|

市场调查报告书

商品编码

1851729

Wi-Fi 分析:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Wi-Fi Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

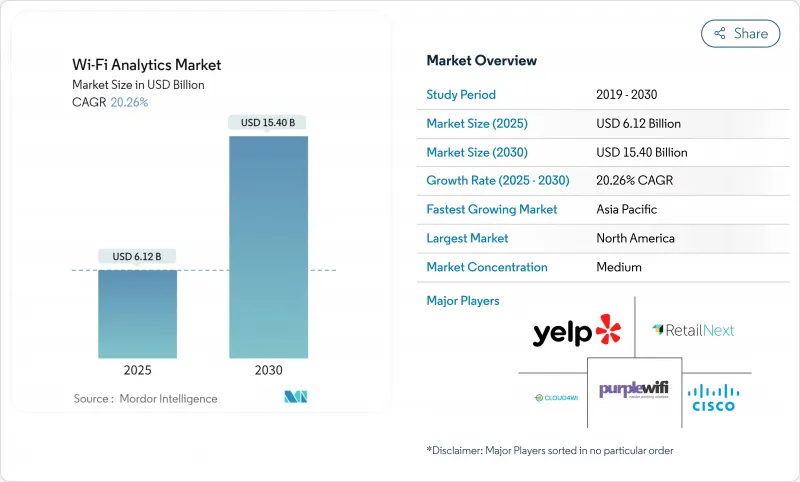

预计到 2025 年,Wi-Fi 分析市场将创造 61.2 亿美元的收入,到 2030 年将达到 154 亿美元。

如今,企业不再将网路基地台视为基本的连接工具,而是将其视为驱动即时决策的资料撷取资产。 Wi-Fi 7 的商业化推广、6 GHz 频段存取的增加以及边缘人工智慧在网路基地台的广泛应用,都将推动市场需求。虽然酒店业仍然是最大的用户群体,但零售业的快速成长表明,实体零售商正在将位置资讯转化为竞争优势。云端部署占据主导地位,因为企业倾向于采用订阅模式,这种模式允许他们在无需大量资本支出的情况下实现规模化扩展。

全球Wi-Fi分析市场趋势与洞察

智慧型手机和智慧型装置的普及速度正在迅速提升

到2024年,将有超过211亿台Wi-Fi设备处于活跃状态,其中Wi-Fi 6E和Wi-Fi 7设备的出货量分别为5.762亿台和2.314亿台。如今,每个连网使用者都携带多台设备,从而能够更丰富地分析跨会话行为。企业可以利用这个高密度的Wi-Fi网络,将匿名的客流量资料转换为分层的客户旅程地图,以提高转换率并延长顾客停留时间。零售连锁店透过将店内热力图与设备类型关联起来,可以更精准地分配员工和促销,增加客单价,并减少缺货情况。人工智慧也反映了这一趋势,随着样本量的成长,预测模型得到增强,能够提前几分钟预测排队状况和顾客对产品的兴趣变化。

实体场所中公共 Wi-Fi 的快速普及

体育场馆、机场和购物中心已将Wi-Fi从成本中心转变为收入引擎。 Extreme Networks目前为25个NFL球场提供分析支持,将球迷动向转化为即时互动队伍。 TD花园球馆的访客平台展示了无缝登入如何提高使用者选择加入率和第一方资料收集量。交通运输机构利用停留时间指标重新定位特许经营摊位,速食店则升级网路基地台,向管理人员推送排队长度警报。新兴趋势是将首页同意资讯与会员ID关联起来,建立持久的使用者画像,并将这些画像延伸到场馆以外的全通路行销。

严格的隐私权法规(GDPR、CCPA 等)

巨额罚款迫使营运商重新思考其使用者许可流程,增设资料保护负责人,并进行定期审核,这可能会使部署预算增加 15% 至 20%。像 Purple 这样的公司正在转向使用明确的使用者帐户和细粒度的许可日誌,以满足 GDPR 的要求。一些公司现在正在晶片层级对探测请求资料进行匿名化处理,用聚合密度图取代单一路径。随着企业寻求合规保证,那些将隐私保护放在首位的供应商正在赢得竞标。

细分市场分析

解决方案仍将占据主导地位,预计到 2024 年将占 Wi-Fi 分析市场份额的 56.5%。然而,受市场对即用型洞察而非 DIY 仪錶板的需求驱动,服务将以 21.4% 的复合年增长率 (CAGR) 超越市场整体成长速度。企业正将分析解读、隐私管治和跨系统整合等工作外包给专家,从而减少内部工作量并加快价值实现速度。

