|

市场调查报告书

商品编码

1851428

金属包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

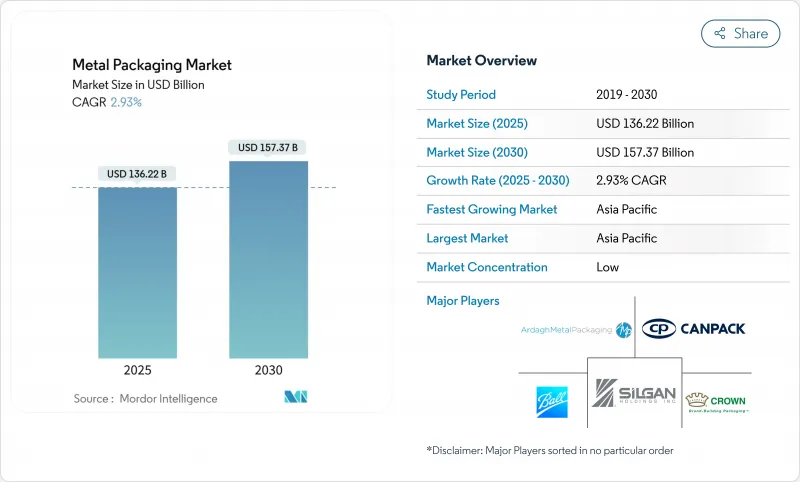

预计到 2025 年,金属包装市场规模将达到 1,362.2 亿美元,到 2030 年将达到 1,573.7 亿美元,在此期间的复合年增长率为 2.93%。

循环经济法规、即饮饮料的优质化以及零售商承诺以金属替代塑料,共同推动了市场的稳定成长。铝材优异的回收经济性,加上轻量化材料的进步以及品牌商提出的范围3减排目标,正巩固金属包装市场作为碳酸饮料和机能饮料首选包装的地位。生产商继续透过长期合约和废料供应策略来规避铝和钢价格波动的风险,而涂料供应商则加速向不含无BPA)的化学品转型,以保障消费者安全。在竞争日趋成熟但机会无限的市场中,领先的罐体製造商不断深化在涂料、回收和数位印刷领域的垂直整合,以巩固市场份额,因此市场竞争格局依然保持适度。

全球金属包装市场趋势与洞察

循环经济要求扩大罐头到罐头的回收循环

日益严格的监管正在重塑价值链经济格局,强制规定铝罐的最低再生材料含量标准,而铝罐的再生材料含量已经超过该标准,这使得金属包装市场在合规方面占据优势。欧盟的PPWR指令要求到2030年,饮料容器的再生材料含量必须达到30%,而铝罐的平均再生材料含量为71%。押金返还机制正在推动回收率在2029年达到90%,从而确保废料流向的可预测性,并减少对原生金属的依赖。像波尔公司这样的全球製造商的目标是实现85%的再生材料含量,并透过提高闭合迴路效率来降低原料成本风险。澳洲正效法欧盟的规定,要求到2040年,食品罐的消费后再生材料基准值达到80%。持续的监管力度正在巩固铝相对于PET的优势,尤其是在饮料业,因为采购现在已将循环性评分纳入供应商的竞标中。

新兴亚洲即饮饮料的优质化

高端罐装饮料需求的激增正在推动亚太地区金属包装市场的成长。随着消费者寻求低卡路里、低酒精饮品,预计2018年至2023年间,日本罐装酒在美国的销售量将增加两倍。朝日啤酒旗下的生酒(Nama Jokki)等品牌就是一个很好的例子,它展示了包装创新如何将店内体验带回家。中国和印度消费者可支配收入的成长,正推动高端即饮咖啡、康普茶和功能性代餐饮料进入零售主流市场。优质化趋势使得製造商能够将更高的材料成本转嫁给消费者,从而在铝价波动的情况下维持净利率。

伦敦金属交易所铝和钢铁价格波动

主导价格波动给利润率带来压力,因为金属包装市场仍然依赖于滞后于现货价格波动的转嫁条款合约。欧洲冶炼厂面临持续的能源成本压力,加剧了全球价格波动。虽然大型冶炼厂能够透过废钢原料和多年期合约来吸收波动,但小型冶炼厂仍面临风险,导致其资本支出週期放缓。

