|

市场调查报告书

商品编码

1851602

隔热涂料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Thermal Insulation Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

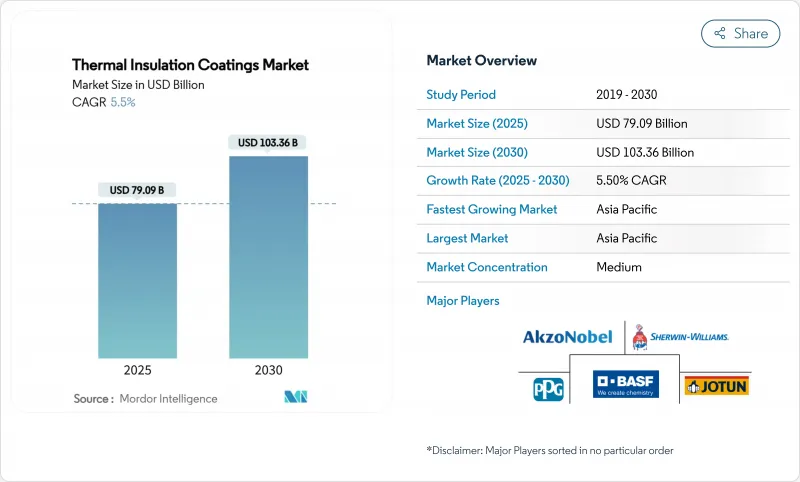

预计到 2025 年,隔热涂料市场规模将达到 790.9 亿美元,到 2030 年将达到 1,033.6 亿美元,预测期(2025-2030 年)复合年增长率为 5.5%。

这一优异表现表明,市场对高性能保温材料的需求将持续成长,远远超出传统建筑应用领域,涵盖电气化製程热系统、液化天然气基础设施和电池温度控管等。欧洲各地能源效率法规、脱碳需求以及第四代区域供热管网的建设,正在加速采用能够承受超过1200°C高温的先进隔热材料。同时,亚太地区的工业扩张正在扩大炼油厂、石化企业和汽车零件行业高性能涂料的基本客群,而北美的航太专案则推动了超高温钇安定氧化锆(YSZ)系统的应用。由此产生的竞争环境将使那些将垂直整合与材料科学进步相结合的供应商受益,例如,采用气凝胶-环氧树脂混合配方,实现低于0.020 W m-1 K-1的热导率。

全球隔热涂料市场趋势及洞察

新建炼油厂

全球炼油厂建设持续推动隔热涂料市场的发展。印度、中国和阿拉伯湾地区的新炼油厂在蒸馏塔和热交换器壳体上采用多层环氧树脂隔热层,工作温度介于200°C至800°C之间。计划业主越来越多地将防腐蚀和数位膜厚监测功能整合到同一涂层方案中,以减少非计划性停机并延长设备使用寿命。能够提供适用于常温和循环温度环境认证的供应商,正获得大量大型资本计划订单。

扩大区域供热和製冷网络

第四代区域供热製冷网路将在较低的供热温度下运行,因此需要使用能够承受反覆热循环并降低输送损耗的涂层。丹麦市政能源合作社已证明,先进的隔热材料可以将年度热损耗降低几个百分点,并提高热泵效率。德国和瑞典也正在进行类似的维修,使用气凝胶底漆,以满足更严格的隔热目标。

高额资金需求

等离子喷涂室、自动化龙门架和可控气氛固化炉造价数百万美元,限制了新进业者的产能。因此,大型综合製造商主导长期供应协议,而小型施用器则面临资金筹措难题。正如近期一家多元化化工集团内部的资产剥离讨论所表明的那样,资产组合重组凸显了资本密集型行业面临的压力。

细分市场分析

预计到2024年,环氧树脂体系将维持36.19%的隔热涂料市场份额,这主要得益于其优异的附着力和耐化学腐蚀性,尤其适用于炼油厂管路、船舶甲板和海上平台。这些产品将支撑亚太和中空地区规划中的防护衬里计划,占据隔热涂料市场的大部分份额。采用空心玻璃微球增强配方,可在不牺牲涂层韧性的前提下,达到0.180 W m-1 K-1或更低的导热係数。

