|

市场调查报告书

商品编码

1851573

能源产业的预测性维护:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Predictive Maintenance In The Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

预计到 2025 年,能源产业的预测性维护市场规模将达到 22.5 亿美元,到 2030 年将达到 70.8 亿美元。

持续的电气化、资料中心的激增以及对电网可靠性日益增长的担忧,正迫使资产所有者用资料主导模型取代传统的「运行至故障」模式,以降低全生命週期拥有成本并延长资产寿命。诸如美国环保署针对长寿命燃煤电厂90%碳捕获率的规定以及欧盟的《企业永续性报告指令》等监管要求,推动了数位化预算的增加,因为营运商现在必须证明其运作和排放绩效。同时,工业物联网感测器价格的快速下降和人工智慧演算法的日益成熟,使得大型设备的投资回收期缩短至18-24个月,加速了其在汽轮机房、变电站和中游管道等领域的应用。将边缘运算与云端分析相结合的供应商已经报告称,透过减少停机时间和优化零件库存,实现了数亿美元的成本节约。

全球能源预测性维护市场趋势与洞察

整合工业物联网、人工智慧和巨量资料分析

西门子的Senseye平台可自动产生数位化行为模型,在解决关键劳动力短缺问题的同时,将维护成本降低高达40%。雪佛龙的即时异常侦测接地故障保护技术可保障密集型耗能资料中心丛集的持续供电。边缘节点在本地处理振动和温度数据,然后传输到云端,从而创建一个自主生态系统,该系统能够挖掘整个车队的运作模式,并在无需人工干预的情况下安排干预措施。这些市场发展趋势使能源预测性维护市场成为资产密集型公用事业公司数位转型蓝图的核心。

降低非计划性停机时间的成本压力

由于人工智慧工作负载的增加,停机罚款不断攀升,需求激增,停机已成为董事会层面的风险,预测性维护也从可有可无转变为营运必要。 NextEra Energy 的燃气涡轮机专案实现了 23% 的停机时间减少和每年 2,500 万美元的节约,充分证明了能源预测性维护市场的投资回报率。领先的油气业者已证明,优化维护週期可将资产寿命延长 20% 至 40%,从而在数十年内提升设备循环利用的价值。而那些行动迟缓的企业则面临着糟糕的客户体验和更高的能源成本,因为竞争对手能够以更低的备件库存维持更高的资产可用性。

初始部署和整合成本高昂

对于大型公用事业公司而言,全面的传感器维修、边缘网关和云端协作通常会使计划预算高达数千万美元,这对资金紧张的开发中国家营运商构成了一大障碍。 GE Vernova 在美国耗资约 6 亿美元的工厂升级项目,展现了在车队层级释放预测价值所需的现代化规模。铜和稀土价格的上涨将使硬体支出从 2024 年起增加高达 25%。儘管如此,主要采用者已在两年内收回了投资,而且随着供应商推出与性能保证挂钩的订阅模式,财务壁垒正在降低,这再次印证了能源预测性维护市场的长期竞争力。

细分市场分析

到2024年,解决方案将占据能源预测性维护市场65.3%的份额,这反映出营运商偏好选择整合分析、视觉化和工作流程自动化的平台。虽然能够每天处理TB级Terabyte和变压器数据的软体套件仍然至关重要,但具备设备端推理能力的嵌入式感测器将增强边缘智能,减少不必要的数据排放并加速洞察。公用事业公司和独立发电企业依赖供应商提供整合、变更管理和全天候监控服务。

服务供应商正受益于资料科学和旋转机械物理学领域日益增长的人才缺口。随着营运商将传统历史资料库迁移到云端资料湖,且不中断生产,整合和实施尤其重要。託管服务通常以基于结果的合约形式构建,可确保可用性指标,从而使供应商的奖励与资产性能保持一致。随着客户将重点放在结果而非套件包上,能源预测性维护产业正稳步转型为以服务为导向的市场,在这个市场中,卓越营运比功能清单更为重要。

预计到2024年,云端运算在能源预测性维护市场的占比将达到72.6%,随着演算法复杂性和资料量的成长超过本地运算能力,云端运算的地位将进一步巩固。目前,单一离岸风力发电每天会产生数十Terabyte的SCADA和雷射雷达数据,因此云原生架构更适合实现即时扩展和持续的模型重训练。边缘云混合架构可以降低负载削减和叶片桨距调整的延迟,在保持关键任务迴路本地运行的同时,集中处理总体分析。