细分市场分析

预计到2024年,铝将占金属包装市场份额的42.46%,到2030年将以3.68%的复合年增长率成长。钢材在大型食品和工业用桶领域仍占据重要地位,但由于重量和能源方面的考虑,其成长速度正在放缓。诺贝丽斯公司投资9000万美元将其在英国的易拉罐回收能力翻番,突出了这种材料的战略重要性。铝材的轻量化特性可以减少物流排放,符合环境、社会和治理(ESG)标准,并增强饮料品牌的顾客忠诚度。随着市场参与企业不断投资于重熔技术,与再生铝相关的金属包装市场规模正在稳步扩大。

与原生铝相比,再生铝的价格优势有助于品牌控制原物料成本并降低采购风险。印度铝业(Hindalco)100亿美元的生产力计画表明,一体化冶炼和回收中心如何缩短供应链并支持积极的再生材料含量目标。钢铁的磁性可回收性在混合废弃物处理中仍然是一大优势,但随着碳排放税的日益普及,容器重量和运输成本也随之增加。虽然钢铁在优先考虑机械强度和抗穿刺性的耐用应用领域仍有一席之地,但总体而言,铝的成本、循环性和重量优势巩固了其主导地位。

到2024年,罐装产品将占金属包装市场41.67%的份额,复合年增长率(CAGR)为6.34%,主要得益于全球便利通路中即饮咖啡、碳酸饮料和机能饮料的优质化。波尔公司的Dynamark Advanced Pro可变图形系统可大规模实现罐身个人化,协助负责人提升互动性和货架吸引力。食品罐将保持稳定的市场份额,为番茄酱、汤料和宠物食品等产品的全球贸易提供高阻隔保护。随着疫情后新兴市场对美髮造型、除臭剂和家用清洁用品等品类的强劲需求,气雾罐也将受惠于个人护理产品的成长。

轻量化措施在不影响产品完整性的前提下降低了单位铝材用量,从而有助于控製成本并减少范围 3 的碳足迹。瓶盖、封盖和坚固耐用的容器凭藉其防篡改保护和便利性,继续保持其在特定领域的市场地位。散装桶和中型钢製容器在农药和食用油领域仍然很受欢迎,因为可重复使用性和联合国运输认证对这些产品至关重要。综上所述,这些动态共同确保了罐装产品将继续占据金属包装市场的主导地位,而辅助包装领域将透过材料科学和设计创新不断发展。

区域分析

亚太地区预计到2024年将占全球金属包装市场38.56%的份额,并在2030年之前以6.12%的复合年增长率成长。在地化的罐板供应,加上印度铝业公司(Hindalco)投资数十亿美元建设的冶炼厂及回收设施,支撑了其成本领先优势和循环经济理念,这些优势对全球品牌所有者极具吸引力。日本在设计方面引领潮流,并出口高品质的罐头包装,影响区域市场的发展趋势;而东南亚国家则受益于旅游业主导的饮料需求以及新的押金返还试点计画。

北美市场已趋于成熟,国内製罐生产线接近满载运作,并与主要啤酒和软性饮料灌装商签订了长期供应协议。关税迫使製罐商在国内采购金属,刺激了对废料加工钢坯厂和仓库自动化设施的投资,降低了单位成本。各州普遍实施的瓶罐回收法案使铝回收率维持在60%以上,增强了二次生产的原料供应。

欧洲凭藉其严格的PPWR(聚对苯二甲酸乙二醇酯)要求和先进的回收网络,已成为涂层创新和数位浮水印试点计画的摇篮。皇冠集团位于西班牙和义大利的可扩展工厂近期新增了为精酿啤酒出口商生产的高速生产线,证明即使是饱和的市场也蕴藏着永续的机会。以巴西为首的南美洲市场正经历强劲的销售成长,啤酒品牌商纷纷转向罐装包装,以提升产品高端定位和物流效率。儘管中东和非洲的基础设施建设相对滞后,但不断增长的人口和日益提高的收入为气雾剂空气清新剂和罐装食品开闢了待开发区前景,从而确保了全球金属包装市场的全部区域增长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 循环经济政策推动罐头回收循环

