|

市场调查报告书

商品编码

1851344

欧洲行动云:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Europe Mobile Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

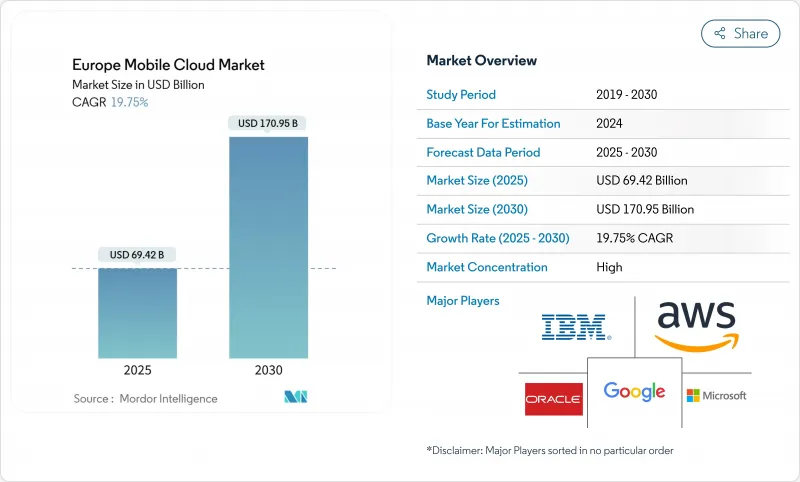

欧洲行动云市场预计到 2025 年将达到 694.2 亿美元,到 2030 年将扩大到 1,709.5 亿美元,复合年增长率为 19.75%。

主权云端框架的日益普及、5G独立组网(SA)覆盖范围的扩大以及企业对低延迟移动工作负载日益增长的关注,都推动了这一发展趋势。此外,5G SA网路已实现低于10毫秒的往返延迟,从而催生了对即时工业、游戏和金融科技等应用场景的新需求。通讯业者与云端平台的合作,例如德国电信与NVIDIA合作的工业AI云平台,显示通讯业者正在转型为AI工作负载的基础设施供应商。同时,监管机构对超大规模云端服务商市场支配力的审查,促使其进行价格结构调整,包括取消出口费用,从而降低了云端平台切换门槛,并促进了多重云端策略的发展。

欧洲移动云市场趋势与洞察

欧盟27国主权云区的发展

欧盟委员会的 EuroStack 计画旨在 2030 年部署 10,000 个分散式边缘云端节点,创建符合严格资料居住规定的本地处理点。 Orange 和 Capgemini 于 2024 年推出的 Bleu 平台,旨在根据 SecNumCloud 规则提供微软技术,这表明合规优先的服务能够吸引敏感工作负载。即将推出的欧盟云端服务计画将根据主权和安全标准对服务提供者进行认证,加速先前託管在欧盟境外的敏感产业资料的回流。同时,欧盟资料法要求供应商在 2027 年 1 月前取消转换费用,从而削弱锁定效应,并奖励竞争性生态系统的发展。随着公共机构调整采购规则,欧洲业者预计与受监管产业相关的云端需求将显着成长。

增强型 5G SA 部署可降低行动云端延迟

全球已有超过60家营运商,包括德国、英国、义大利和西班牙的营运商,推出了商用5G SA网路。网路切片技术能够预先定义延迟和频宽等级,以满足行动云端应用的需求,并透过加值服务层级直接实现获利。德国电信的5G+游戏试点计画已成功实现了云端游戏流量端到端延迟低于10毫秒。 GSMA预测,到2030年,5G将为欧洲经济贡献1,640亿欧元,其中大部分将依赖SA部署。核心网路升级,例如O2 Telefónica的云端原生双模核心网,进一步减少了维护停机时间,并支援持续的功能发布。

对超大规模资料中心营运商市场力量的批评日益增多(CMA 和 EU DMA)

英国竞争与市场管理局 (CMA) 发现,AWS 和微软各自控制英国国内 30% 至 40% 的云端支出,并提案了战略市场地位义务,这可能迫使它们调整互通性和价格。竞争改革每年可为英国企业节省 4.3 亿英镑。随着布鲁塞尔《数位市场法案》的实施,「安全隔离网闸」平台将受到额外的合规约束,例如将软体授权与云端使用量挂钩的限制。在最终裁决公布之前,AWS 和微软都已调整了自身行为,提前取消了客户更换供应商的退出费用。虽然这些让步有利于客户,但可能会挤压供应商的利润空间,并减缓近期的投资步伐。