预计2025年至2030年间,Wi-Fi分析服务市场规模将成长一倍以上,因为供应商会将咨询、託管营运和基于结果的定价模式捆绑在一起。 RetailNext从Battery Ventures资金筹措进一步巩固了投资者对分析即服务模式将推动未来成长的信心。 Cloud4Wi的Fogsense微型设备展示了服务公司如何缩小硬体占用空间,并将价值向上游转移至业务层面。

到2024年,云端平台将占据Wi-Fi分析市场62.9%的份额,预计该细分市场将以21.8%的复合年增长率成长。订阅模式无需资本支出,并提供弹性储存和当日更新的AI功能。过去缺乏内部IT人员的中小型零售商现在可以在数小时内完成部署,从而释放先前閒置的网路数据。

思科的AI原生Wi-Fi 7网路基地台可在本地处理遥测数据,并将摘要同步到云端。在国防、医疗保健和金融机构等仍采用自主託管和传统架构的行业,本地部署仍然至关重要。

区域分析

到2024年,北美将占全球收入的31.2%,这主要得益于企业早期采用以及隐私和分析之间成熟的监管平衡。 Extreme Networks的高密度Wi-Fi最佳实践已在25个NFL体育场部署,便是典型例证。智慧型手机的高普及率和强大的云端基础设施为平台的持续升级提供了可能。

亚太地区是成长最快的地区,预计到2030年复合年增长率将达到20.5%。中国拥有约4,000家私人无线工厂,为进行细緻分析提供了基础;而印度计画分配的6GHz频谱预计在2034年前释放4.03兆美元的经济价值。快速的都市化和政府的公共数位化政策正在推动无线技术在交通枢纽、购物中心和智慧校园等场所的部署。

在欧洲,GDPR将催生以隐私为主导的模式,并指导平台设计。能够获得用户同意并匿名化数据的营运商将享有先发优势。在德国,一家大型零售连锁店正严格遵守相关规定,将访客Wi-Fi与其忠诚度计画关联起来;英国火车站的公共Wi-Fi倡议则展示了在全国范围内进行高流量分析的能力。边缘部署降低了云端存取成本,并符合当地的永续性目标。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧型手机和智慧型装置的快速普及

- 实体场所中公共 Wi-Fi 的快速普及

- 零售和餐旅服务业对即时客户体验个人化的需求

- AI/ML引擎与Wi-Fi分析平台的集成

- 采用Wi-Fi RTT进行亚米级室内定位

- 基于边缘运算的存取点分析可降低整体拥有成本

- 市场限制

- 严格的隐私权法规(GDPR、CCPA 等)

- 持续存在的网路层级安全漏洞

- MAC位址随机化会影响资料准确性

- 高密度区域的频谱壅塞

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 评估市场的宏观经济因素

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 透过部署

- 本地部署

- 云

- 透过使用

- 存在分析

- 市场分析

- 按最终用户行业划分

- 零售

- 饭店业

- 运动与休閒

- 运输

- 卫生保健

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cisco Systems Inc.

- Cloud4Wi Inc.

- Purple WiFi Ltd

- RetailNext Inc.

- Yelp WiFi Inc.

- CommScope Inc.(Ruckus Wireless)

- Fortinet Inc.

- Blix Inc.

- Skyfii Limited

- Singtel Optus Pty Ltd

- MetTel Inc.

- Hewlett Packard Enterprise(Aruba Networks)

- Extreme Networks Inc.

- Cambium Networks Ltd

- Ubiquiti Inc.

- Aislelabs Inc.

- Plume Design Inc.

- Euclid Analytics

- Near Intelligence Holdings

- Mist Systems(Juniper Networks)

- Cloud5 Communications

- Datavalet Technologies Inc.

- GoZone WiFi LLC

第七章 市场机会与未来展望

The Wi-Fi analytics market generated USD 6.12 billion in 2025 and is on track to reach USD 15.40 billion by 2030, reflecting a 20.26% CAGR.

Enterprises now treat access points as data-collection assets that fuel real-time decision making, rather than as basic connectivity tools. Commercial roll-outs of Wi-Fi 7, wider 6 GHz spectrum access, and the spread of edge AI in access points amplify demand. Hospitality remains the largest user group, while retail's fast climb shows how brick-and-mortar operators are turning location data into a competitive advantage. Cloud deployment rules the landscape as companies favor subscription models that scale without heavy capital expense.

