|

市场调查报告书

商品编码

1851316

北美:人机介面市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)North America Human Machine Interface - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

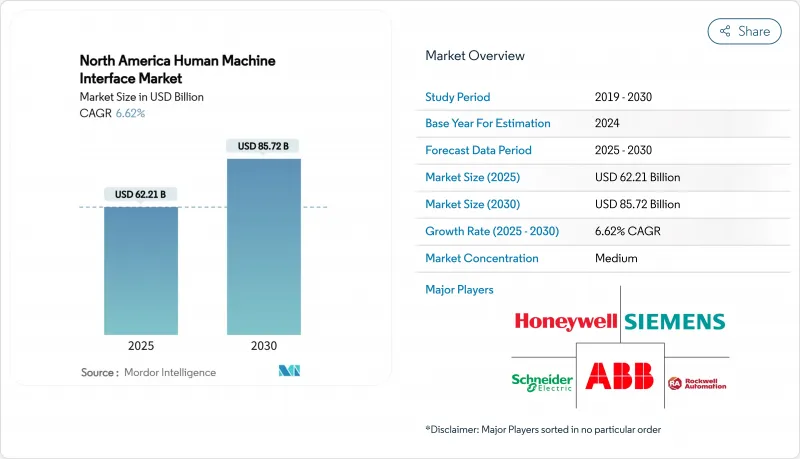

北美:预计到 2025 年,人机介面市场规模将达到 622.1 亿美元,到 2030 年将达到 857.2 亿美元,年复合成长率为 6.62%。

该地区向工业4.0转型、私有5G网路部署以及更严格的OSHA-NIST网实整合法规的推进,正在推动市场需求,并迫使製造商用安全、以数据为中心的系统取代传统的操作面板。现代工厂期望人机介面(HMI)不仅能够传达机器状态,还能将即时生产资料流传输到云端进行分析,这项期望正在改变离散製造和流程製造业的筹资策略。儘管半导体供不应求和OT-IT整合人才匮乏构成了短期限制因素,但包括电动车电池超级工厂在内的新产能扩张仍在持续支撑着未来多年的计划储备。因此,能够整合硬体、软体和安全功能的供应商正在北美人机介面市场获得竞争优势。

北美:人机介面市场趋势与洞察

美国离散製造业中工业4.0的日益普及推动了对互联机器介面的需求

如今,汽车、电子和包装产品线的工厂经理们正在推行单一资料架构策略,将PLC逻辑、MES事务和品质分析整合到一个统一的人机介面(HMI)平台下。西门子的Industrial Copilot荣获2025年赫尔墨斯奖,它融合了生成式人工智慧技术,在缩短工程时间的同时,提高了程式码的健壮性。福特在其路易斯维尔组装厂整合了软体定义的SIMATIC自动化工作站,使生产单元的重新配置时间从数天缩短至数小时。一家中型契约製造製造商的类似部署标誌着人机介面结构正在转变,从固定功能面板转向可扩展的、以软体为中心的HMI,从而支援预测性维护和能源优化。这些升级直接扩大了北美人机介面市场的潜在用户群。

美国职业安全与健康管理局 (OSHA) 和美国国家标准与技术研究院 (NIST) 的网实整合物理合规性要求推动人机介面 (HMI) 升级

监管机构现在将不安全的HMI视为安全隐患。美国职业安全与健康管理局(OSHA)引用了NIST SP 800-82标准,并敦促製药和化学企业加固远端网路基地台并实施多因素身份验证。美国网路安全与基础设施安全局(CISA)在2024年的建议中指出,广泛部署的操作员工作站存在SQL注入漏洞,促使企业弃用不再受支援的版本。违规的成本超过了现代化改造预算,资金正被重新分配到加密通讯协定和基于角色的存取控制方面。为符合IEC 62443标准的面板提供预认证的供应商报告称,其在北美的人机介面市场实现了高于平均水平的成长。