目前二氧化硅气凝胶涂层的销售额仍处于个位数成长阶段,但预计到2030年将达到5.91%的复合年增长率。其0.015 W m⁻¹ K⁻¹的超低电导率使其能应用于以往需要真空绝热板的常压环境。透过将气凝胶粉末共分散在环氧树脂基体中,製造商将机械强度与近乎超高的绝缘性能相结合,进一步提升了该行业对未来技术规范的影响力。在航太领域,熵稳定氧化物和氧化钇稳定氧化锆(YSZ)平台正瞄准工作温度超过1200°C的涡轮叶片蒙皮,预示着技术交叉融合的更多机会。

到2024年,液态喷涂线将占据热障涂层市场45.19%的份额,继续以6.45%的复合年增长率领先其他喷涂方式。其主要优势在于能够无缝覆盖焊接和弯曲半径,并且由于整合了机器人喷头,生产速度得以提高。目前,加工厂正在部署视觉分析技术来测量湿膜厚度并自动校正喷枪速度,从而最大限度地减少过喷并提高产量比率。粉末喷涂线在网壳结构以外的区域以及某些利用静电吸引形成均匀涂层的管道中仍然具有应用价值。

隔热涂料市场报告按树脂类型(丙烯酸、环氧树脂、聚氨酯等)、涂料形式(液体喷涂、粉末、真空沉淀)、应用(建筑外墙、工业设备和管道、储存槽和容器等)、最终用户行业(建筑和施工、工业/製造、汽车等)和地区(亚太地区、北美、欧洲等)进行细分。

区域分析

亚太地区预计到2024年将占总收入的40.08%,这主要得益于中国、印度和韩国的计划储备。该地区各国政府正优先考虑炼油自给自足,直接推动了隔热涂料市场的发展。此外,日本的液化低温运输以及服务东南亚岛屿的浮体式储存再气化装置(FSRA)计画也正在加速推进。

北美地区得益于航太航太推进计画和重工业区製程热电气化试点计画的支持。联邦刺激计画鼓励社区进行节能维修,引导市政公用事业公司采用先进的覆层材料以减少输电损耗。诸如2020年加拿大建筑节能规范等法规提高了墙体结构的隔热要求,从而推动了喷涂陶瓷微球产品需求的成长。

欧洲在政策主导的脱碳领域持续保持领先地位,并占据了人口最密集的区域供热市场,这推动了经现场热循环耐久性检验的涂层不断升级。新建重工业设施的短缺使得人们的关注点转向对老旧工业园区维修,加装高温热泵系统,而涂层可以有效降低导热油迴路中的传导损失。同时,中东和非洲正利用石油资本投资计划,扩大石化工业的涂层应用;南美洲的矿区也开始采用涂层来保护製程容器免受腐蚀性酸和昼夜温差的影响。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新炼油厂的建设

- 扩大区域供热和製冷网络

- 建设产业需求增加

- 重工业製程热的电气化。

- 液化天然气低温运输物流快速成长

- 市场限制

- 高额资金需求

- 易挥发原料(环氧树脂和聚氨酯)价格

- 在高温资产中的适用性有限

- 供应链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依树脂类型

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 钇安定氧化锆(YSZ)

- 其他树脂类型(例如二氧化硅气凝胶基树脂等)

- 按涂层类型

- 液体喷雾

- 粉末

- 真空沉淀

- 透过使用

- 建筑物外墙(墙壁、屋顶)

- 工业设备和管道

- 储存槽和容器

- 汽车零件

- 船体外壳和甲板结构

- 航太和涡轮机零件

- 按最终用户行业划分

- 建筑/施工

- 工业/製造业

- 车

- 海洋

- 其他(食品加工、製药)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AkzoNobel NV

- BASF

- Behr Process LLC

- DAW SE

- Dow

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Mascoat

- Nippon Paint Holdings Co., Ltd

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International

- Sharpshell Engineering

- Sika AG

- Synavax

- The Sherwin-Williams Company

第七章 市场机会与未来展望

The Thermal Insulation Coatings Market size is estimated at USD 79.09 billion in 2025, and is expected to reach USD 103.36 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

This performance signals sustained demand that now stretches far beyond conventional construction use cases and into electrified process-heat systems, LNG infrastructure, and battery thermal management. Enforceable energy-efficiency codes, mounting decarbonization mandates, and the build-out of fourth-generation district-heating grids across Europe are accelerating the adoption of advanced thermal barriers capable of service temperatures above 1,200 °C. In parallel, Asia-Pacific's industrial expansion is widening the customer base for high-performance coatings in refineries, petrochemicals, and automotive components, while North American aerospace programs are stimulating uptake of ultra-high-temperature yttria-stabilized zirconia (YSZ) systems. The resulting competitive environment rewards suppliers that combine vertical integration with materials science advances, such as hybrid aerogel-epoxy formulations that deliver sub-0.020 W m-1 K-1 thermal conductivity.