细分市场分析

到2024年,企业工作负载将占欧洲行动云端市场收入的67%,因为企业优先考虑效能保证和自主合规性。像BBVA这样的金融机构指出,在切换到云端原生资料平台后,分析时间缩短了94%。这些可衡量的成果证明了高额合约价格的合理性,并刺激了持续的基础设施投资。消费者采用率虽然目前规模较小,但正以19.90%的复合年增长率快速成长,主要得益于云端游戏订阅和行动娱乐方案的推动。德国电信(Telefonica)已将其100万5G用户迁移到AWS核心云,从而融合了企业和消费者价值链,并证明差异化的网路服务能够同时实现这两个领域的盈利。儘管企业仍然是欧洲行动云端市场的基础,但消费者的成长使收入来源更加多元化,并为企业的预算週期提供了缓衝。

消费者主导的成长日益依赖位于人口中心附近的边缘运算节点,从而降低图形密集型游戏和视讯串流的抖动。网路营运商受益于批发流量的成长,超大规模资料中心将内容快取分发到大都会圈的各个存取点。同时,企业买家正在扩大其多重云端布局以降低厂商锁定风险,沃达丰则透过维持其三大供应商之间的「商业性张力」来实现成本节约。先进的财务营运(FinOps)仪表板按业务部门追踪使用情况,并确保所有工作负载都在最佳性价比范围内运作。这种双管齐下的演进使欧洲行动云端产业保持了强大的韧性。

预计到2024年,游戏业务将占总营收的32%,复合年增长率(CAGR)为22.60%。德国电信的5G+游戏服务展示了网路切片如何确保在行动宽频速度下实现稳定的影格速率。金融和商业应用,尤其是那些透过安全、低延迟网路传输的即时风险分析应用,其价值位居第二。资本市场核心企业对演算法交易的确定性延迟有着迫切的需求,这推动了对边缘最佳化区域的需求。

随着远距学习平台和诊断人工智慧工作负载迁移到云端,教育和医疗保健应用在云端领域的份额持续成长。监管机构允许敏感的医疗资料储存在主权云端区域中,使服务提供者能够在不违反隐私法的情况下部署人工智慧驱动的影像处理。娱乐平台也像游戏一样利用边缘运算资源,实现自我调整比特率影片的流畅播放。这些多样化的应用场景正在推动欧洲行动云市场的成长,确保不断增长的云端容量能够找到买家。

欧洲行动云市场报告按使用者(企业和消费者)、应用程式(游戏、娱乐、教育、其他)、服务模式(SaaS、PaaS、其他)、部署模式(公共云端、私有云端、其他)和国家进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在欧盟27国范围内发展主权云圈

- 增强型 5G SA 部署可降低行动云端延迟

- 企业用于管理多重云端成本的FinOps工具的激增

- 边缘云端伙伴关係实现网路 API通讯业者

- 人工智慧辅助的行动应用开发和营运加速了云端迁移速度。

- 德国和北欧的绿色资料中心税收优惠政策

- 市场限制

- 加强对超大规模资料中心营运商市场力量的审查(CMA 和 EU DMA)

- 跨国资料传输的合规成本(Schrems II、GDPR)

- 能源价格波动对资料中心营运成本带来压力。

- 认证云端安全专业人员短缺

- 价值链分析

- 监管环境

- 技术展望(5G SA、Edge、GenAI)

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争的激烈程度

第五章 市场规模与成长预测

- 使用者

- 企业

- 消费者

- 透过使用

- 游戏

- 金融与商业

- 娱乐

- 教育

- 卫生保健

- 旅行

- 按服务模式

- 软体即服务(SaaS)

- 平台即服务 (PaaS)

- 基础设施即服务 (IaaS)

- 按配置模型

- 公共云端

- 私有云端

- 混合云端

- 按国家/地区

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- IBM Corporation

- SAP SE

- Deutsche Telekom(T-Systems)

- Vodafone Group

- Orange Business Services

- Telefonica Tech

- Oracle Corporation

- Salesforce Inc.

- Akamai Technologies

- OVHcloud

- Rackspace Technology

- Cloudflare Inc.