儘管在偏远盆地和对网路主权和延迟要求极高的核能发电厂等地区,本地部署系统仍然不可或缺,但大多数供应商都在捆绑云端连接器,以便未来迁移。Honeywell与Verizon合作部署的5G智慧电錶正是这项转变的典型例证。安全的蜂窝回程传输将亚秒遥测数据传输到人工智慧引擎,该引擎能够提前数天预测变压器热点。这类应用案例凸显了能源预测性维护市场与更广泛的电网数位化倡议密不可分的原因,而这些计画都依赖于无所不在的低延迟连线。

能源产业预测性维护市场细分依据产品类型(解决方案和服务)、部署模式(云端、本地部署)、最终用户产业(发电、可再生能源、石油天然气等)、资产类型(涡轮机和旋转设备、变压器和变电站等)以及地区划分。市场预测以美元计价。

区域分析

北美将继续保持领先地位,预计到2024年将占全球收入的27.9%,这主要得益于联邦基础设施项目、公共产业的大力投入以及人工智慧平台的早期应用。美国能源资讯署预测,到2030年,国内电力需求将成长15%至20%,部分原因是超大规模资料中心的兴起,这将促使人们更加关注如何预防停电。云端原生法规环境和充足的创业投资资金将进一步加速新技术试点,巩固该地区在能源预测性维护市场的主导地位。

在绿色新政脱碳目标和严格的停电处罚机制的推动下,欧洲保持着稳定发展的势头,这些措施提高了可靠性指标。企业永续性报告要求公用事业公司揭露即时排放和能源效率关键绩效指标。大型车队营运商正在将数位孪生技术与基于卫星的植被监测相结合,以满足合规性和韧性目标。

亚太地区是成长最快的区域,年复合成长率高达26.5%,主要得益于中国数位化电网规划和东南亚快速电气化进程的推动。中国南方电网的端到端数位转型展示了跨越式技术如何绕过传统瓶颈,并将预测性工作流程直接嵌入到新的基础设施中。同时,印度和印尼正大力投资升级电网,从而催生了对发送类型分析的待开发区需求。儘管规模较小,但中东和非洲地区也对预测性维护表现出越来越浓厚的兴趣,这得益于“2030愿景”大型企划以及类似倡议,这些项目要求即使在严酷的沙漠环境中也能运作完美运行,从而扩大了能源领域的预测性维护市场基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 能源基础设施老化与对电网可靠性的重视(主流)

- 工业物联网、人工智慧和巨量资料分析的融合(主流)

- 降低非计划性停机时间的成本压力(主流)

- 安全/排放气体法规(主流)

- 结合无人机和卫星遥感探测(低调进行)

- 数位双胞胎驱动的基于风险的维护(鲜为人知)

- 市场限制

- 高昂的领先成本和整合成本(主流)

- 网路安全漏洞日益增多(主流观点)

- 能源领域资料科学人才短缺(鲜为人知)

- 多方资产中关于资料所有权和责任的争议(鲜为人知)

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 评估市场的宏观经济因素

第五章 市场规模及成长预测(价值,2024-2030 年)

- 报价

- 解决方案

- 软体平台

- 嵌入式硬体和感测器

- 服务

- 整合与实施

- 託管服务

- 解决方案

- 按部署模式

- 云

- 本地部署

- 按最终用户行业划分

- 发电(火力发电、核能、水力)

- 可再生能源(风能、太阳能和储能)

- 石油和天然气(上游、中游、下游)

- 公共产业和输配电

- 采矿和矿产

- 依资产类型

- 涡轮机和旋转设备

- 变压器和变电站

- 管道和压缩机

- 泵浦和阀门

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- SAP SE

- Siemens AG

- GE Digital

- ABB Ltd

- Schneider Electric SE

- Intel Corporation

- Robert Bosch GmbH

- Accenture plc

- Honeywell International Inc.

- Hitachi Energy Ltd.

- Emerson Electric Co.

- Aspen Technology, Inc.

- AVEVA Group plc

- Uptake Technologies Inc.

- SparkCognition, Inc.

- Senseye Ltd.

- SKF Group

- Bentley Systems, Inc.