Global Wi-Fi Analytics Market Trends and Insights

Surging Smartphone and Smart-Device Penetration

More than 21.1 billion Wi-Fi devices were active in 2024, with 576.2 million Wi-Fi 6E and 231.4 million Wi-Fi 7 units shipped during the year. Each connected user now carries multiple devices, enabling richer cross-session behavioral profiles. Enterprises that harness this density translate anonymous foot-traffic counts into layered customer-journey maps, improving conversion and dwell time. Retail chains that correlate device classes with in-store heatmaps allocate associates and promotions more precisely, raising basket size and reducing stock-outs. The trend strengthens predictive modeling accuracy as sample sizes grow, feeding AI that anticipates queue build-ups or product interest shifts minutes ahead of time.

Rapid Rollout of Public Wi-Fi in Physical Venues

Stadiums, airports, and malls moved Wi-Fi from cost center to revenue engine. Extreme Networks now supports analytics at 25 NFL stadiums, turning fan movement into real-time engagement cues. TD Garden's guest platform shows how seamless log-in increases opted-in first-party data capture. Transport hubs use dwell metrics to reshape concession placement, while quick-service restaurants upgrade access points to push queue-length alerts to managers. The emerging norm links splash-page consent with loyalty IDs, building persistent profiles that extend beyond venue walls into omnichannel marketing.

Stringent Privacy Regulations (GDPR, CCPA, etc.)

Hefty fines push operators to overhaul consent flows, add data-protection officers, and run routine audits that can add 15-20% to deployment budgets. Firms such as Purple pivoted to explicit user accounts and granular consent logs that meet GDPR demands. Some venues now anonymize probe-request data at the chip level, trading individual paths for aggregated density maps. Vendors that bake privacy first in their design win bids as enterprises seek compliance assurance.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Real-Time Customer Experience Personalisation

- Integration of AI/ML Engines with Wi-Fi Analytics Platforms

- MAC-Address Randomization Impacting Data Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions continued to dominate, holding 56.5% of the Wi-Fi analytics market share in 2024. However, services are outpacing at 21.4% CAGR, driven by demand for turnkey insight rather than do-it-yourself dashboards. Enterprises outsource analytics interpretation, privacy governance, and cross-system integration to specialists, lowering internal workloads while compressing time-to-value.

The Wi-Fi analytics market size for services is anticipated to more than double between 2025 and 2030 as vendors bundle consulting, managed operations, and outcome-based pricing. RetailNext's fresh funding from Battery Ventures underscores investor belief that analytics-as-a-service will underpin future growth. Cloud4Wi's Fogsense micro-device shows how service firms shrink hardware footprints and shift value upstream to business context.

Cloud platforms controlled 62.9% of the Wi-Fi analytics market share in 2024, and the segment is forecast to advance at a 21.8% CAGR. Subscription models eliminate capex and provide elastic storage plus AI updates on release day. Small and midsize retailers that once lacked internal IT staff now deploy within hours, unlocking network data that previously sat idle.

Edge compute addresses latency and data-sovereignty concerns; Cisco's AI-native Wi-Fi 7 access points process telemetry locally while syncing summaries to the cloud.On-premise remains relevant in defense, healthcare, and financial institutions where sovereign hosting or legacy architectures persist.

Wi-Fi Analytics Market Report is Segmented by Component (Solutions, Services), Deployment (On-Premise, Cloud), Application (Presence Analytics, Marketing Analytics), End-User Vertical (Retail, Hospitality, Sports and Leisure, Transportation, Healthcare and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

North America accounted for 31.2% of global revenue in 2024, driven by early enterprise adoption and mature regulatory balance between privacy and analytics. Flagship examples include Extreme Networks' deployments across 25 NFL stadiums that demonstrate best practices in high-density Wi-Fi. High smartphone penetration and robust cloud infrastructure sustain continuous platform upgrades.

Asia-Pacific is the fastest expanding region, growing at a 20.5% CAGR through 2030. China hosts about 4,000 private wireless factories that lay groundwork for granular analytics, while India's prospective 6 GHz allocation could unlock USD 4,030 billion in economic value by 2034. Rapid urbanisation and government digital-in-public policies spur deployments across transport hubs, malls, and smart campuses.

Europe presents a privacy-led model where GDPR dictates platform design. Operators that secure user consent and anonymise data gain first-mover advantage. Germany leads with large retail chains linking guest Wi-Fi to loyalty programs under strict compliance, and the United Kingdom's public Wi-Fi initiatives in rail stations illustrate high-traffic analytics at national scale. Edge-enabled deployments lower cloud egress costs and align with the region's sustainability targets.

- Cisco Systems Inc.