- 亚洲新兴国家即饮饮料的优质化

- 零售商塑胶变金属承诺

- 与PET相比,较高的废料回收率降低了实际成本。

- Incan 的 QR/NFC 技术开启了消费者资料货币化之路

- 市场限制

- 伦敦金属交易所铝和钢铁价格波动

- 品牌所有者对第三阶段二氧化碳排放量的强烈反对

- 单一材料纸瓶的兴起

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治局势如何影响市场

- 投资分析

第五章 市场规模与成长预测

- 依材料类型

- 铝

- 钢

- 依产品类型

- 能

- 食品罐头

- 饮料罐

- 气雾罐

- 散装容器

- 运输用桶子和罐

- 盖子与封口装置

- 能

- 按最终用户行业划分

- 饮料

- 食物

- 化妆品和个人护理

- 家用

- 其他终端用户产业

- 按涂层/衬里类型

- 含双酚A的环氧树脂

- BPA-NI环氧树脂

- 聚酯/PET

- 其他涂层/衬里类型

- 按货柜容量

- 少于 250 毫升

- 251-500mL

- 501-1000mL

- 1000毫升或更多

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲、纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ardagh Metal Packaging SA

- Ball Corporation

- Crown Holdings Inc.

- CANPACK SA

- Silgan Holdings Inc.

- Greif Inc.

- TUBEX Packaging GmbH

- Mauser Packaging Solutions

- Nampak Limited

- Colep Packaging

- CPMC Holdings Ltd.

- Toyo Seikan Group Holdings

- Amcor plc(Metal division)

- AptarGroup Inc.

- Alcoa Corporation

- Sherwin-Williams(Can Coatings)

- Novelis Inc.

- Hindalco Industries Ltd.

- RPC Group plc

- BWAY Corporation

- Berlin Packaging

第七章 市场机会与未来展望

The metal packaging market size is valued at USD 136.22 billion in 2025 and is projected to reach USD 157.37 billion by 2030, reflecting a 2.93% CAGR over the period.

Steady growth stems from circular-economy legislation, premiumisation of ready-to-drink beverages, and retailers' plastic-to-metal substitution pledges. Aluminium's superior recycling economics, combined with material-lightweighting advances and brand-owner scope-3 reduction targets, reinforce the metal packaging market as the default option for carbonated and functional beverages. Producers continue to hedge aluminium and steel price swings through long-term contracts and scrap-based supply strategies, while coating suppliers accelerate the shift to BPA-free chemistries that underpin consumer safety narratives. Competitive intensity remains moderate as the leading canmakers deepen vertical integration across coating, recycling, and digital printing capabilities to defend share in a mature yet opportunity-rich landscape.

Global Metal Packaging Market Trends and Insights

Circular-Economy Mandates Boost Can-to-Can Recycling Loops

Tighter legislation is reshaping value-chain economics by mandating minimum recycled-content thresholds that aluminium cans already exceed, giving the metal packaging market a compliance edge. The EU's PPWR requires 30% recycled material in beverage containers by 2030, yet aluminium cans average 71% recycled content. Deposit-return schemes are driving collection rates toward 90% by 2029, supporting predictable scrap flows and reducing virgin-metal dependency. Global producers such as Ball target 85% recycled content, reinforcing closed-loop efficiencies that temper raw-material cost risk. Australia mirrors EU rules with an 80% post-consumer threshold for food-grade cans by 2040.Sustained regulatory momentum cements aluminium's moat over PET, particularly in beverages where procurement now factors circularity scores into supplier bids.

Premiumization of RTD Beverages in Emerging Asia

Surging demand for premium canned drinks is accelerating the metal packaging market growth in Asia-Pacific. Japan's canned chuhai segment tripled in the United States between 2018 and 2023 as consumers seek low-calorie, low-alcohol options. Brands like Asahi's Nama Jokki can demonstrate how packaging innovations replicate on-premise experiences in at-home settings. Rising disposable incomes in China and India push premium RTD coffee, kombucha, and functional meal-replacement beverages into mainstream retail, all of which rely on cans for flavor protection and thermal performance. The premiumisation wave enables manufacturers to pass higher material costs through to consumers, sustaining margins despite aluminium volatility.

Price Volatility of LME Aluminium and Steel

Energy-driven price swings strain margins because the metal packaging market still relies on contracts with pass-through clauses that lag spot fluctuations. North American tariffs add complexity, forcing producers to blend hedging tools with regional sourcing to protect competitiveness.European smelters face persistent energy-cost pressure, contributing to global price turbulence. While large players offset volatility through scrap-based feedstocks and multi-year agreements, smaller converters remain exposed, which can slow capital investment cycles.