- Mitsubishi Electric Corporation

- Caterpillar Inc.(Asset Intelligence)

- DNV AS

- KONUX GmbH

第七章 市场机会与未来展望

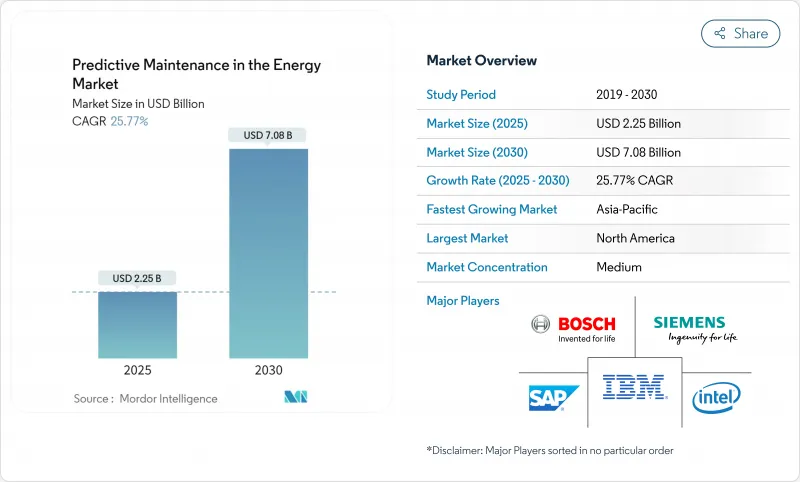

The predictive maintenance in the energy market size reached USD 2.25 billion in 2025 and is on track to hit USD 7.08 billion by 2030, reflecting a compelling 25.77% CAGR over the forecast period.

Unrelenting electrification, surging data-center build-outs, and mounting grid-reliability concerns are pushing asset owners to replace run-to-failure routines with data-driven models that lower the lifetime cost of ownership while stretching remaining asset life. Regulatory mandates such as the EPA's 90% carbon-capture rule for long-term coal plants and the EU's Corporate Sustainability Reporting Directive are catalyzing digitalization budgets because operators must now prove both uptime and emissions performance. Simultaneously, rapid IIoT sensor price declines and maturing AI algorithms are shrinking payback cycles to 18-24 months for large fleets, amplifying adoption momentum across turbine halls, substations, and midstream pipelines. Vendors that fuse edge computing with cloud analytics already report nine-figure savings driven by shorter outage windows and optimized part inventories.

Global Predictive Maintenance In The Energy Market Trends and Insights

Integration of IIoT, AI and Big-Data Analytics

The fusion of low-cost sensors with AI pattern-recognition algorithms is recasting maintenance from reactive to prescriptive modes across turbine decks and compressor stations.Siemens' Senseye platform now generates digital behavior models automatically, slicing maintenance spend by up to 40% while addressing acute workforce shortages. Chevron's real-time anomaly detection for leak prevention safeguards continuous power delivery to energy-intensive data-center clusters. Edge nodes process torrents of vibration and temperature data locally before forwarding condensed insights to the cloud for fleet-wide pattern mining, creating near-autonomous ecosystems that schedule interventions without human prompts. These developments place predictive maintenance in the energy market squarely at the center of digital-transformation roadmaps for asset-heavy utilities.

Cost Pressure to Cut Unplanned Downtime

Escalating outage penalties and demand spikes from AI workloads are making downtime a board-level risk, moving predictive maintenance from a discretionary line item to an operational imperative. NextEra Energy's gas-turbine program delivered a 23% outage reduction and USD 25 million in annual savings, validating the hard ROI underpinning the predictive maintenance in the energy market. Large oil-and-gas operators have documented 20-40% asset-life extension through optimized service intervals, compounding value over decades-long equipment cycles. Firms that lag on adoption face customer-experience erosion and higher delivered-energy costs as competitors sustain higher asset availability with leaner spares inventories.

High Upfront Implementation and Integration Cost

Comprehensive sensor retrofits, edge gateways, and cloud orchestration commonly push project budgets into eight figures for large utilities, deterring cash-constrained operators in developing economies. GE Vernova's nearly USD 600 million U.S. factory upgrades illustrate the scale of modernization needed to unlock predictive value at fleet level. Rising copper and rare-earth prices have inflated hardware outlays by up to 25% since 2024. Nonetheless, leading adopters recuperate capital within two years, and financial barriers are softening as vendors roll out subscription models linked to performance guarantees, reiterating the long-term competitiveness of the predictive maintenance in the energy market.

