|

市场调查报告书

商品编码

1851419

金融服务桌面虚拟化:市场占有率分析、产业趋势与成长预测(2025-2030 年)Financial Services Desktop Virtualization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

预计到 2025 年金融服务桌面虚拟化市场规模将达到 288 万美元,到 2030 年将达到 575 万美元,预测期内复合年增长率将达到 14.8%。

随着银行、保险公司和金融科技公司越来越重视符合零信任要求、GPU加速风险分析和严格资料居住规定的安全虚拟桌面环境,市场需求正在成长。一级金融机构正从资本支出模式转向按需付费模式,促使供应商将合规工具和高效能图形功能整合到其产品中。儘管亚太地区凭藉金融业的快速数位化和对云端准则的支持而占据主导地位,但北美仍然是最大的采用者,这得益于其成熟的交易和监管基础设施[CMCGLOBAL.COM.VN]。供应商竞争的核心在于如何透过云端编配在超低延迟交易员桌面和提升营运效率之间取得平衡。

全球金融服务桌面虚拟化市场趋势与洞察

一级银行云端迁移策略的普及程度

领先银行正基于混合云端蓝图重建其桌面环境,以提高系统弹性并降低整体拥有成本。敏感的交易平台仍保留在本地,而后勤部门桌面则迁移到云端订阅模式,从而能够为承包商、测试团队和灾害復原演练提供动态资源配置。因此,采购模式正从硬体更新周期转向与业务成果相符的营运支出合约。这种转变加速了云端原生安全控制的标准化,并促进了跨虚拟会话整合审核追踪功能。随着金融机构在 24 至 36 个月内分阶段推进迁移,能够将传统资料中心与多重云端编配连接起来的供应商的需求日益增长。

向零信任安全框架的转型正在加速。

金融机构现在坚持要求所有虚拟桌面连线都必须持续进行身份验证,并整合多因素身份验证 (MFA)、行为分析和基于会话的风险评分。交易员使用生物识别和位置控制登录,如果出现异常情况,资料存取将被阻止,合规团队可以即时审核击键层级的历史记录。这些功能将虚拟桌面基础架构 (VDI) 的选择标准从效能提升到原生零信任架构的契合度。因此,拥有网路安全和虚拟化综合专业知识的专业整合商正在收取更高的咨询费,平台蓝图也越来越多地纳入用于威胁情报来源的 API 介面。

与传统大型主机整合的复杂性

许多银行仍然使用几十年前的大型主机来处理高价值交易。将这些系统桥接到现代虚拟桌面基础架构 (VDI) 平台需要客製化中间件、冗余身分验证路径和延迟解决方案,导致部署週期长达 6-12 个月,预算增加两位数。对稀缺的 COBOL 专家和专有工具的依赖降低了供应商的议价能力,减缓了创新速度,与数位原民化同行相比,价值实现速度也更慢。

细分市场分析

2024年,託管虚拟桌面将维持47.1%的收入份额,而桌面即服务(DaaS)的复合年增长率将达到17.8%,持续削弱现有市场的主导地位。 DaaS凭藉其按使用量计费的模式,能够适应咨询、交易和合规部门常见的员工人数波动趋势,因此正在迅速发展。服务提供者将监管日誌记录和GPU选项捆绑在一起,使中型银行能够在不大幅增加资本支出的情况下获得企业级技术堆迭。託管共用桌面产品凭藉标准化应用程式占据了一定的市场,而远端桌面服务则为分店提供传统的Windows工作负载。

随着DaaS供应商预先整合零信任和灾难復原方案,金融服务桌面虚拟化市场受益匪浅,部署时间从数月缩短至数週。多租用户控制平面可自动执行修补程式和漏洞扫描,从而减轻审核压力。相较之下,对于那些保单禁止异地资料的机构而言,本地部署的HVD设施仍然具有吸引力,但其更新周期会推高整体成本。因此,前瞻性的买家倾向于采用混合采购模式,将核心交易桌面迁移到私有云端,同时将后台使用者迁移到公有DaaS平台。