- Cloud4Wi Inc.

- Purple WiFi Ltd

- RetailNext Inc.

- Yelp WiFi Inc.

- CommScope Inc. (Ruckus Wireless)

- Fortinet Inc.

- Blix Inc.

- Skyfii Limited

- Singtel Optus Pty Ltd

- MetTel Inc.

- Hewlett Packard Enterprise (Aruba Networks)

- Extreme Networks Inc.

- Cambium Networks Ltd

- Ubiquiti Inc.

- Aislelabs Inc.

- Plume Design Inc.

- Euclid Analytics

- Near Intelligence Holdings

- Mist Systems (Juniper Networks)

- Cloud5 Communications

- Datavalet Technologies Inc.

- GoZone WiFi LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging smartphone and smart-device penetration

- 4.2.2 Rapid rollout of public Wi-Fi in physical venues

- 4.2.3 Demand for real-time CX personalisation in retail and hospitality

- 4.2.4 Integration of AI/ML engines with Wi-Fi analytics platforms

- 4.2.5 Adoption of Wi-Fi RTT for sub-meter indoor positioning

- 4.2.6 Edge-based analytics on access points lowering TCO

- 4.3 Market Restraints

- 4.3.1 Stringent privacy regulations (GDPR, CCPA, etc.)

- 4.3.2 Persistent network-level security vulnerabilities

- 4.3.3 MAC-address randomisation impacting data accuracy

- 4.3.4 Spectrum congestion in high-density locations

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Application

- 5.3.1 Presence Analytics

- 5.3.2 Marketing Analytics

- 5.4 By End-user Vertical

- 5.4.1 Retail

- 5.4.2 Hospitality

- 5.4.3 Sports and Leisure

- 5.4.4 Transportation

- 5.4.5 Healthcare

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Cloud4Wi Inc.

- 6.4.3 Purple WiFi Ltd

- 6.4.4 RetailNext Inc.

- 6.4.5 Yelp WiFi Inc.

- 6.4.6 CommScope Inc. (Ruckus Wireless)

- 6.4.7 Fortinet Inc.

- 6.4.8 Blix Inc.

- 6.4.9 Skyfii Limited

- 6.4.10 Singtel Optus Pty Ltd

- 6.4.11 MetTel Inc.

- 6.4.12 Hewlett Packard Enterprise (Aruba Networks)

- 6.4.13 Extreme Networks Inc.

- 6.4.14 Cambium Networks Ltd

- 6.4.15 Ubiquiti Inc.

- 6.4.16 Aislelabs Inc.

- 6.4.17 Plume Design Inc.

- 6.4.18 Euclid Analytics

- 6.4.19 Near Intelligence Holdings

- 6.4.20 Mist Systems (Juniper Networks)

- 6.4.21 Cloud5 Communications

- 6.4.22 Datavalet Technologies Inc.

- 6.4.23 GoZone WiFi LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

Wi-Fi 分析市场:按部署类型、组件、应用程式和最终用户产业划分-2026-2032 年全球市场预测

Wi-Fi 分析市场:按部署类型、组件、应用程式和最终用户产业划分-2026-2032 年全球市场预测 宽频测试工具市场预测至2034年-按组件、类型、测试类型、部署模式、技术、最终用户和地区分類的全球分析

宽频测试工具市场预测至2034年-按组件、类型、测试类型、部署模式、技术、最终用户和地区分類的全球分析 2026年全球Wi-Fi分析市场报告

2026年全球Wi-Fi分析市场报告 Wi-Fi 分析市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署类型、位置、垂直产业、地区和竞争格局划分,2021-2031 年)

Wi-Fi 分析市场 - 全球产业规模、份额、趋势、机会及预测(按组件、部署类型、位置、垂直产业、地区和竞争格局划分,2021-2031 年) Wi-Fi 分析市场规模、份额和成长分析(按组件、类型、部署类型、应用、最终用户和地区划分)—2026-2033 年行业预测

Wi-Fi 分析市场规模、份额和成长分析(按组件、类型、部署类型、应用、最终用户和地区划分)—2026-2033 年行业预测 2025 年至 2033 年 Wi-Fi 分析市场规模、份额、趋势及预测(按组件、部署、应用、行业垂直和地区划分)

2025 年至 2033 年 Wi-Fi 分析市场规模、份额、趋势及预测(按组件、部署、应用、行业垂直和地区划分) Wi-Fi 分析市场:成长、未来前景、竞争分析,2024-2032 年

Wi-Fi 分析市场:成长、未来前景、竞争分析,2024-2032 年