传统人机介面通讯协定存在安全漏洞

CISA 的 2025 年漏洞目录重点指出了 Modbus-TCP 和 DNP3 协议的漏洞,这些漏洞可能允许在未打补丁的设备上执行远端程式码,从而加强了对工厂运营技术 (OT) 风险的板级审查。由于许多北美工厂仍依赖「空气间隙」的假象,新揭露的漏洞正在加速老旧配电盘的更换计画。然而,棕地线路的复杂性以及需要分阶段停机维护,延缓了全面过渡的进程。

细分市场分析

可程式逻辑控制器(PLC)市场规模将在2024年达到174.2亿美元,占总支出的28%。製造执行系统(MES)平台虽然规模较小,但到2030年将以每年9.5%的速度成长,反映出市场正朝着闭合迴路品质控制和即时成本会计的方向发展。供应商正在将运动分析、安全分析和边缘分析整合到新一代PLC中,缩小机柜尺寸,同时扩大企业云端的资料吞吐量。电子产业的早期采用者在将PLC标籤整合到MES仪錶板后,废品率降低了12%以上。儘管监控与资料收集系统(SCADA)和分散式控制系统(DCS)解决方案在流程工业中仍然占据主导地位,但随着财务长们优先考虑将资本支出转化为营运支出的订阅模式,云端託管的人机介面(HMI)软体正在超越永久授权模式。这种技术融合使它们能够互通而不相互竞食,从而在北美人机介面市场的各个层面维持持续成长。

如今,越来越多的计划将产品生命週期管理 (PLM) 资料与操作介面连接起来,以便工程变更能够立即反映在生产车间。一家汽车原始设备製造商 (OEM) 表示,当 CAD 版本自动更新到人机介面 (HMI) 工作指令时,工程变更的部署时间缩短了两天。基于 TSN 的开放原始码OPC UA 协议已成为一种流行的通讯协定,可将客製化中间件的成本降低 18%。总而言之,这些进展表明,製造商不再仅仅根据面板数量来评判北美人机介面市场,而是关注其将数据转化为可执行的财务成果的能力。

触控萤幕面板凭藉其成熟的IP65防护等级和通用备件生态系统,到2024年将占据北美人机介面市场26%的份额。然而,随着5G私有网路的成熟,行动和穿戴式介面预计将以9.1%的复合年增长率成长。航太组装厂的早期部署表明,透过使用支援AR功能的智慧眼镜(该眼镜可将扭力规格和公差迭加显示),检验员可以核准速度。工业用电脑现在配备了NVIDIA GPU,使视觉应用程式可以直接在设备上运行,无需单独的伺服器。小键盘人机介面在易爆环境和需要戴手套操作的场合仍然适用,触觉确认功能可以防止误触。语音控制的人机介面正在逐步应用于金属成型生产线,因为背景噪音仍然是一个障碍。

中央控制面板管理安全连锁装置,操作人员则携带平板电脑进行非关键性调整。由此形成的介面网路透过冗余机制提高了运作。如果某个控制面板发生故障,可以透过经过认证的行动装置来恢復线路。此配置扩大了采购范围,提升了各设备系列网路安全认证的认可度,并增强了北美人机介面市场中各供应商之间的差异化优势。

北美:人机介面市场按技术(可程式逻辑控制器、SCADA 等)、组件(通讯模组、控制设备等)、介面(触控萤幕、小键盘等)、终端用户产业(汽车、石油天然气等)和国家(美国、加拿大)进行细分。市场规模和预测以美元计价。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国离散製造业中工业4.0的日益普及推动了对互联机器介面的需求

- 美国职业安全与网实整合合规性要求推动人机介面 (HMI) 升级

- 美国墨西哥湾沿岸和亚伯达油砂老旧製程装置的维修

- 部署专用 5G 网络,以实现智慧工厂中的即时人机交互

- 多语言劳动力需求加速了双语人机介面面板的普及

- 北美电动车电池超级工厂的扩张需要先进的介面解决方案

- 市场限制

- 传统人机介面通讯协定的漏洞引发网路安全担忧

- OT-IT整合人才短缺问题日益严重,部署计画延期。

- 半导体供应中断导致控制器和显示器前置作业时间延长

- FDA高昂的检验费用阻碍了製药厂经常进行升级改造。

- 价值/供应链分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析(智慧製造介面的资本投资趋势)