至2024年,本地部署将占金融服务桌面虚拟化市场份额的58.4%,而云端执行个体在2030年之前将维持在16.2%。银行正在透过将敏感资料集隔离在本地,并将季节性或低风险工作负载卸载到超大规模资料中心来平衡其对资料主权的担忧。混合编配平台会根据延迟、合规性标籤和成本来调度桌面资源。

随着监管机构发布更清晰的加密、金钥管理和审核存取指南,降低风险感知,云端加速发展将进一步加快。保险公司透过在更靠近客户的云端进行理赔裁决来改善客户体验,同时将核心精算模型保留在私有环境中。由于保险公司不愿意被单一平台锁定,因此能够跨 AWS、Azure 和 GCP 实现统一保单执行的供应商正在赢得市场份额。

金融服务桌面虚拟化市场报告按桌面交付平台(託管虚拟桌面 (HVD)、託管共用桌面 (HSD) 等)、部署类型(本地部署、云端部署、混合部署)、组织规模(大型企业、中小企业)、最终用户(零售和商业银行、资本市场和交易等)以及地区对行业进行细分。

区域分析

预计到2024年,北美将以41.2%的市占率领跑,这主要得益于零信任架构的早期应用、交易中心的集中以及纽约、芝加哥和多伦多等地大规模GPU虚拟化试点计画的开展。金融机构正大力投资提升系统韧性,包括在大都会圈建构双活桌面对,以满足联邦政府关于业务永续营运的指导方针。亚秒级容错移转和传输中加密已成为标准规范,支出也转向监控和自动化修復,以防范勒索软体攻击。

亚太地区以12.7%的复合年增长率成为成长最快的地区,这主要得益于新加坡、澳洲和日本监管机构明确了云端使用规则,鼓励银行实现分店技术现代化并推出行动优先服务。金融集团正在部署混合桌面网格,将本地资料中心单元与区域超大规模资料中心容量结合,因此能够快速拓展至邻近市场。印度和东南亚的金融科技生态系统透过待开发区计画进一步推动了需求,这些计画突破了传统系统的限制。

在欧洲,GDPR合规性和能源效率要求正推动稳定的设备更新换代。法兰克福和巴黎的银行正着力部署符合ESG目标的精简型用户端,以低功耗终端取代老旧的PC,并将这些终端与集中式虚拟桌面整合。严格的资料主权法规正在刺激对特定国家云端区域和加密金钥託管的投资。在中东和非洲,杜拜和约翰尼斯堡虽然金融自由区尚处于起步阶段,但正在加速推进,鼓励发放数位化优先的银行执照。在南美洲,巴西和智利的金融机构正在试行为客服中心客服人员部署云端桌面,同时将核心应用程式保留在本地。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 云端迁移策略在顶级银行中日益受到重视

- 向零信任安全框架的转型正在加速。

- 资本市场交易大厅实施混合办公模式

- ESG驱动的节能型精简型用户端需求

- 利用GPU扩展风险分析工作负载

- AI-PC 终端的激增使得本地推理卸载成为可能。

- 市场限制

- 传统大型主机整合的复杂性

- 云端原生 VDI 操作方面的技能差距

- 供应商集中风险

- 监管资料驻留要求推高了部署成本。

- 关键法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 透过桌面交付平台

- 託管虚拟桌面 (HVD)

- 託管共用桌面 (HSD)

- Desktop-as-a-Service(DaaS)

- Remote Desktop Services(RDS)

- 透过部署模式

- 本地部署

- 云

- 杂交种

- 按组织规模

- 大公司

- 中小企业

- 最终用户

- 零售银行

- 资本市场与交易

- 保险

- 金融科技和支付服务提供者

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Citrix Systems, Inc.

- Microsoft Corporation

- VMware, Inc.

- Amazon Web Services, Inc.

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Dell Technologies Inc.

- Huawei Technologies Co., Ltd.

- Oracle Corporation

- Google LLC

- Parallels International GmbH(Corel)

- NComputing Co., Ltd.

- Evolve IP, LLC

- Ericom Software Ltd.

- Workspot, Inc.