Other drivers and restraints analyzed in the detailed report include:

- Aging Energy Infrastructure and Grid Reliability Focus

- Regulatory Mandates on Safety / Emissions

- Rising Cyber-Security Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions controlled 65.3% of the predictive maintenance in the energy market in 2024, reflecting operators' preference for unified platforms that amalgamate analytics, visualization, and workflow automation. Software suites capable of ingesting terabytes of turbine and transformer data per day remain central, while embedded sensors equipped with on-device inference augment edge intelligence, reducing unnecessary data egress and accelerating insights. Services, although smaller in absolute revenue, sprint ahead at 25.9% CAGR as utilities and independent power producers rely on vendors for integration, change management, and 24X7 monitoring.

Service providers benefit from widening talent gaps in data science and rotating-machinery physics. Integration and implementation are especially valued when operators migrate legacy historian databases into cloud data lakes without production interruptions. Managed services, often structured as outcome-based contracts, guarantee availability metrics that align vendor incentives with asset performance. As clients prioritize outcomes over toolkits, the predictive maintenance in the energy industry is steadily morphing into a service-oriented market where operational excellence overrides feature checklists.

Cloud deployments represented 72.6% share of the predictive maintenance in the energy market in 2024, a position expected to strengthen as algorithm complexity and data volumes outstrip on-premise compute capacity. A single offshore wind farm now generates tens of terabytes of SCADA and lidar data daily; instant scalability and continuous model retraining favor cloud-native architectures. Edge-cloud hybrids mitigate latency for load-shedding or blade-pitch adjustments, keeping mission-critical loops local while bulk analytics run centrally.

On-premise systems persist in remote basins and nuclear sites with stringent sovereignty or latency requirements, yet most vendors bundle cloud connectors for future migration. Honeywell's 5G-enabled smart-meter roll-out with Verizon exemplifies the shift: secure cellular backhaul funnels sub-second telemetry into an AI engine that forecasts transformer hot-spots days in advance. Such use cases underscore why the predictive maintenance in the energy market is entwined with broader grid-digitalization initiatives premised on ubiquitous, low-latency connectivity.

Predictive Maintenance in the Energy Sector Market is Segmented by Offering (Solutions and Services), Deployment Model (Cloud, On-Premise), End-User Industry (Power Generation, Renewables, Oil and Gas, and More), Asset Type (Turbines and Rotating Equipment, Transformers and Sub-Stations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

North America retained leadership with 27.9% of 2024 revenue, supported by federal infrastructure programs, aggressive utility spending, and early adoption of AI platforms. The Energy Information Administration projects domestic electricity demand to rise 15-20% by 2030, partly due to hyperscale data centers, intensifying the focus on outage prevention. Cloud-native regulatory environments and ample venture financing further accelerate new-tech pilots, anchoring regional dominance in the predictive maintenance in the energy market.

Europe maintains steady momentum driven by the Green Deal's decarbonization targets and strict outage-penalty regimes that elevate reliability metrics. The Corporate Sustainability Reporting Directive obliges utilities to disclose real-time emissions and energy-efficiency KPIs, for which predictive-maintenance datasets are highly synergistic. Large fleet operators are combining digital twins with satellite-based vegetation monitoring to meet both compliance and resilience goals.

Asia-Pacific is the fastest-growing territory at 26.5% CAGR, buoyed by China's state-backed digital-grid blueprint and Southeast Asia's rapid electrification. China Southern Power Grid's end-to-end digital transformation shows how leapfrog technology can embed predictive workflows directly into new infrastructure, bypassing legacy bottlenecks. Concurrently, India and Indonesia invest heavily in transmission upgrades, creating greenfield demand for cloud-delivered analytics. The Middle East and Africa, though smaller, show rising interest as mega-projects under Vision 2030 and similar initiatives demand flawless uptime under harsh desert conditions, expanding the predictive maintenance in the energy market footprint.

- IBM Corporation

- SAP SE

- Siemens AG

- GE Digital

- ABB Ltd

- Schneider Electric SE

- Intel Corporation

- Robert Bosch GmbH

- Accenture plc

- Honeywell International Inc.

- Hitachi Energy Ltd.

- Emerson Electric Co.

- Aspen Technology, Inc.

- AVEVA Group plc

- Uptake Technologies Inc.

- SparkCognition, Inc.

- Senseye Ltd.

- SKF Group

- Bentley Systems, Inc.