Other drivers and restraints analyzed in the detailed report include:

- Retailers' Plastic-to-Metal Substitution Pledges

- High Scrap Recovery Rates Lower True Cost vs. PET

- Brand-Owner Push-Back on Scope-3 CO2 Footprint

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminium generated 42.46% of the metal packaging market share in 2024 and is projected to grow at a 3.68% CAGR through 2030, benefiting from closed-loop recycling systems that meet PPWR mandates. Steel maintains relevance in large-format food and industrial drums but grows more slowly due to weight and energy considerations. Novelis's USD 90 million UK expansion to double can-recycling capacity underscores the material's strategic importance. Aluminium's light weight reduces logistics emissions, aligning with ESG scorecards and deepening customer loyalty among beverage brands. Market participants continue to invest in remelt technology, enabling the metal packaging market size associated with secondary aluminium to expand steadily.

Secondary aluminium pricing advantages help brands manage raw-material costs relative to virgin metal, mitigating procurement risk. Hindalco's USD 10 billion capacity plan illustrates how integrated smelting and recycling hubs shorten supply chains and support aggressive recycled-content targets. Steel's magnetic recoverability remains a plus in mixed-waste streams, yet higher container weight raises transport costs as carbon taxes spread. Altogether, aluminium's cost, circularity, and weight advantages cement its leadership position, even as steel serves resilient niches that prioritize mechanical strength and puncture resistance.

Cans represented 41.67% of the metal packaging market in 2024 and are set to grow at a 6.34% CAGR, propelled by the premiumisation of RTD coffee, hard seltzer, and functional beverages across global convenience channels. Ball's Dynamark Advanced Pro variable-graphics system personalizes cans at scale, allowing marketers to boost engagement and shelf appeal. Food cans hold a stable base, supplying high-barrier protection that underwrites global trade in tomato paste, soups, and pet food. Aerosol cans tap personal-care growth as pent-up post-pandemic demand lifts hair styling, deodorant, and household-cleaning categories in emerging markets.

Light-weighting initiatives reduce aluminium per unit without compromising integrity, helping contain costs and shrink scope-3 footprints. Caps, closures, and lug lids maintain niche relevance by providing tamper evidence and convenience. Bulk drums and intermediate steel containers retain popularity for agrochemicals and edible oils, where reusability and UN transport certifications are critical. Collectively, these dynamics guarantee that cans remain the metal packaging market's flagship product while ancillary segments evolve through material science and design innovation.

The Metal Packaging Market Report is Segmented by Material Type (Aluminum, Steel), Product Type (Bulk Containers, Shipping Barrels and Drums, Caps and Closures, and More), End-User Industry (Beverage, Food, and More), Coating/Lining Type (BPA-Based Epoxy, BPA-NI Epoxy and More), Container Capacity (less Than 250 Ml, 251-500, and More), Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.56% of the metal packaging market in 2024 and is tracking a 6.12% CAGR through 2030, anchored by China's burgeoning RTD sector and India's rising middle class. Localised can-sheet supply, combined with Hindalco's multi-billion-dollar smelter-plus-recycling build-out, underpins cost leadership and circular credentials that appeal to global brand owners. Japan contributes design leadership, exporting high-quality chuhai formats that influence regional adoption patterns, while Southeast Asian nations leverage tourism-driven beverage demand and emerging deposit-return pilots.

North America represents a mature arena where domestic can lines run near full utilisation, cushioned by long-term supply contracts with major beer and soft-drink fillers. Tariff regimes compel canmakers to source metal domestically, spurring investment in scrap-based billet facilities and warehouse automation to drive down per-unit costs. Widespread state-level bottle bills keep aluminium recovery rates above 60%, bolstering feedstock security for secondary production.

Europe combines rigorous PPWR requirements with sophisticated recycling networks, making it a crucible for coating innovations and digital watermark pilots. Crown's scalable plants in Spain and Italy recently added high-speed lines to serve craft-beer exporters, evidencing sustained opportunity even within a saturated market. South America, spearheaded by Brazil, exhibits strong volume growth as beer brand owners convert to cans for premium positioning and logistics efficiency. The Middle East and Africa trail on infrastructure, yet population expansion and rising incomes provide greenfield prospects for aerosol deodorant and canned-food penetration, ensuring region-wide growth contributions to the global metal packaging market.

- Ardagh Metal Packaging S.A.

- Ball Corporation

- Crown Holdings Inc.

- CANPACK S.A.

- Silgan Holdings Inc.

- Greif Inc.

- TUBEX Packaging GmbH

- Mauser Packaging Solutions

- Nampak Limited

- Colep Packaging

- CPMC Holdings Ltd.