- Alibaba Cloud

- Tencent Cloud

- Huawei Cloud

- Nokia Cloud and Network Services

- Kyndryl Holdings

第七章 市场机会与未来展望

Europe mobile cloud market value reached USD 69.42 billion in 2025 and is forecast to rise to USD 170.95 billion by 2030, registering a 19.75% CAGR.

Rising adoption of sovereign-cloud frameworks, expanding 5G standalone (SA) coverage, and intensifying enterprise focus on low-latency mobile workloads underpin this trajectory. National data-sovereignty mandates are forcing workload repatriation from extra-regional hyperscale zones to EU-hosted platforms, while 5G SA networks already deliver sub-10 millisecond round-trip latency, opening fresh demand for real-time industrial, gaming and fintech use cases. Telco-cloud alliances-such as Deutsche Telekom's NVIDIA-powered industrial AI cloud-illustrate how telecom operators are transforming into infrastructure suppliers for AI workloads. At the same time, regulatory scrutiny of hyperscaler market power is prompting price realignments, including the removal of egress fees, which lowers switching barriers and encourages multi-cloud strategies.

Europe Mobile Cloud Market Trends and Insights

Development of Sovereign-Cloud Zones Across EU-27

The European Commission's EuroStack programme targets 10,000 distributed edge-cloud nodes by 2030, creating local processing points that satisfy strict data-residency statutes. Orange and Capgemini's Bleu platform was launched in 2024 to offer Microsoft technology under SecNumCloud rules, proving that compliance-first offerings can attract sensitive workloads. The forthcoming EU Cloud Services Scheme will certify providers against sovereignty and security standards, accelerating repatriation of critical-sector data previously hosted outside the bloc. Simultaneously, the EU Data Act obliges vendors to abolish switching fees by January 2027, undermining lock-in economics and incentivizing a competitive ecosystem. As public agencies adapt procurement rules, European operators expect a sizeable uplift in cloud demand tied to regulated industries.

Intensifying 5G SA Roll-out Lowers Mobile-Cloud Latency

More than 60 operators worldwide have launched commercial 5G SA networks, including installations across Germany, the UK, Italy, and Spain. Network slicing allows predefined latency and bandwidth classes that match mobile-cloud application requirements, directly monetised through premium service tiers. Deutsche Telekom's 5G+ Gaming pilot has already proven sub-10 millisecond end-to-end latency for cloud gaming traffic. The GSMA projects EUR 164 billion in European economic value from 5G by 2030, most of which depends on SA deployment. Core-network upgrades, such as O2 Telefonica's cloud-native dual-mode core, further cut maintenance downtime and enable continuous feature releases.

Rising Scrutiny of Hyperscaler Market Power (CMA and EU DMA)

The UK Competition and Markets Authority found AWS and Microsoft each control 30-40 % of domestic cloud spend, proposing Strategic Market Status obligations that could force interoperability and pricing remedies. The watchdog estimates competitive reforms might save UK businesses GBP 430 million annually. Parallel Digital Markets Act enforcement in Brussels adds further compliance layers for "gatekeeper" platforms, including limits on tying software licences to cloud consumption. Both AWS and Microsoft have pre-emptively eliminated egress fees for customers switching providers, demonstrating behavioural adjustments ahead of final rulings. While such concessions help clients, they compress provider margins and may reduce near-term investment pace.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Enterprise FinOps Tooling for Multi-Cloud Cost Control

- Telco Edge-Cloud Partnerships Monetising Network APIs

- Cross-Border Data-Transfer Compliance Costs (Schrems II and GDPR)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Enterprise workloads produced 67% of 2024 Europe mobile cloud market revenue as corporates prioritised performance guarantees and sovereignty compliance. Financial institutions such as BBVA highlighted time-to-insight gains-94% faster analytics-after pivoting to cloud-native data platforms. These measurable outcomes justify premium contract values and spur continued infrastructure investment. Consumer adoption, while smaller, is expanding briskly at a 19.90% CAGR due to cloud gaming subscriptions and mobile entertainment bundles. Telefonica Germany moved 1 million 5G users onto AWS core cloud, blending enterprise and consumer value chains, proving that differentiated network services can monetise both segments. Although enterprises remain the bedrock of the Europe mobile cloud market, consumer growth diversifies revenue and cushions against corporate budget cycles.

