。

聚丙烯树脂价格波动

预计2025年初北美聚丙烯价格将上涨4-5美分/磅,与2024年开始的类似涨幅相呼应。印度双向拉伸聚丙烯(BOPP)价格曾达到每吨1020美元,但国内需求仅增长11%,而新增产能却增长了20%,导致行业盈利跌至十年来的最低点8%。加工企业面临现金流紧张的局面,并加速併购以实现规模经济。

细分市场分析

预计到2030年,金属化薄膜的复合年增长率将达到8.36%。到2024年,透明薄膜将占以金额为准的51.32%,对于强调产品新鲜度的零食和烘焙食品橱窗而言至关重要。加工商对高真空金属化设备的投资,使得泡壳包装的金属化BOPP薄膜市场规模将超过30亿美元。

白色、不透明和珠光等级的BOPP薄膜常用于标籤纸、胶带和高檔包装,以提供美观的对比度和紫外线阻隔性,但与通用透明等级的BOPP薄膜相比,其市场份额仍然较小。诸如AluBond和AlOx之类的特种涂层透过提高与金属的黏合性和光学透明度,拓宽了BOPP薄膜的应用范围,并正在推动BOPP薄膜市场的发展,以替代受监管药品包装盒中的PVdC涂层PVC。

厚度大于45微米的薄膜市场正以7.54%的复合年增长率成长,这主要得益于工业胶带、化肥袋和立式袋等需要机械刚度的应用领域。 15-30微米厚度的薄膜仍占36.34%的市场份额,在註重成本平衡的零嘴零食包装和标籤领域保持主导地位。顺序双轴取向技术目前已将机器方向的取向角度提升至12度,使以往仅限于较厚薄膜的性能也能应用于更薄的薄膜。这种技术变革可能会逐渐削弱厚薄膜在非关键包装领域的优势。

厚度小于15微米的特殊薄膜面临捲绕和穿孔的问题,但聚合物成核剂和可控冷却技术可以改善其製程稳定性。厚度为30-45微米的中厚薄膜仍然是药品包装和高檔咖啡内衬的主要材料,兼顾了刚度和阻隔性能。这种多样性体现了双向拉伸聚丙烯薄膜市场多层次的成长模式。

本报告涵盖双轴延伸聚丙烯薄膜的市场分析,按薄膜类型(透明、金属化、其他)、厚度(小于 15 毫米、15-30 毫米、其他)、应用(包装、标籤、环绕、其他)、最终用户行业(食品、食品和饮料、其他)以及地区(北美、欧洲、亚太地区、南美、中东和非洲)进行细分。

区域分析

亚太地区预计到2024年将占总营收的45.21%,复合年增长率(CAGR)高达8.43%,是成长最快的地区,这主要得益于印度聚合物消费量在2024财年至2025财年间增长8.5%。一体化生产、低廉的人事费用以及接近性零食和医药市场等优势,为亚太地区带来了结构性优势。然而,烯烃供应过剩和老旧资产运作正在挤压利润空间,促使企业采取选择性停产和出口导向生产模式的调整。

在北美,随着电子商务拓展农村配送业务并推动邮寄薄膜消费,市场需求稳定成长。然而,树脂的挥发性正挑战加工商的盈利,并促使他们在垂直整合和再生材料应用方面进行创新。在欧洲,为满足PPWR法规的要求,阻隔性可回收复合材料的需求推动了本地品牌所有者对单一材料双向拉伸聚丙烯(BOPP)的投资。

中东和非洲正受益于基础设施的改善。 UFlex位于埃及的工厂毗邻消费市场,并可利用其与欧洲的贸易便利。在南美,当地食品加工商瞄准的是品牌化的常温零嘴零食,但货币波动和对树脂进口的依赖限制了成长。这些区域案例凸显了双向拉伸聚丙烯薄膜市场地理分布的多样性。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 开发中国家对高透明度零嘴零食包装的需求激增

- 品牌拥有者出于永续性目标,将PVC包装膜更换为BOPP包装膜。

- 电子商务的蓬勃发展推动了热封BOPP邮寄薄膜的需求。

- 一家综合性聚烯製造商迅速扩大产能

- 可回收单一材料层压板的商业化

- 市场限制

- 聚丙烯树脂价格波动

- 中国运作的传统生产线拉低了全球利润率

- 在高端细分市场中,生物基阻隔薄膜面临竞争

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要宏观经济趋势对市场的影响

第五章 市场规模与成长预测

- 按胶片类型

- 透明的

- 金属化

- 不透明/白色

- 珠光

- 其他胶片类型

- 按厚度

- 小于15微米

- 15-30µm

- 30-45µm

- 45微米或以上

- 透过使用

- 包裹

- 标籤和环绕

- 贴合加工

- 感压胶带

- 其他应用

- 按最终用户行业划分

- 食物

- 饮料

- 製药和医疗

- 个人护理和化妆品

- 产业

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 肯亚

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Taghleef Industries

- Jindal Poly Films

- Toray Industries

- SRF Limited

- Uflex Ltd

- Cosmo Films

- Polyplex Corp

- Oben Holding Group

- Treofan Group

- Vacmet India

- NAN YA Plastics

- Mitsui Chemicals Tohcello

- Futamura Chemical

- Innovia Films

- Irplast SpA

- Inteplast Group

- Biofilm SA

- Manucor Spa

- Dunmore Corp

- Tatrafan SRO

第七章 市场机会与未来展望

The global BOPP films market size stands at USD 14.22 billion in 2025 and is projected to advance to USD 17.99 billion by 2030, translating into a 4.82% CAGR over the forecast period.

Growth stems from regulatory streamlining that shortens food-contact approval cycles, accelerating adoption of novel biaxially oriented polypropylene (BOPP) formulations for snack, pharmaceutical, and e-commerce packaging. Rising digital retail has pushed brand owners to favor lightweight, heat-sealable mailer films that reduce packaging volume by 23% compared with corrugated formats. Meanwhile, polypropylene resin volatility-prices in North America rose 4-5 cents per pound in early 2025-continues to squeeze converter margins, encouraging vertical integration and hedging instruments. On the policy front, the European Union's Packaging and Packaging Waste Regulation (PPWR) requires all packaging to be recyclable by 2030, catalyzing demand for mono-material BOPP structures across global supply chains.

Global BOPP Films Market Trends and Insights

Surging Demand for High-Clarity Snack Packaging in Developing Economies

Urban grocery expansion and premiumization of regional snack brands are pushing the BOPP films market toward transparent, high-clarity grades. Indian snack producers such as Haldiram's now leverage transparent BOPP to extend shelf life by up to 20%, boosting product visibility in modern retail displays. Similar shifts in Southeast Asia are driven by food-safety rules that favor see-through packs for easy inspection. The move enables cost-effective barrier performance while reducing waste through tamper-evident seals. Emerging players, incentivized by lower conversion costs versus PET, remain key adopters, ensuring sustained demand through 2030.

Brand-Owner Switch from PVC Wrap to BOPP for Sustainability Goals

Regulatory pressure to eliminate halogenated substrates has accelerated the global pivot from PVC wraps to BOPP. Unilever's 2024 commitment to phase out PVC by 2026 frames BOPP films as the material of choice for flexible packs across food and personal care lines. The shift yields 10-15% cost savings at Nestle due to simplified recycling logistics, while recyclability rates jumped from 23% to 87% after migrating confectionery wraps to BOPP. Converters invest in new sealing jaws and equipment retrofits, but lower compliance fees and positive brand equity offset capex hurdles.

Volatility in Polypropylene Resin Prices

North American polypropylene prices climbed 4-5 cents per pound in early 2025, echoing similar hikes from 2024. India's BOPP prices touched USD 1,020 per ton, yet domestic demand rose only 11% against 20% fresh capacity, pushing industry profitability toward a decade-low 8%. Converters face cash-flow strain and accelerate M&A to gain economies of scale.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Boom Driving Heat-Sealable BOPP Mailer Films

- Commercialization of Recycle-Ready Mono-Material Laminates

- Under-Utilized Legacy Lines in China Depressing Global Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallized films secured an 8.36% CAGR outlook through 2030 as pharmaceutical packs demand superior oxygen and moisture barriers. Transparent films held 51.32% of the BOPP films market in 2024 by value, proving indispensable in snack and bakery windows that highlight product freshness. Converter investment in high-vacuum metallizers supports premium foil-equivalent performance at lower weight. In parallel, the BOPP films market size tied to metallized grades for blister over-wraps is projected to top USD 3 billion by 2030, buoyed by stringent stability mandates.

White, opaque, and pearlescent variants serve labelstock, tape, and luxury wraps, providing aesthetic contrast and UV opacity. Yet, their share remains niche compared with commodity clear grades. Specialty coatings such as AluBond and AlOx are widening the application canvas by improving metal adhesion and optical clarity, reinforcing the BOPP films market as a replacement for PVdC-coated PVC within regulated drug cartons.

Films above 45 µm are growing at 7.54% CAGR thanks to industrial tapes, fertilizer bags, and stand-up pouches that need mechanical rigidity. The 15-30 µm segment nonetheless captures 36.34% of the BOPP films market size, maintaining primacy for cost-balanced snack wraps and labels. Sequential biaxial stretching techniques now raise machine-direction orientation to ratios of 12, yielding thinner films with performance once limited to heavier gauges. This engineering shift could gradually erode heavy-gauge dominance in non-critical packaging.

The sub-15 µm niche faces winding and puncture concerns; however, polymer nucleating agents and controlled cooling have improved process stability. Middle-weight 30-45 µm films remain staples for pharmaceutical over-wrap and premium coffee liners, balancing stiffness and barrier demands. Such diversity illustrates the multi-tiered growth profile underlying the BOPP films market.