- Toyo Seikan Group Holdings

- Amcor plc (Metal division)

- AptarGroup Inc.

- Alcoa Corporation

- Sherwin-Williams (Can Coatings)

- Novelis Inc.

- Hindalco Industries Ltd.

- RPC Group plc

- BWAY Corporation

- Berlin Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Circular-economy mandates boost can-to-can recycling loops

- 4.2.2 Premiumisation of RTD beverages in emerging Asia

- 4.2.3 Retailers' plastic-to-metal substitution pledges

- 4.2.4 High scrap recovery rates lower true cost vs. PET

- 4.2.5 In-can QR/NFC tech unlocking consumer-data monetisation

- 4.3 Market Restraints

- 4.3.1 Price volatility of LME aluminium and steel

- 4.3.2 Brand-owner push-back on scope-3 CO? footprint

- 4.3.3 Rise of mono-material paper bottles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitical Scenario on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Product Type

- 5.2.1 Cans

- 5.2.1.1 Food Cans

- 5.2.1.2 Beverage Cans

- 5.2.1.3 Aerosol Cans

- 5.2.2 Bulk Containers

- 5.2.3 Shipping Barrels and Drums

- 5.2.4 Caps and Closures

- 5.2.1 Cans

- 5.3 By End-user Industry

- 5.3.1 Beverage

- 5.3.2 Food

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Household

- 5.3.5 Other End-user Industry

- 5.4 By Coating / Lining Type

- 5.4.1 BPA-Based Epoxy

- 5.4.2 BPA-NI Epoxy

- 5.4.3 Polyester / PET

- 5.4.4 Other Coating / Lining Type

- 5.5 By Container Capacity

- 5.5.1 Less than 250 ml

- 5.5.2 251 - 500 ml

- 5.5.3 501 - 1000 ml

- 5.5.4 More than 1000 ml

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardagh Metal Packaging S.A.

- 6.4.2 Ball Corporation

- 6.4.3 Crown Holdings Inc.

- 6.4.4 CANPACK S.A.

- 6.4.5 Silgan Holdings Inc.

- 6.4.6 Greif Inc.

- 6.4.7 TUBEX Packaging GmbH

- 6.4.8 Mauser Packaging Solutions

- 6.4.9 Nampak Limited

- 6.4.10 Colep Packaging

- 6.4.11 CPMC Holdings Ltd.

- 6.4.12 Toyo Seikan Group Holdings

- 6.4.13 Amcor plc (Metal division)

- 6.4.14 AptarGroup Inc.

- 6.4.15 Alcoa Corporation

- 6.4.16 Sherwin-Williams (Can Coatings)

- 6.4.17 Novelis Inc.

- 6.4.18 Hindalco Industries Ltd.

- 6.4.19 RPC Group plc

- 6.4.20 BWAY Corporation

- 6.4.21 Berlin Packaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

金属包装市场:依材料、产品类型、最终用途产业及地区划分

金属包装市场:依材料、产品类型、最终用途产业及地区划分 2025-2033年金属包装市场报告(依产品类型、材料、应用和地区)

2025-2033年金属包装市场报告(依产品类型、材料、应用和地区) 金属包装市场按产品类型、材料类型、涂层类型、产品设计、生产技术、最终用途产业划分-2025-2030 年全球预测

金属包装市场按产品类型、材料类型、涂层类型、产品设计、生产技术、最终用途产业划分-2025-2030 年全球预测 泰国金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)乳製品金属包装市场按容器类型、材料类型、封盖类型、应用和分销管道划分 - 全球预测 2025-2030

泰国金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)乳製品金属包装市场按容器类型、材料类型、封盖类型、应用和分销管道划分 - 全球预测 2025-2030 全球金属包装市场:市场规模、份额、趋势分析(按材料、产品类型、最终用途和地区)、细分市场预测(2025-2030 年)

全球金属包装市场:市场规模、份额、趋势分析(按材料、产品类型、最终用途和地区)、细分市场预测(2025-2030 年) 金属包装市场规模、份额和成长分析(按产品类型、材料、应用和地区)- 产业预测 2025-2032印度金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)2030 年钢包装市场预测:按产品、材料、分销管道、最终用户和地区进行的全球分析金属包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

金属包装市场规模、份额和成长分析(按产品类型、材料、应用和地区)- 产业预测 2025-2032印度金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)2030 年钢包装市场预测:按产品、材料、分销管道、最终用户和地区进行的全球分析金属包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测