第五章 市场规模与成长预测

- 透过技术

- 可程式逻辑控制器(PLC)

- 监控与数据采集(SCADA)

- 企业资源规划(ERP)

- 分散式控制系统(DCS)

- 人机介面(HMI)软体

- 产品生命週期管理(PLM)

- 製造执行系统(MES)

- 其他技术

- 按介面类型

- 触控萤幕操作面板

- 工业用电脑(面板和机壳)

- 小键盘/功能键人机介面

- 行动和穿戴式人机介面

- 支援语音和扩增实境的人机交互

- 按组件

- 通讯部门

- 控制设备

- 机器视觉系统

- 机器人

- 感应器

- 其他部分

- 按最终用户行业划分

- 车

- 石油和天然气

- 化工/石油化工

- 製药

- 饮食

- 金属和采矿

- 其他行业

- 按国家/地区

- 美国

- 加拿大

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- Emerson Electric Company

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Incorporated

- Yokogawa Electric Corporation

- Omron Corporation

- Advantech Co., Ltd.

- Beijer Electronics Group

- Red Lion Controls(Spectris plc)

- Maple Systems Inc.

- BandR Industrial Automation GmbH(ABB Group)

- Phoenix Contact GmbH and Co. KG

- Keyence Corporation

- Parker Hannifin Corporation

- Eaton Corporation plc

- Lenze SE

第七章 市场机会与未来展望

The North America human machine interface market reached USD 62.21 billion in 2025 and is forecast to touch USD 85.72 billion by 2030, advancing at a 6.62% CAGR.

Demand scales with the region's push toward Industry 4.0, private 5G roll-outs, and stricter OSHA-NIST cyber-physical rules that force manufacturers to replace legacy operator panels with secure, data-centric systems. Modern plants now expect an HMI to stream real-time production data into cloud analytics rather than simply relay machine status, and this expectation is changing procurement strategies across discrete and process industries. Semiconductor shortages and the lack of OT-IT integration talent form a near-term drag, yet fresh capacity build-outs-especially EV battery gigafactories-continue to anchor multi-year project pipelines. Consequently, vendors that blend hardware, software, and cybersecurity functions occupy a premium competitive position in the North America human machine interface market.

North America Human Machine Interface Market Trends and Insights

Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces

Plant managers in automotive, electronics, and packaged-goods lines now pursue single data fabric strategies that unify PLC logic, MES transactions, and quality analytics under one HMI umbrella. Siemens' Industrial Copilot, honored with the 2025 Hermes Award, embeds generative AI that cuts engineering hours while boosting code robustness. Ford integrated the software-defined SIMATIC Automation Workstation across Louisville assembly to reconfigure production cells within hours, not days. Similar deployments across mid-sized contract manufacturers indicate a structural shift from fixed-function panels to scalable, software-centric HMIs that support predictive maintenance and energy optimization. These upgrades directly enlarge the addressable base of the North America human machine interface market.

OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades

Regulators now treat unsecured HMIs as safety risks. OSHA citations reference NIST SP 800-82 controls, compelling pharmaceutical and chemical operators to harden remote-access points and implement multi-factor authentication. CISA advisories in 2024 flagged SQL injection flaws in widely deployed operator stations, pushing firms to retire unsupported versions. The cost of non-compliance dwarfs modernization budgets, shunting capital toward encrypted protocols and role-based access. Vendors that pre-certify panels to IEC 62443 standards report above-market growth across the North America human machine interface market.

Persistent vulnerabilities in legacy HMI communication protocols

CISA's 2025 catalog highlights modbus-TCP and DNP3 weaknesses that permit remote code execution on unpatched terminals, intensifying board-level scrutiny of plant OT risk. Because many North American facilities still rely on air-gap illusions, each newly disclosed exploit accelerates plans to replace aging panels. However, complexity of brown-field wiring, combined with the need to stage line outages, slows full migration.