- Nerdio, Inc.

- Anunta Tech Inc.

- Accops Systems Pvt. Ltd.

- XTIUM(ATSG)

- DXC Technology Company

第七章 市场机会与未来展望

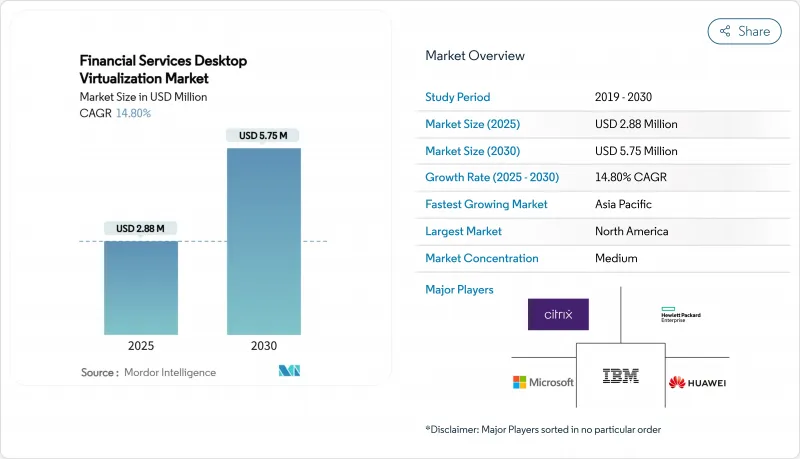

The financial services desktop virtualization market size stands at USD 2.88 million in 2025 and is projected to reach USD 5.75 million by 2030, posting a 14.8% CAGR over the forecast period.

Demand rises as banks, insurers, and FinTechs converge on secure virtual desktop environments that satisfy zero-trust mandates, GPU-accelerated risk analytics, and stringent data-residency rules. Tier-1 institutions are shifting from capital spending to consumption-based models, pushing vendors to embed compliance tooling and high-performance graphics in offerings. Asia-Pacific outpaces other regions on account of rapid financial-sector digitization and supportive cloud guidelines, while North America remains the largest adopter owing to mature trading and regulatory infrastructures [CMCGLOBAL.COM.VN]. Vendor competition centers on balancing ultra-low-latency trader desktops with operational efficiency gains from cloud orchestration.

Global Financial Services Desktop Virtualization Market Trends and Insights

Widespread Cloud-Migration Strategies Among Tier-1 Banks

Large banks refactor desktop estates around hybrid-cloud blueprints to improve resilience and cut ownership costs. Sensitive trading platforms stay on-premises, while back-office desktops shift to cloud subscription models, enabling dynamic provisioning for contractors, test teams, and disaster-recovery drills . Procurement therefore pivots from hardware refresh cycles to operating-expense contracts aligned with business outcomes. The shift accelerates standardization on cloud-native security controls and drives embedded audit-trail functionality across virtual sessions. Vendors capable of bridging legacy data centers with multi-cloud orchestration capture heightened demand as institutions roll out phased migrations over 24-36 months.

Accelerated Move to Zero-Trust Security Frameworks

Financial firms now insist that every virtual desktop connection authenticates continuously, integrating MFA, behavioral analytics, and session-based risk scoring. Traders log in with biometrics and location controls that inhibit data access when anomalies arise, while compliance teams audit keystroke-level histories in real time. These capabilities elevate VDI selection criteria beyond performance to encompass native zero-trust alignment. Consequently, specialist integrators with combined cybersecurity and virtualization expertise command premium consulting rates, and platform roadmaps increasingly embed API hooks for threat-intelligence feeds.

