|

市场调查报告书

商品编码

1851220

3D列印材料和服务:市场份额分析、行业趋势、统计数据和成长预测(2025-2030年)3D Printing Materials And Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

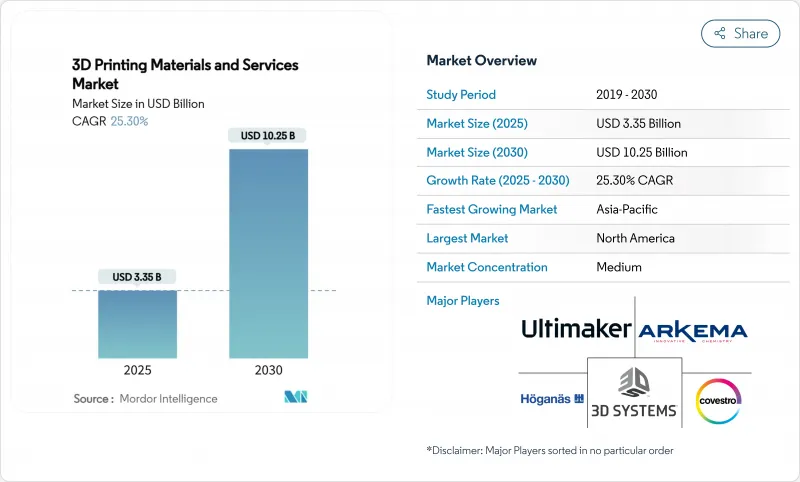

预计到 2025 年,3D 列印材料和服务市场规模将达到 33.5 亿美元,到 2030 年将达到 102.5 亿美元,预测期(2025-2030 年)的复合年增长率为 25.30%。

这一成长反映了航太、医疗保健和电动车等领域从快速原型製作向认证生产级应用的稳定转变。需求成长主要得益于列印即服务订阅模式的普及,该模式使中小企业能够避免巨额资本支出;此外,监管机构对金属增材製造(AM)在航空关键部件製造方面的认可也推动了这一增长。混合挤出、生物相容性聚合物和可回收长丝的出现拓展了材料选择范围,而成本压力则促使製造商转向分散式按需製造模式。

北美国防资金、欧盟绿色交易激励措施以及亚太地区数位化製造的推动,共同支撑了这一发展势头。服务业务将在2024年维持58%的领先收入份额,并将在2030年之前实现14%的最快复合年增长率。儘管FDM/FFF技术拥有最大的装机量,但多射流熔融(MJF)和黏着剂喷涂成型正以每年15%的速度成长,这得益于它们的高产能和等向性,使其适用于中小批量生产。虽然丝材仍是主流形式,但粉末的使用量正以每年14%的速度成长,这主要得益于钛合金和铝合金的广泛应用。儘管原型製作仍占营收的42%,但功能性零件的复合年增长率也达到了15%,尤其是在航太领域,轻量化、整合的结构能够缩短供应链。总体而言,3D列印材料和服务市场正进入一个认证生产、永续性和服务模式相互交融的阶段,这将为各行各业释放新的利润空间。

全球3D列印材料及服务市场趋势及洞察

金属积层製造技术在航太的快速应用

监管机构现已接受经认证的金属增材製造(AM)零件用于航空领域。 Materialise公司将于2025年获得EN9100认证,届时将可供应符合航太品质标准的钛合金和铝合金结构件。 3D Systems公司已为太空任务交付了超过2000个关键的钛合金和铝合金零件。这些里程碑事件检验了积层製造技术在安全关键零件製造方面的应用价值,并加速了从传统铸造方式转型为积层製造的。

成本压力推动按需服务的发展

不断上涨的库存和模具成本正促使製造商将生产外包给分散的服务机构。 MX3D计画在2025年募集700万欧元,以按需列印模式拓展电弧增材製造业务,该模式可将原料浪费减少高达90%。 Protolabs报告称,其2024年3D列印收入将达到8,300万美元,这表明其以服务为先的商业性模式取得了成功,该模式缩短了前置作业时间并提高了自由现金流。

高纯度金属粉末价格波动

由于矿石短缺和监管限制,钛粉和铜粉价格波动,推高了航太和医疗器材製造的材料成本。钛增材製造市场预计到2032年将达到14亿美元,但供应的不确定性迫使原始设备製造商(OEM)囤积原料或回收废料以维持利润率。