The Report Covers Biaxially Oriented Polypropylene Films Market Analysis and is Segmented by Film Type ( Transparent, Metallized, and More), Thickness ( Less Than 15 Mm, 15 - 30 Mm, and More), Application (Packaging, Labeling and Wrap-Arounds, and More), End-User Vertical (Food, Beverage, and More) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific accounted for 45.21% of 2024 revenue and records the fastest 8.43% CAGR, underscored by India's polymer consumption growth of 8.5% in FY 2024-25. Integrated production, low labor costs, and proximity to snack and pharmaceutical demand create structural advantages. Nonetheless, olefin oversupply and under-utilized legacy assets weigh on margins, prompting selective shutdowns and export rebalancing.

North America illustrates steady demand growth as e-commerce expands rural deliveries, fueling mailer film consumption. Resin volatility, however, challenges converter profitability, spurring vertical integration and recycled-content innovations. Europe centers on high-barrier, recycle-ready laminates to meet PPWR mandates, encouraging mono-material BOPP investments among local brand owners.

The Middle East & Africa benefits from infrastructure upgrades; UFlex's Egypt complex positions it near consumer markets while leveraging trade access to Europe. South America advances as local food processors move toward branded, shelf-stable snacks, yet currency volatility and import dependency on resin temper growth. Together, these regional narratives underline the geographically diversified trajectory of the BOPP films market.

- Taghleef Industries

- Jindal Poly Films

- Toray Industries

- SRF Limited

- Uflex Ltd

- Cosmo Films

- Polyplex Corp

- Oben Holding Group

- Treofan Group

- Vacmet India

- NAN YA Plastics

- Mitsui Chemicals Tohcello

- Futamura Chemical

- Innovia Films

- Irplast S.p.A

- Inteplast Group

- Biofilm SA

- Manucor Spa

- Dunmore Corp

- Tatrafan SRO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for high-clarity snack packaging in developing economies

- 4.2.2 Brand-owner switch from PVC wrap to BOPP for sustainability goals

- 4.2.3 E-commerce boom driving heat-sealable BOPP mailer films

- 4.2.4 Rapid capacity additions by integrated polyolefin producers

- 4.2.5 Commercialization of recycle-ready mono-material laminates

- 4.3 Market Restraints

- 4.3.1 Volatility in polypropylene resin prices

- 4.3.2 Under-utilized legacy lines in China depressing global margins

- 4.3.3 Competition from bio-based barrier films in premium niches

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Key Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Type

- 5.1.1 Transparent

- 5.1.2 Metallized

- 5.1.3 Opaque / White

- 5.1.4 Pearlescent

- 5.1.5 Other Film Type

- 5.2 By Thickness

- 5.2.1 Less than 15 µm

- 5.2.2 15 - 30 µm

- 5.2.3 30 - 45 µm

- 5.2.4 More than 45 µm

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Labeling and Wrap-Arounds

- 5.3.3 Laminating

- 5.3.4 Pressure-Sensitive Tapes

- 5.3.5 Other Application

- 5.4 By End-user Vertical

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Pharmaceutical and Medical

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Industrial

- 5.4.6 Other End-user Vertical

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Taghleef Industries

- 6.4.2 Jindal Poly Films

- 6.4.3 Toray Industries

- 6.4.4 SRF Limited

- 6.4.5 Uflex Ltd

- 6.4.6 Cosmo Films

- 6.4.7 Polyplex Corp

- 6.4.8 Oben Holding Group

- 6.4.9 Treofan Group

- 6.4.10 Vacmet India

- 6.4.11 NAN YA Plastics

- 6.4.12 Mitsui Chemicals Tohcello

- 6.4.13 Futamura Chemical

- 6.4.14 Innovia Films

- 6.4.15 Irplast S.p.A

- 6.4.16 Inteplast Group

- 6.4.17 Biofilm SA

- 6.4.18 Manucor Spa

- 6.4.19 Dunmore Corp

- 6.4.20 Tatrafan SRO

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2034年BOPP薄膜市场规模、份额、趋势及预测(按类型、厚度、製造流程、应用和地区划分)日本双向拉伸聚丙烯薄膜市场规模、份额、趋势及预测(按类型、厚度、製造流程、应用和地区划分),2026-2034年

2026-2034年BOPP薄膜市场规模、份额、趋势及预测(按类型、厚度、製造流程、应用和地区划分)日本双向拉伸聚丙烯薄膜市场规模、份额、趋势及预测(按类型、厚度、製造流程、应用和地区划分),2026-2034年 BOPP 薄膜市场-全球产业规模、份额、趋势、机会和预测,按类型、厚度、生产流程、应用、地区和竞争细分,2020-2030 年

BOPP 薄膜市场-全球产业规模、份额、趋势、机会和预测,按类型、厚度、生产流程、应用、地区和竞争细分,2020-2030 年 BOPP 薄膜市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

BOPP 薄膜市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 印度 BOPP 薄膜:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

印度 BOPP 薄膜:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 全球BOPP薄膜市场(2016-2036)

全球BOPP薄膜市场(2016-2036) BOPP薄膜市场规模、份额、趋势分析报告:按类型、厚度、製造流程、应用、地区和细分市场预测,2024-2030年

BOPP薄膜市场规模、份额、趋势分析报告:按类型、厚度、製造流程、应用、地区和细分市场预测,2024-2030年