Other drivers and restraints analyzed in the detailed report include:

- Retrofitting aging process plants in U.S. Gulf Coast and Alberta oil sands

- Deployment of private 5G networks enabling real-time HMI in smart factories

- Acute shortage of OT-IT integration talent inflating implementation timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The North America human machine interface market size for Programmable Logic Controllers stood at USD 17.42 billion in 2024 and retained a 28% share of total spending. MES platforms, although smaller, will grow 9.5% annually to 2030, reflecting a pivot toward closed-loop quality and real-time costing. Vendors integrate motion, safety, and edge analytics into new PLC generations, compressing cabinet footprint while expanding data throughput to enterprise clouds. Early adopters in electronics witness scrap reductions above 12% after unifying PLC tags with MES dashboards. While SCADA and DCS solutions maintain strongholds in process industries, cloud-hosted HMI software outsells perpetual licenses as CFOs prioritize subscription models that convert capex to opex. This technology convergence keeps technologies interoperating rather than cannibalizing, sustaining incremental growth in every layer of the North America human machine interface market.

A growing subset of projects now marries PLM data with operator interfaces so that engineering changes flow instantly to the shop floor. Automotive OEMs cite reductions of two days per engineering change roll-out when CAD revisions automatically populate HMI work instructions. Open-source OPC UA over TSN gains traction as common protocol, trimming custom middleware costs by 18%. Collectively, these advances underline how manufacturers judge the North America human machine interface market not simply on panel counts but on the capacity to convert data into actionable financial outcomes.

Touch-screen panels preserved 26% of the North America human machine interface market in 2024 due to their proven IP-65 housings and universal spare-parts ecosystems. Yet mobile and wearable interfaces will compound 9.1% per year as private 5G matures. Early roll-outs at aerospace assembly plants indicate 30% faster first-piece approvals when inspectors use AR-enabled smart glasses that overlay torque specs and tolerances. Industrial PCs now ship with NVIDIA GPUs, letting vision apps run directly on-device and eliminating separate servers. Keypad models stay relevant in explosive or gloved-hand zones, where tactile affirmations prevent mis-clicks. Voice-controlled HMIs inch forward, although background noise remains a barrier in metal-forming lines.

Hybrid deployments become common: a central panel governs safety interlocks while operators carry tablets for non-critical adjustments. The resulting interface mesh boosts uptime through redundancy; if a panel fails, the line can still be jogged from a certified mobile unit. Such configurations widen procurement scope and elevate the profile of cybersecurity certifications that span device families, reinforcing vendor differentiation across the North America human machine interface market.

The North America Human Machine Interface Market is Segmented by Technology (Programmable Logic Controller, SCADA and More), Component (Communication Segment, Control Device and More), Interface (Touchscreen, Keypad and More), End-User Industry (Automotive, Oil and Gas and More), and Country (United States, Canada). Market Size and Forecasts are Provided in USD.

List of Companies Covered in this Report:

- ABB Ltd.

- Emerson Electric Company

- Fanuc Corporation

- General Electric Company

- Honeywell International Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Incorporated

- Yokogawa Electric Corporation

- Omron Corporation

- Advantech Co., Ltd.

- Beijer Electronics Group

- Red Lion Controls (Spectris plc)

- Maple Systems Inc.

- BandR Industrial Automation GmbH (ABB Group)

- Phoenix Contact GmbH and Co. KG

- Keyence Corporation

- Parker Hannifin Corporation

- Eaton Corporation plc

- Lenze SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Industry 4.0 adoption in U.S. discrete manufacturing driving demand for connected machine interfaces

- 4.2.2 OSHA and NIST cyber-physical compliance mandates boosting HMI upgrades

- 4.2.3 Retrofitting ageing process plants in U.S. Gulf Coast and Alberta oil sands

- 4.2.4 Deployment of private 5G networks enabling real-time HMI in smart factories

- 4.2.5 Multilingual workforce requirements accelerating bilingual HMI panel adoption

- 4.2.6 Expansion of North American EV battery gigafactories requiring advanced interface solutions

- 4.3 Market Restraints

- 4.3.1 Persistent vulnerabilities in legacy HMI communication protocols raising cybersecurity concerns

- 4.3.2 Acute shortage of OT-IT integration talent inflating implementation timelines