细分市场分析

到2024年,服务收入将占总收入的58%,年复合成长率达14%,这主要得益于企业将设计检验和小批量生产外包。预计到2025年,3D列印材料和服务市场规模将达到19.4亿美元,到2030年将超过61亿美元。像3Dock这样的供应商提供的订阅方案降低了间歇性用户的进入门槛。虽然材料规模较小,但高利润率的特殊粉末和生物聚合物正在推动服务创新。

材料板块正以每年12%的速度成长,主要成长动力来自粉末床熔融用粉末。到2024年,长丝将占据最大份额,达到48%。惠普的无卤PA 12 FR展示了工程聚合物如何在满足严格的阻燃标准的同时,降低20%的营运成本。再生长丝和复合颗粒技术的进步,吸引了那些寻求更低环境影响的客户,并增强了以材料主导的服务差异化优势。

由于其庞大的装机量和亲民的价格分布, FDM/FFF技术预计在2024年将保持38%的市场份额。此细分市场仍维持11%的成长,但成长不及MJF和黏着剂喷涂成型,后者的复合年增长率高达15%。这些粉末基技术具有近乎等向性的特性,适用于夹具、固定装置以及中小批量生产。惠普与INDO-MIM的黏着剂喷涂伙伴关係正在扩大金属零件的生产规模,这些零件已通过航太检验,展现出批量生产的潜力。

SLA、DLP 和 SLS 技术在精密牙科模型和医疗设备领域仍然具有重要意义。 EOS 系统可在数天内生产出病患客製化的颅骨植入,进而提高医院的效率。线弧增材製造目前仍属于小众技术,但正如 MX3D 的融资扩张所表明的那样,它在能源和海事领域的大型钛结构製造方面正逐渐崭露头角。

3D 列印材料和服务市场按产品(材料及其他)、技术(FDM/FFF、SLS/SLA/DLP、DMLS/EBM/L-PBF 及其他)、形式(材料)(丝材、粉末及其他)、应用(原型製作、功能零件及其他)、最终用户(航太与国防、汽车与电动交通及其他)和地区进行细分。

区域分析

到2024年,北美将占总销售额的40%。国防项目加速了金属增材製造(AM)的认证进程,通用电气航空航太公司(GE Aerospace)斥资10亿美元扩建产能,以加强国内增材製造供应链。医院正在采用可列印的解剖模型,将手术时间缩短高达30%,从而成为医疗保健领域的领导者。

欧洲则位居第二,这主要得益于德国庞大的装置容量和欧盟对可回收材料的优惠政策。弗劳恩霍夫研究所将聚丙烯废弃物转化为长丝的计划体现了政策主导的创新。西班牙被指定为Formnext 2025伙伴国,凸显了该地区製造业的復兴和出口导向。

亚太地区是成长最快的地区,复合年增长率达15%。中国正将积层製造技术应用于汽车、电子和髋植入等领域,而日本则专注于精密工具製造。政府补贴、健全的製造业生态系统以及不断增长的医疗保健支出都在支持市场需求。南美和中东等新兴市场也是增材製造技术的成长点,儘管规模较小,但这些地区的积层製造技术已应用于石油天然气零件和航太零件的生产。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 金属增材製造技术在航太航太领域快速应用于符合航空标准的零件

- 成本压力推动美国和欧盟按需製造服务的发展。

- 生物相容性聚合物助力亚洲照护现场发展

- 混合材料挤出製程可实现轻量化电动车零件

- 市场限制

- 高纯度金属粉末价格波动

- 关键零件增材製造的资质标准有限

- 价值/供应链分析

- 监理与技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 新冠疫情与地缘经济影响评估

第五章 市场规模与成长预测

- 报价

- 材料

- 塑胶(PLA、ABS/ASA、PETG、光敏聚合物)

- 金属(Ti-6Al-4V、Inconel、AlSi10Mg、SS 316L)

- 陶瓷(氧化铝、氧化锆、氮化硅)

- 其他复合材料(碳纤维、生物聚合物)

- 服务

- 快速原型製作

- 工具和设备

- 生产/桥樑製造

- 设计及工程服务

- 材料

- 透过技术

- FDM/FFF

- SLS/SLA/DLP

- MJF和黏着剂喷涂成型

- DMLS/EBM/L-PBF

- 其他新兴市场(LCD、CLIP、WAAM)

- 按形式(材料)

- 灯丝

- 粉末

- 液体/树脂

- 透过使用

- 原型製作

- 功能部件

- 模具

- 牙科和整形外科植入

- 最终用户

- 航太/国防

- 汽车与出行

- 医疗保健和生命科学

- 工业机械

- 消费品和电子产品

- 建筑/建筑设计

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 亚太其他地区

- 南美洲

- 巴西

- 其他南美洲

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略性措施与资金筹措

- 市占率分析

- 公司简介

- 3D Systems Corp.