Legacy Mainframe Integration Complexity

Many banks still process high-value transactions on decades-old mainframes. Bridging these systems to modern VDI stacks demands custom middleware, doubled authentication paths, and latency work-arounds that add 6-12 months to roll-outs and raise budgets by double-digit percentages. Dependence on scarce COBOL specialists and proprietary tooling reduces vendor leverage and slows innovation, hampering time-to-value compared to digital-native peers.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid-Work Mandates for Capital-Market Trading Floors

- Growing GPU-Enabled Risk-Analytics Workloads

- Skills Gap in Cloud-Native VDI Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hosted Virtual Desktop retained 47.1% revenue share in 2024, yet Desktop-as-a-Service posts a 17.8% CAGR that steadily erodes incumbent dominance. DaaS gains ground because fee-for-use pricing aligns with volatile head-count swings common in advisory, trading, and compliance units. Service providers bundle regulatory logging and GPU options, letting mid-tier banks access enterprise-grade stacks without capital expenditure spikes. Hosted Shared Desktop products occupy niche environments with standardized apps, while Remote Desktop Services deliver legacy Windows workloads in branches.

The financial services desktop virtualization market benefits as DaaS vendors pre-integrate zero-trust and disaster-recovery playbooks, shortening deployment from months to weeks. Multi-tenant control planes automate patching and vulnerability scans, easing audit pressures. In contrast, on-premises HVD estates still appeal to institutions whose policies prohibit off-site data but face refresh cycles that elevate total cost. Forward-looking buyers therefore favor hybrid procurement, sinking core trading desktops into private clouds while diverting clerical users to public DaaS.

On-premises estates held 58.4% financial services desktop virtualization market share in 2024, but cloud instances compound at 16.2% through 2030. Banks reconcile sovereignty concerns by ring-fencing sensitive data sets locally, then off-loading seasonal or low-risk workloads to hyperscalers. Hybrid orchestration platforms schedule desktops based on latency, compliance tags, and cost.

Cloud acceleration intensifies as regulators publish clearer guidance on encryption, key management, and audit access, lowering perceived risk. Insurers run claims adjudication in cloud regions close to customers for better experience, while core actuarial models remain in private zones. Vendors that deliver uniform policy enforcement across AWS, Azure, and GCP win share as institutions resist platform lock-in.

The Financial Services Desktop Virtualization Market Report Segments the Industry Into Desktop Delivery Platform (Hosted Virtual Desktop (HVD), Hosted Shared Desktop (HSD), and More), Deployment Mode (On-Premise, Cloud and Hybrid), Organization Size (Large Enterprises, and Small and Mid-Sized Enterprises (SMEs)), End-User (Retail and Commercial Banking, Capital Markets and Trading, and More), and Geography.

Geography Analysis

North America led with 41.2% market share in 2024, powered by early zero-trust adoption, dense trading hubs, and large-scale GPU virtualization pilots in New York, Chicago, and Toronto. Institutions invest heavily in resilience, building active-active desktop pairs across metro zones to satisfy Federal guidelines on business continuity. Sub-second failover and encryption-in-transit are baseline specifications, and spending shifts toward monitoring and automated remediation to guard against ransomware.

Asia-Pacific records the fastest 12.7% CAGR, as regulators in Singapore, Australia, and Japan clarify cloud usage rules, encouraging banks to modernize branch technology and launch mobile-first services. Financial groups deploy hybrid desktop grids blending local data-center pods with regional hyperscaler capacity, allowing rapid expansion into adjacent markets. FinTech ecosystems in India and Southeast Asia further fuel demand through green-field builds that leapfrog legacy limitations.

Europe experiences steady replacement cycles driven by GDPR compliance and energy-efficiency mandates. Banks in Frankfurt and Paris emphasize thin-client rollouts tied to ESG targets, swapping aging PCs for low-wattage endpoints that integrate with centralized virtual desktops. Stringent data-sovereignty statutes spur investments in country-specific cloud regions and encryption key escrow. Middle East and Africa show nascent but accelerating uptake in Dubai and Johannesburg, where financial free zones incentivize digital-first banking licenses. South America advances selectively, with Brazilian and Chilean lenders piloting cloud desktops for contact-centre agents while core applications stay on-premises.

- Citrix Systems, Inc.

- Microsoft Corporation

- VMware, Inc.

- Amazon Web Services, Inc.

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Dell Technologies Inc.

- Huawei Technologies Co., Ltd.

- Oracle Corporation

- Google LLC

- Parallels International GmbH (Corel)

- NComputing Co., Ltd.