Global Thermal Insulation Coatings Market Trends and Insights

Construction of New Refineries

Global refinery buildouts continue to anchor the thermal insulation coatings market. New complexes in India, China, and the Arabian Gulf specify multilayer epoxy barriers for distillation towers and heat-exchanger shells that run between 200 °C and 800 °C. Project owners increasingly bundle corrosion resistance and digital thickness monitoring into the same coating package to curb unplanned outages and extend asset life. Suppliers that can certify systems for both normal and cyclic temperature environments gain access to the largest capital projects pipeline.

Expansion of District Heating and Cooling Networks

Fourth-generation district-heating grids operate at lower supply temperatures, demanding coatings capable of reducing distribution losses while surviving repetitive thermal cycling. Denmark's municipal energy cooperatives demonstrate that advanced insulation can shave multiple percentage points from annual heat losses, thereby improving heat-pump efficiency. Similar retrofits across Germany and Sweden specify aerogel-infused primers to meet the stricter heat-retention targets.

High Capital Requirement

Plasma-spray booths, automated gantries, and controlled-atmosphere curing ovens can cost several million USD, limiting new-entrant capacity. Large integrated producers therefore dominate long-run supply contracts, while smaller applicators face financing hurdles. Portfolio restructuring, as seen in recent divestiture discussions inside diversified chemistry groups, underscores capital intensity pressures.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Construction Industry

- Electrification of Process-Heat in Heavy Industry

- Volatile Raw-Material (Epoxy and PU) Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy systems retained a 36.19% share of the thermal insulation coatings market in 2024, buoyed by strong adhesion and chemical resistance that suit refinery piping, marine deck plates, and offshore platforms. They underpin a significant portion of the thermal insulation coatings market size for protective-lining projects scheduled across APAC and the Middle East. Enhanced formulations embed hollow-glass microspheres to bring thermal conductivity below 0.180 W m-1 K-1 without sacrificing film toughness.

Silica-aerogel coatings, while holding only single-digit revenue today, record a 5.91% CAGR to 2030. Ultra-low conductivity readings of 0.015 W m-1 K-1 unlock ambient-pressure applications that once demanded vacuum-insulated panels. Manufacturers co-disperse aerogel powder into epoxy matrices to combine mechanical strength with near-super-insulating performance, giving the segment outsized influence on future specifications. At the aerospace frontier, entropy-stabilized oxide and YSZ platforms target turbine-blade skins running above 1,200 °C, suggesting further technology crossover opportunities.

Liquid spray lines captured 45.19% of thermal insulation coatings market share in 2024 and continue to outpace other forms at a 6.45% CAGR. Their chief advantages include seamless coverage on weld seams and radius bends, plus production-rate gains from robot-integrated spray heads. Process yards now deploy vision analytics to gauge wet-film thickness and self-correct gun speed, minimizing overspray and improving yield. Powder lines remain relevant in gridshell architecture and certain pipeline externals where electrostatic attraction ensures uniform film builds.

The Thermal Insulation Coatings Market Report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, and More), Coating Form (Liquid Spray, Powder, Vacuum-Deposited), Application (Building Envelope, Industrial Equipment and Pipelines, Storage Tanks and Vessels, and More), End-User Industry (Building and Construction, Industrial/Manufacturing, Automotive, and More), and Geography (Asia Pacific, North America, Europe, and More).

Geography Analysis

Asia-Pacific holds 40.08% of 2024 revenue, reflecting megaproject pipelines in China, India, and South Korea. Regional governments prioritize refinery self-sufficiency, which directly inflates the thermal insulation coatings market. Added momentum comes from LNG cold-chain terminals in Japan and floating storage regasification units serving Southeast Asian islands.

North America is assisted by aerospace propulsion programs and process-heat electrification pilots in heavy industry alleys. Federal stimulus packages encourage district-energy retrofits, steering municipal utilities toward advanced coating overlays that lower distribution losses. Regulations like Canada's National Energy Code for Buildings 2020, which lifts thermal-resistance requirements for wall assemblies, anchor recurrent demand for spray-applied ceramic microsphere products.