- Stratasys Ltd.

- EOS GmbH

- General Electric(GE Additive)

- HP Inc.

- SLM Solutions Group AG

- Desktop Metal Inc.

- Materialise NV

- Arkema SA

- BASF Forward AM

- Evonik Industries AG

- Hoganas AB

- Sandvik AB

- Royal DSM(Covestro)

- Markforged Holding Corp.

- Protolabs Inc.

- Voxeljet AG

- ExOne(Desktop Metal)

- Carbon Inc.

- Ultimaker BV

- Carpenter Technology Corporation

- Renishaw plc

- Xometry Inc.

第七章 市场机会与未来展望

The 3D Printing Materials And Services Market size is estimated at USD 3.35 billion in 2025, and is expected to reach USD 10.25 billion by 2030, at a CAGR of 25.30% during the forecast period (2025-2030).

This growth reflects the steady shift from rapid prototyping to certified, production-grade uses in aerospace, healthcare and e-mobility. Demand is amplified by Print-as-a-Service subscriptions that let small and medium enterprises avoid large capital outlays, as well as by regulatory acceptance of metal additive manufacturing (AM) in flight-critical parts. Hybrid extrusion, bio-compatible polymers and recyclable filaments are widening the material palette, while cost-down pressures push manufacturers toward distributed, on-demand builds.

Momentum is supported by North American defense funding, EU Green Deal incentives and Asia Pacific's digital manufacturing push. Services hold leadership with 58% revenue share in 2024 and also post the fastest 14% CAGR to 2030. FDM/FFF keeps the largest installed base, yet Multi Jet Fusion (MJF) and Binder Jetting are scaling 15% annually as their throughput and isotropic properties suit low-to-mid-volume production. Filament remains the dominant format, but powder usage is advancing 14% per year on the back of titanium and aluminum alloy adoption. Prototyping still commands 42% of revenue, though functional parts are increasing at 15% CAGR, particularly in aerospace where lightweight, consolidated structures shorten supply chains. Overall, the 3D printing materials and services market is entering a phase where certified production, sustainability and service models intersect to unlock new profit pools across industrial verticals.

Global 3D Printing Materials And Services Market Trends and Insights

Rapid adoption of metal AM in aerospace

Regulators now accept certified metal AM parts for flight use. Materialise obtained EN 9100 accreditation in 2025, unlocking the supply of structural titanium and aluminum components that meet aerospace quality standards. Parallel U.S. defense programs with America Makes are standardizing qualification pathways, and 3D Systems has already delivered over 2,000 mission-critical titanium or aluminum components for space missions.These milestones validate AM for safety-critical parts, accelerating procurement away from legacy castings.

Cost-down pressure fueling on-demand services

Inventory inflation and tooling costs have led manufacturers to outsource builds to distributed service bureaus. MX3D raised EUR 7 million in 2025 to scale Wire Arc AM on a Print-on-Demand model that cuts raw-material waste by up to 90%. Protolabs reported USD 83 million in 2024 3D-printing revenue, illustrating commercial traction for service-first models that compress lead time and free cash flow.

Volatility of high-purity metal powder prices

Prices for titanium and copper powders swing with ore shortages and regulatory curbs, inflating bill-of-material costs for aerospace and medical builds. The titanium AM market is expected to reach USD 1.4 billion by 2032, yet supply instability forces OEMs to stockpile feedstock and recycle scrap to maintain margins, especially in Europe, where energy tariffs are high.

Other drivers and restraints analyzed in the detailed report include:

- Bio-compatible polymers for point-of-care

- Hybrid extrusion for lightweight e-mobility

- Energy-intensive post-processing inflating TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services generated 58% of 2024 revenue and are expanding at a 14% CAGR as enterprises outsource design validation and low-volume production. The 3D printing materials and services market size for services stood at USD 1.94 billion in 2025 and is forecast to exceed USD 6.1 billion by 2030. Subscription packages from providers like 3Dock lower entry barriers for intermittent users. Materials, while smaller, fuel service innovation through higher-margin specialty powders and bio-polymers.

The materials segment is growing 12% per year, propelled by powders for powder-bed fusion. Filament held the largest 48% share in 2024. HP's halogen-free PA 12 FR illustrates how engineered polymers trim operating costs by 20% while meeting strict flame-retardancy norms. Advancements in recycled filament and composite pellets appeal to customers seeking lower environmental impact, reinforcing material-driven differentiation within service offerings.

FDM/FFF retained a 38% revenue share in 2024 through its vast installed base and accessible price point. The segment still registers 11% growth, but MJF and Binder Jetting are outpacing it at a 15% CAGR. These powder-based technologies deliver near-isotropic properties that suit jigs, fixtures, and low-to-mid-volume production runs. HP and INDO-MIM's binder-jet partnership is scaling metal parts that pass aerospace validation, indicating readiness for serial output.

SLA, DLP, and SLS retain relevance for precision dental models and medical devices. EOS systems fabricate patient-specific cranial implants within days, enhancing hospital throughput. Wire Arc AM, currently niche, is gaining traction for large titanium structures in energy and maritime sectors, as demonstrated by MX3D's funded expansion.

The 3D Printing Materials & Services Market is Segmented by Offering ( Materials and More), Technology ( FDM / FFF, SLS / SLA / DLP, DMLS / EBM / L-PBF and More), Form (Materials) ( Filament, Powder and More), Application ( Prototyping, Functional Parts and More), End-User ( Aerospace and Defense, Automotive and E-Mobility, and More), and Geography

Geography Analysis

North America accounted for 40% of 2024 revenue. Defense programs accelerate metal AM qualification, and GE Aerospace's USD 1 billion capacity expansion will strengthen domestic AM supply chains. Hospitals adopt printed anatomical models that cut surgical time by up to 30%, adding healthcare pull.

Europe holds the second-largest position, bolstered by Germany's installed base and EU incentives for recyclable materials. Fraunhofer's project that converts polypropylene waste to filament illustrates policy-driven innovation. Spain's designation as Formnext 2025 partner country underscores the region's manufacturing renaissance and export orientation.

Asia Pacific is the fastest-growing region at 15% CAGR. China deploys AM for automotive, electronics, and hip implants, while Japan emphasizes precision tooling. Government grants, a deep manufacturing ecosystem, and rising healthcare spending underpin demand. Emerging markets in South America and the Middle East use AM for oil-and-gas spares and aerospace parts, providing additional, though smaller, growth nodes.

- 3D Systems Corp.

- Stratasys Ltd.

- EOS GmbH

- General Electric (GE Additive)

- HP Inc.

- SLM Solutions Group AG

- Desktop Metal Inc.

- Materialise NV

- Arkema SA

- BASF Forward AM

- Evonik Industries AG

- Hoganas AB

- Sandvik AB

- Royal DSM (Covestro)

- Markforged Holding Corp.

- Protolabs Inc.

- Voxeljet AG

- ExOne (Desktop Metal)

- Carbon Inc.

- Ultimaker B.V.

- Carpenter Technology Corporation

- Renishaw plc

- Xometry Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study AssumptionsandMarket Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Metal AM in Aerospace for Air-Worthiness Certified Parts

- 4.2.2 Cost-Down Pressure Fueling On-Demand Manufacturing Services in USandEU

- 4.2.3 Bio-compatible Polymers Unlocking Point-of-Care Medical Printing in Asia

- 4.2.4 Hybrid Material Extrusion Enabling Lightweight e-Mobility Components

- 4.3 Market Restraints

- 4.3.1 Volatility of High-Purity Metal Powder Prices

- 4.3.2 Limited Qualification Standards for AM in Critical Parts

- 4.4 Value/Supply-Chain Analysis

- 4.5 RegulatoryandTechnological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 COVID-19 and Geo-economic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Materials

- 5.1.1.1 Plastics (PLA, ABS/ASA, PETG, Photopolymers)

- 5.1.1.2 Metals (Ti-6Al-4V, Inconel, AlSi10Mg, SS 316L)

- 5.1.1.3 Ceramics (Alumina, Zirconia, Silicon Nitride)