The consumer-driven upswing is increasingly tied to edge-compute nodes situated near population centres, reducing jitter for graphics-intensive titles and video streaming. Network operators benefit from incremental wholesale traffic, while hyperscalers distribute content caches across metropolitan points of presence. Meanwhile, enterprise buyers widen multi-cloud footprints to mitigate lock-in, with Vodafone registering cost savings by maintaining "commercial tension" across three large providers. Advanced FinOps dashboards track usage by business unit, ensuring every workload runs in the optimal cost-performance zone. This dual-track evolution keeps the Europe mobile cloud industry resilient

Gaming secured a 32% slice of 2024 revenue and is projected to expand at 22.60% CAGR, propelled by pay-as-you-go cloud gaming services that remove local hardware constraints. Deutsche Telekom's 5G+ Gaming offer demonstrates how network slicing guarantees frame-rate consistency at mobile broadband speeds. Finance and business applications rank second in value, powered by real-time risk analytics delivered over secure, low-latency pipes. Enterprises in capital-markets hubs depend on deterministic latency for algorithmic trading, steering demand toward edge-optimised zones.

Education and healthcare applications continue gaining share as remote-learning platforms and diagnostic AI workloads migrate to cloud. Regulators permit sensitive health data to reside in sovereign cloud zones, enabling providers to roll out AI-powered imaging without contravening privacy law. Entertainment platforms capitalise on the same edge footprints that gaming uses, streaming adaptive-bitrate video without buffering. Collectively, these diverse use cases reinforce growth across the Europe mobile cloud market, ensuring that incremental capacity finds ready buyers.

The Europe Mobile Cloud Market Report is Segmented by User (Enterprise and Consumer), Application (Gaming, Entertainment, Education, and More), Service Model (Software-As-A-Service (SaaS), Platform-As-A-Service (PaaS), and More), Deployment Model (Public Cloud, Private Cloud, and More), and Country.

List of Companies Covered in this Report:

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- IBM Corporation

- SAP SE

- Deutsche Telekom (T-Systems)

- Vodafone Group

- Orange Business Services

- Telefonica Tech

- Oracle Corporation

- Salesforce Inc.

- Akamai Technologies

- OVHcloud

- Rackspace Technology

- Cloudflare Inc.

- Alibaba Cloud

- Tencent Cloud

- Huawei Cloud

- Nokia Cloud and Network Services

- Kyndryl Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Development of sovereign-cloud zones across EU-27

- 4.2.2 Intensifying 5G SA roll-out lowers mobile-cloud latency

- 4.2.3 Surge in enterprise FinOps tooling for multi-cloud cost control

- 4.2.4 Telco edge-cloud partnerships monetising network APIs

- 4.2.5 AI-assisted mobile app dev-ops shrinks time-to-cloud

- 4.2.6 Green-datacentre tax incentives in Germany and Nordics

- 4.3 Market Restraints

- 4.3.1 Rising scrutiny of hyperscaler market power (CMA and EU DMA)

- 4.3.2 Cross-border data-transfer compliance costs (Schrems II, GDPR)

- 4.3.3 Energy-price volatility squeezing datacentre OPEX

- 4.3.4 Shortage of certified cloud-security professionals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (5G SA, Edge, GenAI)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By User

- 5.1.1 Enterprise

- 5.1.2 Consumer

- 5.2 By Application

- 5.2.1 Gaming

- 5.2.2 Finance and Business

- 5.2.3 Entertainment

- 5.2.4 Education

- 5.2.5 Healthcare

- 5.2.6 Travel

- 5.3 By Service Model

- 5.3.1 Software-as-a-Service (SaaS)

- 5.3.2 Platform-as-a-Service (PaaS)

- 5.3.3 Infrastructure-as-a-Service (IaaS)

- 5.4 By Deployment Model

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.4.3 Hybrid Cloud

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Microsoft Azure

- 6.4.3 Google Cloud

- 6.4.4 IBM Corporation

- 6.4.5 SAP SE

- 6.4.6 Deutsche Telekom (T-Systems)

- 6.4.7 Vodafone Group

- 6.4.8 Orange Business Services

- 6.4.9 Telefonica Tech

- 6.4.10 Oracle Corporation

- 6.4.11 Salesforce Inc.

- 6.4.12 Akamai Technologies

- 6.4.13 OVHcloud

- 6.4.14 Rackspace Technology

- 6.4.15 Cloudflare Inc.

- 6.4.16 Alibaba Cloud

- 6.4.17 Tencent Cloud

- 6.4.18 Huawei Cloud

- 6.4.19 Nokia Cloud and Network Services

- 6.4.20 Kyndryl Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment