|

市场调查报告书

商品编码

1851263

北美积体电路市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)NA ICS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

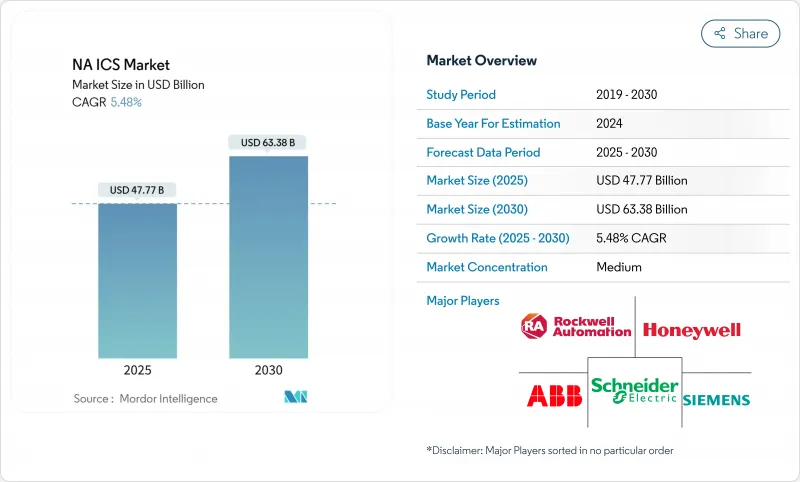

预计到 2025 年,北美工业控制系统市场规模将达到 477.7 亿美元,到 2030 年将达到 633.8 亿美元,复合年增长率为 5.48%。

2024年,硬体仍将维持最大的收入份额,达到57.2%,这主要得益于对PLC、分散式控制硬体和I/O模组的持续投资。美国《晶片与积体电路法案》(CHIPS Act)宣布投资4,500亿美元用于半导体产能建设,以缓解元件短缺并促进新的自动化部署。工业乙太网在2024年占已安装通讯设备的48.9%,但随着工厂寻求灵活的连接方式,无线通讯协定以10.4%的复合年增长率(CAGR)快速发展。云端采用率以9.31%的复合年增长率成长,但由于对延迟敏感的控制迴路和严格的安全策略,81%的云端部署仍保留在本地。汽车製造商占了18.6%的需求份额,但製药业是成长最快的终端用户,复合年增长率达到9.1%,这主要得益于对高品质设计要求的不断提高。

北美ICS - 市场趋势与洞察

美国汽车工厂的棕地现代化改造正在加速进行

汽车製造商正以统一架构取代分散的控制层,以提高灵活性和运转率。奥迪美国车身车间采用了西门子Simatic S7-1500V虚拟控制器,并将其连接到私有云端,以整合IT和OT工作流程,从而缩短换车时间。美国仅有31%的工厂实现了全自动化功能,凸显了现代化改造的巨大空间。金佰利公司逐步将PLC系统迁移到DCS系统,采取了谨慎的策略——在10年内每年迁移一条生产线——以最大限度地减少停机时间,同时建立一个具备网路安全功能的平台。

网实整合安全标准的采用率不断提高

在过去12个月中,93%的OT设施报告了入侵事件,这推动了ISA/IEC 62443框架的快速普及。此框架定义了区域、通道和连续监控。 2025年2月发布的ANSI/ISA-62443-2-1更新引入了成熟度模型,使资产所有者能够根据自身风险状况客製化控制措施。公用事业公司和离散製造企业都在建立纵深防御体系,以减少非计划性停机和保险成本。

遗留的棕地系统被锁定在专有通讯协定中

90年代建造的工厂仍依赖特定厂商的汇流排,这使得资料撷取和云端连接变得复杂。菲尼克斯电气建议逐步迁移I/O以最大程度地减少停机时间,但整合商必须将数千个传统暂存器对应到现代物件模型。伍德PLC指出,考虑到製程的生命週期长达30年,一次性全部更换并不现实,业主需要在未来几年内分期投资建造双栈架构。

细分市场分析

硬体业务占2024年营收的57.2%,主要得益于PLC机架、DCS节点和马达驱动器订单的持续成长。 ABB製程自动化部门预测2024年营收将达到68亿美元,显示市场对资本设备的需求仍强劲。将边缘分析技术整合到控制器中,例如Honeywell的ControlEdge PLC,其内建OPC UA和MQTT功能,正在推动高端产品的销售。

生命週期支援外包虽然目前规模较小,但正以8.9%的复合年增长率快速成长。截至2024年9月,罗克韦尔自动化公司的生命週期服务订单已达17亿美元,这反映出市场对以结果为导向、将费用与可用性提升挂钩的合约的需求。技能短缺问题,尤其是到2025年网路安全负责人缺口将达到350万人,将推动维护合约和远端监控合约的成长,进而提升北美工业控制系统产业的经常性收入。

预计到2024年,PLC将占据北美工业控制系统市场31.4%的份额,主要得益于其确定性控制和久经考验的可靠性。罗克韦尔自动化的Logix控制器系列为该地区的汽车和食品生产线提供动力。目前,供应商提供的PLC产品均具备原生CIP安全功能和TLS加密功能,从而减少了对网关的依赖。

随着製造商寻求批次级溯源和订单到批次的同步,MES平台正以7.6%的复合年增长率快速成长。随着工业4.0的普及,到2024年,全球互联设备数量将翻一番,达到170亿台,由此产生的数据集可被MES转化为可执行的生产KPI。汽车OEM厂商正在利用MES协调机器人喷涂、电池组装和最终检验,缩短产品上市週期,并整合企业资源计画(ERP)。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速美国汽车工厂棕地现代化改造

- 网实整合安全标准(ISA/IEC 62443)正变得越来越普及。

- 美国《晶片法案》提升半导体产能

- 加拿大的净零电网指令促使公用事业公司自动化

- 墨西哥湾沿岸中游液化天然气投资不断成长

- 墨西哥原始设备製造商推出边缘运算预测性维护

- 市场限制

- 遗留的棕地系统被锁定在专有通讯协定中

- OSHA功能安全改造的资本维修成本

- ISA认证的OT网路安全人才短缺

- 北美供应链对稀土磁铁进口的风险敞口

- 价值/供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 按组件

- 硬体

- 软体

- 服务

- 依系统类型

- SCADA(监控与资料收集)

- DCS(分散式控制系统)

- PLC(可程式逻辑控制器)

- MES(製造执行系统)

- 产品生命週期管理 (PLM)

- ERP(企业资源计画)

- 人机介面 (HMI)

- 其他(OTS、机器安全)

- 透过通讯协定

- 现场汇流排

- 工业乙太网

- 无线的

- 透过部署模式

- 本地部署

- 云

- 杂交种

- 按最终用户行业划分

- 车

- 化工/石油化工

- 公共产业(电力/水)

- 製药

- 饮食

- 石油和天然气

- 采矿和金属

- 纸浆和造纸

- 其他的

- 按国家/地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corp.

- Omron Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Yokogawa Electric Corp.

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Advantech Co. Ltd.

- Eaton Corp. plc

- BandR Industrial Automation GmbH

- Beckhoff Automation GmbH

- FANUC Corp.

- Delta Electronics Inc.

- Hitachi Ltd.

- IDEC Corp.

第七章 市场机会与未来展望

The North American industrial control systems market size stands at USD 47.77 billion in 2025 and is projected to reach USD 63.38 billion by 2030, reflecting a 5.48% CAGR.

Hardware retains the largest revenue share at 57.2% in 2024, underpinned by steady investment in PLCs, distributed control hardware, and I/O modules. Demand is reinforced by the U.S. CHIPS Act, which has mobilized USD 450 billion of announced semiconductor capacity investments, easing component shortages and spurring new automation roll-outs. Industrial Ethernet accounted for 48.9% of installed communications in 2024, while wireless protocols advanced at a 10.4% CAGR as plants sought flexible connectivity. Although cloud deployments are expanding at 9.31% CAGR, 81% of installations remain on-premise because of latency-sensitive control loops and strict security policies. Automotive producers captured 18.6% of demand, yet pharmaceuticals are the fastest-growing end user at 9.1% CAGR as quality-by-design mandates intensify.

NA ICS Market Trends and Insights

Accelerated brown-field modernization across U.S. automotive plants

Automotive manufacturers are replacing fragmented control layers with unified architectures to boost flexibility and uptime. Audi's U.S. body shop adopted Siemens Simatic S7-1500V virtual controllers connected to its private cloud, merging IT and OT workflows and shortening change-over times. Only 31% of domestic factories have fully automated a function, highlighting large headroom for modernization. Kimberly-Clark's phased PLC-to-DCS migration illustrates the cautious pace: one line per year over a decade to limit downtime while embedding cybersecurity-ready platforms.

Growing cyber-physical safety standards adoption

Ninety-three percent of OT facilities reported an intrusion in the past 12 months, prompting rapid uptake of ISA/IEC 62443 frameworks that define zones, conduits, and continuous monitoring. The February 2025 ANSI/ISA-62443-2-1 update introduced a maturity model, allowing asset owners to tailor controls to risk profiles. Utilities and discrete manufacturers alike are structuring multi-layer defenses, reducing unplanned outages and insurance premiums.

Legacy brown-field systems with proprietary protocol lock-in

Plants built in the 1990s still rely on vendor-specific buses that complicate data acquisition and cloud connectivity. Phoenix Contact advises staged I/O migration to minimise shutdowns, yet integration crews must map thousands of legacy registers to modern object models-an effort that prolongs project timelines and inflates labor costs. Wood PLC notes that process-site lifecycles of 30 years make wholesale replacement impractical, obliging owners to fund dual-stack architectures for years.

Other drivers and restraints analyzed in the detailed report include:

- U.S. CHIPS Act-fuelled semiconductor capacity build-out

- Canada's net-zero grid mandate driving utility automation

- Capital-intensive retrofit costs for OSHA functional-safety

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware contributed 57.2% of 2024 revenue, led by sustained orders for PLC racks, DCS nodes, and motor drives. ABB's Process Automation unit posted USD 6.8 billion of 2024 sales, showing continued appetite for capital equipment. Integration of edge analytics into controllers, such as Honeywell's ControlEdge PLC with embedded OPC UA and MQTT, is boosting sell-through of premium SKUs.

Services, though smaller, are scaling rapidly at 8.9% CAGR as owners outsource lifecycle support. Rockwell Automation's Lifecycle Services backlog reached USD 1.70 billion in September 2024, reflecting demand for outcome-based contracts that tie fees to availability gains. Skills shortages-3.5 million cybersecurity roles lacking by 2025-push maintenance and remote-monitoring agreements higher, elevating recurring revenue in the North American industrial control systems industry.

PLCs held 31.4% of the North American industrial control systems market size in 2024, valued for deterministic control and proven reliability. Rockwell's Logix controller family anchors automotive and food lines across the region. Vendors now ship PLCs with native CIP-Security and TLS encryption, reducing gateway dependencies.

MES platforms are expanding at 7.6% CAGR as manufacturers seek lot-level genealogy and order-to-batch synchronisation. Industry 4.0 roll-outs nearly doubled connected devices to 17 billion globally in 2024, creating data sets that MES converts into actionable production KPIs. Automotive OEMs use MES to coordinate robotic paint, battery assembly, and final inspection, shortening launch cycles and connecting enterprise resource planning.

The North American Industrial Control Systems Market Report is Segmented by Component (Hardware, Software, Services), Type of System (Supervisory Control & Data Acquisition, Distributed Control Systems, and More), Communication Protocol (Fieldbus, Industrial Ethernet, Wireless), Deployment Mode (On-Premise, Cloud, Hybrid), End-User Industry, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Johnson Controls International plc

- Mitsubishi Electric Corp.

- Omron Corp.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Yokogawa Electric Corp.

- Bosch Rexroth AG

- Phoenix Contact GmbH

- Advantech Co. Ltd.

- Eaton Corp. plc

- BandR Industrial Automation GmbH

- Beckhoff Automation GmbH

- FANUC Corp.

- Delta Electronics Inc.

- Hitachi Ltd.

- IDEC Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Brown-Field Modernization across U.S. Automotive Plants

- 4.2.2 Growing Cyber-physical Safety Standards (ISA/IEC 62443) Adoption

- 4.2.3 U.S. CHIPS Act-fuelled Semiconductor Capacity Build-out

- 4.2.4 Canada's Net-Zero Grid Mandate Driving Utility Automation

- 4.2.5 Rising Mid-stream LNG Investments in Gulf Coast

- 4.2.6 Edge-enabled Predictive Maintenance Roll-outs in Mexican OEMs

- 4.3 Market Restraints

- 4.3.1 Legacy Brown-field Systems with Proprietary Protocol Lock-in

- 4.3.2 Capital-intensive Retrofit Costs for OSHA Functional-Safety

- 4.3.3 Shortage of ISA-Certified OT-Cybersecurity Workforce

- 4.3.4 North American Supply-Chain Exposure to Rare-earth Magnet Imports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Type of System

- 5.2.1 SCADA (Supervisory Control and Data Acquisition)

- 5.2.2 DCS (Distributed Control Systems)

- 5.2.3 PLC (Programmable Logic Controller)

- 5.2.4 MES (Manufacturing Execution Systems)

- 5.2.5 PLM (Product Lifecycle Management)

- 5.2.6 ERP (Enterprise Resource Planning)

- 5.2.7 HMI (Human Machine Interface)

- 5.2.8 Others (OTS, Machine-safety)

- 5.3 By Communication Protocol

- 5.3.1 Fieldbus

- 5.3.2 Industrial Ethernet

- 5.3.3 Wireless

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By End-user Industry

- 5.5.1 Automotive

- 5.5.2 Chemical and Petrochemical

- 5.5.3 Utilities (Power and Water)

- 5.5.4 Pharmaceutical

- 5.5.5 Food and Beverage

- 5.5.6 Oil and Gas

- 5.5.7 Mining and Metals

- 5.5.8 Pulp and Paper

- 5.5.9 Others

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Co.

- 6.4.3 General Electric Co.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Johnson Controls International plc

- 6.4.6 Mitsubishi Electric Corp.

- 6.4.7 Omron Corp.

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 Yokogawa Electric Corp.

- 6.4.12 Bosch Rexroth AG

- 6.4.13 Phoenix Contact GmbH

- 6.4.14 Advantech Co. Ltd.

- 6.4.15 Eaton Corp. plc

- 6.4.16 BandR Industrial Automation GmbH

- 6.4.17 Beckhoff Automation GmbH

- 6.4.18 FANUC Corp.

- 6.4.19 Delta Electronics Inc.

- 6.4.20 Hitachi Ltd.

- 6.4.21 IDEC Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

PLC配件市场:产品类型、安装类型、电压和功率额定值、应用和产业划分-全球预测,2026-2032年

PLC配件市场:产品类型、安装类型、电压和功率额定值、应用和产业划分-全球预测,2026-2032年 工业共生平台市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分工业自动化雷射雷达市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分

工业共生平台市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户及解决方案划分工业自动化雷射雷达市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分 2026年全球工业控制市场报告PLC控制器市场按类型、组件、产业、通讯协定、应用和程式语言划分,全球预测,2026-2032年基于云端的自动化控制系统市场:按最终用户、组件、系统类型、技术、公司规模和产品/服务划分,全球预测,2026-2032年

2026年全球工业控制市场报告PLC控制器市场按类型、组件、产业、通讯协定、应用和程式语言划分,全球预测,2026-2032年基于云端的自动化控制系统市场:按最终用户、组件、系统类型、技术、公司规模和产品/服务划分,全球预测,2026-2032年 工业製程製造控制市场:依技术、硬体及软体、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

工业製程製造控制市场:依技术、硬体及软体、应用、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 工业控制系统市场规模、份额和成长分析(按组件、技术、最终用途和地区划分)-2026年至2033年产业预测

工业控制系统市场规模、份额和成长分析(按组件、技术、最终用途和地区划分)-2026年至2033年产业预测 工业计数器市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测

工业计数器市场规模、份额和成长分析(按类型、应用和地区划分)-2026-2033年产业预测 云端基础工业控制系统市场预测至2032年:按组件、控制系统类型、部署模式、最终用户和地区分類的全球分析

云端基础工业控制系统市场预测至2032年:按组件、控制系统类型、部署模式、最终用户和地区分類的全球分析