- Mitsubishi Electric Corporation

- Caterpillar Inc. (Asset Intelligence)

- DNV AS

- KONUX GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging energy infrastructure and grid reliability focus (mainstream)

- 4.2.2 Integration of IIoT, AI and big-data analytics (mainstream)

- 4.2.3 Cost pressure to cut unplanned downtime (mainstream)

- 4.2.4 Regulatory mandates on safety / emissions (mainstream)

- 4.2.5 Drone- and satellite-enabled remote sensing fusion (under-the-radar)

- 4.2.6 Digital-twin-driven risk-based maintenance (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 High upfront implementation and integration cost (mainstream)

- 4.3.2 Rising cyber-security vulnerabilities (mainstream)

- 4.3.3 Scarcity of energy-domain data-science talent (under-the-radar)

- 4.3.4 Data-ownership and liability disputes in multi-party assets (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, 2024-2030)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Software Platforms

- 5.1.1.2 Embedded Hardware and Sensors

- 5.1.2 Services

- 5.1.2.1 Integration and Implementation

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By End-user Industry

- 5.3.1 Power Generation (Thermal, Nuclear, Hydro)

- 5.3.2 Renewables (Wind, Solar, Storage)

- 5.3.3 Oil and Gas (Upstream, Mid, Downstream)

- 5.3.4 Utilities and TandD

- 5.3.5 Mining and Minerals

- 5.4 By Asset Type

- 5.4.1 Turbines and Rotating Equipment

- 5.4.2 Transformers and Sub-stations

- 5.4.3 Pipelines and Compressors

- 5.4.4 Pumps and Valves

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Siemens AG

- 6.4.4 GE Digital

- 6.4.5 ABB Ltd

- 6.4.6 Schneider Electric SE

- 6.4.7 Intel Corporation

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Accenture plc

- 6.4.10 Honeywell International Inc.

- 6.4.11 Hitachi Energy Ltd.

- 6.4.12 Emerson Electric Co.

- 6.4.13 Aspen Technology, Inc.

- 6.4.14 AVEVA Group plc

- 6.4.15 Uptake Technologies Inc.

- 6.4.16 SparkCognition, Inc.

- 6.4.17 Senseye Ltd.

- 6.4.18 SKF Group

- 6.4.19 Bentley Systems, Inc.

- 6.4.20 Mitsubishi Electric Corporation

- 6.4.21 Caterpillar Inc. (Asset Intelligence)

- 6.4.22 DNV AS

- 6.4.23 KONUX GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

製造业维护机器人市场:依产品、经营模式、部署方式、应用和产业划分-全球预测,2026-2032年

製造业维护机器人市场:依产品、经营模式、部署方式、应用和产业划分-全球预测,2026-2032年 预测性维护市场分析及至2035年预测:依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及设备划分

预测性维护市场分析及至2035年预测:依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及设备划分 全球预测性维护市场规模、份额、趋势和成长分析报告(2026-2034年)

全球预测性维护市场规模、份额、趋势和成长分析报告(2026-2034年) 全球半导体製造设备预测性维护市场:预测(至2034年)-按组件、类型、设备类型、部署方式、最终用户和地区分類的分析全球车辆生命週期最佳化平台市场:预测(至2034年)-依解决方案类型、部署方式、车辆类型、技术、应用、最终使用者和地区进行分析全球车辆生命週期预测工具市场预测(至2034年):按组件、部署类型、应用、最终用户和地区划分晶圆厂预测性维护:全球市场预测至2034年,按组件、部署模式、最终用户和地区划分

全球半导体製造设备预测性维护市场:预测(至2034年)-按组件、类型、设备类型、部署方式、最终用户和地区分類的分析全球车辆生命週期最佳化平台市场:预测(至2034年)-依解决方案类型、部署方式、车辆类型、技术、应用、最终使用者和地区进行分析全球车辆生命週期预测工具市场预测(至2034年):按组件、部署类型、应用、最终用户和地区划分晶圆厂预测性维护:全球市场预测至2034年,按组件、部署模式、最终用户和地区划分 预测性维护市场规模、份额和趋势分析报告:按组件、解决方案、服务、部署、公司规模、监控技术、最终用途、地区和细分市场预测(2026-2033 年)预测性维护市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)2032年能源基础设施市场预测:按解决方案类型、组件、基础设施类型、技术、最终用户和地区分類的全球分析

预测性维护市场规模、份额和趋势分析报告:按组件、解决方案、服务、部署、公司规模、监控技术、最终用途、地区和细分市场预测(2026-2033 年)预测性维护市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)2032年能源基础设施市场预测:按解决方案类型、组件、基础设施类型、技术、最终用户和地区分類的全球分析