- Evolve IP, LLC

- Ericom Software Ltd.

- Workspot, Inc.

- Nerdio, Inc.

- Anunta Tech Inc.

- Accops Systems Pvt. Ltd.

- XTIUM (ATSG)

- DXC Technology Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread cloud-migration strategies among Tier-1 banks

- 4.2.2 Accelerated move to zero-trust security frameworks

- 4.2.3 Hybrid-work mandates for capital-market trading floors

- 4.2.4 ESG-driven demand for energy-efficient thin clients

- 4.2.5 Growing GPU-enabled risk-analytics workloads

- 4.2.6 Proliferation of AI-PC endpoints enabling local inference off-loading

- 4.3 Market Restraints

- 4.3.1 Legacy mainframe integration complexity

- 4.3.2 Skills gap in cloud-native VDI operations

- 4.3.3 Concentrated vendor-dependency risk

- 4.3.4 Regulatory data-residency requirements raising deployment cost

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Desktop Delivery Platform

- 5.1.1 Hosted Virtual Desktop (HVD)

- 5.1.2 Hosted Shared Desktop (HSD)

- 5.1.3 Desktop-as-a-Service (DaaS)

- 5.1.4 Remote Desktop Services (RDS)

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By End-User

- 5.4.1 Retail and Commercial Banking

- 5.4.2 Capital Markets and Trading

- 5.4.3 Insurance

- 5.4.4 FinTech and Payment Providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Citrix Systems, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 VMware, Inc.

- 6.4.4 Amazon Web Services, Inc.

- 6.4.5 Hewlett Packard Enterprise Development LP

- 6.4.6 IBM Corporation

- 6.4.7 Dell Technologies Inc.

- 6.4.8 Huawei Technologies Co., Ltd.

- 6.4.9 Oracle Corporation

- 6.4.10 Google LLC

- 6.4.11 Parallels International GmbH (Corel)

- 6.4.12 NComputing Co., Ltd.

- 6.4.13 Evolve IP, LLC

- 6.4.14 Ericom Software Ltd.

- 6.4.15 Workspot, Inc.

- 6.4.16 Nerdio, Inc.

- 6.4.17 Anunta Tech Inc.

- 6.4.18 Accops Systems Pvt. Ltd.

- 6.4.19 XTIUM (ATSG)

- 6.4.20 DXC Technology Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2025年全球桌面虚拟化市场报告2025年全球远端桌面软体市场报告

2025年全球桌面虚拟化市场报告2025年全球远端桌面软体市场报告 2025-2029 年全球虚拟桌面虚拟化市场

2025-2029 年全球虚拟桌面虚拟化市场 2025 年至 2033 年桌面虚拟化市场报告(按类型(虚拟桌面基础设施、桌面即服务、远端桌面服务)、组件、组织规模、垂直行业和地区划分)

2025 年至 2033 年桌面虚拟化市场报告(按类型(虚拟桌面基础设施、桌面即服务、远端桌面服务)、组件、组织规模、垂直行业和地区划分) 製造业中的桌面虚拟化:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)日本桌面虚拟化市场报告(按组件、类型(虚拟桌面基础设施、桌面即服务、远端桌面服务)、组织规模、行业垂直领域和地区)2025 年至 2033 年

製造业中的桌面虚拟化:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)日本桌面虚拟化市场报告(按组件、类型(虚拟桌面基础设施、桌面即服务、远端桌面服务)、组织规模、行业垂直领域和地区)2025 年至 2033 年 远端桌面软体的全球市场

远端桌面软体的全球市场 远端桌面软体市场规模、份额和成长分析(按部署类型、企业规模、最终用户和地区)- 产业预测 2025-2032全球虚拟桌面市场印度虚拟桌面:市场占有率分析、行业趋势和成长预测(2025-2030 年)

远端桌面软体市场规模、份额和成长分析(按部署类型、企业规模、最终用户和地区)- 产业预测 2025-2032全球虚拟桌面市场印度虚拟桌面:市场占有率分析、行业趋势和成长预测(2025-2030 年)