- 4.3.3 Semiconductor supply disruptions causing controller and display lead-time spikes

- 4.3.4 Stringent FDA re-validation costs discouraging frequent upgrades in pharma plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis (Capital Expenditure Trends in Smart Manufacturing Interfaces)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Programmable Logic Controller (PLC)

- 5.1.2 Supervisory Control and Data Acquisition (SCADA)

- 5.1.3 Enterprise Resource Planning (ERP)

- 5.1.4 Distributed Control System (DCS)

- 5.1.5 Human Machine Interface (HMI) Software

- 5.1.6 Product Lifecycle Management (PLM)

- 5.1.7 Manufacturing Execution System (MES)

- 5.1.8 Other Technologies

- 5.2 By Interface Type

- 5.2.1 Touch-Screen Operator Panels

- 5.2.2 Industrial PCs (Panel and Box)

- 5.2.3 Keypad / Function-Key HMIs

- 5.2.4 Mobile and Wearable HMIs

- 5.2.5 Voice- and AR-Enabled HMIs

- 5.3 By Component

- 5.3.1 Communication Segment

- 5.3.2 Control Device

- 5.3.3 Machine Vision Systems

- 5.3.4 Robotics

- 5.3.5 Sensors

- 5.3.6 Other Components

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Oil and Gas

- 5.4.3 Chemical and Petrochemical

- 5.4.4 Pharmaceutical

- 5.4.5 Food and Beverage

- 5.4.6 Metals and Mining

- 5.4.7 Other Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Company

- 6.4.3 Fanuc Corporation

- 6.4.4 General Electric Company

- 6.4.5 Honeywell International Inc.

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 Yokogawa Electric Corporation

- 6.4.13 Omron Corporation

- 6.4.14 Advantech Co., Ltd.

- 6.4.15 Beijer Electronics Group

- 6.4.16 Red Lion Controls (Spectris plc)

- 6.4.17 Maple Systems Inc.

- 6.4.18 BandR Industrial Automation GmbH (ABB Group)

- 6.4.19 Phoenix Contact GmbH and Co. KG

- 6.4.20 Keyence Corporation

- 6.4.21 Parker Hannifin Corporation

- 6.4.22 Eaton Corporation plc

- 6.4.23 Lenze SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

人机介面市场:依介面类型、技术、最终用户和应用划分-2026-2032年全球市场预测

人机介面市场:依介面类型、技术、最终用户和应用划分-2026-2032年全球市场预测 2026年全球人机互动市场报告2026年全球人机介面市场报告

2026年全球人机互动市场报告2026年全球人机介面市场报告 人机介面市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、最终用户及功能划分

人机介面市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、最终用户及功能划分 全球人机介面市场规模、份额、趋势和成长分析报告(2026-2034)

全球人机介面市场规模、份额、趋势和成长分析报告(2026-2034) 人机介面市场-全球产业规模、份额、趋势、机会与预测:产品、部署模式、配置、产业垂直领域、地区和竞争格局(2021-2031年)人机介面软体市场-全球产业规模、份额、趋势、机会、预测:按部署方式、产品、配置、产业、地区和竞争对手划分,2021-2031年智慧驾驶座人机互动系统市场(按触控互动、语音互动、手势互动、触觉回馈、抬头显示器互动和眼动追踪互动)——全球预测,2026-2032年驾驶座显示器人机介面(HMI)市场:2025-2030 年预测

人机介面市场-全球产业规模、份额、趋势、机会与预测:产品、部署模式、配置、产业垂直领域、地区和竞争格局(2021-2031年)人机介面软体市场-全球产业规模、份额、趋势、机会、预测:按部署方式、产品、配置、产业、地区和竞争对手划分,2021-2031年智慧驾驶座人机互动系统市场(按触控互动、语音互动、手势互动、触觉回馈、抬头显示器互动和眼动追踪互动)——全球预测,2026-2032年驾驶座显示器人机介面(HMI)市场:2025-2030 年预测 人机协作:全球市场占有率及排名、总收入及需求预测(2025-2031 年)

人机协作:全球市场占有率及排名、总收入及需求预测(2025-2031 年)