Europe maintains leadership in policy-driven decarbonization and commands the densest district-heating market, fostering continuous specification upgrades for coatings with validated ex-situ thermal-cycling endurance. Scarcity of new-build heavy industry shifts focus to retrofitting aging industrial parks with high-temperature heat-pump systems, where coatings moderate conductive losses on hot-oil loops. Meanwhile, the Middle-East and Africa leverages oil-capex programs to expand adoption in petrochemical parks, whereas South America's mining belts employ coatings to buffer process vessels against aggressive acids and wide daily temperature swings.

- AkzoNobel N.V.

- BASF

- Behr Process LLC

- DAW SE

- Dow

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd

- Mascoat

- Nippon Paint Holdings Co., Ltd

- OC Oerlikon Management AG

- PPG Industries, Inc.

- RPM International

- Sharpshell Engineering

- Sika AG

- Synavax

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction of New Refineries

- 4.2.2 Expansion of District Heating and Cooling Networks

- 4.2.3 Increasing demand for the construction industry

- 4.2.4 Electrification of Process-Heat in Heavy Industry

- 4.2.5 Surge in LNG Cold-Chain Logistics

- 4.3 Market Restraints

- 4.3.1 High Capital Requirement

- 4.3.2 Volatile Raw-Material (Epoxy and PU) Prices

- 4.3.3 Limited Applicability in Ultra High Temperature Assets

- 4.4 Supply Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Yttria-Stabilised Zirconia (YSZ)

- 5.1.5 Other Resin Types (Silica Aerogel-Based, etc.)

- 5.2 By Coating Form

- 5.2.1 Liquid Spray

- 5.2.2 Powder

- 5.2.3 Vacuum-Deposited

- 5.3 By Application

- 5.3.1 Building Envelope (Walls, Roofs)

- 5.3.2 Industrial Equipment and Pipelines

- 5.3.3 Storage Tanks and Vessels

- 5.3.4 Automotive Components

- 5.3.5 Marine Hull and Deck Structures

- 5.3.6 Aerospace and Turbine Parts

- 5.4 By End-user Industry

- 5.4.1 Building and Construction

- 5.4.2 Industrial/Manufacturing

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Others (Food Processing, Pharma)

- 5.5 By Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 BASF

- 6.4.3 Behr Process LLC

- 6.4.4 DAW SE

- 6.4.5 Dow

- 6.4.6 Evonik Industries AG

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 Kansai Paint Co., Ltd

- 6.4.10 Mascoat

- 6.4.11 Nippon Paint Holdings Co., Ltd

- 6.4.12 OC Oerlikon Management AG

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International

- 6.4.15 Sharpshell Engineering

- 6.4.16 Sika AG

- 6.4.17 Synavax

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球耐热阻隔涂层市场规模、份额、趋势和成长分析报告(2026-2034年)

全球耐热阻隔涂层市场规模、份额、趋势和成长分析报告(2026-2034年) 隔热涂布市场-全球产业规模、份额、趋势、机会、预测:按产品、最终用户产业、地区和竞争对手划分,2021-2031年

隔热涂布市场-全球产业规模、份额、趋势、机会、预测:按产品、最终用户产业、地区和竞争对手划分,2021-2031年 全球防风雨涂料市场:按技术、涂料类型、应用、最终用户和分销管道分類的预测(2026-2032 年)

全球防风雨涂料市场:按技术、涂料类型、应用、最终用户和分销管道分類的预测(2026-2032 年) 隔热市场规模、份额和成长分析(按产品、技术、涂层组合、应用和地区划分)—产业预测(2026-2033 年)

隔热市场规模、份额和成长分析(按产品、技术、涂层组合、应用和地区划分)—产业预测(2026-2033 年) 奈米多孔隔热膜市场预测至2032年:按材料、製造流程、最终用户和地区分類的全球分析

奈米多孔隔热膜市场预测至2032年:按材料、製造流程、最终用户和地区分類的全球分析 全球隔热涂料市场占有率及排名、总收入及需求预测(2025-2031年)2032 年隔热涂层市场预测:按产品类型、涂层材料、技术、应用、最终用户和地区进行的全球分析

全球隔热涂料市场占有率及排名、总收入及需求预测(2025-2031年)2032 年隔热涂层市场预测:按产品类型、涂层材料、技术、应用、最终用户和地区进行的全球分析 隔热涂层:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)隔热涂层市场(材料类型、技术、应用和地区)2026-2032

隔热涂层:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)隔热涂层市场(材料类型、技术、应用和地区)2026-2032 隔热涂层市场:依产品类型、涂层材料、技术、应用和地区划分

隔热涂层市场:依产品类型、涂层材料、技术、应用和地区划分