- 5.1.1.4 CompositesandOthers (Carbon-Fiber, Bio-Polymers)

- 5.1.2 Services

- 5.1.2.1 Rapid Prototyping

- 5.1.2.2 ToolingandFixtures

- 5.1.2.3 Production / Bridge Manufacturing

- 5.1.2.4 DesignandEngineering Services

- 5.1.1 Materials

- 5.2 By Technology

- 5.2.1 FDM / FFF

- 5.2.2 SLS / SLA / DLP

- 5.2.3 MJFandBinder Jetting

- 5.2.4 DMLS / EBM / L-PBF

- 5.2.5 Other Emerging (LCD, CLIP, WAAM)

- 5.3 By Form (Materials)

- 5.3.1 Filament

- 5.3.2 Powder

- 5.3.3 Liquid / Resin

- 5.4 By Application

- 5.4.1 Prototyping

- 5.4.2 Functional Parts

- 5.4.3 ToolingandMolds

- 5.4.4 DentalandOrthopedic Implants

- 5.5 By End-user

- 5.5.1 AerospaceandDefense

- 5.5.2 Automotiveande-Mobility

- 5.5.3 HealthcareandLife Sciences

- 5.5.4 Industrial Machinery

- 5.5.5 Consumer ProductsandElectronics

- 5.5.6 ConstructionandArchitecture

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 US

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 UK

- 5.6.2.4 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 Rest of Asia Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic MovesandFunding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, ProductsandServices, and Recent Developments)

- 6.4.1 3D Systems Corp.

- 6.4.2 Stratasys Ltd.

- 6.4.3 EOS GmbH

- 6.4.4 General Electric (GE Additive)

- 6.4.5 HP Inc.

- 6.4.6 SLM Solutions Group AG

- 6.4.7 Desktop Metal Inc.

- 6.4.8 Materialise NV

- 6.4.9 Arkema SA

- 6.4.10 BASF Forward AM

- 6.4.11 Evonik Industries AG

- 6.4.12 Hoganas AB

- 6.4.13 Sandvik AB

- 6.4.14 Royal DSM (Covestro)

- 6.4.15 Markforged Holding Corp.

- 6.4.16 Protolabs Inc.

- 6.4.17 Voxeljet AG

- 6.4.18 ExOne (Desktop Metal)

- 6.4.19 Carbon Inc.

- 6.4.20 Ultimaker B.V.

- 6.4.21 Carpenter Technology Corporation

- 6.4.22 Renishaw plc

- 6.4.23 Xometry Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-spaceandUnmet-need Assessment

全球 3D 列印材料市场(按类型、几何形状、应用、技术、最终用途行业和地区划分)- 预测至 2030 年

全球 3D 列印材料市场(按类型、几何形状、应用、技术、最终用途行业和地区划分)- 预测至 2030 年 全球3D列印材料市场:预测至2032年-依材料类型、形态、列印技术、应用、最终用户及地区进行分析

全球3D列印材料市场:预测至2032年-依材料类型、形态、列印技术、应用、最终用户及地区进行分析 3D 列印材料市场(按材料成分、材料形式、材料等级、最终用途产业和应用)—全球预测,2025-2032 年

3D 列印材料市场(按材料成分、材料形式、材料等级、最终用途产业和应用)—全球预测,2025-2032 年 PET 长丝 3D 列印材料市场 - 预测至 2025 年至 2030 年

PET 长丝 3D 列印材料市场 - 预测至 2025 年至 2030 年 全球光聚合物市场3D列印材料市场:产业趋势及全球预测(~2035年):依材料类型、形态、技术、应用、最终用户及地区3D 列印材料市场分析及预测(至 2034 年):类型、产品、服务、技术、应用、材料类型、最终用户、模式

全球光聚合物市场3D列印材料市场:产业趋势及全球预测(~2035年):依材料类型、形态、技术、应用、最终用户及地区3D 列印材料市场分析及预测(至 2034 年):类型、产品、服务、技术、应用、材料类型、最终用户、模式 光聚合物市场-全球产业规模、份额、趋势、机会及预测(按性能、技术、应用、地区和竞争细分,2020-2030 年)

光聚合物市场-全球产业规模、份额、趋势、机会及预测(按性能、技术、应用、地区和竞争细分,2020-2030 年) 3D列印资料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)全球 3D 列印材料市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

3D列印资料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)全球 3D 列印材料市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测